Semiconductor Circular Economy Market Insights

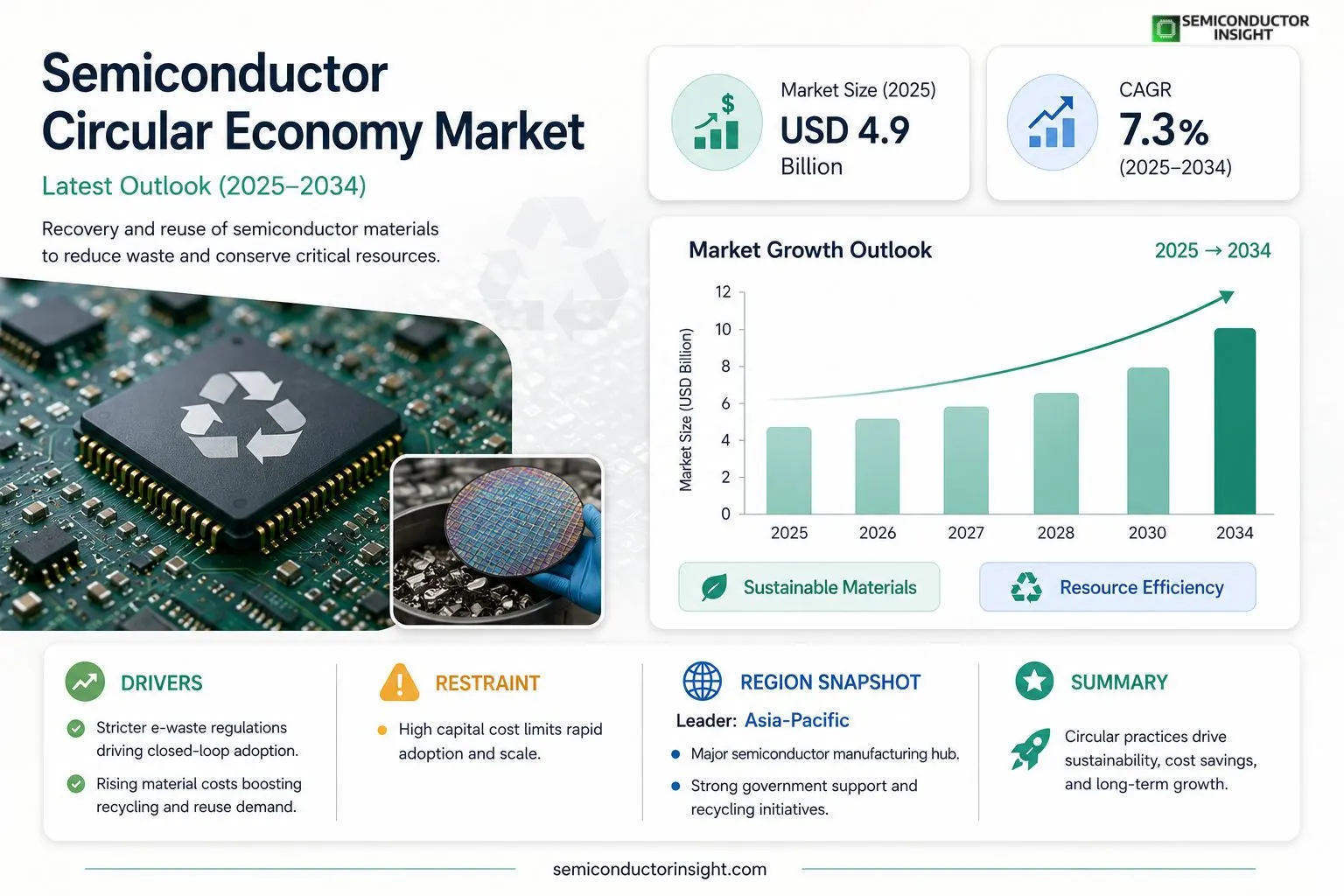

Global Semiconductor Circular Economy Market size was valued at USD 4.9 billion in 2025. The market is projected to grow from USD 5.1 billion in 2025 to USD 9.8 billion by 2034, exhibiting a CAGR of 7.3% during the forecast period.

The Semiconductor Circular Economy encompasses the systematic recovery, refurbishment, and reuse of semiconductor components and manufacturing waste,including silicon wafers, packaging materials, and rare‑earth metals,to minimize resource extraction and landfill disposal while maintaining product performance.The market is experiencing rapid expansion because stricter e‑waste regulations worldwide are driving manufacturers toward closed‑loop processes; however, rising material costs are prompting firms to adopt recycling technologies faster. Furthermore, advances in wafer‑level reclamation and the growing demand for sustainable electronics are fueling investment across the value chain.

MARKET DRIVERS

Regulatory Momentum Toward Circular Practices

The tightening of e‑waste regulations in North America, Europe, and parts of Asia is compelling semiconductor manufacturers to adopt closed‑loop processes. Companies are now required to achieve a minimum 30% material recovery rate, which is accelerating investments in re‑fabrication and remanufacturing facilities within Semiconductor Circular Economy Market.

Increasing Cost Pressures on Primary Materials

Silicon wafer prices have risen by roughly 8% year‑over‑year due to supply chain bottlenecks, prompting firms to explore reclaimed silicon and recycled rare‑earth components. This cost dynamic is driving a shift toward resource‑efficient design, thereby expanding the market’s growth trajectory.

➤ “By 2030, circular sourcing could offset up to 20% of new silicon demand, delivering annual savings of $4 billion for the industry.”

Adoption of advanced recycling technologies, such as hydrometallurgical leaching for noble metals, further underpins market expansion. These innovations enable higher purity recovery, positioning circular solutions as a competitive advantage for OEMs.

MARKET CHALLENGES

Technological Complexity of Semiconductor Recycling

Recovering high‑purity silicon and delicate photolithography layers requires precision processes that are still maturing. The lack of standardized recycling protocols leads to inconsistent yields, deterring smaller players from entering Semiconductor Circular Economy Market.

Other Challenges

Infrastructure Gaps

Existing e‑waste collection networks are not optimized for semiconductor‑specific streams, resulting in material loss during transport and sorting. Investment in dedicated collection hubs is essential to sustain growth.

MARKET RESTRAINTS

High Capital Expenditure for Circular Facilities

Establishing clean‑room compatible recycling lines demands capital outlays of $150 million–$200 million per plant. Many manufacturers hesitate to allocate such resources without clear short‑term ROI, limiting rapid market adoption.Additionally, the long payback period,often exceeding five years,creates financial restraint for companies focused on quarterly performance metrics.Regulatory compliance costs, including reporting and certification, further increase operational overhead, constraining smaller firms from participating fully in the circular ecosystem.

MARKET OPPORTUNITIES

Growth of Sustainable Design Services

Consultancies offering eco‑design and life‑cycle assessment are emerging as strategic partners. These services enable semiconductor firms to integrate circularity at the product development stage, unlocking new revenue streams and enhancing brand reputation.Furthermore, the rise of urban mining initiatives in high‑tech hubs presents an untapped source of reclaimed semiconductor components. Leveraging these secondary resources can reduce dependence on virgin material extraction.Finally, collaboration platforms that align manufacturers, recyclers, and end‑users are fostering data‑driven circular models. The resulting transparency accelerates material traceability, positioning Semiconductor Circular Economy Market for sustained long‑term growth.

Semiconductor Circular Economy Market Trends

Regulatory Push for Closed‑Loop Manufacturing

Semiconductor Circular Economy Market is being reshaped by an accelerating wave of e‑waste regulations that now require manufacturers to demonstrate closed‑loop handling of silicon wafers, packaging and rare‑earth components. In regions such as the European Union, China and North America, compliance checkpoints have moved from voluntary reporting to mandatory recovery targets, prompting fast‑track investments in on‑site refurbishing facilities. Companies are integrating traceability software to verify that each reclaimed component meets original performance specifications, thereby protecting brand reputation while reducing landfill disposal. This regulatory environment is also encouraging cross‑industry consortia that share best practices and develop standardized recycling protocols, creating a more predictable operating landscape for participants.

Other Trends

Wafer‑Level Reclamation Advances

A notable subtopic is the rapid maturation of wafer‑level reclamation technologies. Advanced chemical‑mechanical polishing and laser lift‑off processes now enable the extraction of up to 85 % of usable silicon from spent wafers, a figure that was below 60 % a few years ago. These reclaimed substrates are being re‑qualified for lower‑performance nodes, extending the useful life of high‑purity silicon and reducing the demand for virgin material. The cost advantage of in‑house reclamation is further amplified by decreasing reagent consumption and shorter turnaround times, making the approach economically attractive for mid‑size fabs seeking to improve sustainability metrics without compromising throughput.

Materials Recovery Strengthens Supply Chains

Another emerging trend focuses on the systematic recovery of rare‑earth metals and specialty packaging polymers that are critical to high‑performance chips. New hydrometallurgical and plasma‑based separation techniques allow for the selective extraction of neodymium, dysprosium and other strategic elements from end‑of‑life modules, supporting supply‑chain resilience in the face of geopolitical constraints. At the same time, manufacturers are redesigning chip packages with mono‑material constructs that simplify disassembly and improve recycling yields. Investment in these material‑recovery solutions is rising, driven by both cost‑avoidance motives and the growing expectation of investors that Semiconductor Circular Economy Market will align with broader ESG objectives.

COMPETITIVE LANDSCAPEKey Industry Players

Emerging Leaders and Growth Drivers in the Semiconductor Circular Economy

The market is dominated by a handful of vertically integrated semiconductor manufacturers that have invested heavily in closed‑loop recycling and wafer‑level reclamation programs. Intel, Samsung Electronics, and Taiwan Semiconductor Manufacturing Company (TSMC) lead the ecosystem because they control both front‑end fab capacity and downstream packaging, allowing them to capture scrap silicon, rare‑earth metals, and process chemicals for reuse. These giants have established dedicated circular‑economy units, partnered with material‑recovery firms, and disclosed ambitious e‑waste reduction targets that shape industry standards. Their scale also creates barriers to entry, as smaller firms must rely on third‑party services or niche specialization to participate in the circular supply chain.Beyond the dominant tier, a diverse cohort of specialist and mid‑size players is expanding the market breadth. Companies such as ASE Technology Holding, STMicroelectronics, Infineon Technologies, and Texas Instruments are developing proprietary refurbishment lines for legacy devices and leveraging modular packaging to extend product lifecycles. Meanwhile, niche recyclers and equipment providers,including Applied Materials, Lam Research, ASM International, and Heraeus,supply the critical processes that enable material recovery at wafer, die, and component levels. This layered structure fosters innovation, as each participant addresses distinct value‑chain gaps, from high‑purity metal extraction to low‑temperature cleaning technologies.

List of Key Semiconductor Circular Economy Companies Profiled

- Intel Corporation

- Samsung Electronics

- Taiwan Semiconductor Manufacturing Company (TSMC)

- ASE Technology Holding

- STMicroelectronics

- Infineon Technologies

- Texas Instruments

- Applied Materials

- Lam Research

- ASM International

- Heraeus Holding

- NXP Semiconductors

- ON Semiconductor

- GlobalFoundries

- Advanced Micro Devices (AMD)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Reclaimed Silicon Wafers are emerging as the dominant type because they enable manufacturers to sustain high‑performance device yields while dramatically reducing the demand for virgin silicon. • They integrate seamlessly into existing fab lines with minimal process adaptation. • Their reuse extends wafer lifecycles, fostering a closed‑loop ecosystem that aligns with evolving e‑waste regulations. • Clients appreciate the reliability of reclaimed wafers, which support continuous innovation in advanced node technologies. |

| By Application |

|

Integrated Circuit Manufacturing benefits most from circular practices because it consumes the largest volume of high‑purity silicon and associated chemicals. • Closed‑loop reclamation reduces material waste, supporting cost‑effective scaling of advanced nodes. • The approach enhances supply chain resilience by diversifying sources of critical inputs. • Industry partners cite improved environmental credentials as a strategic advantage in competitive market positioning. |

| By End User |

|

Consumer Electronics Manufacturers drive circular adoption to meet strict product‑take‑back mandates and brand sustainability goals. • They prioritize reclaimed wafers and packaging to reduce the ecological footprint of smartphones, wearables, and tablets. • Collaborative recycling programs with fabs enable rapid material reintegration, shortening product development cycles. • The sector views circularity as a differentiator that resonates with environmentally conscious end‑users. |

| By Lifecycle Stage |

|

Manufacturing Recovery stands out as the pivotal stage where most material value is reclaimed. • Advanced wafer‑level cleaning and de‑processing techniques preserve silicon integrity for subsequent fab runs. • Recovery of rare‑earth metals from spent packaging supplies critical inputs for next‑generation photonics. • Firms that excel at this stage build robust closed‑loop networks that mitigate raw‑material volatility. |

| By Material |

|

Silicon remains the cornerstone material, and its circular handling drives the broader market narrative. • Recycled silicon achieves comparable electrical performance, enabling seamless integration into high‑density chips. • The material’s abundance through reclamation reduces pressure on primary mining, aligning with global sustainability agendas. • Industry consortia underline silicon’s recyclability as a benchmark for assessing the overall maturity of the semiconductor circular economy. |

Regional Analysis: North America

North America

North America is witnessing significant advancements in technologies aimed at recovering valuable materials from end-of-life semiconductors. These methods range from traditional mechanical processes to more sophisticated chemical and thermal treatments. The development and scaling of these technologies are crucial for reducing reliance on virgin materials and minimizing environmental impact within Semiconductor Circular Economy Market.

A growing trend in North America is the adoption of “design for circularity” principles. This involves designing semiconductor devices with end-of-life considerations in mind, facilitating easier disassembly, material separation, and recycling. This proactive approach is gaining traction among leading semiconductor manufacturers seeking to enhance the sustainability of their products and comply with evolving environmental regulations.

Government policies and regulations in North America are playing a vital role in promoting Semiconductor Circular Economy Market. Extended producer responsibility (EPR) schemes and regulations on electronic waste management are encouraging manufacturers to take greater responsibility for the end-of-life management of their products. These regulatory frameworks are driving innovation and investment in circular economy solutions within the semiconductor sector.

Several industry consortia and collaborations are emerging in North America to accelerate the adoption of circular practices in the semiconductor industry. These initiatives bring together semiconductor manufacturers, equipment suppliers, recyclers, and research institutions to share knowledge, develop best practices, and collectively address the challenges of creating a circular economy for semiconductors.

Europe

Europe is actively shaping Semiconductor Circular Economy Market with a strong emphasis on environmental sustainability and resource efficiency. Driven by stringent regulations like the European Green Deal and the Waste Framework Directive, the region is investing heavily in innovative technologies for material recovery and recycling from end-of-life semiconductors. Several European countries are leading the way in developing circular economy strategies specific to the electronics sector, including policies promoting product durability, repairability, and recyclability. The focus extends beyond material recovery to encompass the entire product lifecycle, with efforts to optimize design for recyclability and extend product lifespans. Collaboration between industry, academia, and public authorities is central to achieving these goals, fostering the development of closed-loop systems and reducing the environmental footprint of the semiconductor industry. The European approach often prioritizes a holistic view of circularity, integrating environmental, social, and economic considerations.

Asia-Pacific

Asia-Pacific represents a dynamic and rapidly evolving landscape for Semiconductor Circular Economy Market. With a significant concentration of semiconductor manufacturing in countries like Taiwan, South Korea, and China, the region faces both challenges and opportunities in adopting circular practices. Government initiatives are increasingly emphasizing sustainability and resource security, prompting investments in recycling infrastructure and technology development. While the region’s semiconductor industry is characterized by high volumes of production, there is a growing awareness of the environmental impact of electronic waste. Strategies are emerging to improve material recovery rates and promote the responsible disposal of semiconductor waste. The focus is shifting towards building robust domestic recycling capabilities and fostering a circular economy ecosystem within the semiconductor value chain. Increased collaboration on international standards and knowledge sharing is also crucial for advancing Semiconductor Circular Economy Market in Asia-Pacific.

South America

Semiconductor Circular Economy Market in South America is in its nascent stages but presents significant long-term potential. Driven by the growth of the electronics industry and increasing awareness of environmental issues, there is a growing need for responsible e-waste management practices. While formal recycling infrastructure is still developing in many countries, there are emerging initiatives focused on collecting and recovering valuable materials from end-of-life electronics. The adoption of circular economy principles in the semiconductor sector is gradually gaining traction, with pilot projects exploring material recovery technologies. Addressing the challenges of informal e-waste recycling and promoting regulatory frameworks are key priorities for fostering the growth of Semiconductor Circular Economy Market in the region. International collaborations and technology transfer will play a vital role in accelerating this transition.

Middle East & Africa

Semiconductor Circular Economy Market in the Middle East & Africa is characterized by emerging opportunities and unique challenges. With growing investments in technology and infrastructure, the region is witnessing an increase in demand for semiconductors. However, formal e-waste management systems are still underdeveloped in many countries, posing a significant challenge to the circularity of the semiconductor industry. Government initiatives are beginning to focus on promoting responsible e-waste disposal and exploring the potential for material recovery. Adopting circular economy principles in the semiconductor sector requires addressing the lack of infrastructure, technical expertise, and regulatory frameworks. International collaborations and investments in recycling technologies are crucial for unlocking the potential of Semiconductor Circular Economy Market in this region.

Report Scope

This market research report provides a comprehensive analysis of the Semiconductor Circular Economy Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Semiconductor Circular Economy Market?

-> Global Semiconductor Circular Economy Market was valued at USD 4.9 billion in 2025 and is expected to reach USD 9.8 billion by 2034, with a CAGR of 7.3%.

Which key companies operate in Semiconductor Circular Economy Market?

-> Key players include leading semiconductor manufacturers and recycling technology providers.

What are the key growth drivers?

-> Key growth drivers include stricter e‑waste regulations, rising material costs, advances in wafer‑level reclamation, and growing demand for sustainable electronics.

Which region dominates the market?

-> Asia‑Pacific is a leading region due to its concentration of semiconductor manufacturing, while Europe also shows strong market presence.

What are the emerging trends?

-> Emerging trends include wafer‑level reclamation technologies, increased adoption of circular economy practices, and development of sustainable semiconductor manufacturing processes.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...