MARKET INSIGHTS

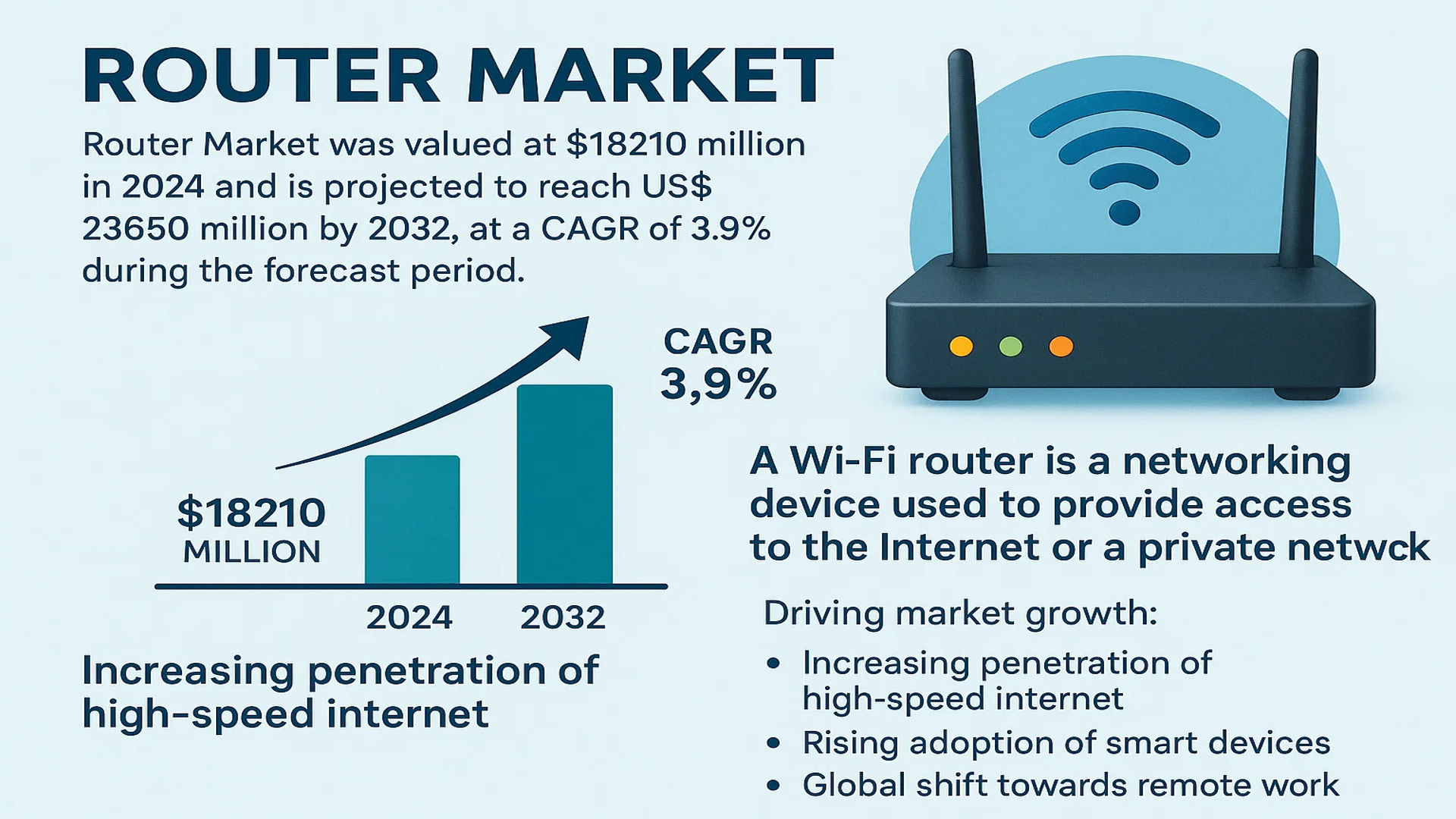

The global Router Market was valued at 18210 million in 2024 and is projected to reach US$ 23650 million by 2032, at a CAGR of 3.9% during the forecast period.

A router is a networking device that forwards data packets between computer networks. A Wi-Fi/wireless router performs the functions of a router and also includes the functions of a wireless access point. It is used to provide access to the Internet or a private computer network and can function in a wired LAN (local area network), in a wireless-only LAN (WLAN), or in a mixed wired/wireless network. These devices are critical for modern connectivity, enabling everything from basic web browsing to supporting complex smart home ecosystems and remote work infrastructures.

Market growth is primarily driven by the increasing penetration of high-speed internet, the rising adoption of smart devices, and the global shift towards remote work and digital entertainment. The United States is the largest market, accounting for over 40% of global revenue, due to high consumer spending on technology and advanced network infrastructure. However, the Asia-Pacific region, particularly China, is experiencing significant growth because of rapid digitalization and expanding e-commerce. Key players such as TP-LINK, NETGEAR, ASUS, D-Link, and Huawei dominate the competitive landscape, with the top five manufacturers collectively holding a market share exceeding 40%.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of High-Speed Internet and Smart Devices to Drive Router Demand

The global expansion of high-speed internet infrastructure, particularly the rollout of fiber-optic networks and 5G technology, is significantly boosting router market growth. With over 5.5 billion internet users worldwide and increasing penetration of smart homes, the demand for reliable, high-performance routers has surged. The average number of connected devices per household has risen to more than 10, requiring advanced routers capable of handling multiple simultaneous connections without compromising speed or stability. This trend is particularly pronounced in developed markets where smart home adoption rates exceed 40% of households, driving the need for routers with enhanced bandwidth capabilities and improved network management features.

Rising Remote Work and Digital Transformation Initiatives to Accelerate Market Expansion

The shift toward remote and hybrid work models has created sustained demand for enterprise-grade routers and advanced consumer models. Organizations worldwide are investing in robust network infrastructure to support secure remote access, video conferencing, and cloud-based applications. The enterprise router segment has witnessed particularly strong growth, with businesses upgrading their networks to accommodate distributed workforce requirements. This transformation extends beyond corporate environments to educational institutions, healthcare facilities, and government agencies, all requiring reliable networking solutions to maintain operational continuity and service delivery in increasingly digital environments.

Increasing Demand for Advanced Security Features to Stimulate Router Upgrades

Growing cybersecurity concerns are driving router manufacturers to integrate advanced security features directly into their devices. With cyber threats becoming more sophisticated and frequent, consumers and businesses are seeking routers with built-in firewall protection, VPN support, threat detection, and parental controls. The market has responded with routers featuring AI-powered security systems that can identify and block potential threats in real-time. This security-focused approach has become particularly important as more critical activities, including financial transactions and sensitive communications, are conducted over home and business networks, creating a compelling reason for users to upgrade to newer, more secure router models.

MARKET RESTRAINTS

Market Saturation and Extended Product Lifecycles to Limit Growth Potential

The router market faces significant challenges from product saturation in developed regions and extended replacement cycles. Many consumers and businesses retain routers for several years before upgrading, particularly when existing devices meet basic connectivity needs. This extended product lifecycle, often ranging from three to five years, creates natural limitations on market expansion. Additionally, in mature markets where router penetration approaches 90% of households, growth depends primarily on replacement sales rather than new customer acquisition, creating a more competitive environment where manufacturers must convince users to upgrade rather than simply purchasing their first router.

Price Sensitivity and Intense Competition to Constrain Profit Margins

Intense competition among router manufacturers, particularly in the consumer segment, has led to significant price pressure and shrinking profit margins. The market is characterized by numerous players offering similar specifications at increasingly competitive price points, making it challenging for companies to maintain profitability while investing in research and development. This price sensitivity is particularly evident in emerging markets where consumers prioritize affordability over advanced features. Manufacturers must balance cost considerations with the need to incorporate newer technologies such as Wi-Fi 6 and mesh networking capabilities, creating complex pricing strategies that can impact overall market revenue growth.

Technical Complexity and Interoperability Issues to Hinder Market Adoption

Increasing technical complexity presents challenges for both consumers and network administrators. The proliferation of networking standards, frequency bands, and compatibility requirements creates confusion among non-technical users, potentially delaying purchase decisions or leading to suboptimal product choices. Interoperability issues between routers and various internet service providers’ equipment further complicate the user experience. Additionally, the integration of routers with smart home ecosystems and IoT devices requires seamless compatibility that is not always achieved, creating frustration and potentially limiting the adoption of more advanced router models that promise enhanced connectivity but deliver complex setup processes.

MARKET CHALLENGES

Rapid Technological Obsolescence and Standard Evolution to Challenge Market Stability

The router industry faces continuous challenges from rapidly evolving technology standards and the constant threat of product obsolescence. The transition from Wi-Fi 5 to Wi-Fi 6 and the emerging development of Wi-Fi 7 create a environment where products can become outdated within relatively short timeframes. This rapid standard evolution requires manufacturers to constantly innovate while managing inventory of previous-generation products. Consumers face decision paralysis when choosing routers, uncertain whether to invest in current technology or wait for next-generation standards, potentially delaying purchases and creating sales volatility within the market.

Other Challenges

Supply Chain Disruptions

Global supply chain vulnerabilities have impacted router manufacturing and distribution, causing production delays and component shortages. The reliance on semiconductor components, which have experienced significant supply constraints, has affected router availability and increased manufacturing costs. These disruptions have forced manufacturers to reassess their supply chain strategies and inventory management approaches, creating operational challenges that can affect product availability and pricing stability across the market.

Regulatory Compliance

Router manufacturers must navigate complex regulatory environments across different regions and countries. Compliance with various radio frequency regulations, safety standards, and environmental requirements adds complexity to product development and distribution. These regulatory hurdles can delay product launches and increase development costs, particularly for companies operating in multiple international markets with differing requirements and certification processes.

MARKET OPPORTUNITIES

Emergence of IoT and Smart City Infrastructure to Create New Growth Avenues

The expansion of Internet of Things applications and smart city initiatives presents significant opportunities for router manufacturers. As cities worldwide deploy connected infrastructure for traffic management, public safety, and utility monitoring, the demand for industrial-grade routers capable of supporting numerous connected devices in harsh environments is increasing. Similarly, the proliferation of IoT devices in residential settings, expected to exceed 25 billion connected devices globally, requires routers with enhanced capacity and management capabilities. This trend is driving innovation in router design, with manufacturers developing specialized products for various IoT applications across consumer, commercial, and municipal sectors.

Development of Value-Added Services and Subscription Models to Enhance Revenue Streams

Router manufacturers are increasingly exploring revenue opportunities beyond hardware sales through value-added services and subscription models. Advanced security features, parental controls, network optimization services, and cloud management platforms represent potential recurring revenue streams that can complement traditional hardware sales. This approach allows manufacturers to maintain customer relationships beyond the initial purchase and create ongoing value propositions. The service-based model also helps differentiate products in a competitive market and provides consumers with continuously updated features and protection against evolving cyber threats.

Expansion into Emerging Markets and Rural Connectivity Initiatives to Drive Future Growth

Significant growth opportunities exist in emerging markets where internet penetration continues to increase and rural connectivity initiatives are expanding network access. Governments worldwide are investing in broadband infrastructure projects aimed at connecting underserved communities, creating demand for reliable networking equipment. These markets often require routers specifically designed for challenging environmental conditions and limited technical support availability. Manufacturers developing products tailored to these unique requirements can capture market share in regions experiencing rapid digital transformation and increasing disposable income among growing middle-class populations.

ROUTER MARKET TRENDS

Wi-Fi 6 and 6E Adoption to Emerge as a Dominant Trend in the Market

The global router market is undergoing a significant transformation driven by the accelerated adoption of Wi-Fi 6 (802.11ax) and Wi-Fi 6E standards. This shift is primarily fueled by the exponential growth in connected devices per household and the increasing demand for high-bandwidth applications such as 4K/8K video streaming, cloud gaming, and smart home ecosystems. Wi-Fi 6 offers substantial improvements over its predecessor, including higher data rates, increased capacity, better performance in dense environments, and improved power efficiency. The extension into the 6 GHz band with Wi-Fi 6E is particularly crucial, as it provides a massive, uncongested spectrum that alleviates network congestion, a persistent challenge in the 2.4 GHz and 5 GHz bands. This technological evolution is not merely an incremental update but a fundamental enhancement necessary to support the modern digital lifestyle, prompting both consumers and enterprises to upgrade their networking infrastructure. Consequently, manufacturers are rapidly pivoting their product portfolios, with over 60% of new router models launched in the last 18 months supporting these advanced standards, signaling a strong and sustained market trend.

Other Trends

Integration of AI and Machine Learning for Network Optimization

A pivotal trend reshaping the router landscape is the deep integration of Artificial Intelligence (AI) and Machine Learning (ML) to create smarter, self-optimizing home and office networks. Modern routers are increasingly equipped with AI-driven software that can automatically manage bandwidth allocation, prioritize traffic for latency-sensitive applications like video conferencing or online gaming, and identify and mitigate potential security threats in real-time. These systems learn from network usage patterns to predict peak times and preemptively adjust settings to maintain consistent performance. Furthermore, AI-enhanced mesh networking systems can dynamically select the fastest pathways for data transmission between nodes, ensuring seamless coverage throughout a property. This shift from manual configuration to autonomous network management is a key value proposition for consumers seeking a hassle-free, high-performance internet experience, making it a major driver for premium product segments within the market.

Rising Demand for Secure and Scalable Networking Solutions for SOHO

The structural shift towards hybrid and remote work models has fundamentally altered demand dynamics, creating a robust market for routers tailored to the Small Office/Home Office (SOHO) segment. This user base requires enterprise-grade security features, such as integrated VPN support, advanced threat protection, and secure guest networking capabilities, previously found only in corporate hardware. There is a growing emphasis on routers that offer scalable performance to support multiple simultaneous video calls, large file transfers, and access to corporate cloud resources without compromising stability. This trend is complemented by the proliferation of smart home devices, which necessitates a router that can reliably manage dozens of connected endpoints. The convergence of professional and personal networking needs within a single device is compelling manufacturers to innovate rapidly, blending user-friendly interfaces with powerful, professional-grade functionality to capture this expanding and highly valuable market segment.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Focus on Innovation and Strategic Expansion to Maintain Market Position

The global router market exhibits a semi-consolidated structure, characterized by a mix of large multinational corporations and smaller regional players competing intensely. TP-LINK stands as a dominant force, largely attributable to its extensive and diverse product portfolio that caters to both consumer and commercial segments, alongside a robust distribution network spanning North America, Europe, and Asia-Pacific. The company’s aggressive pricing strategy and consistent innovation in Wi-Fi 6 and Wi-Fi 7 technologies have solidified its leadership, contributing significantly to its estimated market share of over 15% in 2024.

NETGEAR and ASUS also command substantial market presence, particularly in the mid-to-high-end consumer and prosumer segments. Their growth is propelled by a strong emphasis on gaming routers and mesh networking systems, which address the rising demand for low-latency and whole-home coverage. Both companies have leveraged their brand reputation for performance and reliability to capture a loyal customer base, with NETGEAR’s Nighthawk series and ASUS’s ROG (Republic of Gamers) line being notable examples of successful product differentiation.

Furthermore, these industry leaders are actively pursuing growth through strategic initiatives, including geographical expansion into emerging markets and continuous new product launches featuring advanced security protocols and IoT integration. Such moves are anticipated to further consolidate their market positions throughout the forecast period.

Meanwhile, companies like Huawei and Xiaomi are strengthening their global footprint through significant investments in research and development, particularly in 5G and AI-driven network optimization. Their competitive pricing and rapidly improving technological capabilities allow them to challenge established players, especially in the Asia-Pacific region. Their approach often involves forming strategic partnerships with telecom service providers to offer bundled solutions, ensuring sustained growth within an increasingly connected landscape.

List of Key Router Companies Profiled

- TP-LINK (China)

- D-Link Corporation (Taiwan)

- Tenda Technology (China)

- NETGEAR, Inc. (U.S.)

- ASUSTek Computer Inc. (Taiwan)

- Huawei Technologies Co., Ltd. (China)

- Qihoo 360 Technology Co. Ltd. (China)

- Gee Technology Co., Ltd. (China)

- Xiaomi Corporation (China)

Segment Analysis:

By Type

Wireless Router Segment Dominates the Market Due to Proliferation of Smart Devices and IoT Ecosystems

The market is segmented based on type into:

- Wireless Routers

- Subtypes: Single-band, Dual-band, Tri-band

- Wired Routers

- Edge Routers

- Core Routers

- Virtual Routers

By Application

Consumer Use Segment Leads Due to Exponential Growth in Remote Work and Online Entertainment

The market is segmented based on application into:

- Consumer Use

- Subtypes: Home networking, Gaming, Streaming

- Commercial Use

- Subtypes: Small & Medium Enterprises, Large Enterprises

- Service Provider

- Data Centers

By Speed

High-Speed Segments Gain Traction to Support Bandwidth-Intensive Applications and 4K/8K Streaming

The market is segmented based on speed into:

- 150Mbps

- 300Mbps

- 450Mbps

- Above 1Gbps

- Others

By Distribution Channel

Online Retail Segment Expands Rapidly Owing to E-commerce Penetration and Direct-to-Consumer Models

The market is segmented based on distribution channel into:

- Online Retail

- Subtypes: E-commerce platforms, Brand websites

- Offline Retail

- Subtypes: Electronics stores, Specialty stores, Hypermarkets

- Direct Sales

- Value-Added Resellers

Regional Analysis: Router Market

North America

The North American router market, led by the United States which holds over 40% of the global market share, is characterized by high consumer spending power and rapid technological adoption. Demand is primarily driven by the widespread need for reliable, high-speed internet connectivity for both home office and entertainment applications. The shift towards Wi-Fi 6 and Wi-Fi 6E compatible routers is significant, fueled by the increasing number of connected devices per household and the growing prevalence of remote work. Major players like NETGEAR and TP-LINK have a strong presence, competing through innovation in mesh networking systems and advanced security features. While the market is mature, consistent upgrades to home networking infrastructure and the rollout of fiber-optic services by telecom providers continue to sustain steady growth.

Europe

Europe represents a sophisticated and well-established router market, with stringent regulations on product standards and data security influencing manufacturing and consumer preferences. Countries like Germany, the U.K., and France show robust demand for high-performance routers that support seamless connectivity for smart home ecosystems and professional home offices. The market is highly competitive, with a mix of global giants like ASUS and D-Link and strong regional brands. A key trend is the growing consumer awareness of cybersecurity, leading to increased demand for routers with built-in, subscription-based security software. Furthermore, environmental directives are pushing manufacturers toward more energy-efficient designs and sustainable packaging, adding a new dimension to product development in the region.

Asia-Pacific

As the largest volume market globally, the Asia-Pacific region is a powerhouse of router production and consumption. This dominance is largely driven by China, a major manufacturing hub for key brands like TP-LINK, Huawei, and Xiaomi, and a massive domestic market. The region exhibits a dual nature: a highly competitive budget segment with a focus on value-for-money 300Mbps and 450Mbps models, and a rapidly growing premium segment adopting advanced Wi-Fi 6 routers. The expansion of broadband infrastructure, particularly in India and Southeast Asia, is a primary growth driver, bringing millions of new users online. However, the market is also marked by intense price competition and a diverse range of consumer needs, from basic connectivity to high-bandwidth gaming and streaming applications.

South America

The router market in South America is in a growth phase, though it is susceptible to regional economic fluctuations. Countries like Brazil and Argentina are the main contributors, with market expansion tied to increasing internet penetration and the gradual modernization of telecom networks. Consumer purchasing decisions are often heavily influenced by price sensitivity, making the 150Mbps to 450Mbps segments particularly popular. While international brands have a footprint, local distribution channels and affordability are critical for success. Challenges include economic volatility, which can impact consumer electronics spending, and inconsistent broadband service quality in certain areas, which can dampen the demand for high-end router hardware. Nonetheless, the long-term outlook remains positive as digitalization efforts continue.

Middle East & Africa

This region presents an emerging but promising market for routers, characterized by significant variation in development between nations. Gulf Cooperation Council (GCC) countries like Saudi Arabia and the UAE have advanced, high-spending markets with demand for premium, feature-rich routers aligned with smart city initiatives and high disposable incomes. In contrast, other parts of Africa are focused on improving basic connectivity, where affordable and durable routers are essential. The overall growth is fueled by large-scale investments in national broadband projects and a young, increasingly digital-savvy population. While the market share is currently smaller than other regions, the potential for expansion is substantial as infrastructure develops and internet accessibility becomes more widespread across the continent.

Report Scope

This market research report provides a comprehensive analysis of the global Router market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Router Market?

-> Router Market was valued at 18210 million in 2024 and is projected to reach US$ 23650 million by 2032, at a CAGR of 3.9% during the forecast period.

Which key companies operate in Global Router Market?

-> Key players include TP-LINK, D-Link, Tenda, NETGEAR, ASUS, Huawei, Qihoo 360, Gee, and Xiaomi, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for high-speed internet, proliferation of smart devices, growth in remote work and online entertainment, and increasing investments in 5G infrastructure.

Which region dominates the market?

-> North America is the largest market, with a share over 40%, while Asia-Pacific is the fastest-growing region.

What are the emerging trends?

-> Emerging trends include Wi-Fi 6 and Wi-Fi 7 adoption, integration of AI for network optimization, increased focus on cybersecurity features, and the development of mesh networking systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...