MARKET INSIGHTS

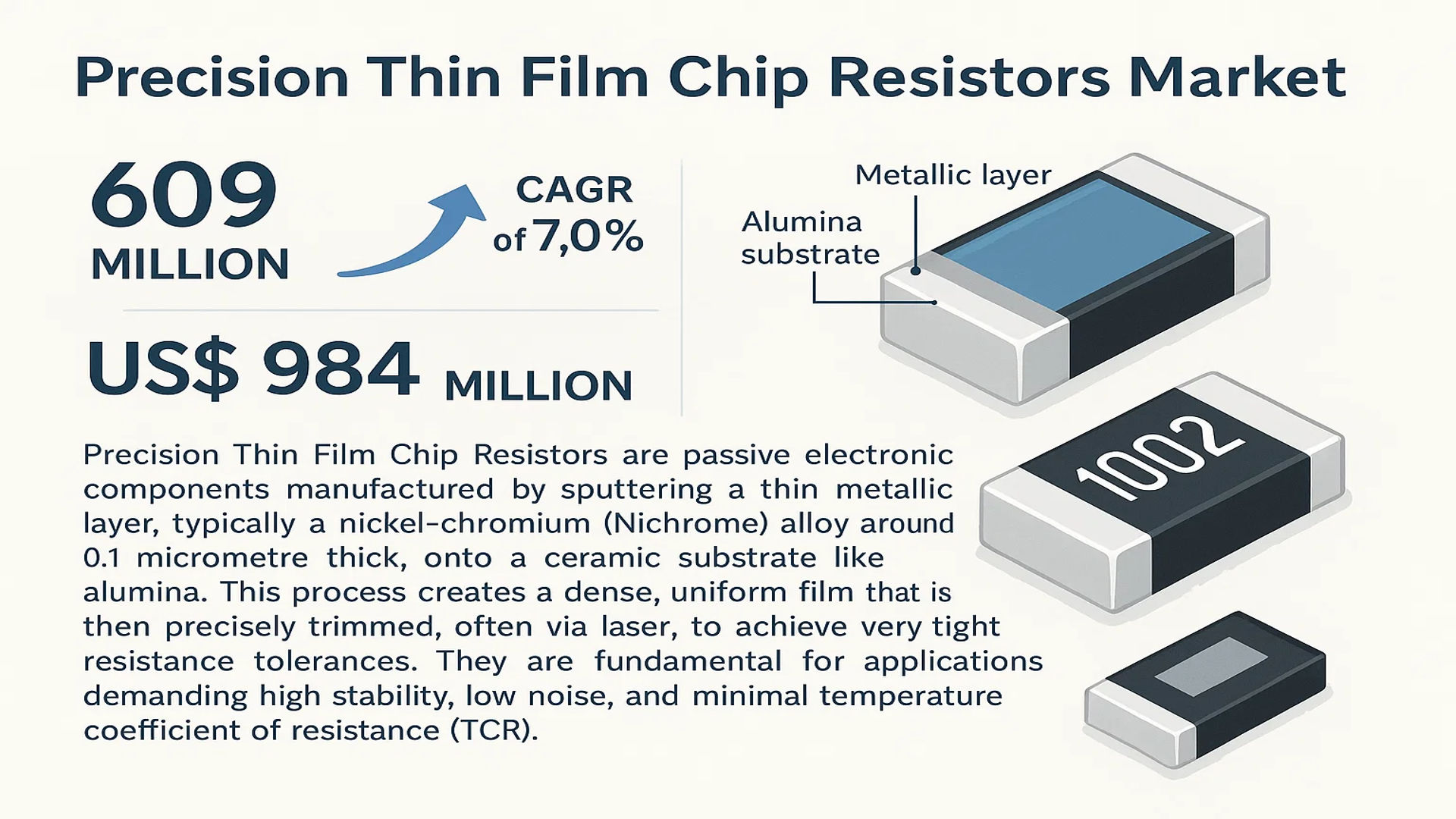

The global Precision Thin Film Chip Resistors Market was valued at 609 million in 2024 and is projected to reach US$ 984 million by 2032, at a CAGR of 7.0% during the forecast period.

Precision Thin Film Chip Resistors are passive electronic components manufactured by sputtering a thin metallic layer, typically a nickel-chromium (Nichrome) alloy around 0.1 micrometre thick, onto a ceramic substrate like alumina. This process creates a dense, uniform film that is then precisely trimmed, often via laser, to achieve very tight resistance tolerances. They are fundamental for applications demanding high stability, low noise, and minimal temperature coefficient of resistance (TCR).

The market’s robust growth is primarily driven by the escalating demand for high-precision electronics across various sectors. Key growth factors include the rapid expansion of industrial automation, advanced medical diagnostic equipment, and the increasing electronic content in automotive and communication devices. Asia Pacific is the dominant regional market, accounting for over 27% of global sales volume in 2024, with China being the largest single consumer. The market is also characterized by a high concentration of key players; for instance, Vishay Intertechnology, Inc. held a significant revenue share of 29.96% in 2024, underscoring the competitive landscape.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of High-Precision Electronics to Drive Market Growth

The global precision thin film chip resistors market is experiencing significant growth driven by the expanding demand for high-precision electronics across multiple industries. These components are essential in applications requiring exceptional accuracy, stability, and reliability, such as medical devices, industrial measurement equipment, and advanced communication systems. The market is projected to grow from 609 million USD in 2024 to 984 million USD by 2032, representing a compound annual growth rate of 7.0%. This growth is largely fueled by technological advancements in sectors like healthcare, where precision instruments increasingly rely on components with tolerances as low as 0.05% and temperature coefficients below 25 ppm/°C. The automotive electronics sector is also contributing substantially, with modern vehicles incorporating numerous precision resistors for safety systems, infotainment, and electric vehicle power management.

Rising Adoption of 5G and IoT Technologies to Boost Demand

The rapid deployment of 5G networks and Internet of Things (IoT) devices is creating substantial demand for precision thin film chip resistors. These components are critical for high-frequency applications where low parasitic inductance and capacitance are essential for maintaining signal integrity. The global 5G infrastructure market is expanding rapidly, requiring sophisticated communication devices that utilize precision resistors in RF circuits, base stations, and network equipment. Similarly, IoT devices increasingly incorporate precision components for accurate sensor readings and reliable data transmission. The manufacturing of these advanced electronic systems requires resistors that can maintain performance under varying environmental conditions, making thin film technology particularly valuable. This technological shift is driving innovation in resistor design and manufacturing processes, with leading companies developing new products specifically for these high-frequency applications.

Furthermore, the ongoing miniaturization of electronic devices continues to push the boundaries of component design. As devices become smaller and more powerful, the demand for precision thin film chip resistors with smaller form factors and higher performance characteristics increases significantly. This trend is particularly evident in portable medical devices, wearable technology, and compact communication equipment where space constraints are critical.

➤ For instance, leading manufacturers have introduced ultra-compact thin film chip resistors with dimensions as small as 0201 (0.6mm x 0.3mm) while maintaining tolerances of 0.1% and temperature coefficients of 5 ppm/°C, enabling next-generation electronic designs.

The combination of these technological advancements and growing end-market applications creates a robust foundation for continued market expansion throughout the forecast period.

MARKET CHALLENGES

High Manufacturing Costs and Complex Production Processes to Challenge Market Penetration

Despite strong market growth, precision thin film chip resistors face significant challenges related to manufacturing complexity and cost structures. The production process involves sophisticated vacuum deposition techniques, precise laser trimming, and stringent quality control measures that require substantial capital investment and specialized equipment. These factors contribute to manufacturing costs that are typically 3-5 times higher than those of thick film resistors, creating price sensitivity in cost-conscious market segments. The requirement for ultra-clean manufacturing environments and advanced metrology equipment further increases operational expenses, making it challenging for manufacturers to achieve economies of scale while maintaining the high quality standards demanded by precision applications.

Other Challenges

Supply Chain Vulnerabilities

The market faces ongoing challenges related to supply chain stability and material availability. Many precision thin film resistors require specialized materials including high-purity nickel-chromium alloys, premium ceramic substrates, and advanced packaging materials. Disruptions in the supply of these critical materials can significantly impact production schedules and product availability. Additionally, the specialized nature of manufacturing equipment creates dependency on a limited number of equipment suppliers, potentially leading to extended lead times for capacity expansion.

Technical Performance Limitations

While offering superior performance characteristics, thin film technology faces inherent limitations in power handling capabilities and maximum resistance values compared to alternative technologies. This restricts their application in certain high-power circuits where thick film or wirewound resistors might be preferred. The technology also faces challenges in achieving very high resistance values while maintaining stability and precision, creating design constraints for some specialized applications.

MARKET RESTRAINTS

Competition from Alternative Technologies to Limit Market Expansion

Precision thin film chip resistors face significant competition from alternative technologies that offer different performance trade-offs. Thick film resistors, while generally less precise, provide advantages in cost-effectiveness, higher power ratings, and broader resistance ranges. The development of advanced thick film technologies has narrowed the performance gap in some applications, particularly where ultra-high precision is not required. Additionally, metal foil resistors continue to compete in certain precision applications where stability and low noise are paramount. This competitive landscape creates pricing pressure and may limit market share growth for thin film technology in price-sensitive segments.

Furthermore, the emergence of integrated passive devices and system-in-package solutions presents a long-term challenge. As electronics manufacturers seek higher levels of integration, discrete components including resistors are increasingly being incorporated into multi-chip modules and integrated circuits. This trend toward integration could potentially reduce the demand for standalone precision resistors in some applications, particularly in consumer electronics and mass-market products where space optimization is critical.

The market also faces restraints from the lengthy qualification processes required in certain industries. Automotive, medical, and aerospace applications often require extensive testing and certification that can take 12-24 months, delaying product adoption and increasing development costs. These extended qualification cycles can slow market penetration and create barriers for new entrants seeking to establish presence in these high-reliability segments.

MARKET OPPORTUNITIES

Growth in Electric Vehicles and Renewable Energy Systems to Create New Opportunities

The rapid expansion of electric vehicle production and renewable energy systems presents significant growth opportunities for precision thin film chip resistors. Electric vehicles require numerous precision components for battery management systems, power conversion, and sensor interfaces where accuracy and reliability are critical for safety and performance. The global electric vehicle market is projected to maintain strong growth, with annual sales expected to exceed 30 million units by 2030, creating substantial demand for advanced electronic components. Similarly, solar inverters, wind turbine controls, and energy storage systems increasingly incorporate precision resistors for accurate measurement and control functions.

Additionally, the ongoing digital transformation across industrial sectors is driving demand for precision measurement and control systems. Industry 4.0 initiatives and smart manufacturing require sophisticated sensors and control systems that utilize precision resistors for accurate signal conditioning and data acquisition. This industrial modernization trend is creating new application areas in robotics, automated test equipment, and process control systems where measurement accuracy directly impacts operational efficiency and product quality.

The development of emerging technologies including artificial intelligence hardware, quantum computing systems, and advanced medical imaging equipment also creates new opportunities. These cutting-edge applications often require precision components with exceptional stability and minimal noise characteristics, positioning thin film technology as the preferred solution. Manufacturers that can develop products specifically optimized for these emerging applications are well-positioned to capture significant market share and drive future growth.

PRECISION THIN FILM CHIP RESISTORS MARKET TRENDS

Demand for High-Precision Electronics Driving Market Expansion

The global precision thin film chip resistors market is experiencing robust growth, primarily fueled by the escalating demand for high-precision electronic components across multiple industries. These resistors are critical in applications where accuracy, stability, and reliability are non-negotiable, such as in medical diagnostic equipment, aerospace avionics, and advanced automotive systems. The market’s valuation at 609 million USD in 2024 underscores its foundational role in modern electronics. This demand is further amplified by the global push towards miniaturization and enhanced performance in electronic devices. Manufacturers are increasingly adopting these components because they offer superior performance characteristics, including tolerances as low as 0.05% and extremely low temperature coefficients, often below 25 ppm/°C. The transition towards Industry 4.0 and smart manufacturing is also integrating more sophisticated measurement and control systems, which rely heavily on the precision that thin film technology provides. While the automotive sector’s electrification is a significant contributor, the medical field’s relentless innovation in imaging and monitoring devices represents a equally powerful, sustained driver for market expansion.

Other Trends

Technological Advancements in Manufacturing Processes

Continuous innovation in deposition and trimming technologies is a key trend shaping the competitive landscape of the thin film chip resistor market. The core process of sputtering a metallic alloy, such as Nichrome, onto a ceramic substrate has seen refinements that enhance film uniformity and density. Laser trimming, a critical calibration step, has evolved to achieve unprecedented precision, allowing for the creation of complex patterns that fine-tune resistance values with minimal introduced parasitic effects. These manufacturing advancements are directly responsible for the components’ excellent high-frequency performance, characterized by low inherent inductance and capacitance. This is particularly crucial for the next generation of communication devices, including 5G infrastructure and satellite systems, where signal integrity is paramount. Furthermore, research into novel substrate materials beyond traditional alumina ceramics promises to unlock new performance thresholds in thermal management and stability.

Asia-Pacific’s Dominance as a Manufacturing and Consumption Hub

The geographical concentration of the electronics manufacturing industry firmly establishes the Asia-Pacific region as the dominant force in the precision thin film chip resistors market. Accounting for over 27% of global sales volume, the region, led by China, Japan, and South Korea, is both a massive production base and a leading consumption center. This dominance is not merely a function of volume but also of technological capability, with numerous key players, including Susumu, KOA Speer Electronics, and Walsin Technology, headquartered and operating major production facilities within the region. The extensive local supply chains for consumer electronics, industrial equipment, and telecommunications hardware create a powerful, integrated ecosystem that fuels consistent demand. Furthermore, growing investments in automotive electronics production across Southeast Asia are positioning countries like Thailand and Vietnam as emerging, high-growth markets, ensuring the region’s leadership continues to strengthen through the forecast period.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Manufacturers Focus on Innovation and Geographic Expansion to Maintain Market Position

The global precision thin film chip resistors market exhibits a semi-consolidated structure, characterized by the presence of established multinational corporations, specialized mid-sized manufacturers, and niche regional players. Vishay Intertechnology, Inc. dominates the competitive landscape, holding a commanding 29.96% revenue share in 2024. This leadership position is largely attributable to its extensive, technologically advanced product portfolio, robust global distribution network, and significant investment in research and development, particularly in high-reliability applications for the automotive and industrial sectors.

Susumu Co., Ltd. and KOA Speer Electronics, Inc. also command significant market influence, holding approximately 12.26% and 9.48% revenue shares, respectively. The sustained growth of these companies is driven by their relentless focus on innovation, particularly in developing ultra-high precision resistors with tolerances as low as 0.05% and extremely low temperature coefficients. Their strong relationships with OEMs in the medical equipment and precision instrumentation markets provide a stable demand base.

Furthermore, strategic growth initiatives are a common theme across the industry. Companies are actively pursuing geographical expansions, especially into the high-growth Asia-Pacific region, which accounted for over 27% of global sales volume in 2024. New product launches targeting emerging applications in electric vehicles, 5G infrastructure, and renewable energy systems are also critical strategies for capturing additional market share over the forecast period.

Meanwhile, other key players such as Yageo Corporation and Panasonic Corporation are strengthening their market presence through strategic acquisitions and significant investments in automated manufacturing technologies. This enhances their production efficiency and capability to offer cost-competitive solutions without compromising on the high-performance standards required in precision applications, ensuring their continued relevance in an increasingly competitive market.

List of Key Precision Thin Film Chip Resistor Companies Profiled

- Vishay Intertechnology, Inc. (U.S.)

- Susumu Co., Ltd. (Japan)

- KOA Speer Electronics, Inc. (U.S.)

- Viking Tech Corporation (Taiwan)

- Yageo Corporation (Taiwan)

- Panasonic Corporation (Japan)

- Walsin Technology Corporation (Taiwan)

- Ta-I Technology Co., Ltd. (Taiwan)

- Bourns, Inc. (U.S.)

- UniOhm Co., Ltd. (China)

- TE Connectivity Ltd. (Switzerland)

- Samsung Electro-Mechanics (South Korea)

- Ralec Electronics Corp. (Taiwan)

- Ever Ohms Technology Co., Ltd. (Taiwan)

Segment Analysis:

By Type

0.1% Tolerance Segment Dominates the Market Due to Optimal Balance of Precision and Cost-Effectiveness

The market is segmented based on tolerance into:

- 0.05% Tolerance

- 0.1% Tolerance

- 1% Tolerance

- Others

By Application

Industrial and Measurement Equipment Segment Leads Due to Critical Need for High Accuracy and Stability

The market is segmented based on application into:

- Industrial and Measurement Equipment

- Medical Equipment

- Automotive Electronics

- Communication Device

- Others

By End-User Industry

Electronics Manufacturing Segment Holds Largest Share Driven by Proliferation of Smart Devices and IoT

The market is segmented based on end-user industry into:

- Electronics Manufacturing

- Healthcare and Medical Devices

- Automotive and Transportation

- Telecommunications

- Aerospace and Defense

By Packaging Technology

Surface Mount Device (SMD) Packaging Prevails Due to Compatibility with Automated Assembly Processes

The market is segmented based on packaging technology into:

- Surface Mount Device (SMD)

- Through-Hole Technology

- Chip Array Packages

- Custom Packaging Solutions

Regional Analysis: Precision Thin Film Chip Resistors Market

Asia-Pacific

The Asia-Pacific region is the dominant force in the global Precision Thin Film Chip Resistors market, accounting for over 27% of global sales volume. This leadership is driven by the massive electronics manufacturing ecosystems in China, Japan, and South Korea, which are major hubs for producing industrial and measurement equipment, communication devices, and automotive electronics. China alone holds a significant portion of the market share, fueled by its extensive domestic supply chain and government initiatives supporting high-tech manufacturing. While cost-competitive thick film resistors are widely used, the region is experiencing a pronounced shift toward high-precision thin film components. This transition is propelled by the increasing sophistication of end-products, stringent quality requirements from global customers, and the rapid expansion of the region’s automotive and medical device sectors. The presence of key manufacturers like Panasonic, Samsung Electro-Mechanics, and Yageo further solidifies the region’s production and innovation capabilities.

North America

North America represents the second-largest market, characterized by a strong demand for high-reliability and precision components. The region’s advanced industrial base, particularly in sectors like aerospace, defense, medical technology, and telecommunications, necessitates the use of high-performance thin film chip resistors with tight tolerances and low temperature coefficients. The market is driven by stringent performance standards and a focus on innovation, with major players like Vishay and TE Connectivity having a significant operational presence. Investments in next-generation technologies, including 5G infrastructure, electric vehicles, and advanced medical diagnostics, are key growth drivers. However, the market is also characterized by higher cost sensitivity for advanced components compared to Asia, leading to a careful balancing act between performance requirements and economic feasibility.

Europe

Europe’s market is shaped by its robust automotive industry, industrial automation sector, and a strong focus on research and development. German and French manufacturers, in particular, are major consumers of precision resistors for use in automotive electronics, measurement instrumentation, and industrial control systems. The region’s strict regulations regarding product quality, safety, and environmental compliance act as a significant driver for adopting high-performance components like thin film chips. European innovation often focuses on miniaturization and enhancing performance parameters to meet the demands of advanced applications. While the market is mature and stable, growth is sustained through continuous technological upgrades in end-user industries and the region’s commitment to high-value manufacturing.

South America

The South American market for Precision Thin Film Chip Resistors is emerging and relatively niche. Demand is primarily concentrated in countries with developing industrial and automotive sectors, such as Brazil and Argentina. The market growth is tempered by economic volatility, which impacts capital investment in high-tech manufacturing and limits the widespread adoption of premium-precision components. Most demand is met through imports, as local production capabilities for such advanced passive components are limited. However, the gradual modernization of industrial infrastructure and the growth of the telecommunications sector present long-term opportunities for market expansion, albeit from a small base.

Middle East & Africa

This region represents the smallest but growing segment of the global market. Demand is primarily driven by infrastructure development projects, particularly in the telecommunications and energy sectors in nations like Saudi Arabia, Israel, and the UAE. The market is largely import-dependent, with components being sourced for use in communication infrastructure, industrial equipment, and medical devices. The pace of adoption is slower compared to other regions, influenced by factors such as limited local manufacturing, a focus on cost-effective solutions, and a less mature high-tech industrial base. Nonetheless, ongoing economic diversification efforts and urban development projects are expected to foster gradual market growth in the long term.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Precision Thin Film Chip Resistors markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Precision Thin Film Chip Resistors Market?

-> Precision Thin Film Chip Resistors Market was valued at 609 million in 2024 and is projected to reach US$ 984 million by 2032, at a CAGR of 7.0% during the forecast period.

Which key companies operate in Global Precision Thin Film Chip Resistors Market?

-> Key players include Vishay, Susumu, KOA Speer Electronics, Viking Tech, Yageo, Panasonic, Walsin Technology, Ta-I Technology, Bourns, UniOhm, TE Connectivity, Samsung Electro-Mechanics, Ralec Electronics, and Ever Ohms, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for precision instruments, growth in medical equipment, automotive electronics, and communication devices, and advancements in semiconductor fabrication techniques.

Which region dominates the market?

-> Asia-Pacific is the largest consumption region, with China alone accounting for 27.09% of global sales volume, while North America holds over 28.71% of the market share.

What are the emerging trends?

-> Emerging trends include miniaturization of components, integration of AI/IoT in precision controls, development of ultra-low tolerance resistors, and increased adoption in high-frequency applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...