MARKET INSIGHTS

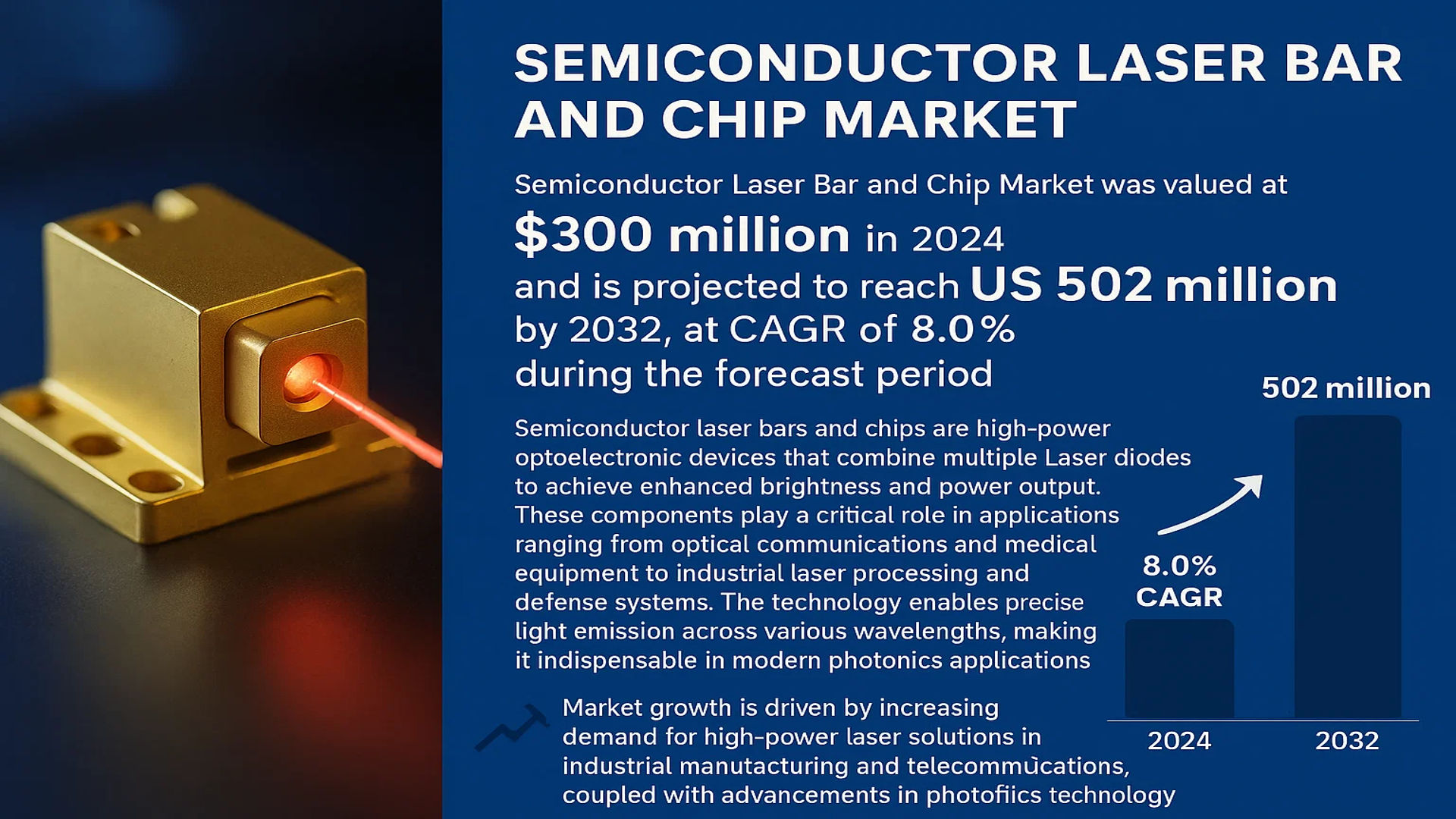

The global Semiconductor Laser Bar and Chip Market was valued at 300 million in 2024 and is projected to reach US$ 502 million by 2032, at a CAGR of 8.0% during the forecast period.

Semiconductor laser bars and chips are high-power optoelectronic devices that combine multiple laser diodes to achieve enhanced brightness and power output. These components play a critical role in applications ranging from optical communications and medical equipment to industrial laser processing and defense systems. The technology enables precise light emission across various wavelengths, making it indispensable in modern photonics applications.

Market growth is driven by increasing demand for high-power laser solutions in industrial manufacturing and telecommunications, coupled with advancements in photonics technology. The U.S. market represents a significant share of global demand, while China is emerging as a fast-growing regional market. Key industry players including Coherent, ams Osram, and Jenoptik are expanding their product portfolios through technological innovations, further accelerating market expansion.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for High-Power Laser Applications to Accelerate Market Expansion

The semiconductor laser bar and chip market is experiencing substantial growth driven by increasing adoption across multiple high-power applications. Industries such as material processing, medical equipment, and defense increasingly rely on semiconductor lasers for their precision, efficiency, and reliability. The material processing sector alone constitutes over 35% of the market share, utilizing laser bars for cutting, welding, and additive manufacturing. As industrial automation rises globally, manufacturers are rapidly adopting laser-based processes, which are more efficient than traditional methods, thus fueling demand for semiconductor laser solutions.

Advancements in Optical Communication Infrastructure to Boost Adoption

The rapid expansion of 5G networks and data centers worldwide is significantly driving the demand for semiconductor lasers in optical communication. With data traffic growth projected to increase by over 25% annually, fiber optic networks require high-performance laser diodes for efficient signal transmission. Semiconductor laser bars and chips enable high-speed data transfer critical for telecommunications, internet services, and cloud computing. Furthermore, investments in next-generation optical networks exceed $80 billion globally, indicating sustained growth potential for laser diode components.

Medical Laser Technology Innovations to Propel Market Growth

The medical sector represents one of the fastest-growing application areas for semiconductor lasers, with the market expected to expand at a CAGR of 10.2% through 2032. Laser diodes are essential components in surgical tools, dermatology equipment, and dental devices due to their precision and minimally invasive capabilities. Recent technological breakthroughs have enabled the development of compact, high-efficiency laser systems for portable medical devices. The increasing prevalence of chronic diseases and aging populations worldwide further amplifies the need for advanced laser-based medical solutions.

MARKET RESTRAINTS

High Manufacturing Costs and Complex Production Processes to Limit Growth

While the semiconductor laser bar and chip market shows strong potential, the high cost of raw materials and complex fabrication processes present significant challenges. The production of high-quality laser diodes requires specialized materials like gallium arsenide and indium phosphide, which account for nearly 40% of total manufacturing costs. Additionally, maintaining precise temperature control and cleanroom conditions during production increases operational expenses. These cost factors make semiconductor lasers less competitive against alternative technologies in price-sensitive markets.

Other Restraints

Thermal Management Challenges

Efficient heat dissipation remains a critical technical barrier for high-power semiconductor lasers. As power outputs increase, managing thermal loads becomes more complex, often requiring expensive cooling systems. This limitation affects the compactness and reliability of laser systems in applications where space constraints are critical.

Supply Chain Vulnerabilities

Global supply chain disruptions continue to impact the availability of key semiconductor materials and components. Geopolitical tensions and trade restrictions have created uncertainties in raw material procurement, particularly for rare earth elements essential in laser diode production.

MARKET CHALLENGES

Intense Competition and Rapid Technological Obsolescence Pressure Margins

The semiconductor laser industry faces fierce competition among global players, with over 50 manufacturers vying for market share. This competitive landscape forces companies to continuously invest in research and development while facing margin pressures. The average product lifecycle for laser diodes has reduced from 5 years to just 2-3 years, requiring manufacturers to accelerate innovation cycles. Smaller players struggle to keep pace with the rapid technological advancements led by industry leaders, creating market consolidation trends.

Other Challenges

Quality Control Complexities

Maintaining consistent quality across high-volume production remains challenging due to the precision required in laser diode manufacturing. Even minor deviations in material purity or fabrication processes can significantly impact performance, leading to higher rejection rates and production costs.

Regulatory Compliance Demands

Increasingly stringent safety regulations for laser products across different regions require manufacturers to navigate complex certification processes. This regulatory burden slows time-to-market for new products and increases compliance costs, particularly for medical and defense applications.

MARKET OPPORTUNITIES

Emerging Applications in Electric Vehicles and Renewable Energy to Create New Growth Avenues

The rapid adoption of electric vehicles (EVs) and renewable energy systems presents significant opportunities for semiconductor laser technology. Laser processing is becoming essential in battery manufacturing for EVs, particularly in electrode cutting and welding applications where precision is critical. The photovoltaic industry also increasingly utilizes laser bars for solar cell manufacturing, with the global solar market projected to grow at 8.7% CAGR through 2030. As these sectors expand, demand for specialized laser solutions tailored to clean energy applications will create new revenue streams for manufacturers.

Advancements in Consumer Electronics to Drive Miniaturized Laser Demand

The consumer electronics sector offers substantial growth potential for compact semiconductor laser chips. Applications such as 3D sensing in smartphones, augmented reality devices, and LiDAR systems increasingly incorporate miniature laser diodes. With over 1.5 billion smartphones shipped annually, each containing multiple laser components for facial recognition and camera autofocus, this segment continues to expand rapidly. Manufacturers developing ultra-compact, energy-efficient laser chips with improved beam quality stand to benefit most from this burgeoning market opportunity.

Military Modernization Programs to Fuel Defense Applications

Global defense spending exceeding $2.1 trillion annually is driving demand for advanced laser technologies in military applications. Semiconductor laser bars are critical components in rangefinders, target designators, and directed energy weapons systems. Nations worldwide are investing heavily in laser-based defense systems, creating long-term, stable demand for high-reliability laser components. The growing emphasis on asymmetric warfare and precision strike capabilities further amplifies the strategic importance of semiconductor laser technologies in defense applications.

SEMICONDUCTOR LASER BAR AND CHIP MARKET TRENDS

Growing Demand for High-Power Laser Applications Drives Market Expansion

The global semiconductor laser bar and chip market has witnessed significant growth, driven by increasing demand for high-power laser applications in industries such as optical communications, medical equipment, and laser processing. The market, valued at $300 million in 2024, is projected to reach $502 million by 2032, growing at a CAGR of 8.0% during the forecast period. Semiconductor laser bars, which combine multiple laser diodes for high-brightness and high-power outputs, are becoming indispensable in precision manufacturing and advanced medical procedures. The U.S. holds a dominant position, while China is emerging as a key market due to rapid industrialization and advancements in laser technology.

Other Trends

Optical Communications Fueling Market Growth

The surge in data traffic caused by 5G deployment and cloud computing is accelerating the demand for semiconductor lasers in optical communication networks. High-speed data transmission relies on efficient laser diodes, and advancements such as wavelength-division multiplexing (WDM) are pushing the boundaries of connectivity. The increasing preference for fiber-optic communications over traditional copper cables further underscores the critical role of semiconductor laser bars in modern infrastructure.

Technological Innovation in Laser Processing and Medical Applications

Laser processing, including cutting, welding, and additive manufacturing, is experiencing a paradigm shift due to improvements in semiconductor laser efficiency and precision. Medical applications, such as minimally invasive surgeries and aesthetic treatments, are also benefiting from enhanced laser systems. New developments, including compact laser bars with higher power densities, are expanding their use in photodynamic therapy and diagnostic imaging. Leading manufacturers like Coherent and ams Osram are investing in R&D to create next-generation laser solutions tailored for these high-growth sectors.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Investments and Technological Advancements Drive Market Competition

The global Semiconductor Laser Bar and Chip Market is characterized by intense competition, with a mix of established global players and emerging regional manufacturers vying for market share. Coherent leads the industry, leveraging its technological expertise in high-power laser diodes across applications like optical communications and laser processing. With recent acquisitions strengthening its market position, the company continues to dominate with innovative solutions tailored for industrial and medical sectors.

ams Osram and Jenoptik are also key competitors, holding significant shares due to their diversified product portfolios and strong presence in Europe and North America. These companies have focused on expanding their manufacturing capabilities to meet growing demand from the defense and photovoltaic sectors. Their investment in R&D for energy-efficient laser bars has further solidified their market positions.

Meanwhile, Chinese players such as Everbright Photonics and Shandong Huaguang Optoelectronic are rapidly gaining traction, particularly in the Asia-Pacific region. Their competitive pricing strategies and government-backed initiatives in semiconductor manufacturing have enabled them to capture a growing share of the mid-power segment (20-80W).

The market is witnessing increasing competition as companies pursue strategic partnerships and vertical integration. For instance, Quantel Laser (Lumibird) recently expanded its production capacity through acquisitions, while Wuhan Sintec Optronics has focused on developing specialized laser chips for medical applications.

List of Key Semiconductor Laser Bar and Chip Companies Profiled

- Coherent (U.S.)

- ams Osram (Germany)

- Jenoptik (Germany)

- Quantel Laser (Lumibird) (France)

- Everbright Photonics (China)

- Shandong Huaguang Optoelectronic (China)

- Wuhan Sintec Optronics (China)

- Lumispot (South Korea)

Segment Analysis:

By Type

High-Power Laser Bars (More Than 150W) Lead the Market Due to Applications in Industrial and Defense Sectors

The market is segmented based on type into:

- Less Than 20W

- 20-40W

- 40w-80W

- 80w-150W

- More Than 150W

By Application

Laser Processing Segment Dominates Owing to Increased Adoption in Material Cutting and Welding

The market is segmented based on application into:

- Optical Communications

- Medical Laser Equipment

- Laser Processing

- Photovoltaic Manufacturing

- Scientific Research

- Defense and Military

- Others

By Material

Gallium Arsenide (GaAs) Holds Significant Share Due to Superior Laser Efficiency

The market is segmented based on material into:

- Gallium Arsenide (GaAs)

- Indium Phosphide (InP)

- Gallium Nitride (GaN)

- Others

By End User

Industrial Sector Emerges as Key Consumer for Precision Manufacturing Applications

The market is segmented based on end user into:

- Industrial

- Healthcare

- Telecommunications

- Defense & Aerospace

- Research Institutions

Regional Analysis: Semiconductor Laser Bar and Chip Market

Asia-Pacific

The Asia-Pacific region dominates the global semiconductor laser bar and chip market, accounting for the largest revenue share. Rapid industrialization, technological advancements, and expanding applications in telecommunications, healthcare, and manufacturing drive this growth. China, Japan, and South Korea lead in semiconductor laser production, with China investing heavily in domestic manufacturing capabilities under initiatives like “Made in China 2025.” India’s expanding electronics sector and increasing government support for semiconductor manufacturing create new opportunities. The region benefits from strong supply chain integration, competitive manufacturing costs, and growing demand for high-power lasers in industrial applications.

North America

North America represents a technologically advanced market for semiconductor laser bars and chips, driven by substantial R&D investments and defense sector applications. The U.S. holds the largest market share in the region, with strong demand from aerospace, medical devices, and optical communications sectors. Silicon Valley remains a hub for laser innovation, while government contracts in defense laser systems provide steady market growth. Stringent quality standards encourage advanced product development, though high production costs limit price competitiveness against Asian manufacturers. The region shows particular strength in high-power laser chips for industrial and scientific applications.

Europe

Europe maintains a robust position in semiconductor laser technology, with Germany as the regional leader in precision laser manufacturing. The region excels in high-quality, specialized laser components for automotive, medical, and scientific research applications. EU environmental regulations influence product development toward energy-efficient solutions, while strong university-industry collaborations drive innovation in quantum technology applications. The market faces challenges from Asian price competition but maintains advantages in high-end niche applications. Key growth areas include photonics integration and emerging applications in lidar systems for autonomous vehicles.

South America

The semiconductor laser market in South America remains in development stages, with Brazil and Argentina showing most activity. Limited local manufacturing capacity creates reliance on imports, particularly from North America and Asia. The medical device industry represents the primary application area, while industrial adoption grows slowly due to economic constraints. Government initiatives to develop local tech industries show potential for future market expansion, though infrastructure limitations and inconsistent policy support hinder rapid growth. The region presents long-term opportunities as manufacturing capabilities gradually improve.

Middle East & Africa

This emerging market focuses primarily on laser applications in oil & gas, medical, and defense sectors. Israel stands out as a regional technology leader with specialized semiconductor laser capabilities, particularly for military applications. Gulf Cooperation Council countries invest in healthcare infrastructure, driving demand for medical laser systems. While the overall market remains small compared to other regions, strategic investments in technology parks and special economic zones lay foundations for future growth. Infrastructure limitations and reliance on imports currently restrict market expansion, though increasing digitalization initiatives may boost optical communication applications.

Report Scope

This market research report provides a comprehensive analysis of the global Semiconductor Laser Bar and Chip market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Semiconductor Laser Bar and Chip market was valued at USD 300 million in 2024 and is projected to reach USD 502 million by 2032, growing at a CAGR of 8.0%.

- Segmentation Analysis: Detailed breakdown by product type (Less Than 20W, 20-40W, 40W-80W, 80W-150W, More Than 150W) and application (Optical Communications, Medical Laser Equipment, Laser Processing, Photovoltaic Manufacturing, Scientific Research, Defense and Military, Others) to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. market is estimated at USD million in 2024, while China is projected to reach USD million by 2032.

- Competitive Landscape: Profiles of leading market participants including Coherent, ams Osram, Jenoptik, Quantel Laser (Lumibird), Everbright Photonics, Shandong Huaguang Optoelectronic, Wuhan Sintec Optronics, and Lumispot, covering their product portfolios, R&D focus, and recent developments.

- Technology Trends & Innovation: Assessment of emerging semiconductor laser technologies, integration with AI/IoT, and advancements in high-power laser applications.

- Market Drivers & Restraints: Evaluation of factors such as growing demand for laser processing in manufacturing, expansion of optical communication networks, and challenges related to supply chain constraints and regulatory compliance.

- Stakeholder Analysis: Strategic insights for component suppliers, OEMs, system integrators, and investors regarding market opportunities and competitive positioning.

Primary and secondary research methods are employed, including interviews with industry experts and analysis of verified market data, to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Semiconductor Laser Bar and Chip Market?

-> Semiconductor Laser Bar and Chip Market was valued at 300 million in 2024 and is projected to reach US$ 502 million by 2032, at a CAGR of 8.0% during the forecast period.

Which key companies operate in Global Semiconductor Laser Bar and Chip Market?

-> Key players include Coherent, ams Osram, Jenoptik, Quantel Laser (Lumibird), Everbright Photonics, Shandong Huaguang Optoelectronic, Wuhan Sintec Optronics, and Lumispot.

What are the key growth drivers?

-> Key growth drivers include increasing demand for high-power laser applications in manufacturing, expansion of fiber optic networks, and advancements in medical laser technologies.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing market, driven by manufacturing expansion in China and technological advancements in Japan and South Korea.

What are the emerging trends?

-> Emerging trends include development of ultra-high-power laser bars, integration with AI-driven control systems, and increasing adoption in photovoltaic manufacturing.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...