MARKET INSIGHTS

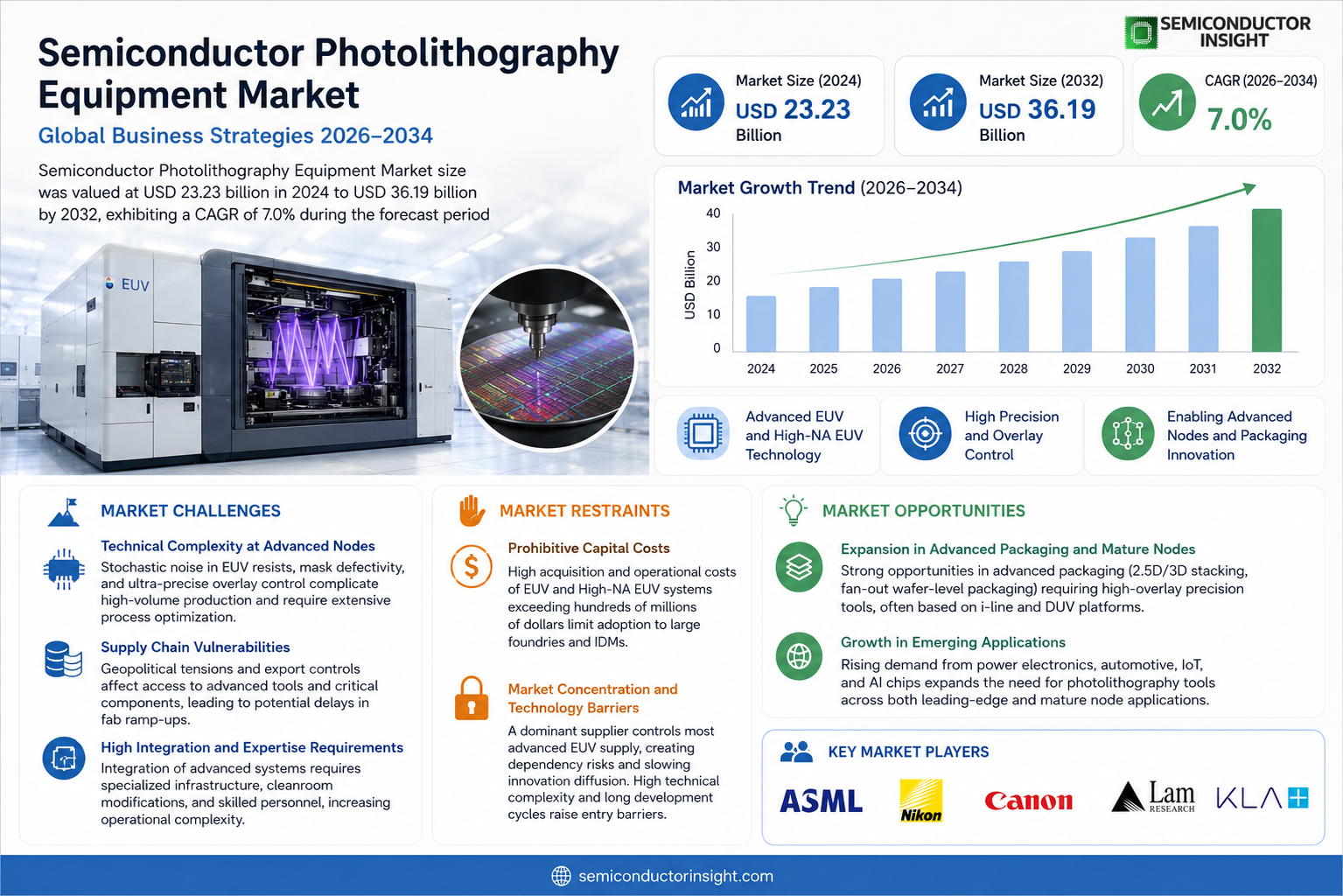

The global semiconductor photolithography equipment market size was valued at USD 23.23 billion in 2024. The market is projected to grow from USD 24.86 billion in 2025 to USD 36.19 billion by 2032, exhibiting a CAGR of 7.0% during the forecast period.

Semiconductor photolithography equipment is a critical tool used in the fabrication of integrated circuits (ICs). This equipment transfers intricate circuit patterns from a photomask onto a silicon wafer using a light source, a process fundamental to creating the microscopic features of modern semiconductors. The primary types of equipment include EUV lithography, ArFi immersion lithography, ArF dry lithography, KrF lithography, and i-line lithography, each catering to different node requirements and precision levels.

The market’s robust growth is primarily driven by the insatiable global demand for advanced electronics, such as smartphones, AI servers, and IoT devices, which require increasingly powerful and smaller chips. This is further accelerated by substantial investments in new semiconductor fabrication plants (fabs) worldwide. However, the market is highly concentrated, with ASML holding a dominant position, accounting for over 90% of the revenue share, particularly in the cutting-edge EUV segment. Nikon and Canon are other key players, while companies like China’s SMEE are focusing on developing domestic capabilities. The concurrent expansion of the overall semiconductor manufacturing market, projected to grow from USD 251.7 billion in 2023 to USD 506.5 billion by 2030, ensures sustained demand for this essential capital equipment.

MARKET DRIVERS

MARKET DRIVERS

Advancing Semiconductor Nodes and EUV Adoption

The Semiconductor Photolithography Equipment Market is primarily driven by the continuous push toward smaller process nodes in semiconductor manufacturing. Leading foundries and IDMs are accelerating adoption of extreme ultraviolet (EUV) lithography systems to enable production at 5nm, 3nm, and below, where traditional deep ultraviolet (DUV) techniques require complex multi-patterning that increases costs and reduces yields.

Rising Demand for AI and High-Performance Computing Chips

Explosive growth in artificial intelligence, high-performance computing, and data center applications has significantly increased lithography intensity per wafer. Advanced logic and memory chips for AI servers demand more critical layers with tighter overlay and critical dimension uniformity, boosting demand for high-precision photolithography equipment across both EUV and advanced DUV platforms.

➤ The transition to High-NA EUV systems represents a major technology inflection, allowing fewer patterning steps and improved process windows for sub-2nm nodes.

Government initiatives such as the US CHIPS Act and European Chips Act are further fueling fab expansions and modernization, creating sustained investment in next-generation photolithography tools to strengthen domestic semiconductor production capabilities.

MARKET CHALLENGES

Technical Complexity at Advanced Nodes

The Semiconductor Photolithography Equipment Market faces significant challenges related to the increasing technical demands of sub-5nm manufacturing. Issues such as stochastic noise in EUV resists, mask defectivity, and the need for ultra-precise overlay control complicate high-volume production and require extensive process optimization.

Other Challenges

Supply Chain Vulnerabilities

Geopolitical tensions and export controls have created bifurcated supply dynamics, particularly affecting access to advanced tools and critical components like light sources and optics, leading to potential delays in fab ramp-ups.

High Integration and Expertise Requirements

Integrating advanced photolithography systems into existing fabs demands highly specialized infrastructure, cleanroom modifications, and skilled personnel, which can slow deployment and increase operational complexity for semiconductor manufacturers.

MARKET RESTRAINTS

Prohibitive Capital Costs

High acquisition and operational costs of advanced photolithography equipment, particularly EUV and emerging High-NA EUV systems that can exceed several hundred million dollars per unit, act as a major restraint in the Semiconductor Photolithography Equipment Market. These expenses limit adoption primarily to large-scale foundries and IDMs with substantial capital resources.

Market Concentration and Technology Barriers

The market remains highly concentrated with a dominant player controlling the majority of advanced EUV supply, creating dependency risks and slowing broader innovation diffusion. Additionally, the extreme technical complexity and lengthy development cycles for new lithography platforms raise significant entry barriers for potential new suppliers.

MARKET OPPORTUNITIES

Expansion in Advanced Packaging and Mature Nodes

The Semiconductor Photolithography Equipment Market presents strong opportunities in advanced packaging applications, including 2.5D/3D stacking and fan-out wafer-level packaging, which require high-overlay precision tools often based on i-line and DUV platforms. This segment broadens the addressable market beyond front-end logic and memory.

Emerging Technologies and Regional Fab Growth

Development of complementary techniques such as nanoimprint lithography (NIL) for specific applications and AI-optimized computational lithography offer pathways to improve throughput and cost-of-ownership. Furthermore, new semiconductor manufacturing hubs in Asia and ongoing capacity expansions in North America and Europe are expected to drive incremental demand for both leading-edge and mature-node photolithography equipment.

Semiconductor Photolithography Equipment Market Trends

Transition to High-NA EUV Lithography

The semiconductor photolithography equipment market continues to evolve rapidly as manufacturers push toward smaller process nodes essential for advanced logic and memory chips. A primary trend is the accelerating adoption of high numerical aperture extreme ultraviolet (High-NA EUV) systems, which offer superior resolution compared to standard EUV tools. These systems, featuring a numerical aperture of 0.55 versus 0.33 in conventional setups, enable finer patterning with reduced reliance on complex multi-patterning techniques. This advancement supports the production of chips at 2nm and below, meeting the stringent requirements of artificial intelligence processors and high-performance computing applications.

Other Trends

Market Concentration and Technological Leadership

The semiconductor photolithography equipment market remains highly concentrated, with one leading supplier maintaining overwhelming dominance in the EUV segment. This supplier accounts for the vast majority of advanced system deliveries, supported by extensive collaborations with optics specialists for precision mirror manufacturing. Meanwhile, established players in deep ultraviolet (DUV) technologies, such as immersion and dry lithography systems, continue to serve mature nodes and critical layers where EUV is not yet fully deployed. Regional efforts to develop domestic capabilities are underway, though they primarily target less advanced lithography solutions at present.

Surging Demand Driven by AI and Advanced Node Expansion

Robust investments in new and upgraded semiconductor fabrication facilities worldwide are sustaining momentum in the semiconductor photolithography equipment market. The proliferation of AI-driven workloads has intensified the need for higher transistor densities and improved power efficiency, directly increasing demand for cutting-edge photolithography tools. Foundries and integrated device manufacturers are prioritizing EUV and High-NA EUV installations to optimize production for logic chips used in data centers and high-bandwidth memory essential for AI accelerators. Concurrently, ArF immersion lithography retains a significant role in supporting high-volume manufacturing across multiple layers, ensuring compatibility with existing fab infrastructures while newer technologies ramp up.

Another notable development involves holistic lithography approaches that integrate computational techniques and process control enhancements. These improvements help mitigate stochastic effects at shrinking feature sizes and enhance overall yield. As chipmakers expand capacity in key regions, the semiconductor photolithography equipment market benefits from sustained capital expenditures focused on precision patterning solutions. The interplay between EUV advancements and continued reliance on DUV systems creates a balanced ecosystem capable of addressing both leading-edge and established semiconductor requirements without disruption.

COMPETITIVE LANDSCAPE

Key Industry Players

Semiconductor Photolithography Equipment Market – Highly Concentrated Competitive Landscape

The semiconductor photolithography equipment market is characterized by extreme concentration, with ASML Holding N.V. maintaining a dominant position, particularly in the critical extreme ultraviolet (EUV) lithography segment essential for advanced nodes below 7nm. This Dutch company commands over 90% of the overall revenue share due to its technological leadership, proprietary high-NA EUV systems, and strong partnerships with leading foundries such as TSMC, Samsung, and Intel. The market structure reflects high barriers to entry, including massive R&D costs, complex supply chains for light sources and optics, and lengthy customer qualification processes that reinforce incumbency advantages in serving the booming demand for AI chips, advanced logic, and memory devices.

While ASML leads the cutting-edge technology, Japanese firms Nikon Corporation and Canon Inc. hold meaningful positions in the deep ultraviolet (DUV) segments, including ArFi immersion, ArF dry, KrF, and i-line lithography systems suited for mature process nodes and specialized applications. China’s Shanghai Micro Electronics Equipment (SMEE) is emerging as a strategic player focused on developing domestic alternatives to reduce reliance on foreign technology. Additional niche participants such as SUSS MicroTec, EV Group, and Veeco Instruments contribute specialized solutions for advanced packaging, mask aligners, and nanoimprint lithography, complementing the primary scanner market amid global fab expansions.

List of Key Semiconductor Photolithography Equipment Companies Profiled

- ASML Holding N.V.

- ASML Holding N.V.

- Nikon Corporation

- Canon Inc.

- Shanghai Micro Electronics Equipment (SMEE)

- SUSS MicroTec SE

- EV Group (EVG)

- Veeco Instruments Inc.

- JEOL Ltd.

- SCREEN Holdings Co., Ltd.

- Tokyo Electron Limited

- Applied Materials, Inc.

- KLA Corporation

- Hitachi High-Tech Corporation

- Onto Innovation Inc.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

EUV Lithography stands as the leading segment due to its unparalleled capability in achieving the finest feature resolutions essential for cutting-edge semiconductor nodes. This technology enables manufacturers to create intricate circuit patterns that support higher transistor densities and enhanced chip performance. Key advantages include reduced complexity in multi-patterning processes compared to older methods, leading to improved yield and efficiency in advanced fabrication. Its adoption accelerates innovation in high-performance computing and artificial intelligence applications, where precision patterning is non-negotiable for competitive advantage. Additionally, EUV systems integrate seamlessly with next-generation process flows, offering long-term scalability as device architectures continue to evolve toward smaller geometries. |

| By Application |

|

Front-end Process emerges as the dominant application area, serving as the foundational stage where critical circuit patterns are transferred onto silicon wafers to define the core functionality of integrated circuits. This segment benefits from the need for extreme precision in creating transistor structures and interconnects that determine overall device speed and power efficiency. Insights highlight its role in enabling complex logic and memory architectures demanded by modern electronics. The process demands sophisticated equipment alignment and overlay accuracy to minimize defects across multiple layers. Furthermore, ongoing advancements in front-end lithography directly influence the industry’s ability to scale production while maintaining stringent quality standards across diverse semiconductor product lines. |

| By End User |

|

Foundries represent the leading end user segment, driven by their pivotal position in providing contract manufacturing services to a wide array of fabless semiconductor companies. This model fosters flexibility and specialization, allowing foundries to invest heavily in state-of-the-art photolithography tools to support diverse client requirements ranging from high-volume logic chips to specialized memory solutions. Their focus on process optimization and technology leadership ensures rapid adoption of advanced lithography techniques. Moreover, foundries play a crucial role in democratizing access to cutting-edge fabrication capabilities, spurring broader ecosystem innovation. The segment’s emphasis on collaborative development with equipment suppliers further enhances throughput and pattern fidelity across varied production runs. |

| By Technology Node |

|

Advanced Nodes (below 7nm) lead this segmentation owing to the relentless pursuit of higher performance, lower power consumption, and greater functionality in semiconductors. Equipment tailored for these nodes excels in delivering the resolution and overlay precision required for dense transistor packing and multi-layer interconnects. This focus supports transformative applications in artificial intelligence, high-performance computing, and mobile processors. Qualitative insights reveal enhanced process windows that mitigate stochastic effects and improve overall manufacturing robustness. The segment drives continuous equipment innovation, emphasizing higher numerical apertures and refined light sources to sustain Moore’s Law progression while addressing thermal and mechanical challenges inherent in ultra-fine patterning. |

| By Light Source |

|

Excimer Laser dominates as the preferred light source, delivering the coherent, high-intensity output necessary for high-throughput and high-resolution patterning across multiple lithography generations. Its versatility supports both deep ultraviolet and related processes, ensuring consistent exposure doses critical for uniform critical dimension control. This source facilitates superior energy efficiency and stability in production environments, reducing variability in wafer processing. Insights underscore its contribution to achieving finer linewidths while maintaining cost-effective operation in high-volume fabs. The technology’s maturity allows seamless integration with advanced photoresists and optical systems, promoting reliable scaling of semiconductor features essential for next-generation electronic devices. |

Regional Analysis: Semiconductor Photolithography Equipment Market

Asia-Pacific demonstrates exceptional technological leadership through continuous upgrades to photolithography infrastructure. The region excels in integrating multi-patterning techniques and high-NA EUV systems, supporting the transition to sub-3nm process technologies. This focus on innovation ensures manufacturers can meet the stringent demands of advanced semiconductor designs while optimizing production efficiency.

The region’s highly integrated semiconductor ecosystem allows for seamless deployment of photolithography equipment. Close proximity between equipment manufacturers, material suppliers, and fabrication plants reduces lead times and enhances customization capabilities, creating a responsive environment for evolving lithography requirements in memory and logic segments.

Policy frameworks across key economies actively promote semiconductor advancement, including incentives for lithography equipment adoption and R&D initiatives. These measures strengthen domestic capabilities in high-precision manufacturing, positioning the region as a preferred destination for global technology deployment in photolithography solutions.

Sustained demand from consumer electronics, automotive, and data center segments fuels ongoing expansion of photolithography capabilities. The region’s manufacturers are strategically investing in capacity upgrades that incorporate the latest lithography tools, ensuring long-term competitiveness in the global semiconductor landscape.

North America

North America maintains a significant presence in the Semiconductor Photolithography Equipment Market through its focus on innovation and high-value applications. The region emphasizes research and development in next-generation lithography technologies, particularly for specialized applications in defense, aerospace, and artificial intelligence. Strong intellectual property frameworks and collaboration between academia and industry drive advancements in precision patterning solutions. While manufacturing scale remains more modest compared to Asia, North American firms excel in designing and optimizing photolithography processes for cutting-edge semiconductor architectures, supporting the development of sophisticated chips required by emerging technologies.

Europe

Europe plays a vital role in the Semiconductor Photolithography Equipment Market by contributing critical expertise in materials science and equipment engineering. The region demonstrates strength in developing enabling technologies that enhance lithography performance, including advanced photoresists and metrology solutions. European semiconductor initiatives focus on strategic autonomy and sustainability, encouraging the adoption of energy-efficient photolithography systems. Collaborative ecosystems involving equipment makers and research consortia help advance EUV and DUV capabilities, particularly for automotive and industrial applications where reliability and precision are paramount.

South America

South America is gradually emerging in the Semiconductor Photolithography Equipment Market as countries explore opportunities to build foundational semiconductor capabilities. The region shows increasing interest in establishing local manufacturing and assembly ecosystems that could eventually incorporate photolithography technologies. While currently limited in scale, strategic investments and international partnerships aim to develop the necessary infrastructure and skilled workforce. Focus areas include supporting regional electronics industries and reducing dependency on external supply chains through targeted technology transfer initiatives.

Middle East & Africa

The Middle East and Africa region is witnessing nascent developments in the Semiconductor Photolithography Equipment Market, driven by diversification efforts away from traditional sectors. Several economies are investing in technology parks and educational programs to foster semiconductor-related skills. Although adoption of advanced photolithography equipment remains in early stages, strategic visions target the creation of knowledge-based economies with potential applications in communications and renewable energy technologies. International cooperation serves as a key catalyst for introducing lithography capabilities suited to regional development priorities.

Report Scope

This market research report provides a comprehensive analysis of the Semiconductor Photolithography Equipment Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

-

Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Semiconductor Photolithography Equipment Market?

-> The Semiconductor Photolithography Equipment Market was valued at USD 24.86 billion in 2025 and is expected to reach USD 36.19 billion by 2034.

Which key companies operate in Semiconductor Photolithography Equipment Market?

-> Key players include ASML, Nikon, Canon, and SMEE, among others.

What are the key growth drivers?

-> Key growth drivers include surging demand for advanced electronics, increasing semiconductor fabrication investments, and rapid adoption of smaller and more powerful chips.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing and dominant region due to large-scale semiconductor manufacturing and extensive fab expansions.

What are the emerging trends?

-> Emerging trends include advancements in EUV technology, rising domestic equipment development in China, and increased integration of AI/IoT in semiconductor fabrication.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...