MARKET INSIGHTS

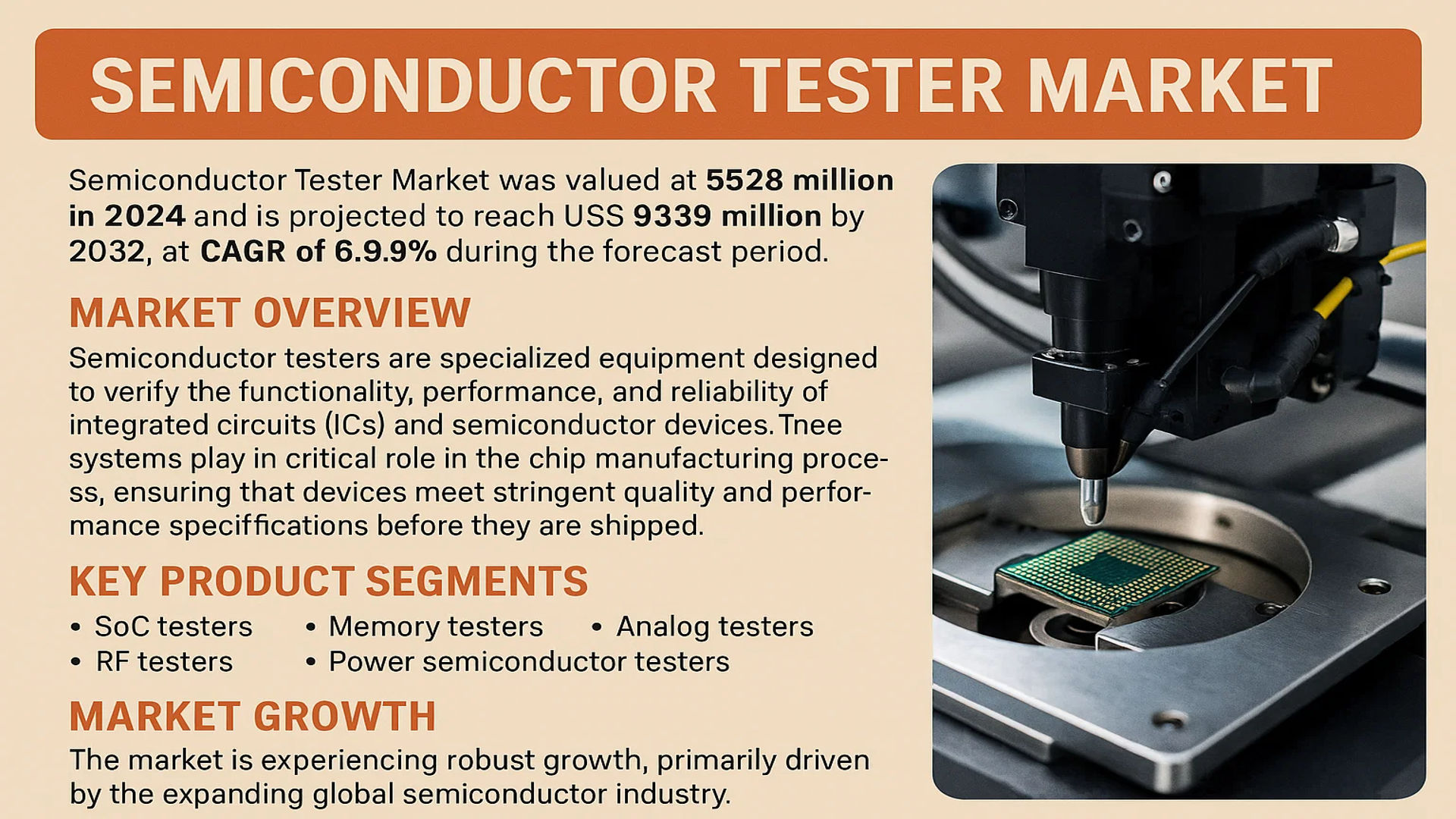

The global Semiconductor Tester Market was valued at 5528 million in 2024 and is projected to reach US$ 9339 million by 2032, at a CAGR of 6.9% during the forecast period.

Semiconductor testers are specialized equipment designed to verify the functionality, performance, and reliability of integrated circuits (ICs) and semiconductor devices. These systems play a critical role in the chip manufacturing process, ensuring that devices meet stringent quality and performance specifications before they are shipped. The market encompasses several key product segments, including SoC testers, memory testers, RF testers, analog testers, and power semiconductor testers, each tailored to specific device types and testing requirements.

The market is experiencing robust growth, primarily driven by the expanding global semiconductor industry. This expansion is fueled by rising demand from key end-use sectors such as smart terminals, autonomous vehicles, artificial intelligence (AI) computing, 5G/6G communications infrastructure, data centers, and the Internet of Things (IoT). As chip complexity increases and production volumes rise, the demand for sophisticated, high-throughput testing solutions becomes more critical. Furthermore, the market is evolving towards faster, more accurate, smarter, and more automated testing equipment to keep pace with advancements in semiconductor technology.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of Advanced Semiconductor Applications to Accelerate Market Expansion

The global semiconductor tester market is experiencing robust growth driven by the proliferation of advanced semiconductor applications across multiple industries. The increasing adoption of artificial intelligence, machine learning, and high-performance computing has created unprecedented demand for sophisticated testing solutions. Semiconductor testers are essential for ensuring the reliability and performance of complex integrated circuits used in data centers, which are projected to require testing equipment capable of handling chips with over 100 billion transistors. The automotive sector’s transition toward electric and autonomous vehicles further amplifies this demand, with modern vehicles containing approximately 1,400 to 1,500 semiconductor chips that require comprehensive testing for safety-critical applications. This expansion across multiple high-growth sectors creates a sustained upward trajectory for semiconductor testing equipment manufacturers.

5G/6G Infrastructure Deployment and IoT Expansion to Fuel Market Growth

The global rollout of 5G infrastructure and ongoing research in 6G technology represents a significant growth driver for the semiconductor tester market. 5G networks require sophisticated radio frequency (RF) semiconductors that demand specialized testing equipment to ensure signal integrity and compliance with international standards. The massive increase in connected devices through Internet of Things (IoT) applications further amplifies this demand, with projections indicating over 29 billion connected devices by 2030. This connectivity explosion requires semiconductor testers capable of handling the diverse requirements of low-power IoT chips, high-frequency RF components, and complex system-on-chip (SoC) designs. The convergence of these technological trends creates a compound growth effect, driving both volume and sophistication requirements in the semiconductor testing equipment market.

Memory Technology Advancements and Storage Demand to Stimulate Tester Market

Advancements in memory technology and exploding data storage requirements are creating substantial opportunities for memory tester manufacturers. The transition to DDR5 memory technology and the development of advanced 3D NAND flash memory require sophisticated testing equipment capable of validating performance at unprecedented speeds and densities. The global datasphere is projected to grow to over 175 zettabytes by 2025, driving demand for storage solutions that depend on rigorously tested semiconductor components. High-bandwidth memory (HBM) implementations in AI accelerators and graphics processing units represent another growth vector, requiring test systems that can validate performance under extreme thermal and electrical conditions. These technological advancements in memory architecture directly translate to increased complexity and cost of testing equipment, driving market value expansion.

MARKET CHALLENGES

Rising Complexity of Semiconductor Designs to Increase Testing Challenges

The semiconductor tester market faces significant challenges due to the escalating complexity of modern chip designs. As semiconductor technology advances toward smaller process nodes below 5 nanometers, testing requirements become exponentially more complex and expensive. The development of advanced packaging technologies such as 2.5D and 3D integration creates additional testing hurdles, requiring equipment capable of validating interconnects and thermal performance across multiple die stacks. This complexity drives up development costs for new testing systems, with leading-edge semiconductor testers now representing investments exceeding 25 million dollars per system. The time required to develop and validate new testing methodologies for cutting-edge semiconductor technologies has also increased, creating potential bottlenecks in the adoption of new semiconductor manufacturing processes.

Other Challenges

Technical Expertise Shortage

The semiconductor testing industry faces a critical shortage of technical expertise capable of developing and operating advanced testing systems. The convergence of multiple engineering disciplines including high-frequency electronics, thermal management, and sophisticated software algorithms requires multidisciplinary teams that are in short supply globally. This skills gap is particularly acute in emerging semiconductor manufacturing regions, where experienced test engineers and application specialists are difficult to recruit and retain. The retirement of experienced professionals from established semiconductor companies further exacerbates this challenge, creating knowledge transfer issues that impact the entire testing ecosystem.

Supply Chain Constraints

Global supply chain disruptions continue to challenge semiconductor tester manufacturers, affecting both component availability and delivery timelines. Critical components such as high-performance analog instruments, precision mechanical systems, and specialized computing hardware face extended lead times ranging from 40 to 60 weeks. These constraints impact the ability of testing equipment manufacturers to respond quickly to market demand fluctuations, particularly during periods of rapid semiconductor industry expansion. The geographical concentration of certain component manufacturers creates additional vulnerability to regional disruptions, whether from natural disasters, trade restrictions, or other unforeseen events.

MARKET RESTRAINTS

High Capital Investment Requirements to Limit Market Penetration

The semiconductor tester market faces significant restraints due to the substantial capital investment required for advanced testing equipment. Modern semiconductor test systems represent major financial commitments, with prices for comprehensive testing solutions ranging from 15 million to over 30 million dollars depending on capabilities and configuration. This high entry barrier particularly affects smaller semiconductor design houses and emerging foundries that may lack the financial resources to invest in state-of-the-art testing infrastructure. The total cost of ownership extends beyond initial acquisition, including maintenance contracts, calibration services, and periodic upgrades that can add 15-20% annually to the operational expenses. These financial considerations create a natural segmentation in the market, where only the largest semiconductor manufacturers can afford the most advanced testing capabilities.

Cyclical Nature of Semiconductor Industry to Create Demand Volatility

The inherent cyclicality of the semiconductor industry presents a significant restraint for testing equipment manufacturers. Historical patterns show that semiconductor capital equipment spending fluctuates dramatically based on global economic conditions, inventory levels, and end-market demand. During industry downturns, semiconductor manufacturers typically delay or cancel equipment purchases, including testing systems, to preserve cash flow and adjust to reduced capacity utilization. This volatility creates challenges for testing equipment companies in maintaining consistent revenue streams and planning long-term research and development investments. The memory segment particularly exhibits pronounced cyclical behavior, with periods of oversupply leading to extended pauses in testing equipment procurement that can last multiple quarters.

Technological Obsolescence Risk to Deter Investment Decisions

Rapid technological evolution in semiconductor manufacturing creates significant obsolescence risks for testing equipment investments. The pace of innovation in semiconductor process technology means that testing systems may become inadequate for new manufacturing nodes within 3-4 years of purchase. This accelerated obsolescence cycle creates hesitation among potential buyers concerned about the longevity of their capital investments. The development of new packaging technologies, emerging materials, and novel transistor architectures further compounds this challenge, requiring testing equipment that can adapt to rapidly changing requirements. This dynamic creates a cautious approach to capital expenditure decisions, particularly among smaller market participants who must carefully balance performance requirements against financial sustainability.

MARKET OPPORTUNITIES

Emerging Domestic Semiconductor Ecosystems to Create New Market Opportunities

The global semiconductor industry is experiencing a significant geographical diversification, with multiple countries establishing domestic semiconductor manufacturing capabilities. This trend creates substantial opportunities for testing equipment manufacturers to serve emerging semiconductor ecosystems. National initiatives across various regions are driving investments in semiconductor infrastructure totaling over 500 billion dollars in committed funding through 2030. These new manufacturing facilities require comprehensive testing capabilities across all semiconductor segments, from basic power devices to advanced computing chips. The establishment of these new semiconductor clusters represents not only immediate equipment sales opportunities but also long-term service and support revenue streams as these facilities ramp production and expand capabilities.

Artificial Intelligence Integration in Test Systems to Enable Efficiency Improvements

The integration of artificial intelligence and machine learning technologies into semiconductor test systems represents a significant opportunity for market expansion. AI-enhanced testing solutions can dramatically improve test efficiency, reduce testing time, and enhance fault detection capabilities. Advanced algorithms can optimize test patterns, predict potential failures, and adapt testing parameters in real-time based on device performance characteristics. This intelligence integration allows semiconductor manufacturers to achieve higher throughput while maintaining or improving test coverage, particularly important for complex devices where testing time represents a substantial portion of total manufacturing cost. The implementation of these AI-driven testing methodologies can reduce overall test time by 25-40% while improving defect detection rates by similar percentages.

Advanced Packaging Technologies to Drive Testing Innovation Requirements

The rapid adoption of advanced packaging technologies including heterogeneous integration, chiplet architectures, and 3D stacking creates substantial opportunities for testing equipment innovation. These packaging approaches require new testing methodologies that can validate performance across multiple die, through-silicon vias, and complex interconnect structures. The market for advanced packaging is projected to grow at approximately 14% annually, driven by performance requirements that cannot be met through traditional monolithic semiconductor approaches. This growth creates demand for testing systems capable of handling the unique challenges of multi-die packages, including thermal management validation, interconnect integrity testing, and system-level performance verification. Equipment manufacturers that can develop comprehensive testing solutions for these advanced packaging platforms stand to capture significant market share in this high-growth segment.

SEMICONDUCTOR TESTER MARKET TRENDS

Integration of AI and Machine Learning to Emerge as a Pivotal Trend

The global semiconductor tester market is witnessing a transformative shift with the deep integration of Artificial Intelligence (AI) and Machine Learning (ML) into test systems. This integration is fundamentally altering test methodologies by enabling predictive maintenance, adaptive test patterns, and significant yield optimization. AI algorithms can analyze vast datasets from previous test runs to identify subtle patterns and potential failure points that are imperceptible to traditional methods, thereby enhancing fault coverage and reducing test escape rates. Furthermore, ML-driven systems are capable of self-optimizing test parameters in real-time, which drastically cuts down test time and operational costs. This trend is particularly critical for testing complex System-on-Chip (SoC) and advanced memory devices, where the sheer number of test vectors can be overwhelming. The move towards AI is not just an incremental improvement but a fundamental re-engineering of the test process, making it smarter, faster, and more cost-effective, which is essential to keep pace with the demanding production cycles of next-generation semiconductors.

Other Trends

Demand Surge from Advanced Packaging and Heterogeneous Integration

The rapid adoption of advanced packaging technologies like 2.5D/3D IC packaging and heterogeneous integration is creating substantial new demand for sophisticated test solutions. These complex architectures, which combine multiple die—often from different process technologies—into a single package, present unique testing challenges that go beyond traditional methodologies. Testers must now handle increased pin counts, higher bandwidth requirements, and manage intricate interactions between disparate components. This has led to a growing need for test equipment capable of performing known-good-die (KGD) testing and system-level test (SLT) to ensure final package reliability. The market for testers serving this segment is expanding rapidly because these advanced packages are foundational to high-performance computing, artificial intelligence accelerators, and premium consumer electronics, where failure rates must be kept exceptionally low.

Expansion Driven by Automotive and Industrial IoT Applications

The relentless growth of the automotive electronics and Industrial Internet of Things (IIoT) sectors is acting as a powerful catalyst for the semiconductor tester market. Semiconductors used in these fields must operate with extreme reliability under harsh environmental conditions and have much longer lifecycles than consumer electronics. This necessitates rigorous and comprehensive testing protocols, often requiring extended temperature cycling, high-voltage stress tests, and enhanced functional safety validation. The automotive sector’s push towards electrification and autonomous driving, in particular, relies on a massive increase in sensor, power management, and processing chips, each requiring validation. Similarly, IIoT applications demand robust, low-power chips that must be thoroughly vetted for long-term deployment in industrial settings. This focus on quality and reliability over pure cost is driving investment in advanced test equipment capable of meeting these stringent requirements, creating a high-value segment within the broader tester market.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Strive to Strengthen their Product Portfolio to Sustain Competition

The global semiconductor tester market exhibits a semi-consolidated competitive structure, characterized by a mix of established multinational corporations and a growing number of specialized regional players. This dynamic is driven by the critical need for high-precision testing equipment across the entire semiconductor value chain, from Integrated Device Manufacturers (IDMs) to Outsourced Semiconductor Assembly and Test (OSAT) providers. The market leaders have built their dominance on decades of R&D investment, extensive intellectual property portfolios, and deep-rooted relationships with major chipmakers.

Teradyne Inc. and Advantest Corporation are unequivocally the market leaders, collectively holding a significant portion of the global market share. Teradyne’s strength lies in its robust portfolio for SoC and memory testing, particularly for advanced applications in AI, automotive, and 5G. Advantest, a Japanese powerhouse, complements this with its leadership in memory testers and its expanding SoC test solutions. Their growth is directly tied to the increasing complexity of semiconductor devices, which demands more sophisticated and faster test systems.

Following these titans, companies like Cohu, Inc. and Chroma ATE have carved out substantial niches. Cohu, through its acquisition of Xcerra, has strengthened its position in handling and test solutions, especially for analog, power, and RF devices. Chroma ATE, based in Taiwan, has seen remarkable growth by offering cost-competitive solutions for power semiconductor and panel testing, capturing significant demand from the Asia-Pacific manufacturing hub. These companies are aggressively pursuing growth through strategic acquisitions and heavy R&D focus on emerging technologies like 5G RF and automotive power modules.

Meanwhile, a notable trend is the rapid ascent of Chinese players such as Beijing Huafeng and Hangzhou Changchuan Technology. Bolstered by national policies aimed at semiconductor self-sufficiency, these companies are rapidly enhancing their technological capabilities and expanding their market presence domestically and are beginning to challenge incumbents in certain segments. Their growth strategies are heavily focused on serving the vast local OSAT and IDM market with increasingly sophisticated and locally-supported test solutions.

Other key participants, including SPEA S.p.A. from Italy and Macrotest from Taiwan, are strengthening their positions by specializing in specific test domains like power devices and mixed-signal ICs. They compete through technological differentiation, flexibility, and by forming strategic partnerships to offer integrated testing solutions, ensuring their sustained relevance in an intensely competitive and innovation-driven market.

List of Key Semiconductor Tester Companies Profiled

- Teradyne Inc. (U.S.)

- Advantest Corporation (Japan)

- Cohu, Inc. (U.S.)

- Beijing Huafeng Test & Control Technology Co., Ltd. (China)

- Hangzhou Changchuan Technology Co., Ltd. (China)

- Chroma ATE Inc. (Taiwan)

- Exicon Co., Ltd. (South Korea)

- ShibaSoku Co., Ltd. (Japan)

- PowerTECH Technology Inc. (Taiwan)

- TESEC Corporation (Japan)

- Unisic Technologies Co., Ltd. (China)

- Macrotest Inc. (Taiwan)

- NI (National Instruments) (U.S.)

- SPEA S.p.A. (Italy)

- STATEC BINDER GmbH (Austria)

- YC Corporation (South Korea)

- UNITEST Inc. (South Korea)

- YTEC Co., Ltd. (South Korea)

- AMIDA Technology Inc. (U.S.)

- Test Research, Inc. (TRI) (Taiwan)

Segment Analysis:

By Type

SoC Tester Segment Leads the Market Fueled by Demand for Complex Integrated Circuits in AI and High-Performance Computing

The market is segmented based on type into:

- SoC Tester

- Memory Tester

- RF Tester

- Analog Tester

- Power Semiconductor Tester

- Others

By Application

IDMs Segment Commands Significant Share Owing to In-House Testing Requirements for Quality Control and Yield Optimization

The market is segmented based on application into:

- IDMs (Integrated Device Manufacturers)

- OSATs (Outsourced Semiconductor Assembly and Test)

- Others

By Technology

Advanced Packaging Testing Gains Prominence Driven by Heterogeneous Integration and 3D IC Trends

The market is segmented based on technology into:

- Wafer Test

- Package Test

- Advanced Packaging Test

By End-User Industry

Consumer Electronics and Automotive Sectors are Key Growth Drivers Due to Proliferation of Smart Devices and Electric Vehicles

The market is segmented based on end-user industry into:

- Consumer Electronics

- Automotive

- Telecommunications

- Industrial

- Aerospace & Defense

- Others

Regional Analysis: Semiconductor Tester Market

Asia-Pacific

The Asia-Pacific region is the undisputed global leader in the Semiconductor Tester market, accounting for over 60% of worldwide consumption. This dominance is fueled by the region’s colossal semiconductor manufacturing ecosystem, concentrated in powerhouses like Taiwan (TSMC), South Korea (Samsung, SK Hynix), and China (SMIC). The relentless demand for advanced SoC testers and memory testers is driven by the production of next-generation chips for smartphones, AI accelerators, and high-performance computing. While Japan remains a key market for precision test equipment, the growth is overwhelmingly led by massive capital expenditures in new fabrication plants, particularly for nodes below 7nm. However, the region also faces challenges, including geopolitical tensions affecting the supply chain and intense cost pressure from local test equipment manufacturers like Hangzhou Changchuan and Beijing Huafeng that are gaining significant market share.

North America

North America is a critical hub for semiconductor design and R&D, which directly fuels demand for high-end, sophisticated test systems. The market is characterized by a strong need for RF testers for 5G/6G applications and advanced SoC testers for AI and data center chips, driven by tech giants and fabless companies. Significant government initiatives, such as the CHIPS and Science Act, which allocates billions in funding for domestic semiconductor production, are creating a renewed push for onshore manufacturing and, consequently, test capacity. Leading players like Teradyne and Cohu are headquartered here, focusing on innovation to meet the stringent performance requirements of cutting-edge technologies. The market’s evolution is closely tied to the success of these re-shoring efforts and the ability to maintain a technological edge over global competitors.

Europe

The European Semiconductor Tester market is defined by its focus on specialized, high-value segments rather than high volume. There is significant demand for test equipment related to automotive semiconductors (power device testers, analog testers) and industrial IoT applications, driven by the region’s strong automotive and engineering sectors. The European Chips Act aims to bolster the region’s semiconductor sovereignty, which is expected to gradually increase demand for test equipment alongside new fabrication projects. Innovation in test methodologies for safety-critical applications, such as those required for autonomous driving, is a key differentiator. Companies like SPEA S.p.A. and NI (via SET GmbH) have a strong presence, catering to these niche but technically demanding requirements. The market growth is steady, though it is tempered by a more fragmented manufacturing base compared to Asia.

South America

The Semiconductor Tester market in South America is nascent and primarily serves downstream assembly and basic consumer electronics production. The region lacks a significant domestic semiconductor fabrication industry, resulting in limited demand for high-end test equipment. Market activity is mostly confined to OSATs (Outsourced Semiconductor Assembly and Test) operations that require testers for final package testing. Economic volatility and a lack of substantial government investment in high-tech infrastructure are the primary restraints hindering market development. While countries like Brazil have sporadic electronics manufacturing, the demand for semiconductor testers remains a fraction of the global total, with growth prospects tied to broader economic stability and potential future industrial policies aimed at technology development.

Middle East & Africa

This region represents an emerging and opportunistic market for semiconductor test equipment. Growth is currently driven by investments in telecommunications infrastructure and data centers, creating a budding need for testing related components. However, the absence of a local semiconductor fabrication industry means demand is almost entirely met through imports for maintenance and small-scale assembly operations. Nations like Israel, with its strong tech startup ecosystem, show potential for design-led demand, but this does not yet translate into significant volume for physical test equipment. The market’s long-term potential is linked to ambitious economic diversification plans in Gulf countries, which could eventually include investments in electronics manufacturing, but for the foreseeable future, it remains a minor part of the global landscape.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Semiconductor Tester markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Semiconductor Tester Market?

-> Semiconductor Tester Market was valued at 5528 million in 2024 and is projected to reach US$ 9339 million by 2032, at a CAGR of 6.9% during the forecast period.

Which key companies operate in Global Semiconductor Tester Market?

-> Key players include Teradyne, Advantest, Cohu, Beijing Huafeng, Hangzhou Changchuan, and Chroma ATE, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for advanced SoC chips, expansion of 5G/6G infrastructure, growth in AI computing, autonomous driving technologies, and increasing IoT adoption.

Which region dominates the market?

-> Asia-Pacific is the dominant region, driven by semiconductor manufacturing hubs in China, Taiwan, South Korea, and Japan.

What are the emerging trends?

-> Emerging trends include integration of AI for predictive testing, increased automation, development of testers for power semiconductors and CIS sensors, and the rise of domestic manufacturers in Asia.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...