MARKET INSIGHTS

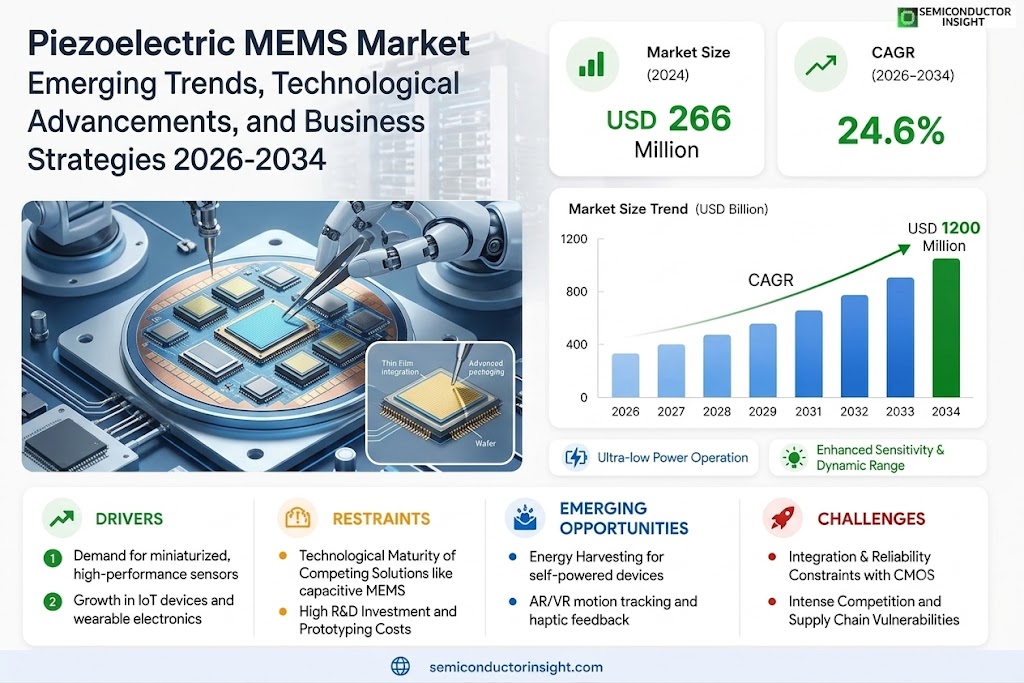

Global Piezoelectric MEMS Market was valued at USD 266 million in 2024 and is projected to reach USD 1200 million by 2032, exhibiting a CAGR of 24.6% during the forecast period.

A piezoelectric microelectromechanical system (piezoMEMS) is a miniature or microscopic device that uses piezoelectricity to generate motion and carry out its tasks. It is a microelectromechanical system that takes advantage of an electrical potential that appears under mechanical stress.

Piezoelectric microelectromechanical system (piezoMEMS) technology combines the structure of microelectromechanical system (MEMS) and the characteristics of piezoelectric materials. MEMS is a micro device or system that integrates micro-mechanisms, micro-sensors, micro-actuators, and signal processing and control circuits, while piezoelectric materials have the characteristics of generating electric charges when subjected to external forces, or mechanical deformation under the action of electric fields. Therefore, piezoelectric MEMS can realize functions such as sensing, driving and energy collection, and has a wide range of applications in high-performance sensors, actuators, energy harvesters and other fields.

MARKET DRIVERS

Proliferation of Consumer Electronics and IoT Devices

The relentless growth in the adoption of smartphones, wearables, and a vast array of Internet of Things (IoT) sensors is a primary driver for the Piezoelectric MEMS market. These devices extensively utilize piezoelectric MEMS components such as microphones, inkjet printer heads, and accelerometers for sensing and actuation. The demand for miniaturized, low-power, and high-performance components is directly fueling market expansion, with the global market for MEMS microphones alone projected to see substantial growth.

Advancements in Healthcare and Automotive Applications

Significant technological advancements are expanding the application scope of piezoelectric MEMS into critical sectors. In healthcare, they are essential for miniaturized medical devices, including implantable pressure sensors and ultrasonic imaging systems. In the automotive industry, the push towards autonomous driving and enhanced safety features is accelerating the use of piezoelectric MEMS in inertial sensors, tire pressure monitoring systems, and ultrasonic parking assistance.

➤ The expansion of 5G infrastructure and emerging Industry 4.0 applications is creating new, high-volume demand for precise timing devices like piezoelectric MEMS oscillators and resonators.

Furthermore, regulatory mandates and a renewed industrial focus on energy harvesting solutions are driving the development of piezoelectric MEMS energy harvesters, which can power low-energy wireless sensors, contributing to the growth of sustainable and maintenance-free IoT networks.

MARKET CHALLENGES

High Fabrication Complexity and Cost Sensitivity

The design and fabrication of Piezoelectric MEMS devices are inherently complex, requiring specialized materials like aluminum nitride (AlN) or lead zirconate titanate (PZT) and sophisticated manufacturing processes. This complexity leads to higher production costs compared to traditional MEMS, making it challenging to achieve the price points demanded by high-volume consumer markets. The need for high-precision deposition and patterning of piezoelectric thin films also presents significant yield challenges.

Other Challenges

Integration and Reliability Constraints

Integrating piezoelectric materials with standard CMOS processes can be difficult, potentially compromising device performance or reliability. Ensuring long-term stability and resilience under varying environmental conditions, such as temperature fluctuations and mechanical stress, remains a critical hurdle for applications in automotive and industrial settings.

Intense Competition and Supply Chain Vulnerabilities

The market faces stiff competition from established capacitive MEMS technologies and new entrants. Additionally, reliance on specific raw materials and specialized fabrication equipment creates vulnerabilities in the supply chain, which can lead to production delays and increased costs, particularly during periods of high demand or global disruption.

MARKET RESTRAINTS

Technological Maturity of Competing Solutions

A key restraint for the Piezoelectric MEMS market is the entrenched position and continuous improvement of alternative sensing technologies, particularly capacitive MEMS. For many applications, capacitive solutions offer a cost-effective and well-understood alternative, making it difficult for piezoelectric MEMS to displace them without demonstrating a clear and necessary performance or power consumption advantage.

High R&D Investment and Prototyping Costs

The significant research and development expenditure required to innovate and bring new Piezoelectric MEMS products to market acts as a barrier, especially for small and medium-sized enterprises. The costs associated with prototyping, testing, and qualification for stringent applications like automotive or medical devices can delay time-to-market and limit the pace of innovation and market penetration.

MARKET OPPORTUNITIES

Emerging Applications in Energy Harvesting and AR/VR

The growing demand for battery-less or energy-autonomous devices presents a significant opportunity for piezoelectric MEMS energy harvesters. These components can convert ambient vibrations into electrical energy, powering sensors in remote or hard-to-reach locations. Simultaneously, the rapid growth of Augmented Reality (AR) and Virtual Reality (VR) markets creates demand for high-precision motion tracking and haptic feedback sensors, areas where piezoelectric MEMS excel.

Expansion in Biomedical and Industrial IoT

There is considerable potential for Piezoelectric MEMS in next-generation biomedical devices, such as lab-on-a-chip systems for point-of-care diagnostics and advanced drug delivery mechanisms. In the industrial sector, the Industrial Internet of Things (IIoT) drives the need for robust, wireless condition monitoring sensors that can operate in harsh environments, offering a robust growth vector for piezoelectric MEMS pressure, accelerometer, and ultrasonic flow sensors.

Piezoelectric MEMS Market Trends

Exponential Growth Driven by Connectivity and Miniaturization

The global Piezoelectric MEMS market is undergoing a significant expansion, projected to grow from a valuation of $266 million in 2024 to $1200 million by 2032, representing a remarkable compound annual growth rate (CAGR) of 24.6%. This surge is primarily fueled by the increasing integration of these miniature devices into next-generation technologies. Piezoelectric MEMS combine the structural principles of microelectromechanical systems (MEMS) with the unique properties of piezoelectric materials, enabling functions like sensing, actuation, and energy harvesting in an ultra-compact form factor. The market is currently dominated by a few key players, with Bosch, STMicroelectronics, and ROHM collectively holding over 84% of the global market share, and the Americas region leading consumption with approximately 48% of the market.

Other Trends

Dominance in Sensor Applications

Market segmentation by type reveals sensors as the leading category. This dominance is directly linked to the core drivers of market growth. The high sensitivity and low power consumption of piezoelectric MEMS sensors make them ideal for a wide array of applications. In the consumer electronics and wearable device sector, they are crucial for monitoring health metrics such as heart rate and blood pressure. Furthermore, their role in industrial automation for precision sensing and control is another significant contributor to their market leadership over actuators.

Regional Market Dynamics and Application Diversification

Geographically, while the Americas hold the largest market share, Europe and Asia-Pacific are substantial and growing markets with shares of about 26% and 24%, respectively. The application landscape is diversifying rapidly. The consumer electronics segment is a major driver, but significant growth is also emerging from the healthcare and industrial sectors. In healthcare, piezoelectric MEMS are advancing remote patient monitoring systems, while in industrial settings, they are key enablers of intelligent manufacturing and automation processes. This diversification, supported by continuous technological advancements and increased R&D investment, ensures the piezoelectric MEMS market’s robust and sustained growth trajectory, moving beyond a reliance on any single industry.

COMPETITIVE LANDSCAPE

Key Industry Players

A Consolidating Market with a Dominant Trio

The global Piezoelectric MEMS market exhibits a high degree of concentration, with the top three companies—Bosch, STMicroelectronics, and ROHM—collectively commanding over 84% of the market share. Bosch is universally recognized as the market leader, leveraging its extensive expertise in MEMS technology and massive scale in automotive and consumer electronics applications. STMicroelectronics follows closely, with a strong presence in sensors and actuators for a wide array of applications, while ROHM solidifies the leading trio with its focus on high-performance electronic components. This concentrated structure is driven by significant R&D investments, extensive patent portfolios, and the complex fabrication processes required for piezoMEMS devices, which create high barriers to entry. These established players are continuously innovating to enhance the sensitivity, reliability, and energy efficiency of their products to meet the growing demands from the Internet of Things (IoT), 5G, and automotive sectors.

Beyond the dominant players, the landscape includes several other significant companies that compete effectively in specific niches or regional markets. Companies like TDK Corporation and Murata Manufacturing are notable for their strong capabilities in piezoelectric materials and components, allowing them to compete in specialized sensor and actuator applications. NXP Semiconductors and Analog Devices bring robust semiconductor expertise to the market, focusing on integrated solutions. Startups and specialized firms such as Vesper and Akoustis Technologies are making strides with innovative products, particularly in acoustic sensors and RF filters for 5G. Taiwanese and Chinese manufacturers, including ASE Group and Goertek, are also growing in importance, often focusing on the cost-effective manufacturing of MEMS components for the massive consumer electronics market, thereby increasing competitive pressure globally.

List of Key Piezoelectric MEMS Companies Profiled

- Bosch

- STMicroelectronics

- ROHM

- TDK Corporation

- Murata Manufacturing

- NXP Semiconductors

- Analog Devices, Inc.

- Vesper

- Akoustis Technologies

- ASE Group

- Goertek

- Infineon Technologies

- Texas Instruments

- Panasonic Corporation

- Realmagicsemi

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Sensor technology represents the dominant force in the Piezoelectric MEMS market due to its critical role in converting mechanical stimuli into electrical signals across a vast range of modern applications. The relentless proliferation of IoT and the rollout of 5G infrastructure have created unprecedented demand for highly sensitive, low-power sensors for data acquisition. Concurrently, the surge in wearable health monitors and smart consumer electronics relies heavily on these sensors for functions like motion detection, health parameter monitoring, and user interface control, cementing their leading market position through broad applicability and technological maturity. |

| By Application |

|

Consumer Electronics is the foremost application segment, driven by the massive and continuous integration of Piezoelectric MEMS into smartphones, wearables, and other smart devices. The insatiable consumer demand for devices with advanced features like haptic feedback, precise motion sensing, and improved audio components creates a robust and ever-expanding market. This segment benefits significantly from high-volume production cycles and rapid technological adoption, making it the primary growth engine. The healthcare and industrial segments, while also showing strong growth potential, are currently secondary in market influence compared to the sheer scale of consumer electronics adoption. |

| By End User |

|

OEMs (Original Equipment Manufacturers) constitute the leading end-user segment, as they are the primary integrators of Piezoelectric MEMS components into final products for consumer, industrial, and healthcare markets. Their dominance stems from the need for reliable, high-volume supply chains to mass-produce everything from smartphones to industrial automation equipment. The continuous innovation and shorter product lifecycles in their respective industries fuel consistent demand. While R&D institutes are crucial for pioneering next-generation applications and system integrators play a key role in specialized implementations, the market scale and purchasing power of OEMs make them the most influential customer group. |

| By Material |

|

Lead Zirconate Titanate (PZT) is the leading material segment, favored for its superior piezoelectric properties, including high electromechanical coupling coefficients and excellent temperature stability, which are essential for high-performance sensors and actuators. Its well-established fabrication processes and proven reliability in demanding applications across consumer electronics and industrial systems contribute to its widespread adoption. Although materials like Aluminum Nitride are gaining traction for CMOS compatibility and lead-free requirements, PZT’s performance advantages and extensive industry experience maintain its position as the material of choice for a majority of current Piezoelectric MEMS applications. |

| By Functionality |

|

Sensing functionality is the preeminent segment, as the core value of Piezoelectric MEMS lies in its ability to provide precise, low-power detection of pressure, force, acceleration, and acoustic waves. This capability is fundamental to the operation of countless modern devices, from automotive airbag triggers and smartphone orientation sensors to medical diagnostic equipment. The drive for greater intelligence and connectivity in systems through the Internet of Things is fundamentally a drive for more sophisticated sensing, ensuring this segment’s continued leadership. While actuation is vital for precise micro-movement and energy harvesting holds promise for powering small electronic devices, the immediate and ubiquitous need for sensing solutions solidifies its dominant market role. |

Regional Analysis: Piezoelectric MEMS Market

Asia-Pacific

The region’s dominance is anchored in its unparalleled electronics manufacturing capacity. The extensive network of contract manufacturers and component suppliers provides a seamless pipeline for integrating Piezoelectric MEMS into consumer devices, ensuring rapid time-to-market and economies of scale that are difficult to match elsewhere in the world.

Strong governmental support through subsidies, tax incentives, and national science and technology programs actively promotes the development and adoption of MEMS technologies. This fosters a vibrant research environment in universities and corporate R&D centers, leading to continuous advancements in Piezoelectric MEMS performance and new application areas.

Beyond consumer electronics, the demand is fueled by burgeoning sectors like automotive, where Piezoelectric MEMS are used in tire pressure monitoring and engine management, and industrial automation, for precise sensing and fluid control. The early adoption of IoT devices across smart cities and homes in the region further expands the addressable market.

A mature and highly integrated semiconductor supply chain, from raw materials to advanced packaging, provides significant cost and logistical advantages. This ecosystem allows for efficient production of Piezoelectric MEMS at competitive prices, making the region the preferred sourcing destination for global technology companies.

North America

North America represents a highly advanced and innovation-driven market for Piezoelectric MEMS, characterized by strong demand from the aerospace, defense, and medical technology sectors. The presence of leading technology companies and research institutions, particularly in the United States, fuels the development of high-performance, specialized MEMS devices for demanding applications. These include inertial navigation systems, medical ultrasound imaging transducers, and energy harvesting solutions. The region’s market is defined by a focus on cutting-edge R&D, stringent quality requirements, and the early adoption of new technologies in premium product segments. Collaborative efforts between academia, national laboratories, and industry players continue to push the boundaries of Piezoelectric MEMS capabilities.

Europe

Europe maintains a strong position in the Piezoelectric MEMS market, with a distinct emphasis on automotive and industrial applications. The region is home to major automotive manufacturers and tier-one suppliers that extensively utilize these sensors for system monitoring, active suspension, and safety features. A robust industrial automation sector also drives demand for precise piezoelectric actuators and sensors in manufacturing equipment. European market dynamics are shaped by stringent regulatory standards for safety and environmental performance, which encourage the integration of sophisticated sensing technologies. Well-funded collaborative research projects within the European Union further support innovation, particularly in developing MEMS for smart systems and green technologies.

South America

The Piezoelectric MEMS market in South America is in a developing stage, with growth primarily driven by the gradual expansion of its consumer electronics and automotive industries. While the market size is smaller compared to other regions, there is increasing adoption in applications like mobile devices and basic industrial sensors. The region faces challenges related to technological infrastructure and local manufacturing capacity, often relying on imports for advanced components. However, economic stabilization efforts and growing investments in industrial modernization in countries like Brazil and Argentina are creating a slowly expanding base for future market growth, focusing on cost-effective solutions.

Middle East & Africa

The Middle East & Africa region presents a niche but emerging market for Piezoelectric MEMS, with demand largely concentrated in the oil and gas industry for condition monitoring and downhole sensing applications. Wealthier Gulf Cooperation Council (GCC) nations are also seeing increased adoption in consumer electronics and burgeoning smart city projects. The broader African market remains limited, characterized by nascent industrial and technological development. Growth potential is linked to infrastructure development and economic diversification plans in key countries, though the market is currently defined by import dependency and a focus on specific industrial applications rather than broad-based consumer adoption.

Report Scope

This market research report provides a comprehensive analysis of the Piezoelectric MEMS Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Piezoelectric MEMS Market?

-> Global Piezoelectric MEMS Market was valued at USD 266 million in 2024 and is projected to reach USD 1200 million by 2032, exhibiting a CAGR of 24.6% during the forecast period.

Which key companies operate in Piezoelectric MEMS Market?

-> Key players include Bosch, STMicroelectronics, ROHM, and Realmagicsemi, among others. Global top 3 companies hold a share over 84%.

What are the key growth drivers?

-> Key growth drivers include the development of the Internet of Things (IoT) and 5G communications, the popularity of wearable devices and consumer electronics, growth in demand for medical sensors, promotion of industrial automation and intelligent manufacturing, and continuous technological progress and R&D investment.

Which region dominates the market?

-> Americas is the largest market, with a share of about 48%, followed by Europe with a share of about 26% and APAC with a share of about 24%.

What are the emerging trends?

-> Emerging trends include the integration of piezoelectric MEMS in high-performance sensors, actuators, and energy harvesters, and its expanding applications across IoT, healthcare monitoring, and industrial automation systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...