Radiation tolerant SerDes chip for LEO satellite constellations Market Insights

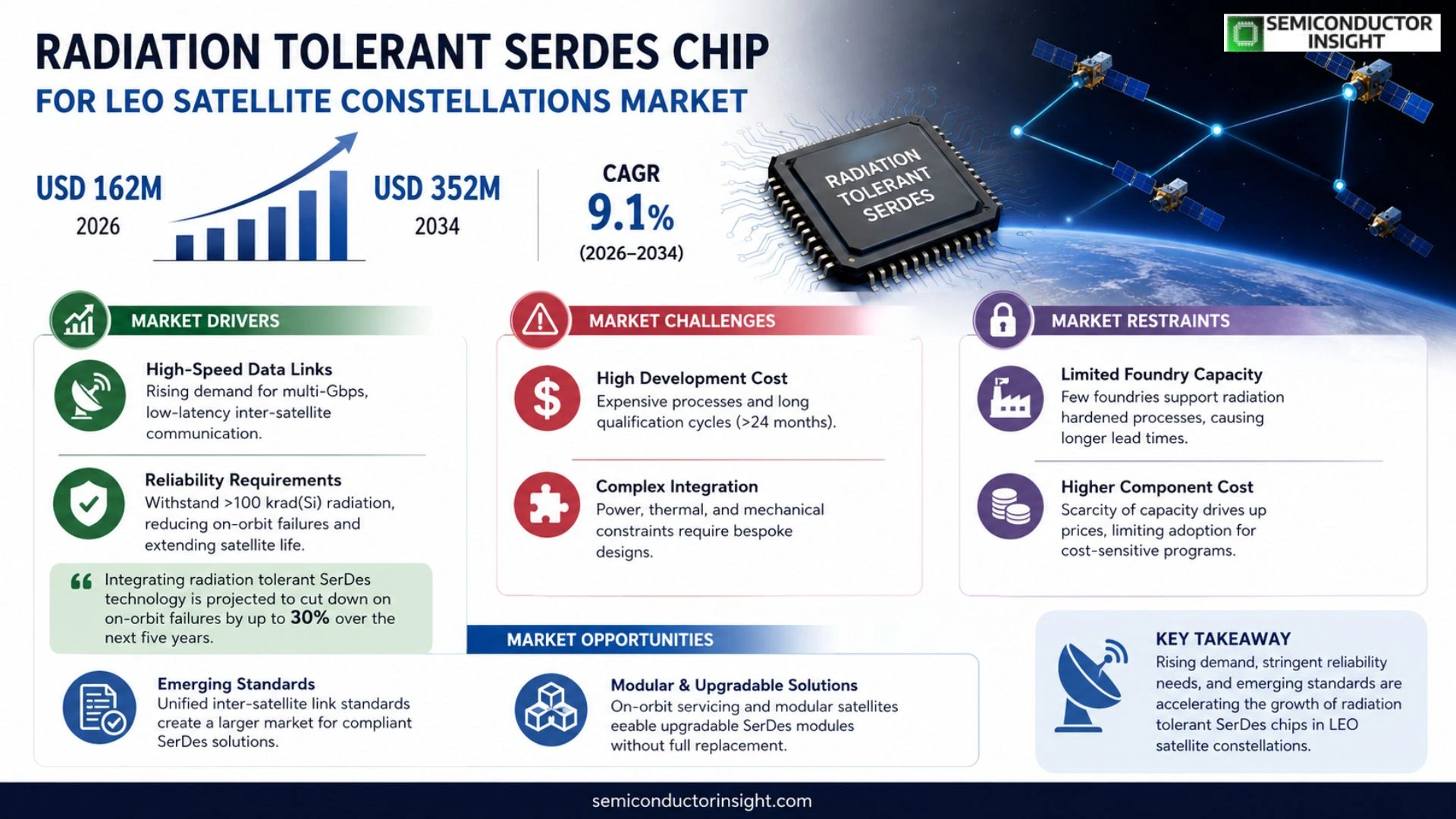

Global Radiation tolerant SerDes chip for LEO satellite constellations market size was valued at USD 152 million in 2025. The market is projected to grow from USD 162 million in 2026 to USD 352 million by 2034, exhibiting a CAGR of 9.1 % during the forecast period.

Radiation tolerant SerDes chips are high‑speed serializer/deserializer devices engineered to operate reliably in the harsh space radiation environment of low‑Earth‑orbit (LEO) constellations. They convert parallel data streams into serial formats and vice versa while incorporating design techniques such as silicon‑on‑insulator (SOI) processes and error‑correcting codes to mitigate single‑event upsets.

The market is experiencing rapid growth because the deployment of mega‑constellation projects,such as Starlink, OneWeb and Kuiper,has surged, driving demand for robust high‑bandwidth inter‑satellite links. Furthermore, increasing government investment in space infrastructure and advances in miniaturized payloads are accelerating adoption. Recent initiatives illustrate this trend; for example, Texas Instruments announced a new radiation‑hardened SerDes family in March 2024 targeting next‑generation LEO platforms. Analog Devices and Broadcom also continue expanding their space‑qualified portfolios, reinforcing competitive dynamics.

MARKET DRIVERS

Growing Demand for High‑Speed Data Links in LEO Constellations

The expansion of low‑earth‑orbit (LEO) satellite constellations is creating urgent need for high‑bandwidth, low‑latency inter‑satellite communication. Radiation tolerant SerDes chips enable reliable multi‑gigabit per second links while withstanding the harsh space environment, making them a cornerstone technology for next‑generation broadband services.

Stringent Reliability Requirements from Defense and Commercial Operators

Both defense agencies and commercial operators demand components that can survive cumulative radiation doses exceeding 100 krad(Si). The radiation hardened design of SerDes chips reduces single‑event upsets, thereby lowering maintenance costs and increasing satellite longevity.

➤ “Integrating radiation tolerant SerDes technology is projected to cut down on on‑orbit failures by up to 30 % over the next five years.”

These drivers collectively push manufacturers to invest in advanced process nodes and design verification, accelerating the overall market momentum for Radiation tolerant SerDes chip for LEO satellite constellations Market.

MARKET CHALLENGES

High Development Cost and Qualification Times

Designing radiation hardened SerDes chips involves expensive silicon‑on‑insulator (SOI) or silicon‑carbide processes, and qualification cycles can extend beyond 24 months. This financial burden limits participation to a handful of well‑funded vendors.

Other Challenges

Complex Integration with Existing Satellite Buses

The need to match power budgets, thermal constraints, and mechanical interfaces often requires bespoke redesigns, which can delay program schedules.

MARKET RESTRAINTS

Limited Foundry Capacity for Radiation Hardened Processes

Only a few semiconductor foundries currently offer the niche process steps needed for radiation tolerant SerDes production. Capacity constraints lead to longer lead times, which can restrain rapid deployment of new LEO constellations.

This scarcity also drives up component pricing, making cost‑sensitive customers reluctant to adopt the latest SerDes solutions without clear ROI evidence.

MARKET OPPORTUNITIES

Emerging Standards for Inter‑Satellite Links

Industry groups are defining unified protocols for inter‑satellite communication, which will standardize the electrical interface and create a larger addressable market for compliant SerDes chips. Early movers that align their designs with these standards can capture significant market share.

Additionally, the rise of on‑orbit servicing and modular satellite architectures opens avenues for upgradable SerDes modules, allowing operators to refresh data‑link capabilities without full satellite replacement.

Radiation tolerant SerSer chip for LEO satellite constellations Market Trends

Growing Demand from Mega‑Constellations

The deployment of large low‑Earth‑orbit (LEO) satellite constellations has accelerated the need for high‑speed, radiation‑tolerant SerDes chips. Operators such as Starlink, OneWeb and Kuiper require reliable inter‑satellite links that can sustain gigabit data rates while withstanding the intense radiation environment of LEO. This demand translates into a steady increase in orders for space‑qualified SerDes devices, prompting foundries to prioritize low‑power, high‑bandwidth architectures that meet stringent launch weight constraints. As payload miniaturization progresses, designers are integrating SerDes chips directly onto system‑on‑chip (SoC) platforms, further consolidating the market around a few specialized suppliers.

Other Trends

Advancements in Radiation‑Hardening Techniques

Recent silicon‑on‑insulator (SOI) processes and built‑in error‑correcting code (ECC) schemes have markedly improved single‑event upset (SEU) resilience. In March 2024, Texas Instruments released a new radiation‑hardened SerDes family that combines SOI with adaptive voltage scaling to reduce latch‑up probability. Analog Devices and Broadcom have followed suit, expanding their portfolios with devices that feature triple‑modular redundancy (TMR) at the circuit level. These technical enhancements enable higher data throughput without compromising reliability, supporting the next wave of high‑capacity LEO services such as broadband internet and Earth‑observation data relay.

Competitive Landscape and Supplier Expansion

Traditional aerospace vendors are increasingly joined by semiconductor giants that are establishing dedicated space‑qualified divisions. The competitive dynamics are shifting toward collaborations that blend advanced process technology with proven radiation‑hardening expertise. Government investment programs in Europe and Asia are also encouraging local manufacturers to certify their SerDes solutions for orbital use, diversifying the supply chain. This broader ecosystem reduces lead times for satellite manufacturers and fosters a more resilient market capable of absorbing rapid constellation growth.

COMPETITIVE LANDSCAPE

Key Industry Players

Radiation‑Tolerant SerDes Chips in LEO Satellite Constellations – Competitive Overview

The market is currently led by a small group of tier‑1 semiconductor firms that have invested heavily in radiation‑hardening processes and space‑qualified design libraries. Texas Instruments debuted a dedicated radiation‑hardened SerDes family in March 2024, targeting high‑throughput inter‑satellite links for mega‑constellation operators. Analog Devices leverages its extensive portfolio of mixed‑signal and RF components to offer integrated SerDes solutions that incorporate error‑correcting codes and silicon‑on‑insulator (SOI) substrates. Broadcom, building on its legacy of high‑speed networking chips, has extended its product line with space‑qualified variants that meet stringent single‑event upset (SEU) mitigation requirements. These leaders dominate revenue share because they can provide end‑to‑end system support, long‑term reliability guarantees, and extensive qualification documentation, which are essential for the high‑volume, cost‑sensitive LEO satellite market. Their scale also enables aggressive pricing that reinforces their market position while new entrants face substantial barriers in both technology development and qualification testing.

Beyond the dominant trio, a cadre of niche but strategically important players contributes depth to the ecosystem. Microchip Technology offers rad‑hard microcontrollers paired with SerDes interfaces that are attractive for small‑satellite payloads. Infineon Technologies supplies silicon‑on‑insulator based components with proven radiation tolerance for defense and space programs. STMicroelectronics and NXP Semiconductors provide mixed‑signal solutions that integrate SerDes functionality with power‑management and sensor interfaces, facilitating highly integrated satellite subsystems. ON Semiconductor (onsemi) and Rohm Semiconductor deliver specialty process options that address specific radiation dose rates. AMS and Teledyne e2v focus on precision analog front‑ends that complement high‑speed serial links. Mitsubishi Electric adds heritage in aerospace‑grade silicon, while Maxim Integrated (now part of Analog Devices) contributes low‑power SerDes blocks for ultra‑compact platforms. Collectively, these firms enhance competition by addressing specialized performance niches, regional procurement preferences, and supply‑chain diversification, thereby enriching the overall market resilience.

List of Key Radiation Tolerant SerDes Companies Profiled

- Texas Instruments

- Analog Devices

- Broadcom

- Microchip Technology

- Infineon Technologies

- STMicroelectronics

- NXP Semiconductors

- ON Semiconductor

- Rohm Semiconductor

- AMS

- Teledyne e2v

- Mitsubishi Electric

- Maxim Integrated

- Skyworks Solutions

- Qorvo

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

SOI‑based SerDes

|

| By Application |

|

Inter‑satellite links

|

| By End User |

|

Satellite operators

|

| By Architecture |

|

Integrated transceiver modules

|

| By Radiation‑Hardening Technique |

|

Error‑correcting code implementations

|

Regional Analysis: North America

Government programs focused on space exploration, national security, and commercial space development are providing substantial funding and fostering technological advancements in radiation-tolerant components. This support is instrumental in driving the adoption of advanced SerDes chips within LEO constellations.

Increased private sector investment in satellite constellations is directly correlated with the demand for robust and reliable components like radiation-tolerant SerDes chips. The growth of companies offering low-Earth orbit services is creating a significant market for these specialized technologies.

Ongoing research and development efforts are leading to more efficient and reliable radiation-tolerant SerDes chips. Innovations in chip design, packaging, and testing are crucial for meeting the stringent requirements of LEO satellite constellations.

North America boasts a well-established ecosystem of component suppliers, system integrators, and research institutions, which facilitates innovation and accelerates the adoption of radiation-tolerant SerDes chips within the LEO satellite market.

Europe

Europe is making significant strides in Radiation tolerant SerDes chip for LEO satellite constellations Market, driven by a growing emphasis on space-based communication and Earth observation. Several European nations have ambitious space programs and are investing in the development of advanced satellite technologies. While the private investment landscape is evolving, government support remains a key driver. The focus is on developing resilient and secure communication networks in space. Competition from established players and emerging startups is fostering innovation in this sector. Europe is strategically positioning itself to capitalize on the expanding LEO satellite market.

Asia-Pacific

Asia-Pacific represents a rapidly expanding market for radiation-tolerant SerDes chips for LEO satellite constellations. Driven by extensive government initiatives in countries like China and Japan, coupled with increasing commercial investment, the region is experiencing rapid growth in satellite deployments. The rise of indigenous satellite manufacturers and a growing demand for high-bandwidth communication are key factors. However, the market is also characterized by a diverse range of players and varying levels of technological sophistication. The Asia-Pacific region presents a significant opportunity for growth, but also requires navigating a complex regulatory and competitive environment.

South America

South America is an emerging market with growing potential for radiation-tolerant SerDes chips in LEO satellite constellations. Increased investments in satellite infrastructure for communication and remote sensing applications are driving demand. While the market is currently smaller compared to North America and Asia-Pacific, the region is expected to witness substantial growth in the coming years. Government initiatives to improve connectivity and leverage satellite technology for various sectors, including agriculture and disaster management, are contributing to this expansion. Overcoming infrastructure limitations and fostering a supportive regulatory environment will be crucial for realizing the full potential of the market.

Middle East & Africa

The Middle East & Africa region presents a nascent but promising market for radiation-tolerant SerDes chips supporting LEO satellite constellations. Growing investments in satellite communications for government, military, and commercial applications are fueling demand. The region’s strategic location and expanding connectivity needs are creating opportunities for satellite-based services. However, challenges such as limited infrastructure, regulatory complexities, and economic uncertainties may hinder rapid growth. Significant investments in infrastructure development and a more conducive regulatory framework are needed to fully unlock the potential of this market.

Report Scope

This market research report provides a comprehensive analysis of the Radiation tolerant SerDes chip for LEO satellite constellations Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Radiation tolerant SerDes chip for LEO satellite constellations Market?

-> Radiation tolerant SerDes chip for LEO satellite constellations market size is projected to grow from USD 162 million in 2026 to USD 352 million by 2034.

Which key companies operate in Radiation tolerant SerDes chip for LEO satellite constellations Market?

-> Key players include Axalta Coating Systems, AkzoNobel, BASF SE, PPG, Sherwin-Williams, and 3M, among others.

What are the key growth drivers?

-> Key growth drivers include railway infrastructure investments, urbanization, and demand for durable coatings.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include bio-based coatings, smart coatings, and sustainable rail solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...