RF Switches Market MARKET INSIGHTS

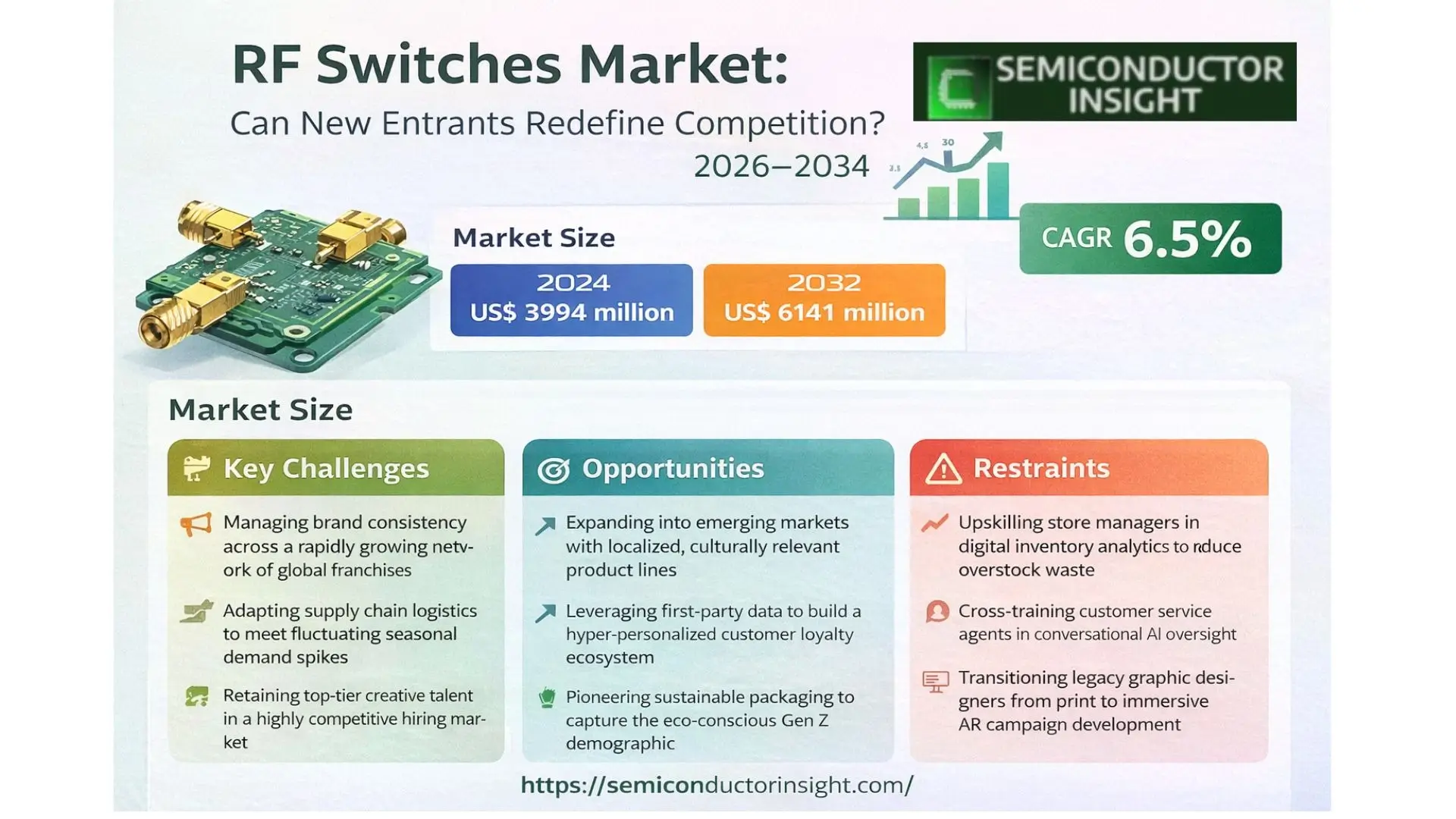

Global RF Switches Market was valued at 3994 million in 2024 and is projected to reach USD 6141 million by 2032, at a CAGR of 6.5% during the forecast period.

RF switches are fundamental electronic components used extensively in wireless systems for signal routing, primarily switching signals between antennas and transmit/receive chains. They are among the highest volume RF devices deployed today, with multiple units typically integrated into a single system block diagram. These devices are broadly categorized into electromechanical switches and solid-state switches. While traditional electromechanical switches have been largely superseded by solid-state alternatives, they are experiencing a resurgence in specific applications through Micro-Electromechanical Systems (MEMS) technology. Solid-state switches, which include PIN diodes and Field-Effect Transistors (FETs), are generally more reliable, offer faster switching times, and have a longer operational lifespan, though they can exhibit higher ON resistance and harmonic distortion compared to their mechanical counterparts.

The market’s growth is propelled by the relentless expansion of wireless communication infrastructure, including the ongoing global rollout of 5G networks, and rising demand in consumer electronics, aerospace, defense, and automotive applications. Advancements in semiconductor technologies, particularly Silicon-on-Insulator (SOI) and Silicon-on-Sapphire (SOS), are challenging established Gallium Arsenide (GaAs) solutions by offering improved performance and cost-effectiveness. The industry is relatively concentrated, with Skyworks leading as the dominant player, holding a 22% revenue share in 2024. Geographically, the Asia-Pacific region is the production powerhouse, accounting for over 62% of the global output value, driven by massive electronics manufacturing hubs.

RF Switches Market MARKET DYNAMICS

RF Switches Market MARKET DRIVERS

Proliferation of 5G Infrastructure Deployment to Accelerate Market Expansion

Global rollout of 5G networks represents a primary catalyst for RF switch demand, requiring advanced switching solutions to manage increased frequency bands and complex antenna systems. 5G infrastructure utilizes massive MIMO (Multiple Input Multiple Output) technology, which significantly increases the number of RF switches per base station. Current estimates indicate that 5G base stations require approximately 30-40% more RF switches compared to 4G installations. The transition to higher frequency millimeter-wave spectrum in 5G networks further drives the need for sophisticated switching solutions capable of handling faster data rates and improved signal integrity. With over 300 commercial 5G networks deployed worldwide and continued expansion anticipated, the demand for high-performance RF switches continues to grow substantially.

Expansion of Internet of Things and Connected Devices to Fuel Market Growth

The exponential growth of IoT applications across industrial, automotive, and consumer segments is creating sustained demand for RF switching components. Connected devices require efficient signal routing between multiple antennas and transceivers, driving the adoption of RF switches in smart home systems, industrial automation, and automotive connectivity modules. The automotive sector alone is projected to incorporate over 150 million 5G-connected vehicles by 2030, each requiring multiple RF switches for various communication systems. Additionally, industrial IoT applications are experiencing compound annual growth rates exceeding 15%, further accelerating the need for reliable RF switching solutions in harsh operating environments.

Advancements in Semiconductor Technologies to Enhance Market Penetration

Technological innovations in semiconductor manufacturing are enabling the development of more efficient and cost-effective RF switches. Silicon-on-insulator (SOI) and silicon-on-sapphire (SOS) technologies have achieved significant performance improvements, with current-generation SOI switches demonstrating insertion losses below 0.5 dB and isolation exceeding 30 dB across frequency bands up to 6 GHz. These advancements allow RF switch manufacturers to deliver products with improved power handling capabilities, typically reaching 30-35 dBm for SOI-based switches, while maintaining competitive pricing. The continuous refinement of MEMS switch technology has also addressed previous reliability concerns, with recent generations demonstrating operational lifetimes exceeding 10 billion cycles, making them suitable for demanding aerospace and defense applications.

Furthermore, the integration of RF switches with other components into front-end modules is creating additional market opportunities while reducing overall system footprint and cost.

RF Switches Market MARKET RESTRAINTS

Technical Limitations in High-Frequency Applications to Constrain Market Development

RF switches face significant technical challenges when operating at millimeter-wave frequencies required for advanced 5G and satellite communication applications. As frequencies increase beyond 24 GHz, conventional semiconductor-based switches experience performance degradation, with insertion losses typically increasing by 15-20% compared to sub-6 GHz operation. This performance limitation becomes particularly critical in phased array systems where consistent signal characteristics across multiple channels are essential. Additionally, power handling capabilities decrease at higher frequencies, with many commercial RF switches limited to approximately 25 dBm output power in millimeter-wave bands, restricting their use in high-power transmission systems.

Supply Chain Constraints and Material Shortages to Impede Market Growth

RF Switches Market faces ongoing challenges related to semiconductor material availability and manufacturing capacity constraints. Gallium arsenide (GaAs) substrates, essential for high-performance RF switches, have experienced supply disruptions with lead times extending from historical averages of 6-8 weeks to 12-16 weeks in recent periods. This shortage is particularly impactful for aerospace and defense applications where GaAs-based switches remain the preferred solution due to their superior high-frequency performance. Additionally, the specialized packaging requirements for RF switches, including advanced ceramic and laminate substrates, have faced manufacturing bottlenecks, with production capacity utilization rates exceeding 85% across major suppliers.

Cost Pressure from Consumer Electronics Market to Limit Profit Margins

Intense price competition in the consumer electronics sector creates significant margin pressure for RF switch manufacturers. Smartphone OEMs continuously demand cost reductions of 5-7% annually for RF components, forcing switch suppliers to optimize manufacturing processes and material costs aggressively. This pricing pressure is particularly challenging for newer technologies such as SOI and MEMS switches, which require substantial capital investment in fabrication facilities. The average selling price for RF switches in consumer applications has declined by approximately 40% over the past five years, while performance requirements have simultaneously increased, creating a challenging environment for maintaining profitability while investing in next-generation technologies.

RF Switches Market MARKET OPPORTUNITIES

Emerging Satellite Communication and Space Applications to Create New Market Segments

The rapidly expanding satellite communication market presents substantial growth opportunities for advanced RF switching solutions. Low Earth Orbit (LEO) satellite constellations require thousands of satellites, each incorporating multiple RF switches for signal routing and beamforming applications. Current projections indicate that over 15,000 new satellites will be launched by 2030, creating demand for radiation-hardened RF switches capable of operating in space environments. These applications require switches with exceptional reliability, typically specifying mean time between failures exceeding 1 million hours, and performance stability across extreme temperature ranges from -40°C to +125°C. The satellite communication segment is expected to grow at approximately 12% annually, providing a high-value market for specialized RF switch manufacturers.

Automotive Radar and Advanced Driver Assistance Systems to Drive Future Demand

The automotive industry’s transition toward autonomous driving systems is generating significant opportunities for RF switch applications. Modern vehicles incorporate multiple radar systems operating at 24 GHz, 77 GHz, and 79 GHz frequencies, each requiring sophisticated RF switching for beam steering and multi-mode operation. Advanced driver assistance systems typically utilize 5-8 radar sensors per vehicle, with high-end models incorporating up to 12 sensors. The automotive radar market is projected to grow at approximately 18% annually, driven by regulatory requirements and consumer demand for safety features. RF switches for automotive applications must meet stringent quality standards, including AEC-Q100 qualification, and demonstrate reliability across temperature ranges from -40°C to +105°C with operational lifetimes exceeding 15 years.

Integration of Artificial Intelligence in RF System Design to Enable Smart Switching Solutions

The incorporation of artificial intelligence and machine learning technologies into RF systems is creating opportunities for intelligent switching solutions. AI-enabled RF switches can dynamically optimize signal paths based on real-time environmental conditions, interference patterns, and performance requirements. These smart switching systems can improve overall network efficiency by 20-30% while reducing power consumption by adapting to changing operational conditions. The development of cognitive radio systems, which automatically select optimal frequency bands and transmission parameters, particularly benefits from advanced RF switching capabilities. The integration of monitoring and control functionalities directly into RF switches enables predictive maintenance and performance optimization, creating additional value propositions for system manufacturers.

RF Switches Market MARKET CHALLENGES

Technical Complexity in Multi-Throw Switch Design to Challenge Performance Requirements

Designing high-performance multi-throw RF switches presents significant technical challenges, particularly as port counts increase beyond SP4T configurations. Each additional throw port introduces parasitic capacitance and inductance that can degrade overall switch performance. In SP8T and higher configurations, maintaining consistent insertion loss across all ports typically requires trade-offs in isolation performance, with degradation of 3-5 dB observed compared to simpler SPST configurations. Additionally, the physical layout constraints become increasingly challenging at higher frequencies, where transmission line lengths must be carefully controlled to maintain phase coherence in phased array applications. These design complexities require advanced simulation tools and specialized engineering expertise, creating barriers to entry for new market participants.

Other Challenges

Thermal Management Constraints

High-power applications generate significant heat dissipation challenges for RF switches, particularly in base station and aerospace applications. Power handling capabilities are often limited by thermal considerations rather than fundamental semiconductor properties. Switch designs must incorporate effective heat spreading techniques and thermal interfaces to maintain junction temperatures within safe operating limits, typically below 150°C for most semiconductor technologies. The thermal resistance from junction to case for advanced RF switches typically ranges from 15-25°C/W, requiring careful system-level thermal design to ensure reliable operation under maximum power conditions.

Testing and Characterization Complexities

Comprehensive RF switch testing requires sophisticated measurement equipment and methodologies, particularly for multi-port devices operating at millimeter-wave frequencies. Automated test systems capable of characterizing 16+ port devices at frequencies up to 40 GHz represent capital investments exceeding D 1 million per system. Additionally, the time required for complete characterization of complex switches can exceed 4-6 hours per device, creating production throughput challenges. The need for temperature cycling tests across military temperature ranges (-55°C to +125°C) further extends validation timelines and increases testing costs, particularly for high-reliability applications.

RF SWITCHES MARKET TRENDS

Advancements in Semiconductor Technologies to Emerge as a Trend in the Market

The evolution of semiconductor technologies is fundamentally reshaping the RF switches landscape, with silicon-on-insulator (SOI) and silicon-on-sapphire (SOS) technologies increasingly challenging traditional gallium arsenide (GaAs) solutions. While GaAs has historically dominated due to its superior high-frequency performance, recent improvements in silicon-based processes have significantly narrowed the performance gap. These advancements have led to SOI/SOS switches achieving cutoff frequencies exceeding 100 GHz and handling power levels up to 40 W, making them highly competitive for numerous applications. Furthermore, the integration of these technologies with complementary metal-oxide-semiconductor (CMOS) processes enables higher levels of integration, reduced power consumption, and lower production costs. This technological shift is particularly evident in the cellular segment, where 5G infrastructure demands both high performance and cost efficiency, driving adoption of advanced silicon-based RF switches across base stations and mobile devices.

Other Trends

Proliferation of 5G and IoT Infrastructure

Global rollout of 5G networks and the exponential growth of Internet of Things (IoT) devices are creating unprecedented demand for RF switching solutions. 5G infrastructure requires sophisticated antenna systems with multiple input multiple output (MIMO) configurations, necessitating a substantial increase in the number of RF switches per base station. Similarly, IoT devices operating across various frequency bands require efficient signal routing capabilities to maintain connectivity while optimizing power consumption. The cellular application segment alone accounted for approximately 45% of the total RF Switches Market revenue in 2024, with this percentage expected to grow as 5G deployment accelerates globally. The wireless communications segment follows closely, driven by the need for advanced switching in Wi-Fi 6/6E and upcoming Wi-Fi 7 standards, which support broader channel bandwidths and more complex frequency band switching requirements.

Expansion in Aerospace, Defense, and Automotive Applications

While consumer and communications applications drive volume, specialized sectors are demonstrating significant growth potential. The aerospace and defense segment requires RF switches that can operate reliably in extreme environmental conditions while maintaining precise signal integrity. These applications often utilize electromechanical and MEMS switches despite their higher cost because of their superior power handling capabilities and lower harmonic distortion. The automotive sector is emerging as another growth area, with advanced driver assistance systems (ADAS), vehicle-to-everything (V2X) communication, and in-vehicle infotainment systems incorporating multiple RF switching components. The industrial and automotive segment is projected to achieve a compound annual growth rate of approximately 7.8% during the forecast period, outpacing the overall market average. This growth is fueled by increasing electronic content in modern vehicles and industrial automation systems that require robust RF signal management solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Strive to Strengthen their Product Portfolio to Sustain Competition

Global RF Switches Market exhibits a semi-consolidated competitive structure, characterized by the presence of several large, established semiconductor companies alongside specialized medium and smaller players. Skyworks Solutions, Inc. is the undisputed market leader, commanding a significant 22% revenue share in 2024. This dominance is primarily attributed to its extensive and technologically advanced product portfolio, which spans multiple switch types including GaAs, SOI, and PIN diode-based solutions, catering to the high-volume cellular and wireless communications segments. Their strong manufacturing footprint and deep relationships with global smartphone OEMs provide a considerable competitive moat.

Qorvo, Inc. and Broadcom Inc. (formerly Avago) are other major forces in the market, holding substantial market shares. The growth trajectory of these companies is heavily driven by their vertically integrated capabilities, allowing them to supply complete RF front-end modules that include switches, filters, and amplifiers. This system-level approach is increasingly critical for modern 5G devices, creating a high barrier to entry for smaller players. Furthermore, their significant and sustained investments in R&D, particularly in advancing SOI and GaAs on insulator technologies, ensure they remain at the forefront of performance and integration.

Additionally, these leading companies are aggressively pursuing growth through strategic geographical expansions, particularly strengthening their presence in the Asia-Pacific region, which accounts for over 62% of the global output value. New product launches focused on 5G infrastructure, automotive radar, and IoT applications are expected to be key growth drivers over the forecast period. For instance, the development of ultra-low-loss, high-linearity switches for massive MIMO systems represents a critical innovation area.

Meanwhile, companies like Infineon Technologies and NXP Semiconductors are strengthening their market positions through significant investments in R&D for automotive and industrial applications. Their strategy often involves leveraging expertise in other semiconductor domains to create optimized, application-specific switch solutions. Analog Devices, Inc. (which acquired Hittite Microwave) continues to be a key player in the high-performance aerospace and defense segment, competing through specialized, high-reliability product offerings. Strategic partnerships with defense contractors and industrial automation firms are crucial for their sustained growth in these niche but high-value markets.

List of Key RF Switches Companies Profiled

- Skyworks Solutions, Inc. (U.S.)

- Qorvo, Inc. (U.S.)

- Broadcom Inc. (U.S.)

- Infineon Technologies AG (Germany)

- NXP Semiconductors N.V. (Netherlands)

- Peregrine Semiconductor (now part of Murata Manufacturing Co., Ltd.) (U.S.)

- Analog Devices, Inc. (U.S.)

- Honeywell International Inc. (U.S.)

- NJR Corporation (Nippon Ceramic Co., Ltd.) (Japan)

- Maxim Integrated (now part of Analog Devices, Inc.) (U.S.)

- MACOM Technology Solutions Holdings, Inc. (U.S.)

- JFW Industries, Inc. (U.S.)

- Mini-Circuits (U.S.)

- Pasternack Enterprises, Inc. (U.S.)

Segment Analysis:

By Type

SOI & SOS Switches Segment Gains Prominence Due to Superior Performance and Cost-Effectiveness

The market is segmented based on type into:

- PIN Diodes

- GaAs

- SOI & SOS

- MEMS

By Application

Cellular Segment Commands Largest Share Owing to Proliferation of 5G and Mobile Devices

The market is segmented based on application into:

- Cellular

- Wireless Communications

- Aerospace & Defense

- Industrial & Automotive

- Consumer

- Others

By Technology

Solid-State Switches Dominate Market Share Driven by Reliability and Faster Switching Speeds

The market is segmented based on technology into:

- Electromechanical Switches

- Solid-State Switches

- Subtypes: PIN Diodes, FET-based

- MEMS Switches

By Frequency Range

DC to 8 GHz Segment Holds Significant Share Due to Broad Compatibility with Wireless Standards

The market is segmented based on frequency range into:

- DC to 8 GHz

- 8 GHz to 26 GHz

- Above 26 GHz

Regional Analysis: RF Switches Market

Asia-Pacific

The Asia-Pacific region dominates the global RF Switches Market, accounting for over 62% of the total output value. This leadership is driven by massive electronics manufacturing hubs in China, South Korea, and Taiwan, coupled with aggressive infrastructure rollouts for 5G and IoT across India, Japan, and Southeast Asia. The region benefits from a robust supply chain ecosystem, cost-competitive manufacturing, and strong government support for technological advancement. While GaAs and PIN diode-based switches remain prevalent due to their cost-effectiveness and maturity, there is a noticeable and accelerating shift toward advanced SOI/SOS and MEMS technologies, particularly in high-end smartphones and emerging automotive applications. The sheer volume of consumer electronics production and the ongoing expansion of wireless communication networks ensure that Asia-Pacific remains the epicenter of both RF switch consumption and innovation.

North America

North America is a critical market characterized by high-value, technologically advanced RF switch demand, primarily driven by the aerospace, defense, and premium wireless communication sectors. The presence of major industry leaders like Skyworks, Qorvo, and Broadcom Inc. fuels significant investment in R&D, particularly in cutting-edge SOI, SOS, and MEMS switch technologies for next-generation applications. Demand is heavily influenced by the need for ultra-reliable, high-frequency components for defense systems, satellite communications, and the ongoing upgrade cycle for 5G infrastructure. While the volume may be lower than Asia-Pacific, the region’s focus on performance, innovation, and securing supply chains for critical technologies ensures it remains a high-margin and strategically important market.

Europe

Europe’s RF Switches Market is defined by its strong automotive and industrial sectors, alongside stringent regulatory standards for performance and energy efficiency. The region’s push towards industrial automation (Industry 4.0) and the electrification of vehicles is creating sustained demand for robust and reliable RF switching solutions in applications like automotive radar, factory connectivity, and smart infrastructure. European manufacturers and consumers prioritize quality, longevity, and compliance with EU regulations, which drives adoption of advanced semiconductor technologies. While the market is mature and growth is steady, it is innovation-led, with a focus on integrating RF switches into complex systems for the automotive and industrial Internet of Things (IoT).

South America

The South American RF Switches Market is in a developing phase, with growth primarily tied to the gradual expansion of cellular networks and consumer electronics adoption in countries like Brazil and Argentina. The market is cost-sensitive, with demand concentrated on established GaAs and PIN diode technologies for consumer devices and basic communication infrastructure. Economic volatility and inconsistent investment in advanced technological infrastructure often delay the widespread adoption of newer switch technologies like SOI or MEMS. However, long-term potential exists as urbanization increases and mobile network operators continue to upgrade their systems to meet growing data consumption needs.

Middle East & Africa

This region represents an emerging opportunity for the RF Switches Market, with growth pockets centered around telecommunications infrastructure development in Gulf Cooperation Council (GCC) nations like Saudi Arabia and the UAE, as well as increasing mobile penetration in parts of Africa. Investment in smart city initiatives and limited 5G deployment is generating demand for communication-grade switches. However, the market’s progression is constrained by funding limitations for large-scale projects and a primary focus on cost-effective solutions, which slows the adoption of premium, advanced switching technologies. The market remains largely volume-driven for low-to-mid-tier applications.

Report Scope

This market research report provides a comprehensive analysis of the global RF Switches market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global RF Switches Market?

-> RF Switches Market was valued at 3994 million in 2024 and is projected to reach USD 6141 million by 2032, at a CAGR of 6.5% during the forecast period.

Which key companies operate in Global RF Switches Market?

-> Key players include Skyworks, Infineon Technologies, NXP Semiconductors, Qorvo, Broadcom (Avago), Analog Devices (Hittite), Honeywell, Peregrine Semiconductor, and MAXIM Integrated, among others.

What are the key growth drivers?

-> Key growth drivers include the proliferation of 5G infrastructure, increasing adoption of IoT devices, rising demand for smartphones, and advancements in wireless communication technologies.

Which region dominates the market?

-> Asia-Pacific is the dominant region, accounting for over 62% of the global output value, driven by strong manufacturing and consumer electronics demand in countries like China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include the adoption of MEMS technology, integration of SOI and SOS switches, development of higher frequency switches for 5G/6G applications, and increased focus on energy-efficient designs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...