Power Semiconductor Switches for 3C Industry Market Insights

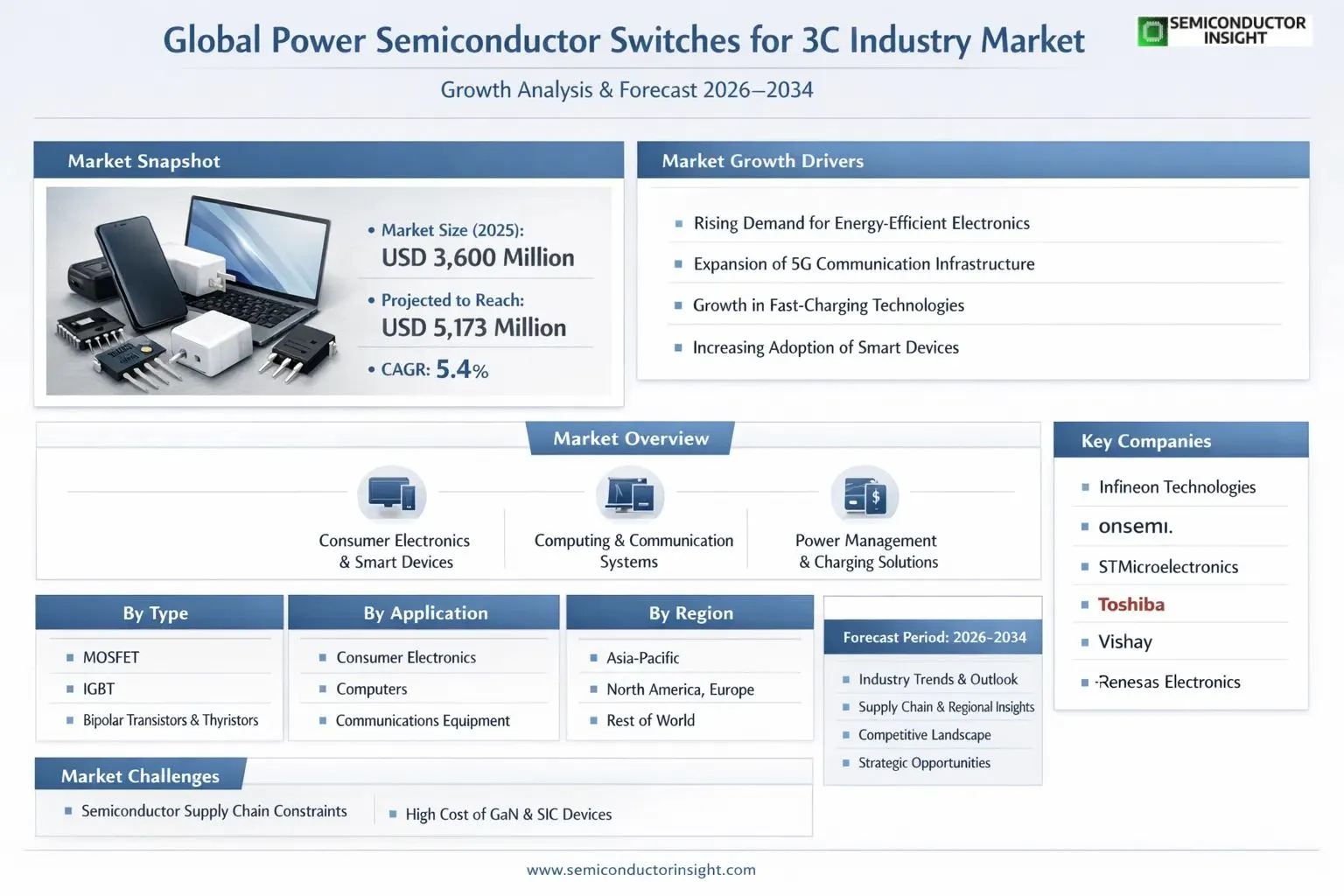

Global Power Semiconductor Switches for 3C Industry market size was valued at USD 3,600 million in 2025. The market is projected to grow from USD 3,794 million in 2026 to USD 5,173 million by 2034, exhibiting a CAGR of 5.4% during the forecast period.

Power Semiconductor Switches for the 3C Industry , encompassing computers, consumer electronics, and communications , are essential semiconductor devices that regulate and control electrical power flow within compact, high-performance electronic systems. These devices, which include MOSFETs, IGBTs, Bipolar Power Transistors, and Thyristors, are integral to efficient power management in smartphones, laptops, tablets, wireless communication equipment, and other consumer-grade electronics. Their ability to switch and convert electrical energy with minimal loss makes them indispensable in meeting the stringent power efficiency demands of modern 3C applications.

The market is witnessing sustained growth driven by the accelerating proliferation of smart devices, rapid advancements in 5G communications infrastructure, and rising consumer demand for energy-efficient electronics. The increasing adoption of wide-bandgap semiconductor materials such as Silicon Carbide (SiC) and Gallium Nitride (GaN) is further elevating device performance in high-frequency, high-efficiency 3C applications. Leading global manufacturers shaping this market include Infineon, onsemi, STMicroelectronics, Toshiba, Vishay, Fuji Electric, Renesas Electronics, Rohm, Nexperia, and Mitsubishi Electric, whose continuous product innovation and strategic collaborations are reinforcing the competitive landscape across key regions.

MARKET DRIVERS

Rising Demand for Energy-Efficient Consumer Electronics Fueling Adoption of Power Semiconductor Switches

Global 3C industry , encompassing computers, communications, and consumer electronics , has emerged as one of the most significant end-use sectors driving demand for advanced power management components. Within this landscape, the market for Power Semiconductor Switches for the 3C Industry is experiencing robust growth, underpinned by the accelerating proliferation of smartphones, laptops, tablets, wearables, and smart home devices. As consumer electronics manufacturers face increasing regulatory and competitive pressure to improve energy efficiency, the integration of high-performance power semiconductor switches such as MOSFETs, IGBTs, and GaN-based transistors has become a critical design priority. These components enable precise control of power flow, reduce switching losses, and support compact form factors essential to modern 3C product architectures.

Rapid Electrification and Fast-Charging Technology Driving Semiconductor Switch Integration

The widespread adoption of fast-charging standards across the 3C industry has been a transformative driver for Power Semiconductor Switches for 3C Industry Market. Protocols such as USB Power Delivery (USB-PD), Qualcomm Quick Charge, and proprietary fast-charging ecosystems deployed by major OEMs require switching components capable of operating at high frequencies with minimal thermal dissipation. Gallium Nitride (GaN) and Silicon Carbide (SiC) power switches have gained particular traction in this segment due to their superior switching speeds and lower on-resistance compared to traditional silicon-based alternatives. The continued rollout of 65W, 100W, and even 240W charger solutions for consumer devices has directly expanded the addressable market for advanced power semiconductor switches within the 3C value chain.

➤ The convergence of 5G connectivity, AIoT integration, and next-generation portable computing platforms is reshaping power architecture requirements across 3C product categories, creating sustained demand for high-frequency, low-loss power semiconductor switching solutions.

Beyond charging infrastructure, the expanding ecosystem of AI-enabled edge devices, foldable smartphones, AR/VR headsets, and ultra-thin notebooks within the 3C segment is placing new demands on power delivery networks. These applications require power semiconductor switches that combine high efficiency with extremely compact packaging, pushing innovation in chip-scale and flip-chip mounting technologies. The growing emphasis on battery life optimization and thermal management in premium 3C products continues to position power semiconductor switches as indispensable components, reinforcing long-term market expansion.

MARKET CHALLENGES

Supply Chain Vulnerabilities and Semiconductor Shortage Impact on 3C Power Switch Availability

Despite strong demand fundamentals, Power Semiconductor Switches for 3C Industry Market faces considerable challenges related to supply chain resilience and production capacity constraints. Global semiconductor shortage that emerged in the early 2020s exposed significant vulnerabilities in the sourcing of specialty power components, with lead times for key power switch families extending substantially. Foundry capacity limitations, particularly for mature process nodes commonly used in power semiconductor fabrication, continue to create supply-demand imbalances that affect 3C manufacturers’ ability to maintain consistent production schedules. These disruptions have prompted many OEMs to pursue dual-sourcing strategies and build strategic component inventories, adding complexity to procurement operations.

Other Challenges

Technological Complexity and Design Integration Barriers

The transition from conventional silicon MOSFETs to wide-bandgap semiconductors such as GaN and SiC introduces considerable design complexity for 3C product engineers. GaN-based power switches, while offering superior performance, require careful gate driver design, PCB layout optimization, and thermal management strategies that differ significantly from established silicon-based design methodologies. The learning curve associated with adopting these next-generation power semiconductor switches presents a real barrier, particularly for smaller 3C manufacturers with limited R&D resources. Ensuring electromagnetic compatibility (EMC) compliance while leveraging high-frequency switching capabilities adds further technical burden to product development cycles.

Pricing Pressure and Margin Compression in Consumer Electronics Segment

The intensely competitive nature of the 3C industry subjects component suppliers to persistent pricing pressure, which directly impacts the commercial viability of premium power semiconductor switch solutions. Consumer electronics OEMs operating on thin margins consistently demand cost reductions from their supply chains, creating tension between the higher bill-of-materials (BOM) cost of advanced GaN or SiC switches and the cost-sensitivity of mass-market 3C products. This dynamic can slow the pace of technology adoption and incentivize continued reliance on lower-cost silicon alternatives even where performance improvements would be achievable with wide-bandgap solutions.

MARKET RESTRAINTS

High Initial Cost of Wide-Bandgap Power Semiconductor Switches Limiting Mass-Market Penetration

One of the most significant restraints affecting Power Semiconductor Switches for 3C Industry Market is the relatively elevated cost of wide-bandgap semiconductor solutions compared to incumbent silicon-based power switches. While GaN and SiC devices offer measurable performance advantages in switching efficiency, thermal handling, and power density, their higher per-unit cost creates adoption barriers, especially in high-volume, cost-sensitive consumer electronics applications. Many mid-range and entry-level 3C products continue to be designed around silicon MOSFETs and bipolar transistors where the cost-performance trade-off favors established technology. Until wafer costs and manufacturing yields for GaN and SiC power switches reach greater parity with silicon, price sensitivity within the broader 3C market is likely to moderate the pace of advanced switch adoption.

Stringent Regulatory Compliance and Certification Requirements Adding Development Overhead

Regulatory frameworks governing electromagnetic emissions, energy efficiency ratings, and product safety certifications impose meaningful constraints on the deployment of power semiconductor switches in 3C applications. Standards such as IEC 62368-1, ENERGY STAR, and regional EMC directives require rigorous testing and validation of power management subsystems, adding time and cost to product development timelines. For manufacturers seeking to incorporate newer power semiconductor switch technologies that operate at higher switching frequencies, achieving compliance with conducted and radiated emissions limits can require significant redesign efforts. These regulatory burdens disproportionately affect smaller 3C manufacturers and component suppliers, potentially slowing the market-wide adoption of next-generation power switching solutions.

MARKET OPPORTUNITIES

Expansion of GaN Based Power Switches Across 3C Fast-Charging and Power Adapter Applications

The accelerating commercialization of GaN power semiconductor technology represents one of the most compelling near-term opportunities within Power Semiconductor Switches for 3C Industry Market. As GaN wafer production scales and manufacturing processes mature, the cost differential relative to silicon is progressively narrowing, improving the business case for adoption across a broader range of 3C product categories. Fast chargers, multi-port desktop charging stations, laptop power adapters, and USB-C power delivery solutions are among the highest-growth application segments where GaN switches are gaining design wins. Leading 3C brands have begun publicly committing to GaN-based charger ecosystems, creating pull-through demand that is expected to sustain strong volume growth for GaN power semiconductor switch suppliers throughout the forecast period.

Growth of Smart Home, Wearable Technology, and AIoT Devices Creating New Design Opportunities

The rapid proliferation of smart home ecosystems, connected wearables, and AIoT-enabled 3C devices is creating a new and diverse addressable market for compact, highly efficient power semiconductor switches. These applications demand switching components capable of operating across wide voltage ranges, maintaining high efficiency at light loads, and conforming to increasingly miniaturized packaging formats. Power semiconductor switches optimized for 3C Industry applications , including ultra-low quiescent current MOSFETs and integrated power switch modules , are well-positioned to capture design wins as the installed base of connected consumer devices expands globally. Semiconductor suppliers that invest in application-specific power switch solutions tailored to the operational requirements of wearables, smart speakers, and home automation platforms stand to benefit from sustained volume growth across the 3C segment.

Localization Initiatives and Regional Supply Chain Development Opening New Market Avenues

Geopolitical dynamics and supply chain diversification strategies pursued by major 3C manufacturing economies are creating meaningful opportunities for regional power semiconductor switch suppliers. Government-backed semiconductor self-sufficiency programs in Asia, North America, and Europe are catalyzing investment in domestic power semiconductor fabrication capacity, with direct implications for the supply landscape serving 3C industry customers. Emerging domestic suppliers in markets such as China, South Korea, and Taiwan are scaling production of power semiconductor switches specifically optimized for consumer electronics applications, intensifying competition while simultaneously expanding total market capacity. For established international players, partnerships with regional foundries and expanded local application support capabilities present strategic pathways to strengthen market positioning within the evolving Power Semiconductor Switches for 3C Industry Market.

Trends

Rising Demand Across Computers, Consumer Electronics, and Communications Driving Power Semiconductor Switches for 3C Industry Market

Power Semiconductor Switches for 3C Industry Market is experiencing sustained momentum driven by accelerating digitalization across the computers, consumer electronics, and communications sectors. As end-use industries push toward greater energy efficiency and miniaturization, demand for advanced switching devices such as MOSFETs, IGBTs, bipolar power transistors, and thyristors continues to rise. These components play a critical role in managing power conversion and distribution within compact, high-performance electronic systems,making them indispensable to modern 3C product design and manufacturing.

Other Trends

MOSFET Technology Gaining Prominence in Consumer Electronics

Among the key product segments in Power Semiconductor Switches for 3C Industry Market, MOSFETs are witnessing strong adoption due to their superior switching speed, low on-resistance, and compatibility with high-frequency circuit designs. Consumer electronics manufacturers are increasingly integrating MOSFET-based power stages to optimize battery performance and thermal management in smartphones, laptops, and wearables. This trend reflects the broader industry shift toward low-power, high-efficiency semiconductor architectures that align with global energy conservation standards.

Asia-Pacific Consolidating Its Leadership Position

The Asia-Pacific region, led by China, Japan, South Korea, and Southeast Asia, continues to dominate Power Semiconductor Switches for 3C Industry Market in terms of both production capacity and consumption volume. China’s robust electronics manufacturing ecosystem and government-backed semiconductor initiatives have reinforced regional supply chains. Meanwhile, South Korea and Japan remain critical hubs for advanced semiconductor fabrication, supporting a steady pipeline of next-generation switching devices tailored to the 3C segment.

Competitive Landscape and Strategic Developments Among Key Manufacturers

Leading players in Power Semiconductor Switches for 3C Industry Market,including Infineon, onsemi, STMicroelectronics, Toshiba, Vishay, Fuji Electric, Renesas Electronics, Rohm, Nexperia, and Mitsubishi Electric,are actively investing in product innovation, capacity expansion, and strategic partnerships to strengthen their market positioning. These manufacturers are focusing on developing switching devices that meet the increasingly stringent power density and thermal performance requirements of next-generation 3C applications. Competitive differentiation is being driven by advances in wide-bandgap materials, packaging technologies, and application-specific design capabilities, as companies work to address evolving requirements across communications infrastructure, computing platforms, and consumer electronics end markets.

COMPETITIVE LANDSCAPE

Key Industry Players

Power Semiconductor Switches for 3C Industry Market , Competitive Dynamics and Strategic Positioning of Leading Global Manufacturers

Global Power Semiconductor Switches for 3C Industry market is characterized by the strong dominance of a few well-established multinational semiconductor corporations. Infineon Technologies leads the competitive field, leveraging its extensive MOSFET and IGBT portfolio tailored for computers, consumer electronics, and communications applications , the three core verticals of the 3C sector. The company’s scale, R&D investment, and broad manufacturing capacity have enabled it to capture a significant share of the market, which was valued at USD 3,600 million in 2025 and is projected to reach USD 5,173 million by 2034 at a CAGR of 5.4%. onsemi and STMicroelectronics closely follow, both offering competitive product lines spanning MOSFETs, IGBTs, and Bipolar Power Transistors that address the efficiency and miniaturization demands of 3C end-use applications. These leading players collectively accounted for a substantial portion of Global revenue share in 2025, reinforcing a moderately consolidated market structure where technology leadership, product reliability, and supply chain integration are key differentiators.

Beyond the top-tier players, the competitive landscape includes several strategically significant contributors. Toshiba and Mitsubishi Electric bring deep heritage in power device engineering, particularly in thyristors and IGBT modules suited for high-performance consumer and computing platforms. Vishay Intertechnology is recognized for its broad discrete semiconductor offerings, while Fuji Electric maintains a strong presence in power module solutions. Renesas Electronics, Rohm Semiconductor, and Nexperia continue to expand their 3C-focused power switch portfolios through targeted product development and regional partnerships. Companies such as Texas Instruments, Microchip Technology, and Alpha and Omega Semiconductor also compete actively in the MOSFET segment, which is expected to register robust growth through 2034. The increasing adoption of energy-efficient power management solutions across smartphones, laptops, and networking equipment is intensifying competition, encouraging continuous innovation in device packaging, switching speed, and thermal performance across all major market participants.

List of Key Power Semiconductor Switches for 3C Industry Companies Profiled

- Infineon Technologies

- onsemi

- STMicroelectronics

- Toshiba

- Vishay Intertechnology

- Fuji Electric

- Renesas Electronics

- Rohm Semiconductor

- Nexperia

- Mitsubishi Electric

- Texas Instruments

- Microchip Technology

- Alpha and Omega Semiconductor

- Diodes Incorporated

- IXYS Corporation (a Littelfuse Company)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

MOSFET holds the leading position in Power Semiconductor Switches for 3C Industry Market, driven by its superior characteristics tailored for compact, high-frequency consumer and computing applications.

|

| By Application |

|

Consumer Electronics stands out as the dominant application segment for Power Semiconductor Switches in the 3C Industry, propelled by surging global demand for smart devices, wearables, and home automation products.

|

| By End User |

|

Original Equipment Manufacturers (OEMs) constitute the most significant end-user category, as they represent the primary point of integration for power semiconductor switches into finished 3C products.

|

| By Technology Node |

|

Silicon (Si)-Based technology remains the dominant foundation for power semiconductor switches deployed across the 3C industry, owing to its mature manufacturing ecosystem, cost competitiveness, and broad compatibility with existing device architectures.

|

| By Sales Channel |

|

Direct Sales channels represent the most strategically significant route to market for power semiconductor switches in the 3C industry, particularly for large-volume transactions between tier-one manufacturers and major OEM customers.

|

Regional Analysis: Power Semiconductor Switches for 3C Industry Market

Asia-Pacific

China dominates the Asia-Pacific landscape for power semiconductor switches used in 3C industry applications. The country’s massive electronics manufacturing base, supported by strong policy incentives and state-led semiconductor development programs, creates consistent demand. Domestic brands competing on innovation and cost-efficiency are driving the need for advanced power management solutions, further solidifying China’s central role in regional market expansion.

Japan and South Korea contribute significantly to the Asia-Pacific power semiconductor switches ecosystem through cutting-edge semiconductor design and precision manufacturing. Leading conglomerates in both nations are investing heavily in wide-bandgap materials and advanced switching topologies suited for high-performance 3C devices. Their emphasis on quality, miniaturization, and energy efficiency continues to set benchmarks for global competitors in the market.

India and Southeast Asian nations are rapidly emerging as significant consumption hubs for power semiconductor switches within the 3C industry market. Expanding middle-class populations, growing smartphone penetration, and government-driven electronics manufacturing incentives are creating fertile ground. These markets are transitioning from pure assembly roles toward value-added manufacturing, opening new opportunities for suppliers of advanced power switching components targeting consumer and communication segments.

The accelerating rollout of 5G infrastructure and the proliferation of smart connected devices across Asia-Pacific is a primary catalyst for demand in Power Semiconductor Switches for 3C Industry Market. Devices requiring faster switching speeds, lower conduction losses, and enhanced thermal performance are driving manufacturers to adopt next-generation semiconductor switch technologies, reinforcing Asia-Pacific’s dominance as both producer and consumer in this evolving landscape.

North America

North America represents a strategically important region in Power Semiconductor Switches for 3C Industry Market, characterized by strong innovation ecosystems, prominent semiconductor design houses, and advanced research institutions. The United States, in particular, plays a central role in defining technology roadmaps for power management solutions integrated into high-performance computing devices, premium consumer electronics, and next-generation communication hardware. The region’s emphasis on energy efficiency regulations and sustainability standards is encouraging the adoption of advanced power semiconductor switches that minimize power dissipation across 3C applications. Significant investments in domestic semiconductor manufacturing capacity, backed by federal policy initiatives, are reshaping supply chain dynamics and reinforcing North America’s strategic importance. Canada contributes through specialized research capabilities and a growing ecosystem of fabless semiconductor companies focused on power electronics innovation. The region’s mature consumer base and early adoption of premium technology products ensure sustained demand for sophisticated power switching solutions throughout the forecast period extending to 2034.

Europe

Europe occupies a distinctive position in Power Semiconductor Switches for 3C Industry Market, driven by stringent energy efficiency mandates, a strong culture of technological innovation, and the presence of globally recognized semiconductor companies specializing in power management solutions. Germany, the Netherlands, Sweden, and France anchor the regional market, hosting both established manufacturers and an active start-up ecosystem focused on wide-bandgap semiconductor technologies. European regulatory frameworks promoting low-power electronics design are compelling 3C device manufacturers operating in the region to prioritize advanced power semiconductor switches that comply with evolving efficiency standards. The region’s sophisticated industrial base, combined with collaborative research programs between academia and industry, accelerates the commercialization of next-generation switching devices. While Europe’s consumer electronics manufacturing scale is comparatively smaller than Asia-Pacific, its role as a technology innovator and premium market consumer ensures continued relevance in shaping global power semiconductor switch development trajectories for the 3C industry through 2034.

South America

South America presents a developing yet increasingly relevant market landscape for Power Semiconductor Switches for 3C Industry applications. Brazil serves as the regional anchor, supported by a growing consumer electronics sector and expanding telecommunications infrastructure investment, both of which generate demand for reliable power switching components. Rising smartphone adoption rates, government-supported digital inclusion programs, and the gradual modernization of computing infrastructure across urban centers are creating incremental demand signals. However, the region faces structural challenges including economic volatility, fragmented supply chains, and dependency on imported semiconductor components that can constrain market acceleration. Despite these headwinds, South America’s young and digitally engaged population represents a long-term growth opportunity for power semiconductor switch suppliers serving the 3C industry market. Strategic partnerships between global semiconductor suppliers and regional electronics assemblers are expected to gradually strengthen the local value chain through the forecast horizon extending to 2034.

Middle East & Africa

The Middle East and Africa region represents a nascent but progressively evolving frontier for Power Semiconductor Switches for 3C Industry Market. Gulf Cooperation Council nations, particularly the United Arab Emirates and Saudi Arabia, are investing substantially in digital infrastructure, smart city initiatives, and technology adoption, generating upstream demand for advanced power management components used in communication and computing hardware. Africa’s expanding mobile-first consumer base, driven by rapid smartphone penetration and improving network coverage, is creating steady demand at the entry-level and mid-range segments of the 3C market. While local semiconductor manufacturing capabilities remain limited, the region’s growing role as an end-market consumer is attracting the attention of global power semiconductor switch suppliers seeking geographic diversification. Long-term structural improvements in technology infrastructure, combined with rising disposable incomes in key urban centers, are expected to position the Middle East and Africa as a gradually expanding contributor to global market dynamics for power semiconductor switches serving 3C industry applications through 2034.

Report Scope

This market research report provides a comprehensive analysis of Power Semiconductor Switches for 3C Industry Market, covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Power Semiconductor Switches for 3C Industry Market?

-> Global Power Semiconductor Switches for 3C Industry Market was valued at USD 3,600 million in 2025 and is expected to reach USD 5,173 million by 2034, growing at a CAGR of 5.4% during the forecast period.

Which key companies operate in Power Semiconductor Switches for 3C Industry Market?

-> Key players include Infineon, onsemi, STMicroelectronics, Toshiba, Vishay, Fuji Electric, Renesas Electronics, Rohm, Nexperia, and Mitsubishi Electric, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for energy-efficient power management solutions, rapid growth in consumer electronics and computing devices, expanding communications infrastructure, and increasing adoption of power semiconductor switches across computers, consumer electronics, and communications applications.

Which region dominates the market?

-> Asia is a dominant and fastest-growing region in Power Semiconductor Switches for 3C Industry Market, driven by strong manufacturing bases in China, Japan, South Korea, and Southeast Asia, while North America and Europe also hold significant market shares.

What are the emerging trends?

-> Emerging trends include increasing adoption of MOSFET and IGBT technologies, growing integration of power semiconductors in next-generation computing and communications equipment, advancements in wide-bandgap semiconductor materials, and rising focus on energy efficiency and miniaturization across 3C industry applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...