SDR-based passive radar exploiting DVB-T2 illuminator Market Insights

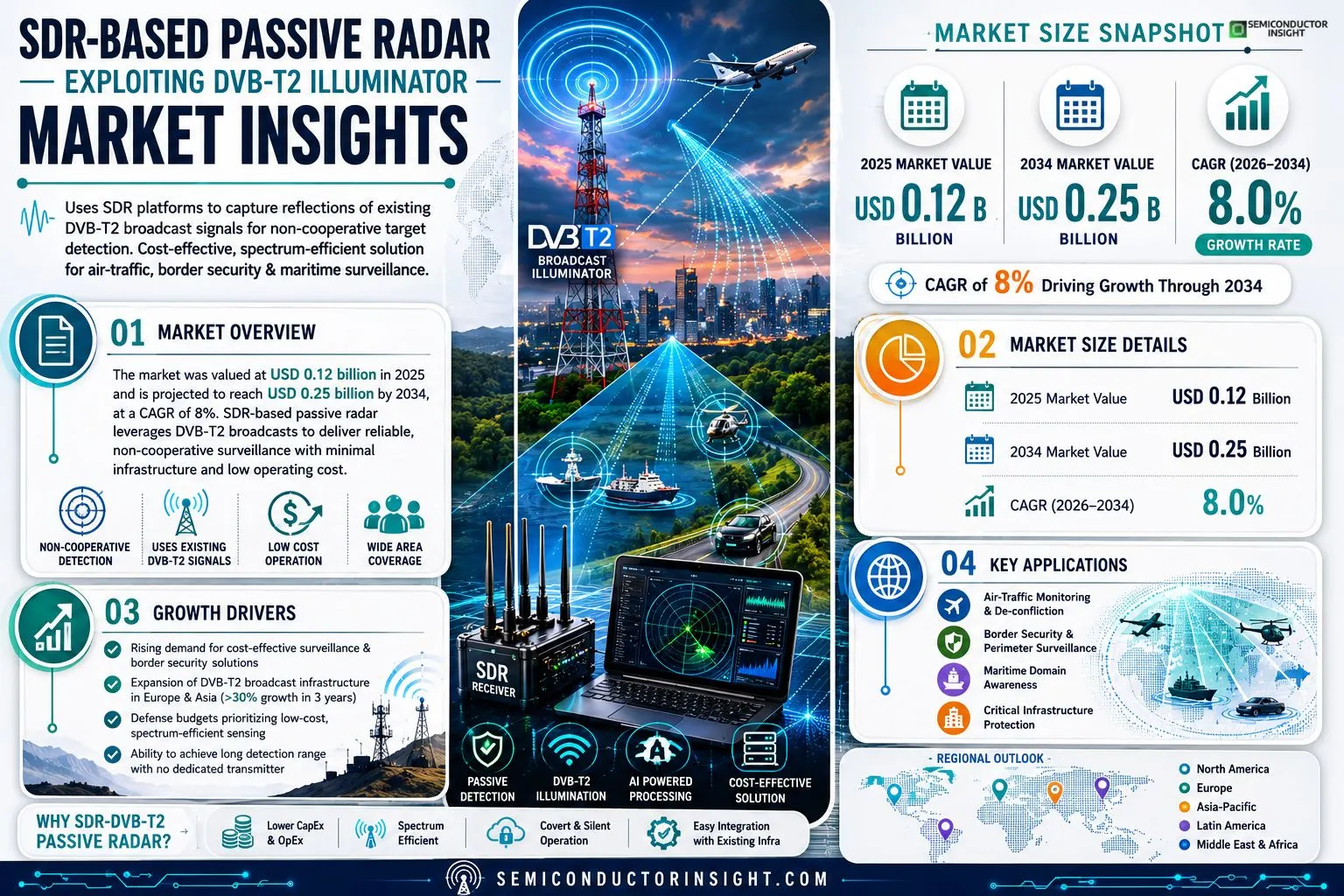

SDR-based passive radar exploiting DVB‑T2 illuminator market size was valued at USD 0.12 billion in 2025. The market is projected to grow from USD 0.12 billion in 2025 to USD 0.25 billion by 2034, exhibiting a CAGR of 8%.

This technology uses software‑defined radio platforms to capture reflections of existing DVB‑T₂ broadcast signals, enabling non‑cooperative target detection without transmitting its own waveform.By leveraging the extensive coverage of digital terrestrial television, it offers a cost‑effective solution for air‑traffic monitoring, border security, and maritime surveillance.The market accelerates because defense budgets are prioritising low‑cost, spectrum‑efficient sensing.

Additionally, the worldwide rollout of next‑generation DVB‑T₂ transmitters expands the illumination footprint.

Key players such as Rohde & Schwarz, Thales Group, Leonardo DRS and Hensoldt are advancing product development and partnering with telecom operators to embed radar capabilities into existing infrastructure.

MARKET DRIVERS

Growing Demand for Cost‑Effective Surveillance Solutions

SDR-based passive radar exploiting DVB‑T2 illuminator Market is benefiting from a surge in demand for low‑cost, high‑performance monitoring systems across border security, air traffic control, and smart‑city initiatives. Leveraging existing broadcast signals eliminates the need for dedicated transmitters, delivering significant cost savings for operators.

Increase in Broadcast Infrastructure Density

European and Asian deployments of DVB‑T2 networks have expanded by more than 30 % in the last three years, creating a denser grid of illuminators that passive radars can exploit. This infrastructure growth directly expands the geographic coverage and detection reliability of SDR‑based systems.

➤ “Passive radar architectures that reuse DVB‑T2 signals can achieve detection ranges comparable to traditional radars while operating at a fraction of the cost.”

These drivers collectively accelerate adoption, positioning the market for a compound annual growth rate that outpaces conventional radar segments.

MARKET CHALLENGES

Regulatory Uncertainty in Frequency Utilization

Regulators in several jurisdictions have yet to finalize rules for passive reception of DVB‑T2 streams for surveillance, raising compliance concerns for manufacturers and end‑users. The lack of clear guidance can delay project approvals and increase legal risk.

Other Challenges

Technical Integration

Integrating SDR hardware with existing command‑and‑control platforms often requires custom middleware, which adds development time and cost. Additionally, signal‑processing algorithms must adapt to varying broadcast conditions to maintain detection performance.

MARKET RESTRAINTS

Limited Commercial‑Grade SDR Platforms

While laboratory‑grade SDRs provide the necessary performance, few commercially‑ready models offer the ruggedness, temperature tolerance, and long‑term support demanded by field deployments, constraining large‑scale rollout.Supply chain constraints for high‑speed analog‑to‑digital converters further limit the availability of ready‑to‑use solutions, forcing many customers to rely on bespoke engineering efforts.

MARKET OPPORTUNITIES

Integration with AI‑Enhanced Target Classification

Embedding machine‑learning models into the signal‑processing chain can improve clutter rejection and enable real‑time classification of aerial threats, creating a differentiated value proposition for defense contractors.Partnerships between SDR manufacturers and cloud‑based analytics providers open pathways for scalable, subscription‑based services that lower upfront investment for end‑users.Emerging standards for secure broadcast metadata also present an opportunity to embed authentication tags, enhancing trust in passive radar data streams and expanding adoption in regulated air‑space environments.

SDR-based passive radar exploiting DVB-T2 illuminator Market Trends

Growth Driven by DVB‑T₂ Infrastructure Expansion

SDR-based passive radar exploiting DVB‑T₂ illuminator Market was valued at USD 0.12 billion in 2025 and is expected to reach USD 0.25 billion by 2034, reflecting an approximate annual growth rate of 8 percent. This expansion is anchored in the widespread deployment of next‑generation DVB‑T₂ broadcast transmitters, which create a dense illumination footprint across urban and coastal regions. By leveraging software‑defined radio platforms, the technology captures reflections of existing DVB‑T₂ signals, delivering non‑cooperative target detection without emitting its own waveform. The resulting cost‑efficiency and spectrum‑friendly operation align closely with defense budget priorities that emphasize low‑cost, high‑density sensing for air‑traffic monitoring, border security, and maritime surveillance. The growing emphasis on spectrum efficiency, combined with the ability to repurpose existing broadcast infrastructure, reduces both capital and operational expenditures. Moreover, regulatory trends favor shared spectrum use, encouraging governments to support passive radar initiatives. As a result, procurement cycles are shortening, and early adopters report improved detection coverage with minimal additional hardware.

Other Trends

Cost‑Effective Defense Applications

Cost‑effective defense applications have become a primary driver for adoption. SDR‑based solutions require only a receiver front‑end and modest processing hardware, reducing acquisition costs compared with traditional active radar systems that need high‑power transmitters. This financial advantage enables smaller nations and agencies to field robust situational‑awareness capabilities without large capital outlays. In addition, the passive nature of the system mitigates electromagnetic interference concerns, which is especially valuable in congested spectrum environments. Operational testing conducted in several European coastal zones has demonstrated reliable detection of low‑observable vessels at ranges exceeding 30 km, reinforcing the technology’s suitability for maritime domain awareness. Furthermore, the modular architecture permits incremental upgrades, allowing operators to scale system capacity in line with evolving threat environments. Training requirements are modest, as the user interface mirrors conventional radar displays, facilitating rapid crew assimilation.

Strategic Partnerships and Product Innovation

Strategic partnerships and product innovation are shaping the next phase of the SDR‑based passive radar exploiting DVB‑T₂ illuminator Market. Leading vendors such as Rohde & Schwarz, Thales Group, Leonardo DRS and Hensoldt are integrating radar processing modules into existing telecom infrastructure, collaborating with broadcast operators to embed sensing capability directly within transmission sites. These alliances accelerate time‑to‑market and expand the pool of available illumination sources. Concurrently, research programs focused on advanced signal‑processing algorithms are improving target discrimination and clutter suppression, further enhancing performance in dense urban environments. The combined effect of partnership‑driven deployment and technology refinement positions the market for sustained growth through the early 2030s. Market forecasts suggest that by 2030, over 60 percent of new border‑security projects will consider passive radar solutions as a baseline component. This shift underlines the technology’s transition from niche experimental deployments to mainstream operational platforms.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive overview of SDR‑based passive radar solutions leveraging DVB‑T2 broadcasts

SDR‑based passive radar market built around DVB‑T₂ illumination is currently dominated by a handful of legacy defense and test‑equipment manufacturers that have leveraged their RF‑front‑end expertise to develop specialised software‑defined solutions. Rohde & Schwarz leads the segment with its high‑performance SDR platforms that integrate tightly with DVB‑T₂ front‑ends, offering modular kits for air‑traffic monitoring and border surveillance. Thales Group follows, supplying end‑to‑end systems that combine signal‑processing algorithms with network‑centric data fusion, targeting NATO‑aligned users. Leonardo DRS contributes advanced sensor‑fusion software that enhances target classification, while Hensoldt focuses on compact, ruggedised receivers for maritime deployments. These incumbents benefit from established defence contracts, deep R&D budgets, and strategic partnerships with telecom operators that facilitate access to nationwide DVB‑T₂ transmitters, shaping a market structure characterised by high entry barriers and a clear tiered hierarchy between large integrators and emerging niche firms.Beyond the primary tier, a broader ecosystem of specialised firms is expanding the application envelope of DVB‑T₂‑based passive radar. Airbus Defence and Space delivers satellite‑linked processing nodes that enable cross‑border tracking over extensive geographic areas. BAE Systems and Saab Group are integrating passive radar modules into existing air‑defence platforms, leveraging their legacy radar portfolios to accelerate adoption. Raytheon Technologies and Lockheed Martin are exploring hybrid architectures that combine active and passive modes for resilient surveillance in contested spectra. Northrop Grumman’s research units focus on AI‑driven clutter suppression, while German test‑lab IABG provides validation services for emerging signal‑processing chains. QPS and Kongsberg Defence & Aerospace offer compact, export‑ready kits for maritime security, and L3Harris Technologies supplies ground‑station software that supports multi‑static configurations. Collectively, these players diversify the supply chain, foster niche innovation, and gradually lower the cost barrier for smaller operators.

List of Key SDR-based passive radar exploiting DVB-T2 illuminator Companies Profiled

- Rohde & Schwarz

- Thales Group

- Leonardo DRS

- Hensoldt

- Airbus Defence and Space

- BAE Systems

- Saab Group

- Raytheon Technologies

- Lockheed Martin

- Northrop Grumman

- IABG

- QPS

- Kongsberg Defence & Aerospace

- L3Harris Technologies

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Software‑centric SDR drives adoption because:

|

| By Application |

|

Air‑traffic monitoring emerges as the leading application because:

|

| By End User |

|

Defense agencies dominate due to:

|

| By Frequency Band |

|

L‑Band is the preferred spectrum segment because:

|

| By Deployment Mode |

|

Embedded telecom‑tower integration gains traction because:

|

Regional Analysis: Europe

Europe

The European defense sector is a significant end-user, with increasing adoption of SDR-based passive radar for border surveillance, coastal protection, and homeland security. The need for covert surveillance capabilities is driving investment in this technology.

The monitoring of critical infrastructure such as power grids, pipelines, and transportation networks is another key application area. SDR-based passive radar offers a non-intrusive method for detecting anomalies and potential threats.

Applications in environmental monitoring, such as tracking wildlife and detecting illegal activities in protected areas, are gaining traction. The passive nature of the technology minimizes disturbance to the monitored environment.

Civil security applications, including traffic management and public safety monitoring, are also contributing to the growth of the market. The ability to operate discreetly makes it suitable for various urban surveillance needs.

North America

North America exhibits a robust market for SDR-based passive radar exploiting DVB-T2 illuminator. Significant investments in technological advancements and a strong defense industry are propelling growth. The focus on enhancing border security and counter-terrorism efforts further drives demand. The United States, in particular, is a key market player with substantial research and development activities in this domain.

Asia-Pacific

The Asia-Pacific region is poised for significant growth, driven by rapid industrialization and increasing security concerns. Countries like China, India, and Japan are investing heavily in advanced surveillance technologies, creating a substantial opportunity for SDR-based passive radar. The affordability and ease of implementation of DVB-T2 illuminators are particularly attractive in this region.

South America

South America presents a moderately growing market, with increasing awareness of the benefits of passive radar technology. Government initiatives aimed at improving infrastructure security and combating illegal activities are contributing to market expansion. The region’s diverse geographical landscape creates various applications for this technology.

Middle East & Africa

The Middle East and Africa represent emerging markets with considerable potential. Growing security threats and increasing investments in defense and surveillance are driving demand for advanced radar solutions. The cost-effectiveness of SDR-based passive radar makes it an attractive option for these regions.

Report Scope

This market research report provides a comprehensive analysis of the SDR-based passive radar exploiting DVB-T2 illuminator Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high‑growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa, including country‑level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market‑entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real‑time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of SDR-based passive radar exploiting DVB-T2 illuminator Market?

-> SDR-based passive radar exploiting DVB-T2 illuminator Market was valued at USD 0.12 billion in 2025 and is expected to reach USD 0.25 billion by 2034.

Which key companies operate in SDR-based passive radar exploiting DVB-T2 illuminator Market?

-> Key players include Rohde & Schwarz, Thales Group, Leonardo DRS, and Hensoldt, among others.

What are the key growth drivers?

-> Key growth drivers include defense budget emphasis on low‑cost, spectrum‑efficient sensing, and the rollout of next‑generation DVB‑T2 transmitters expanding illumination footprints.

Which region dominates the market?

-> The reference material does not disclose a dominant region; the market is currently assessed at a level.

What are the emerging trends?

-> Emerging trends include integration of software‑defined radio platforms with existing DVB‑T2 broadcast infrastructure and strategic partnerships with telecom operators to embed radar capabilities.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...