Polyimide Electrostatic Chuck Market Insights

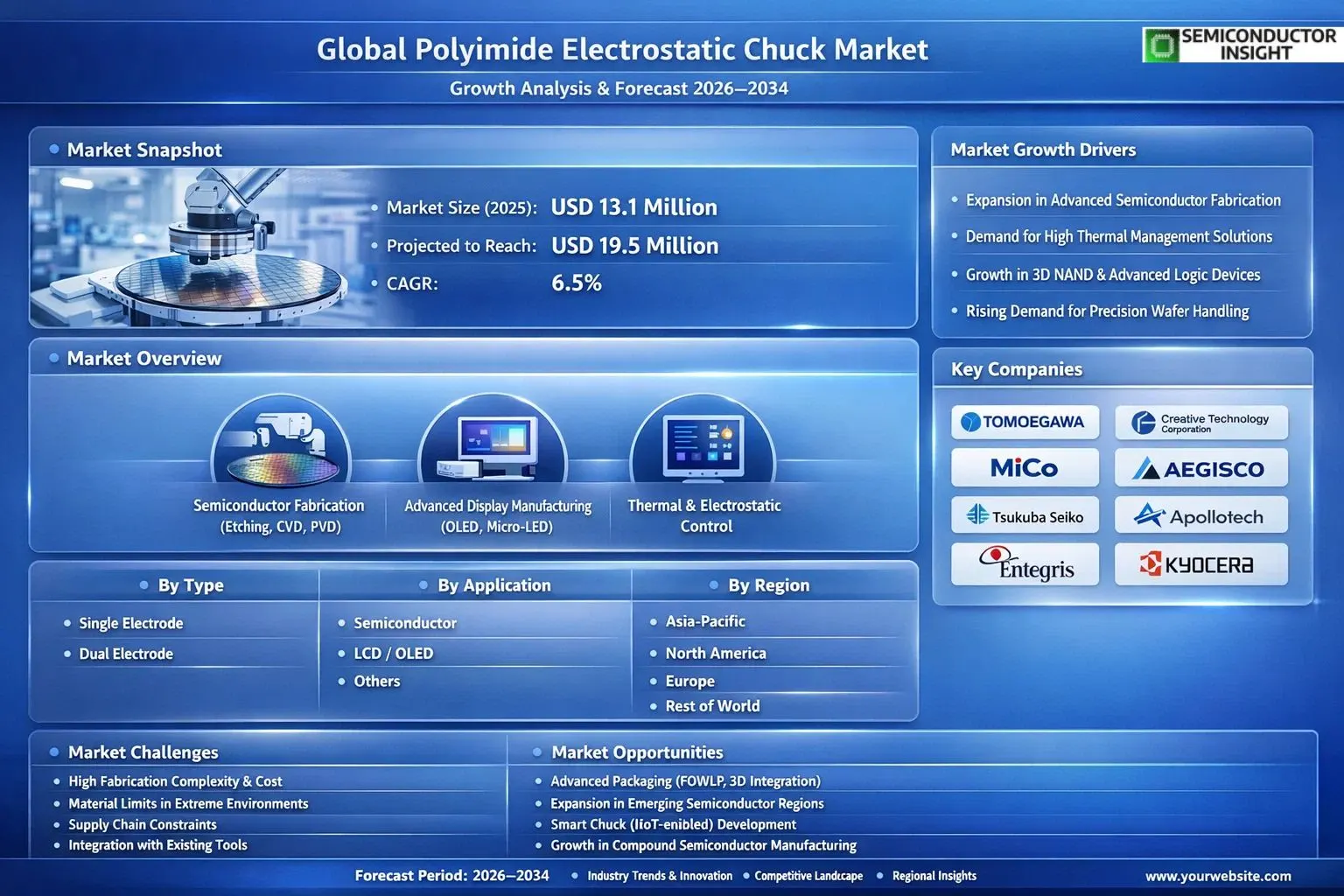

Global Polyimide Electrostatic Chuck market size was valued at USD 13.1 million in 2025. The market is projected to grow from USD 13.9 million in 2026 to USD 19.5 million by 2034, exhibiting a CAGR of 6.5% during the forecast period.

A Polyimide Electrostatic Chuck (ESC) is a specialized wafer-holding device used primarily in semiconductor manufacturing processes such as etching, chemical vapor deposition (CVD), and physical vapor deposition (PVD). Unlike traditional ceramic ESCs, it utilizes polyimide,a high-performance polymer known for its excellent thermal stability, mechanical strength, and dielectric properties,as the key dielectric material. This construction offers distinct advantages, including lighter weight, superior corrosion resistance, and enhanced thermal management during high-precision fabrication steps.

The market’s growth is fundamentally driven by the relentless expansion and technological advancement of Global semiconductor industry, which demands ever-more precise and reliable wafer-handling solutions to improve yield and productivity. Furthermore, the proliferation of advanced display technologies like OLED and micro-LED is creating additional demand in the LCD/OLED application segment. The competitive landscape is highly concentrated, with Japanese company TOMOEGAWA holding a dominant position; it accounted for approximately 60% of Global revenue share in 2025. Other key players include Creative Technology Corporation, MiCo, AEGISCO, Tsukuba Seiko, and Apollotech.

MARKET DRIVERS

Expansion in Advanced Semiconductor Fabrication

The relentless demand for smaller, more powerful semiconductors is a primary driver for the Polyimide Electrostatic Chuck Market. These specialized chucks, known for their excellent thermal stability and dielectric properties, are essential in advanced lithography and etching processes for sub-7nm nodes. The industry’s shift towards complex 3D NAND and high-volume manufacturing of advanced logic devices necessitates precise, contamination-free wafer clamping, directly boosting demand for high-performance polyimide electrostatic chucks. Semiconductor capital expenditure remains high, fueling market growth.

Demand for High Thermal Management Solutions

Effective thermal control is critical during wafer processing. Polyimide materials offer superior thermal resistance and uniform heat dissipation compared to some traditional ceramics, making these chucks vital for processes requiring rapid temperature cycling or extreme temperatures. This capability directly improves yield rates in critical steps like chemical vapor deposition (CVD) and atomic layer deposition (ALD), driving adoption. Manufacturers are investing in polyimide electrostatic chuck designs that enhance thermal conductivity for next-generation tools.

➤ Global push for compound semiconductor and power device manufacturing further catalyzes demand, as these processes benefit from the chuck’s compatibility with harsh chemistries and stable electrical performance.

The material’s inherent durability and resistance to plasma erosion extend operational lifespans, reducing total cost of ownership for fabrication facilities and establishing the polyimide electrostatic chuck as a cost-effective, high-reliability component in the equipment ecosystem.

MARKET CHALLENGES

Technical Complexity and High Fabrication Costs

A significant challenge in the Polyimide Electrostatic Chuck Market is the sophisticated engineering and manufacturing required. Achieving the precise flatness, embedded electrode patterns, and consistent material properties free of micro-voids demands specialized, capital-intensive processes. This complexity results in high unit costs and creates a substantial barrier to entry for new suppliers, consolidating the market among a few established players. Furthermore, integration with existing semiconductor tool platforms requires extensive validation.

Other Challenges

Performance Limitations in Extreme Environments

While polyimide offers excellent general stability, certain ultra-high-temperature processes or exceptionally aggressive plasma chemistries can challenge material limits, potentially leading to faster degradation than some advanced ceramics. This necessitates ongoing material science research and development.

Supply Chain and Material Sourcing Constraints

The market relies on high-purity, specialty-grade polyimide precursors and adhesives. Disruptions in this niche chemical supply chain or geopolitical trade tensions can lead to procurement delays and price volatility, impacting production schedules for chuck manufacturers and, by extension, semiconductor equipment makers.

MARKET RESTRAINTS

Competition from Alternative Materials and Designs

Growth in the Polyimide Electrostatic Chuck Market faces restraint from competing chuck technologies. Advanced anodic ceramic chucks, for instance, offer superior hardness and may be preferred in certain abrasive process environments. Furthermore, the development of hybrid chucks that combine material layers poses a competitive threat. The high cost of completely retrofitting or replacing existing tooling with new chuck systems can also slow adoption rates, as manufacturers weigh the return on investment against incremental performance gains.

Cyclical Nature of Semiconductor Capital Investment

The market is intrinsically tied to the capital expenditure cycles of Global semiconductor industry. During downturns or periods of reduced equipment spending, purchases of critical but expensive components like polyimide electrostatic chucks are often deferred. This cyclicality introduces volatility and forecasting challenges for suppliers, who must manage inventory and production capacity carefully to avoid oversupply during market corrections.

MARKET OPPORTUNITIES

Innovation for Next-Generation Device Packaging

The rise of advanced packaging techniques like Fan-Out Wafer-Level Packaging (FOWLP) and 3D integration presents a substantial opportunity. These processes require precise handling and thermal management of thinner, larger, or panel-form substrates, where polyimide electrostatic chucks can provide solutions. Developing chucks optimized for heterogeneous integration and panel-level processing opens a new, high-growth segment beyond traditional front-end wafer fabrication.

Expansion into Emerging Semiconductor Geographies

Government-led initiatives and substantial investments in domestic semiconductor manufacturing capacity in regions like North America, India, and parts of Southeast Asia are creating greenfield opportunities. These new fabrication facilities will require outfitting with state-of-the-art equipment, including the latest polyimide electrostatic chuck technology. Suppliers who establish strong local partnerships and service networks can capture significant market share in these emerging manufacturing hubs for the long term.

Development of Smart Chuck Technologies

Integrating sensors for real-time monitoring of chuck surface temperature, clamping force, and particle levels represents a forward-looking opportunity. The advent of the Industrial Internet of Things (IIoT) in fabs enables predictive maintenance and process optimization. Polyimide electrostatic chucks with embedded diagnostics can command premium pricing and deepen customer loyalty by improving tool uptime and process yield, aligning with the industry’s smart manufacturing goals.

Polyimide Electrostatic Chuck Market Trends

Increasing Adoption in Advanced Semiconductor Processes

The primary trend driving the Polyimide Electrostatic Chuck Market is its critical integration within advanced semiconductor fabrication. As chip geometries shrink and manufacturing complexity rises, the demand for precise and reliable wafer handling solutions increases. Polyimide ESCs, with their superior heat and corrosion resistance compared to traditional ceramic chucks, provide the stability required for processes like etching and chemical vapor deposition at finer nodes. This trend is solidified by the market’s concentration in leading semiconductor manufacturing regions, primarily in Japan and South Korea.

Other Trends

Dual Electrode Design Gaining Traction

A clear product evolution trend within the Polyimide Electrostatic Chuck Market is the shift towards dual-electrode configurations. These systems offer enhanced clamping force and improved heat dissipation, which are critical for handling larger wafer sizes and managing thermal budgets in advanced lithography. The performance advantages are leading to a faster adoption rate for dual-electrode polyimide chucks, indicating a shift in product preference among equipment manufacturers seeking higher process yields.

Expansion Beyond Core Semiconductor Application

While semiconductors dominate as the primary application for polyimide electrostatic chucks, a significant trend is their growing utilization in flat panel display manufacturing for LCD and OLED production. The same requirements for contamination-free, electrostatic wafer holding that benefit semiconductor fabs are crucial in display panel fabrication. This diversification represents a strategic expansion of the Polyimide Electrostatic Chuck Market into adjacent high-tech manufacturing sectors, broadening the total addressable market.

Regional Consumption Patterns and Supply Chain Dynamics

A defining market trend is the strong geographical correlation between production and consumption. Japan remains the dominant consumer, which aligns with its position as a hub for both polyimide ESC production and advanced semiconductor manufacturing. This regional concentration influences supply chain strategies and competitive dynamics, with leading suppliers like TOMOEGAWA leveraging local expertise. However, the growth of semiconductor capacity in other parts of Asia presents a trend towards gradual geographical diversification in consumption, potentially reshaping future market landscapes.

COMPETITIVE LANDSCAPE

Key Industry Players

A Consolidated Market Led by Specialized Material Innovators

Global Polyimide Electrostatic Chuck (ESC) market is characterized by a high degree of concentration, with technological expertise and material science forming the primary competitive moats. TOMOEGAWA of Japan is the undisputed market leader, commanding a dominant share of global revenue. This position is attributed to its deep expertise in polyimide films and advanced manufacturing processes, which are critical for producing high-performance, reliable chucks essential for semiconductor fabrication. The competitive structure is oligopolistic, with production heavily concentrated in Japan and South Korea, reflecting the close ties between ESC manufacturers and the leading semiconductor equipment and fabrication plants in these regions. Market entry is challenging due to stringent performance requirements, long qualification cycles with chipmakers, and the need for continuous R&D to keep pace with evolving semiconductor node technologies.

Beyond the dominant player, several other companies have carved out significant niches. These firms compete by offering specialized solutions, targeting specific application segments like advanced packaging or flat panel display (FPD) manufacturing, or by providing regional support and customization. Players such as Creative Technology Corporation and MiCo have been enhancing their technological capabilities to improve their market standing. The competitive dynamics are further influenced by the shift towards dual-electrode designs, which offer superior chucking performance for next-generation processes. As the market grows, these established niche players and emerging contenders are focusing on innovation in chuck design, thermal management, and longevity to capture share in the high-value semiconductor segment, which constitutes the vast majority of demand.

List of Key Polyimide Electrostatic Chuck Companies Profiled

- TOMOEGAWA

- Creative Technology Corporation

- MiCo

- AEGISCO

- Tsukuba Seiko

- Apollotech

- Shinko Electric Industries

- Entegris, Inc.

- NGK Insulators, Ltd. (NBK)

- Kyocera Corporation

- Applied Materials, Inc. (via internal or sourced components)

- Lam Research Corporation (via internal or sourced components)

- Tokyo Electron Limited (TEL)

- Shin-Etsu Chemical Co., Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Dual Electrode chucks are the established market leader due to their superior performance and reliability for complex, high-precision manufacturing. This dominance is reinforced by broader compatibility with advanced fabrication processes and a value proposition centered on operational stability. The segment benefits from strong research and development focus, ensuring its design evolution keeps pace with next-generation semiconductor nodes. Furthermore, their integration offers enhanced process control, which is critical for minimizing yield loss in capital-intensive production environments, solidifying their preferred status among equipment manufacturers. |

| By Application |

|

Semiconductor fabrication is the cornerstone application, driving the majority of demand and technological innovation. The relentless miniaturization and complexity of integrated circuits necessitate the exceptional thermal and chemical resistance offered by polyimide materials, making these chucks indispensable for processes like etching and deposition. This segment’s growth is intrinsically linked to global investments in chip manufacturing capacity and the transition to more advanced wafer sizes. Additionally, the push for heterogeneous integration and advanced packaging creates new, demanding use-cases that further entrench the need for high-performance polyimide electrostatic chucks within semiconductor fabs. |

| By End User |

|

Semiconductor Foundries represent the most critical and demanding end-user segment, characterized by an uncompromising focus on yield, uptime, and process uniformity. Their high-volume production models create consistent, bulk demand for reliable chucking solutions. The technological roadmap of leading foundries, which continually adopts more intricate and heat-sensitive processes, directly dictates the performance requirements for polyimide chucks. This segment also exerts significant influence on product development cycles, as chuck manufacturers must closely collaborate with foundries to qualify new materials and designs for use in cutting-edge fabrication tools, creating a high barrier to entry for suppliers. |

| By Manufacturing Technology |

|

Advanced Composite Chucks are emerging as a key growth area, offering enhanced performance characteristics over standard designs. These solutions integrate polyimide with other specialized materials or coatings to improve properties like thermal conductivity, wear resistance, or electrostatic uniformity for specific applications. The development of these composites is driven by the need to address unique challenges in next-generation manufacturing, such as extreme ultraviolet lithography. This segment allows manufacturers to offer differentiated, high-value products and build stronger technical partnerships with leading equipment OEMs and end-users seeking a competitive edge in their process capabilities. |

| By Geographic Production Hub |

|

Japan & South Korea constitute the dominant production hub, characterized by deep-rooted expertise in advanced materials and precision manufacturing for the semiconductor industry. This region benefits from a synergistic ecosystem comprising leading chuck manufacturers, major semiconductor equipment suppliers, and world-class end-users, facilitating rapid innovation and stringent quality validation. The concentration of technical knowledge and established supply chains creates significant economies of scale and a high barrier for new regional competitors. Furthermore, proximity to key consumer markets in East Asia allows for responsive customer support and collaborative development, reinforcing the region’s central role in Global supply and technological advancement of these critical components. |

Regional Analysis: Polyimide Electrostatic Chuck Market

Asia-Pacific

The region hosts the world’s densest cluster of semiconductor foundries and memory chip manufacturers. This immense manufacturing base creates a continuous, high-volume demand cycle for polyimide electrostatic chucks, which are essential for processes like etching, deposition, and inspection in advanced node production.

A mature ecosystem of material suppliers, equipment OEMs, and research institutions fosters rapid innovation and cost-effective production of polyimide electrostatic chuck components. This close collaboration accelerates the development of chucks with higher thermal stability and finer pixel patterns for next-gen applications.

National policies and substantial funding in countries like China, South Korea, and Japan explicitly target semiconductor sovereignty and capacity expansion. These initiatives directly spur capital expenditure on new fabs, thereby driving procurement of critical supporting equipment including advanced polyimide electrostatic chucks.

Beyond front-end fabrication, the region is a leader in advanced packaging technologies. The growth of heterogenous integration and 3D packaging creates additional demand for polyimide electrostatic chucks in backend processes, where their gentle handling and electrostatic precision are crucial for delicate stacked dies.

North America

North America maintains a strong position in the polyimide electrostatic chuck market, characterized by high-value, innovation-driven demand. The region is home to leading semiconductor equipment manufacturers and fabless design companies whose R&D activities and pilot production lines require cutting-edge chucking solutions. Demand is particularly robust for polyimide electrostatic chucks used in compound semiconductor and photonics manufacturing, areas where North American technological leadership is pronounced. Furthermore, significant investments in domestic chip manufacturing capacity, incentivized by recent legislative acts, are expected to catalyze new demand, though the market volume remains focused on advanced, specialized applications rather than the high-volume production seen in Asia-Pacific.

Europe

The European polyimide electrostatic chuck market is driven by a specialized industrial base focusing on precision engineering and research applications. Key demand stems from the automotive semiconductor sector, power device manufacturing, and esteemed research institutes conducting advanced materials science. European equipment suppliers often integrate polyimide electrostatic chucks into highly customized, automated systems for niche markets like MEMS and sensor production. While the region’s overall semiconductor fabrication capacity is smaller, its emphasis on quality, reliability, and specific technical specifications for harsh environment applications supports a stable, high-margin segment within Global polyimide electrostatic chuck landscape.

South America

The South American market for polyimide electrostatic chucks is in a nascent but developing stage, primarily serving downstream industrial and academic research needs rather than large-scale semiconductor manufacturing. Demand is sporadic and often tied to equipment upgrades in university laboratories, specialized electronics assembly, and maintenance contracts for existing imported machinery. The market is largely served by global distributors, with limited local technical support infrastructure. Growth is slow and contingent on broader regional economic stability and potential future investments in higher-value industrial sectors, making it a minor but consistent part of Global supply network.

Middle East & Africa

This region represents an emerging frontier with specific, strategically driven demand points. Investments in technological diversification, particularly in Gulf nations, are creating opportunities in education and research infrastructure, which occasionally require polyimide electrostatic chucks for specialized equipment. The market is characterized by project-based procurement rather than continuous operational demand. While not a major consumption center for high-volume semiconductor production, the region’s focus on building knowledge economies and strategic partnerships with global tech firms may lead to incremental, long-term growth in the adoption of advanced manufacturing tools, including polyimide electrostatic chucks for pilot lines and R&D facilities.

Report Scope

This market research report provides a comprehensive analysis of the Polyimide Electrostatic Chuck Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining the current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductor manufacturing in powering advancements across industries.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, material advancements, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Polyimide Electrostatic Chuck Market?

-> Global Polyimide Electrostatic Chuck Market was valued at USD 13.1 million in 2025 and is projected to reach USD 19.5 million by 2034, growing at a CAGR of 6.5% during the forecast period.

Which key companies operate in Polyimide Electrostatic Chuck Market?

-> Key players include TOMOEGAWA, Creative Technology Corporation, MiCo, AEGISCO, Tsukuba Seiko, and Apollotech, among others.

What are the key growth drivers?

-> Key growth drivers include the development of the semiconductor industry, increasing demand for advanced manufacturing processes, and the superior characteristics of polyimide chucks (lighter, more heat-resistant, and more corrosion-resistant) compared to traditional ceramic ESCs.

Which region dominates the market?

-> The primary markets are concentrated in Asia, with Japan being the largest consumer market, accounting for 49.37% of global revenue share in 2025. Key producer regions are also Japan and South Korea.

What are the emerging trends?

-> Emerging trends include the growing adoption of dual-electrode polyimide electrostatic chucks due to expected faster CAGR, technological advancements in wafer handling, and expanding applications beyond semiconductors into LCD/OLED and other high-tech fields.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...