MARKET INSIGHTS

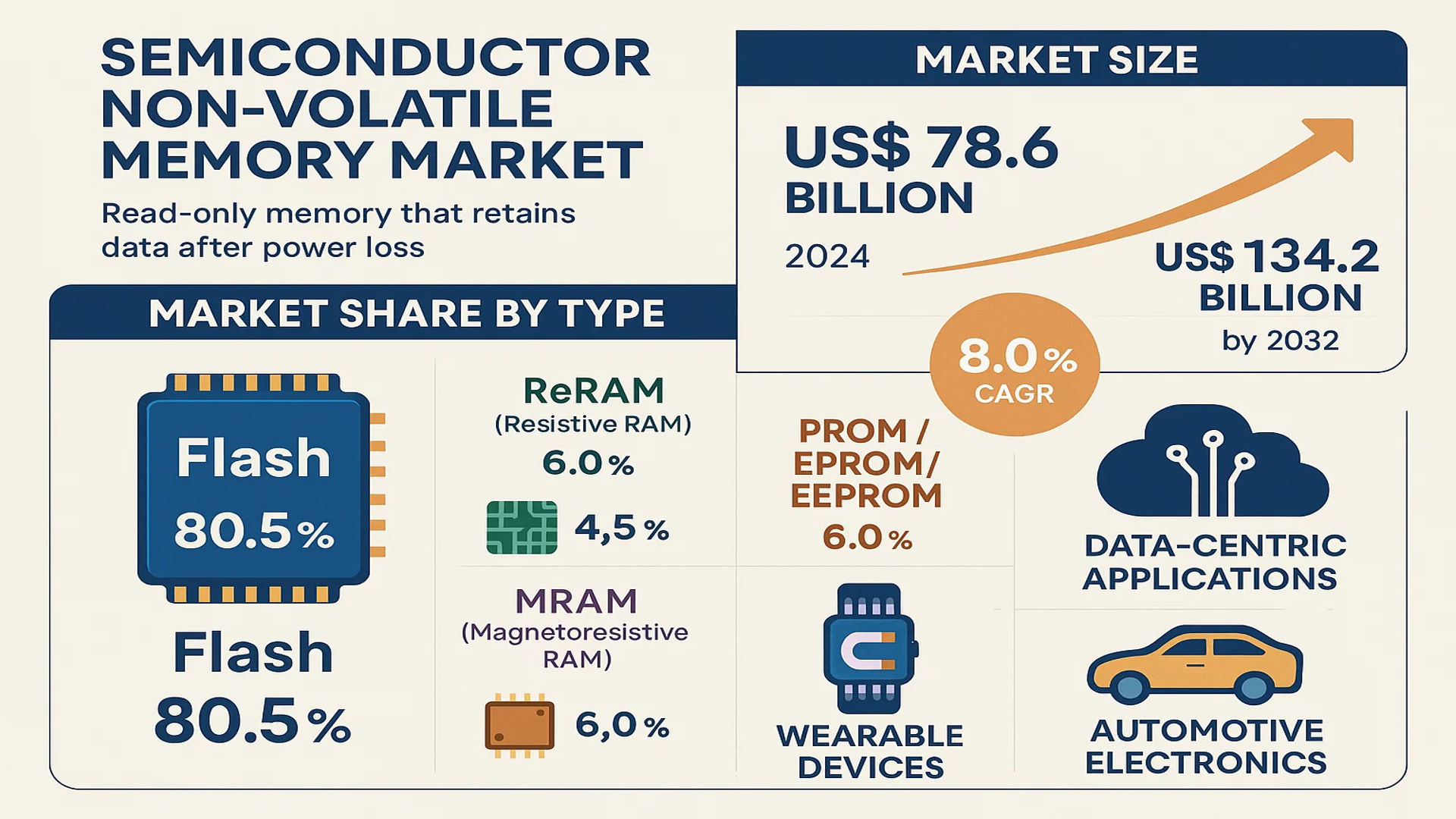

The global Semiconductor Non-Volatile Memory Market size was valued at US$ 78.6 billion in 2024 and is projected to reach US$ 134.2 billion by 2032, at a CAGR of 8.0% during the forecast period 2025-2032. While Flash memory dominates the segment, emerging technologies like Resistive RAM (ReRAM) and Magnetoresistive RAM (MRAM) are gaining traction due to their high-speed and low-power characteristics.

Semiconductor non-volatile memory refers to read-only memory (ROM) that retains data even after power loss, making it critical for data storage applications. Key types include Flash (NAND/NOR), PROM, EPROM, EEPROM, and MASK ROM. Among these, Flash memory accounts for over 80% of the market share due to its widespread use in smartphones, SSDs, and IoT devices. However, innovations in next-generation memory technologies are reshaping the competitive landscape.

The market is driven by the exponential growth of data-centric applications, including AI, cloud computing, and 5G networks. Additionally, rising demand for high-performance memory in automotive electronics and wearable devices is accelerating adoption. In February 2024, Samsung Electronics announced a breakthrough in 3D NAND technology, achieving higher storage densities with lower power consumption. Key players like Micron Technology, SK Hynix, and Intel Corporation continue to invest heavily in R&D to maintain technological leadership.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of IoT and AI Technologies to Fuel Semiconductor Non-Volatile Memory Demand

The rapid expansion of Internet of Things (IoT) devices and artificial intelligence applications is creating unprecedented demand for semiconductor non-volatile memory solutions. With over 30 billion connected IoT devices projected by 2025, the need for reliable, low-power memory storage continues to intensify. Flash memory, particularly 3D NAND technology, has emerged as the preferred solution for these applications due to its durability, high density, and energy efficiency. Automotive applications—including advanced driver-assistance systems (ADAS) and in-vehicle infotainment—are driving particularly strong growth, with the automotive memory market projected to grow at a compound annual growth rate approaching 20% through 2028.

Data Center Expansion to Accelerate High-Density Memory Adoption

Global hyperscale data center capacity is expanding at a rate exceeding 25% annually to meet cloud computing demands, creating substantial opportunities for advanced non-volatile memory solutions. The shift toward memory-intensive workloads like machine learning inference and real-time analytics is pushing data centers to adopt high-performance storage class memory technologies. Emerging solutions such as 3D XPoint and resistive RAM (ReRAM) are gaining traction in enterprise storage applications, offering latencies up to 1,000 times faster than traditional NAND flash. This transition toward memory-centric computing architectures represents a paradigm shift that will continue to drive innovation and investment in the sector.

➤ Intel’s discontinuation of Optane memory products in 2022 created a market gap that has accelerated development of alternative non-volatile memory technologies by competitors.

5G Network Rollouts to Stimulate Memory Demand

The global deployment of 5G infrastructure requires substantial upgrades to memory solutions across network equipment and end-user devices. 5G base stations demand robust non-volatile memory for firmware storage and configuration data, while smartphones and other connected devices require higher density storage solutions to support bandwidth-intensive applications. The telecommunications memory market is expected to maintain growth exceeding 15% annually through 2027, with NOR flash memory seeing particularly strong demand for its fast read speeds and reliability in mission-critical communications applications.

MARKET RESTRAINTS

Semiconductor Supply Chain Vulnerabilities to Constrain Market Growth

Persistent supply chain disruptions continue to impact the semiconductor memory industry, with lead times for certain memory products extending beyond 30 weeks in recent years. Geopolitical tensions have forced companies to reevaluate supply chain dependencies, particularly for materials like silicon wafers and specialty chemicals where production remains concentrated in specific regions. The memory industry’s capital-intensive nature also creates barriers to diversification, as establishing new fabrication facilities requires investments frequently exceeding $10 billion for advanced nodes. These constraints are especially problematic for emerging memory technologies that lack the scale and mature supply chains of established NAND flash products.

Technology Scaling Challenges to Limit Performance Gains

As NAND flash approaches physical scaling limits below 100 layers in 3D configurations, manufacturers face diminishing returns on process node advancements. The critical challenges of cell-to-cell interference and electron leakage become increasingly difficult to manage at advanced nodes, threatening the reliability and endurance of flash memory products. While emerging technologies like ferroelectric RAM (FeRAM) and magnetoresistive RAM (MRAM) offer potential solutions, their widespread adoption faces obstacles including manufacturing complexity and higher per-bit costs compared to established technologies. These technical hurdles prolong development cycles and increase research expenditures for memory manufacturers.

MARKET CHALLENGES

Intensifying Price Competition to Pressure Profit Margins

The memory market remains highly cyclical, with periods of oversupply leading to dramatic price declines that can exceed 30% annually for certain product categories. The highly commoditized nature of NAND flash memory exacerbates this volatility, as manufacturers engage in aggressive pricing strategies to maintain market share. This environment creates significant challenges for companies investing in next-generation memory technologies that carry higher production costs. The recent consolidation among major memory suppliers—reducing the number of major NAND flash producers from eight to six—has somewhat mitigated these pressures but has not eliminated the fundamental dynamics of this competitive landscape.

Other Challenges

Data Retention Limitations

Certain non-volatile memory technologies face fundamental limitations in data retention duration, particularly at elevated temperatures. Automotive and industrial applications requiring 10+ years of data retention at temperatures above 85°C significantly constrain the range of viable memory solutions, limiting design options for engineers.

Security Vulnerabilities

Emerging threats like Rowhammer attacks on DRAM and read-disturb issues in NAND flash have exposed vulnerabilities in memory technologies. Addressing these security challenges requires substantial investments in error correction, wear leveling algorithms, and hardware-based protection mechanisms.

MARKET OPPORTUNITIES

Automotive Memory Innovations to Drive Next Growth Phase

The automotive semiconductor memory market presents one of the most promising growth avenues, with content per vehicle projected to increase 3-4x by 2030 as vehicles incorporate more advanced electronics. Applications range from infotainment systems requiring high-density storage to safety-critical systems demanding ultra-reliable non-volatile memory solutions. The transition toward autonomous driving is creating particularly strong demand for memory technologies that combine high bandwidth, low latency, and exceptional data integrity—characteristics that position emerging non-volatile memory solutions for substantial growth in this sector.

Edge Computing Expansion to Create New Memory Requirements

The proliferation of edge computing deployments is generating demand for memory solutions optimized for distributed intelligence applications. Unlike traditional cloud architectures, edge environments require memory technologies that balance performance with power efficiency in constrained environments. Emerging non-volatile memory solutions like STT-MRAM (spin-transfer torque MRAM) are gaining traction in these applications due to their near-infinite endurance and persistence characteristics. With edge computing infrastructure investments projected to grow at over 20% annually through 2030, this represents a significant opportunity for memory manufacturers to develop application-specific solutions.

➤ Recent advancements in compute-in-memory architectures demonstrate the potential for non-volatile memory to reduce data movement bottlenecks in AI accelerators, opening new market opportunities.

Sustainable Memory Technologies to Align With Environmental Initiatives

Growing emphasis on environmental sustainability is driving innovation in memory technologies that reduce energy consumption throughout their lifecycle. Emerging non-volatile memory solutions offer significant potential energy savings compared to traditional architectures—an increasingly important consideration for data center operators and device manufacturers facing regulatory pressures and ESG commitments. Memory technologies that eliminate the need for constant refresh cycles or reduce write amplification in flash storage are particularly well-positioned to benefit from these market trends, creating opportunities for differentiation beyond traditional performance metrics.

SEMICONDUCTOR NON-VOLATILE MEMORY MARKET TRENDS

Growing Demand for High-Speed, Energy-Efficient Memory Solutions

The semiconductor non-volatile memory market is experiencing significant growth, driven by the rising demand for high-speed, energy-efficient data storage solutions across various industries. Flash memory, particularly NAND and NOR flash, continues to dominate due to its fast read/write capabilities and high endurance. The adoption of 3D NAND technology, which offers higher storage density and lower production costs, is accelerating market expansion. Furthermore, innovations such as ferroelectric RAM (FeRAM) and resistive RAM (ReRAM) are gaining traction, offering faster write speeds and lower power consumption, making them ideal for IoT and edge computing applications.

Other Trends

Expansion of Automotive Electronics

The automotive industry is increasingly relying on semiconductor non-volatile memory for advanced driver-assistance systems (ADAS), infotainment, and vehicle connectivity solutions. Modern vehicles require high-performance memory to handle large volumes of sensor and telemetry data. With the rise of autonomous and electric vehicles, the demand for reliable, persistent storage solutions is expected to grow at a CAGR of 8-10% over the next decade. Memory technologies such as EEPROM and MASK ROM are critical for firmware storage, while high-density NAND flash supports real-time logging and over-the-air (OTA) updates.

Data Center and Cloud Storage Boom

The exponential growth in data generation is fueling demand for high-capacity, low-latency memory solutions in data centers and cloud infrastructure. Enterprise SSD adoption is surging due to the shift from HDDs to faster, more reliable storage mediums. 3D XPoint technology, developed by Intel and Micron, offers near-DRAM speeds with non-volatility, making it an attractive option for tiered memory architectures. Additionally, the growing implementation of AI and machine learning workloads is pushing memory suppliers to develop products with higher endurance and lower power consumption to support real-time processing.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Semiconductor NVM Suppliers Drive Innovation Amid Rising Market Demand

The global semiconductor non-volatile memory (NVM) market features a competitive environment where established tech giants compete alongside specialized memory manufacturers. Samsung Electronics and Micron Technology currently dominate the market, collectively holding over 35% revenue share in 2024. Their leadership stems from vertical integration capabilities across NAND flash and emerging memory technologies like MRAM and ReRAM.

Toshiba Corporation and SK Hynix maintain strong positions through strategic partnerships with foundries and continuous capacity expansions. In 2024, Toshiba announced a $8 billion investment to increase 3D NAND production, while SK Hynix completed its acquisition of Intel’s NAND business – moves that significantly strengthened their market positions.

Meanwhile, Intel Corporation is pivoting towards next-generation solutions, having partnered with Micron to develop 3D XPoint technology before their recent divestiture. IDM players like TSMC and GlobalFoundries are expanding their specialty memory foundry services to capture demand from fabless semiconductor companies.

The market also sees growing competition from emerging players such as Crossbar Inc. and Everspin Technologies, who are commercializing resistive RAM and MRAM technologies respectively. These companies are gaining traction in automotive and industrial applications where durability and fast access times are critical.

List of Key Semiconductor Non-Volatile Memory Companies Profiled

- Samsung Electronics Co., Ltd. (South Korea)

- Micron Technology, Inc. (U.S.)

- Toshiba Corporation (Japan)

- SK Hynix, Inc. (South Korea)

- Intel Corporation (U.S.)

- TSMC (Taiwan)

- GlobalFoundries (U.S.)

- Sandisk Corporation (U.S.)

- Microchip Technology (U.S.)

- Fujitsu Ltd (Japan)

- Synopsys (U.S.)

- IBM (U.S.)

- UMC (Taiwan)

- SMIC (China)

- Everspin Technologies Inc. (U.S.)

- Crossbar Inc. (U.S.)

Segment Analysis:

By Type

Flash (Flash Memory) Segment Leads Due to High Adoption in Data Storage and Embedded Applications

The market is segmented based on type into:

- Flash (Flash Memory)

- Subtypes: NAND Flash, NOR Flash, and others

- PROM (Programmable Read Only Memory)

- EPROM (Erasable Programmable Read Only Memory)

- EEPROM (Electrically Erasable Programmable Read Only Memory)

- MASK ROM (Mask Read Only Memory)

- Others

By Application

Consumer Electronics Segment Dominates Owing to Extensive Use in Smartphones and IoT Devices

The market is segmented based on application into:

- Consumer Electronics

- Medical

- Automobile

- Industry

- Others

By End User

Enterprise Storage Segment Leads Due to Rising Demand for Cloud Computing Solutions

The market is segmented based on end user into:

- Enterprise Storage

- Telecommunications

- Aerospace & Defense

- Healthcare

- Others

Regional Analysis: Semiconductor Non-Volatile Memory Market

Asia-Pacific

The Asia-Pacific region dominates the global semiconductor non-volatile memory market, accounting for the largest revenue share due to strong manufacturing capabilities and rapid technological adoption. Countries like China, Japan, and South Korea are leading contributors, driven by extensive electronics production and increasing demand for data storage in consumer electronics and automotive applications. The China market alone is projected to reach $X million by 2032, fueled by investments in semiconductor fabs and government initiatives like Made in China 2025. While Flash memory remains the most widely adopted, emerging memory technologies like MRAM and ReRAM are gaining traction in advanced applications, supported by local players like SMIC and Samsung Electronics.

North America

North America is a key innovation hub for semiconductor non-volatile memory, with companies like Intel, Micron Technology, and Western Digital driving R&D in high-performance solutions. The U.S. holds the largest regional market share, supported by demand from data centers, automotive (ADAS), and AI-driven applications. The CHIPS and Science Act has further boosted domestic semiconductor production, with $52.7 billion allocated for manufacturing incentives. While NOR and NAND Flash dominate, niche segments like FRAM and PCRAM are growing due to their low-power advantages in IoT and edge computing.

Europe

Europe’s market is defined by stringent data regulations (e.g., GDPR) and strong automotive/industrial demand, particularly for EEPROM and Flash memory in automotive MCUs and smart sensors. Germany leads with companies like Infineon leveraging non-volatile memory for industrial automation. The EU’s Chips Act aims to double its global semiconductor market share to 20% by 2030, focusing on resilience. However, reliance on imports for advanced nodes and slower adoption of next-gen memories like 3D XPoint limit growth compared to Asia and the U.S.

South America

The region shows moderate growth, with Brazil and Argentina as primary markets. Demand is driven by consumer electronics and automotive sectors, though economic instability and limited local fabrication constrain adoption. Most non-volatile memory is imported, with multinational suppliers like Microchip Technology and STMicroelectronics serving the region. Government initiatives to boost tech infrastructure could create long-term opportunities, but progress remains slow compared to global peers.

Middle East & Africa

This is an emerging market, with growth centered in Israel, Saudi Arabia, and the UAE, where investments in datacenters and smart cities are rising. Israel’s tech ecosystem has spurred innovation in flash controllers and embedded memory, while the broader region relies on imports for legacy memory solutions. Limited semiconductor manufacturing and fragmented demand hinder rapid expansion, but partnerships with global players (e.g., TowerJazz in Israel) signal potential for niche growth.

Key Trends Across Regions:

– Flash memory (NAND/NOR) remains dominant due to cost-effectiveness, but alternatives like MRAM and ReRAM are advancing in AI/ML applications.

– Automotive and industrial sectors are critical growth drivers, especially for high-endurance EEPROM and low-power Flash.

– Geopolitical factors (e.g., U.S.-China trade tensions) are reshaping supply chains, with regions like Europe and India incentivizing local production to reduce dependency.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Semiconductor Non-Volatile Memory markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Semiconductor Non-Volatile Memory market was valued at US$ 78.6 billion in 2024 and is projected to reach US$ 134.2 billion by 2032, growing at a CAGR of 8.0%.

- Segmentation Analysis: Detailed breakdown by product type (Flash Memory, PROM, EPROM, EEPROM, MASK ROM), application (Consumer Electronics, Medical, Automobile, Industrial), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America (U.S. market size estimated at USD 12.4 billion in 2024), Europe, Asia-Pacific (China to reach USD 18.9 billion by 2032), Latin America, and the Middle East & Africa.

- Competitive Landscape: Profiles of leading market participants including Samsung Electronics, Micron Technology, Intel Corporation, Toshiba, and SK Hynix, covering their product portfolios, R&D investments, and recent strategic developments.

- Technology Trends & Innovation: Assessment of emerging memory technologies like 3D NAND Flash, MRAM, ReRAM, and their integration with AI/ML applications in data centers and edge computing.

- Market Drivers & Restraints: Evaluation of factors including growing demand for data storage, IoT proliferation, and automotive electronics expansion, balanced against supply chain constraints and fabrication challenges.

- Stakeholder Analysis: Strategic insights for semiconductor manufacturers, foundries, OEMs, and investors regarding technology roadmaps and market opportunities.

The research methodology combines primary interviews with industry experts and secondary data from verified sources including financial reports, trade publications, and regulatory filings to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Semiconductor Non-Volatile Memory Market?

-> Semiconductor Non-Volatile Memory Market size was valued at US$ 78.6 billion in 2024 and is projected to reach US$ 134.2 billion by 2032, at a CAGR of 8.0% during the forecast period 2025-2032.

Which key companies operate in this market?

-> Key players include Samsung Electronics, Micron Technology, Intel Corporation, Toshiba, SK Hynix, Western Digital, and Kioxia, with the top five companies holding approximately 68% market share.

What are the key growth drivers?

-> Growth is driven by increasing data storage demands, 5G deployment, automotive electronics expansion, and cloud computing adoption.

Which region dominates the market?

-> Asia-Pacific dominates with over 45% market share, led by China, South Korea, and Taiwan’s semiconductor manufacturing ecosystem.

What are the emerging technology trends?

-> Emerging trends include 3D NAND scaling challenges, next-gen MRAM adoption in AI applications, and increased integration of NVM in edge computing devices.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...