MARKET INSIGHTS

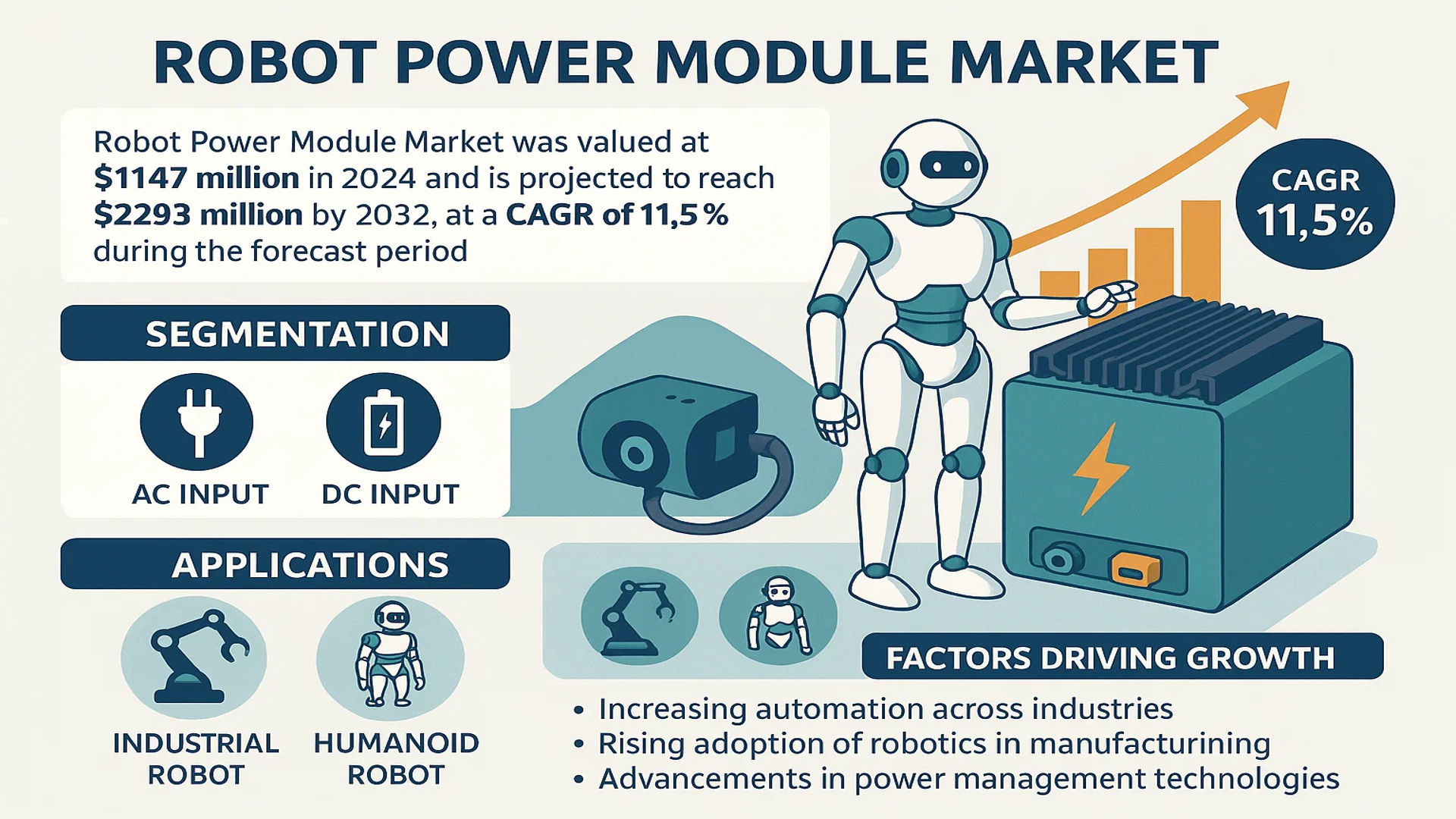

The global Robot Power Module Market was valued at 1147 million in 2024 and is projected to reach US$ 2293 million by 2032, at a CAGR of 11.5% during the forecast period.

A robot power module is a critical electronic component designed to supply, regulate, and manage power efficiently for robotic systems. These modules ensure stable and reliable energy distribution for essential robotic functions, including motion control, sensing, data processing, and communication. The modules are segmented into AC input and DC input types, catering to diverse robotic applications such as industrial robots and humanoid robots.

The market growth is driven by increasing automation across industries, rising adoption of robotics in manufacturing, and advancements in power management technologies. Furthermore, the growing demand for high-performance robotic solutions in sectors like automotive, healthcare, and logistics is accelerating market expansion. Key players such as Yaskawa, NACT, Vicor, and TDK-Lambda dominate the market with their innovative product portfolios and strategic collaborations. For instance, Yaskawa’s latest modular power solutions have significantly enhanced energy efficiency in industrial robotics, reinforcing its market leadership.

MARKET DYNAMICS

MARKET DRIVERS

Rising Industrial Automation Adoption to Fuel Robot Power Module Demand

The global surge in industrial automation is accelerating the adoption of robotic systems across manufacturing, logistics, and healthcare sectors, directly driving demand for robot power modules. These critical components ensure reliable energy distribution in automated environments where operational uptime is paramount. Recent industry trends show that over 3.2 million industrial robots are expected to be operational worldwide by 2026, creating substantial opportunities for power module manufacturers. The transition towards Industry 4.0 implementations, particularly in automotive and electronics manufacturing where precision and continuous operation are non-negotiable, makes stable power management solutions indispensable.

Advancements in Humanoid Robotics Creating New Application Frontiers

Technological breakthroughs in bipedal locomotion and AI integration are expanding humanoid robot applications beyond traditional industrial uses into service sectors such as healthcare assistance and customer interaction. This diversification is generating need for compact, high-efficiency power modules capable of supporting complex motion systems and onboard computing. The humanoid robotics segment is projected to grow at 38% annually as prototypes transition to commercial deployment. Leading robotics firms are collaborating with power electronics specialists to develop customized modules that balance energy density with thermal management challenges inherent in mobile platforms.

Furthermore, government initiatives supporting robotics adoption in hazardous environments and defense applications are providing additional market momentum. Several national robotics development programs now mandate the inclusion of redundant power systems for critical operations, creating premium opportunities for advanced module designs.

MARKET RESTRAINTS

Supply Chain Vulnerabilities in Semiconductor Components Creating Bottlenecks

The robot power module market faces persistent challenges from global semiconductor shortages affecting critical components like power MOSFETs and gate drivers. Industry analysis indicates 28% of robotics manufacturers experienced production delays in recent years due to power electronics component scarcity. These constraints are particularly acute for specialized modules requiring radiation-hardened or high-temperature rated semiconductors. The complex interdependencies in electronics manufacturing have made power module lead times unpredictable, with some high-performance variants facing 40+ week delivery timelines.

Operational Challenges

Thermal Management Limitations

Power density requirements in modern robotics push thermal dissipation capabilities to their limits, restricting module miniaturization. Excessive heat generation can degrade performance by up to 15% in continuous operation scenarios common in industrial applications.

Standardization Fragmentation

The absence of universal interface standards across robotics platforms forces module manufacturers to maintain extensive product variants, increasing inventory costs by an estimated 22% compared to more standardized power electronics segments.

MARKET OPPORTUNITIES

Emerging Wide Bandgap Semiconductor Adoption to Revolutionize Power Density

The transition from silicon to silicon carbide and gallium nitride semiconductors in power modules presents transformative potential for robotics applications. These materials enable 50% smaller module footprints while improving energy efficiency by up to 30%, addressing two critical constraints in mobile robotics. Early adopters in collaborative robotics are already reporting 40% longer operational durations between charges in battery-powered systems. The military robotics sector is driving demand for radiation-tolerant wide bandgap modules capable of withstanding extreme environments.

Additionally, the integration of predictive maintenance capabilities through embedded sensors creates value-added opportunities. Smart modules capable of monitoring capacitor health and predicting failure events weeks in advance could reduce robotic system downtime by over 60% in industrial settings. Several leading manufacturers have begun incorporating IoT connectivity features directly into power modules to enable this functionality.

Market leaders are also capitalizing on the shift towards modular robotic architectures by developing configurable power systems. These allow end-users to combine multiple power modules like building blocks to match specific voltage and current requirements, reducing development cycles for customized robotic solutions.

ROBOT POWER MODULE MARKET TRENDS

Advancements in AI-Driven Robotics Fueling Demand for High-Efficiency Power Modules

The rapid proliferation of artificial intelligence (AI) in robotics has necessitated the development of high-efficiency power modules capable of supporting complex computational and mechanical tasks. Modern robotic applications, ranging from industrial automation to humanoid service robots, require power modules that not only deliver consistent energy but also optimize power consumption through intelligent regulation. The integration of IoT and edge computing in robotics further amplifies this need, as real-time data processing demands stable and uninterrupted power supply. In response, manufacturers are investing in modular, scalable power solutions that enhance energy efficiency while reducing thermal losses.

Other Trends

Shift Toward Customizable and Modular Power Solutions

The increasing adoption of collaborative robots (cobots) in manufacturing and logistics has led to a surge in demand for customizable power modules. Unlike traditional industrial robots, cobots require compact, lightweight power solutions that can be tailored to diverse operational environments. Modular designs, which allow for easy upgrades and maintenance, are gaining traction, particularly in industries with rapidly evolving technological needs. This trend is further supported by the rising emphasis on minimizing downtime and increasing operational flexibility in automated production lines.

Growth in Industrial Automation and Smart Factories

The global push toward Industry 4.0 and smart factories is significantly accelerating the demand for robot power modules, particularly in regions like Asia-Pacific and North America. Industrial robots, which account for over 60% of the market’s power module applications, rely on robust power management systems to perform high-precision tasks such as welding, assembly, and material handling. The rise of 5G-enabled smart factories is also prompting manufacturers to invest in next-generation power modules with enhanced connectivity and energy optimization capabilities. These modules are critical in ensuring seamless communication between robotic systems and centralized control units, thereby improving overall productivity.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Drive Market Competition

The global Robot Power Module market features a dynamic and evolving competitive landscape with Yaskawa emerging as a dominant player, leveraging its extensive experience in robotics and power electronics. The company’s strong foothold in industrial automation and continuous product innovation has solidified its market leadership, particularly in regions like Asia and North America.

Vicor Corporation and TDK-Lambda also command significant shares, driven by their advanced power conversion technologies tailored for high-performance robotic applications. Their ability to deliver efficient and compact power solutions has positioned them as preferred suppliers for industrial and collaborative robots worldwide.

Meanwhile, mid-sized players such as Lead-Win and Shenzhen Jichuang Robot Technology are rapidly gaining traction through cost-effective solutions and localized manufacturing advantages. These companies are increasingly focusing on emerging economies—China especially—where demand for automation is accelerating.

Furthermore, the competitive environment is intensifying as established firms like NACT and RRC Power Solutions invest in R&D to develop next-generation power modules with higher efficiency and thermal stability. Strategic acquisitions and partnerships are also shaping the sector, with companies aiming to expand their technological capabilities and geographic reach.

List of Key Robot Power Module Companies Profiled

- Yaskawa (Japan)

- NACT (U.S.)

- RoboMaster (China)

- Vicor Corporation (U.S.)

- RRC POWER SOLUTIONS COMPANY LIMITED (China)

- TDK-Lambda (Japan)

- Lead-Win (China)

- Shenzhen Jichuang Robot Technology Co., Ltd (China)

Segment Analysis:

By Type

AC Input Segment Dominates Due to Widespread Industrial Adoption

The market is segmented based on type into:

- AC Input

- Subtypes: Single-phase and Three-phase

- DC Input

- Subtypes: High-voltage and Low-voltage

- Hybrid

By Application

Industrial Robot Segment Holds Major Share Owing to Increased Automation in Manufacturing

The market is segmented based on application into:

- Industrial Robot

- Subtypes: Articulated, SCARA, Cartesian, and Others

- Humanoid Robot

- Service Robot

By Power Rating

Medium Power Range (1-10kW) Accounts for Significant Market Share

The market is segmented based on power rating into:

- Low Power (<1kW)

- Medium Power (1-10kW)

- High Power (>10kW)

By End-User Industry

Automotive Sector Leads in Adoption Due to Heavy Robot Utilization

The market is segmented based on end-user industry into:

- Automotive

- Electronics

- Healthcare

- Logistics

- Others

Regional Analysis: Robot Power Module Market

Asia-Pacific

The Asia-Pacific region dominates the global Robot Power Module market, with China, Japan, and South Korea leading in both production and adoption. Rapid industrialization, government initiatives like China’s “Made in China 2025,” and heavy investments in automation drive demand for high-efficiency power modules. Japan’s precision robotics and South Korea’s technological advancements in AI-powered robotics further solidify the region’s leadership. The presence of key players such as Yaskawa and TDK-Lambda strengthens the supply chain. Additionally, manufacturing hubs in India and Southeast Asia are increasingly adopting robotic solutions, creating a robust growth trajectory for power modules. However, cost sensitivity in emerging markets remains a challenge for premium product adoption.

North America

North America represents a high-growth region for Robot Power Modules, propelled by the U.S.’s strong robotics ecosystem and Industry 4.0 advancements. The region prioritizes innovation, with significant R&D investments in collaborative and industrial robots from companies like Vicor and NACT. Defense and aerospace applications also contribute to market expansion, given the stringent power efficiency and reliability requirements. Canada’s focus on sustainable manufacturing further fuels demand. Regulatory emphasis on energy-efficient systems and automation in logistics (e.g., warehouse robotics) ensures steady market growth, though higher production costs remain a restraint for local manufacturers.

Europe

Europe’s Robot Power Module market thrives on strict efficiency standards and automation adoption in automotive and pharmaceutical industries. Germany, as a manufacturing powerhouse, leads demand for modular and scalable power solutions compatible with industrial robots. The EU’s emphasis on green manufacturing encourages innovations in low-power-consumption modules. Collaborative robotics—especially in Scandinavia—fuels niche opportunities. However, slower adoption rates in Southern Europe due to economic constraints and fragmented regulations pose challenges. Companies like RRC POWER SOLUTIONS COMPANY LIMITED are capitalizing on the region’s technical requirements, offering customized solutions.

South America

South America shows gradual but promising growth, with Brazil and Argentina as focal points. Increasing automation in agriculture (e.g., agribots) and mining drives demand for rugged power modules. Local manufacturing is limited, relying heavily on imports from Asia and North America. While economic instability delays large-scale investments, government initiatives to modernize industries offer long-term potential. The lack of localized technical expertise and higher import duties hinder faster adoption, but the market is poised for incremental growth as industries prioritize efficiency.

Middle East & Africa

This emerging market is fueled by infrastructure development and smart city projects in the UAE and Saudi Arabia. Robotics adoption in oil & gas and logistics presents opportunities for high-durability power modules. However, low awareness of advanced robotics and reliance on foreign suppliers slow market penetration. Africa’s nascent industrial automation sector shows potential, particularly in South Africa, but funding gaps and underdeveloped supply chains limit immediate growth. Strategic partnerships with global players could accelerate regional market development in the long term.

Report Scope

This market research report provides a comprehensive analysis of the Global Robot Power Module Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 1,147 million in 2024 and is projected to reach USD 2,293 million by 2032, growing at a CAGR of 11.5%.

- Segmentation Analysis: Detailed breakdown by product type (AC Input, DC Input), application (Industrial Robot, Humanoid Robot), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. The U.S. and China are key markets with significant growth potential.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships. Key players include Yaskawa, NACT, RoboMaster, Vicor, and TDK-Lambda.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of the Global Robot Power Module Market?

->Robot Power Module Market was valued at 1147 million in 2024 and is projected to reach US$ 2293 million by 2032, at a CAGR of 11.5% during the forecast period.

Which key companies operate in the Global Robot Power Module Market?

-> Key players include Yaskawa, NACT, RoboMaster, Vicor, RRC POWER SOLUTIONS COMPANY LIMITED, TDK-Lambda, Lead-Win, and Shenzhen Jichuang Robot Technology Co., Ltd.

What are the key growth drivers?

-> Key growth drivers include increasing automation in industries, rising demand for humanoid robots, and advancements in power module technologies.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by China, Japan, and South Korea, while North America remains a dominant market.

What are the emerging trends?

-> Emerging trends include high-efficiency power modules, integration of AI for smart power management, and miniaturization of components.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...