MARKET INSIGHTS

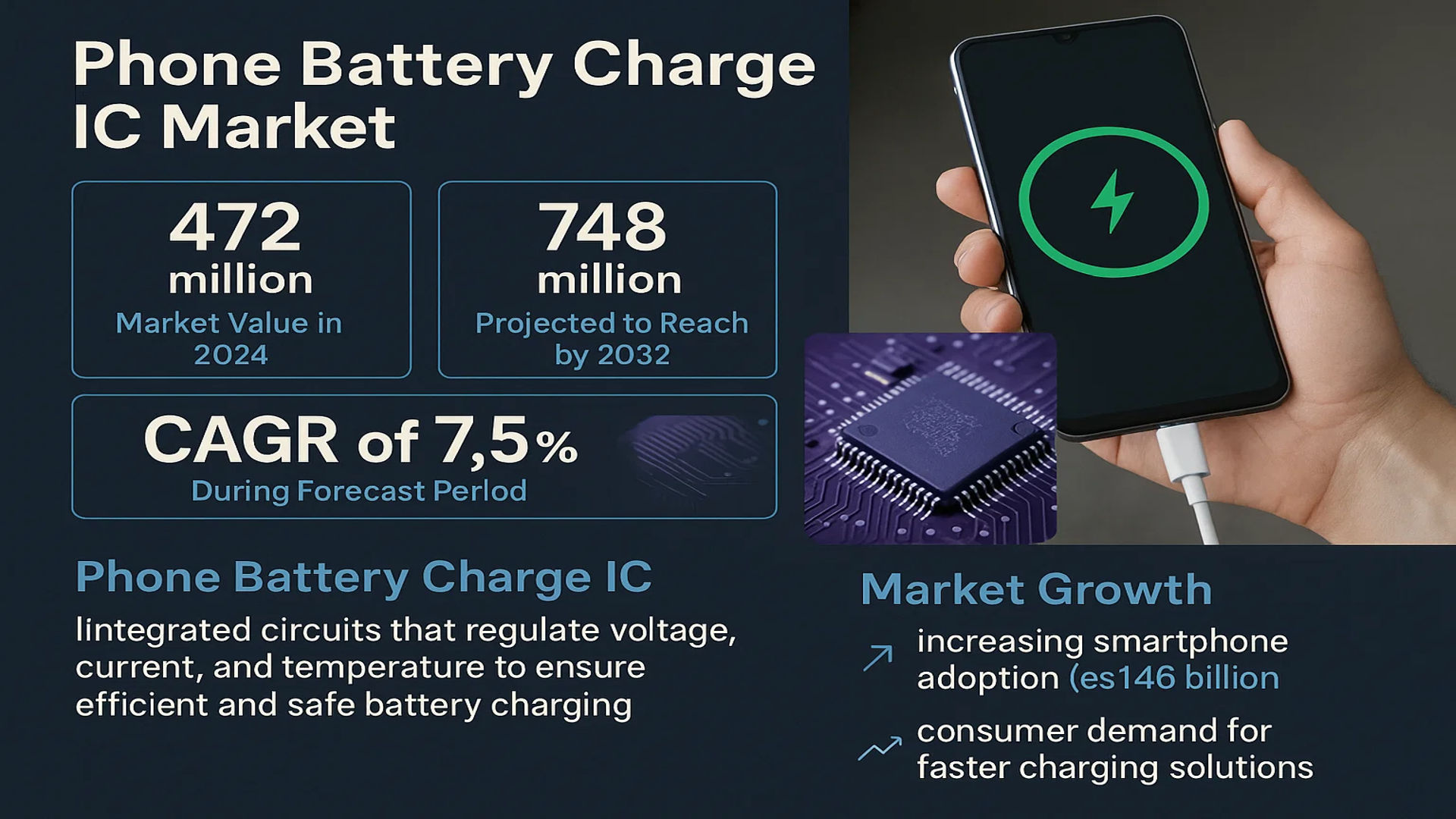

The global Phone Battery Charge IC Market was valued at 472 million in 2024 and is projected to reach US$ 748 million by 2032, at a CAGR of 7.5% during the forecast period.

A Phone Battery Charge IC is an integrated circuit that serves as a critical component in smartphone power management systems. These ICs regulate charging processes by controlling voltage, current, and temperature parameters to ensure efficient and safe battery charging. They support various charging protocols including fast charging (up to 100W in premium devices) and wireless charging standards (Qi-certified solutions reaching 15W), while implementing multiple protection mechanisms against overcharging and overheating.

The market growth is primarily driven by increasing smartphone adoption (estimated at 1.46 billion units shipped globally in 2023) and consumer demand for faster charging solutions. Technological advancements in gallium nitride (GaN) based ICs, offering 93-95% power conversion efficiency, and the development of AI-powered adaptive charging algorithms are shaping the industry landscape. Major manufacturers including Texas Instruments, Qualcomm, and Maxim Integrated (now part of Analog Devices) continue to innovate with more compact and efficient charging solutions to meet evolving market requirements.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Adoption of Fast-Charging Technologies to Fuel Demand for Advanced Charge ICs

The smartphone industry is witnessing unprecedented demand for fast-charging solutions, with consumers prioritizing devices that offer quick battery replenishment. Modern smartphones increasingly incorporate 30W to 120W fast-charging capabilities, requiring sophisticated charge ICs capable of handling higher current while managing heat dissipation efficiently. This demand is further amplified by the growing battery capacities in flagship devices, which now frequently exceed 5,000mAh. Charge IC manufacturers are responding with innovative solutions like multi-phase charging architectures and adaptive voltage scaling, enabling faster power delivery without compromising battery lifespan.

Proliferation of 5G Smartphones Driving Innovation in Power Management

The global transition to 5G networks is significantly impacting power management requirements in smartphones. 5G modems consume substantially more power than their 4G counterparts, creating a need for more efficient charging systems. Charge ICs are evolving to address this challenge through intelligent power allocation between charging and device operation, particularly during simultaneous charging and 5G data transmission. Manufacturers are integrating advanced algorithms that dynamically adjust charging parameters based on real-time power consumption, ensuring optimal battery health even with increased power demands.

Furthermore, the growing emphasis on sustainability is prompting charge IC developers to focus on energy efficiency. Modern charge ICs now achieve conversion efficiencies above 95%, significantly reducing energy waste during charging cycles. This improvement not only benefits end-users through lower electricity consumption but also helps manufacturers meet increasingly stringent environmental regulations across multiple markets.

MARKET RESTRAINTS

Thermal Management Challenges in High-Power Applications Limit Adoption

While fast-charging capabilities continue advancing, thermal management remains a critical constraint. High current charging generates significant heat that can degrade battery performance and safety if not properly managed. Charge ICs must incorporate increasingly complex thermal regulation circuits, which adds to both component costs and design complexity. This challenge is particularly acute in ultra-thin smartphone designs where heat dissipation options are limited. Manufacturers must balance charging speed with thermal constraints, often leading to compromises in peak performance to ensure device safety and longevity.

Other Restraints

Supply Chain Vulnerabilities

The semiconductor shortage experienced in recent years highlighted the vulnerability of charge IC supply chains. Many charge IC manufacturers rely on specialized fabrication processes that aren’t easily transferable between foundries, creating bottlenecks during periods of high demand. These constraints have forced some smartphone makers to redesign their power management systems or delay product launches.

Battery Chemistry Limitations

Current lithium-ion battery technologies are approaching their practical limits in terms of charge acceptance rates. Even with advanced charge ICs, the fundamental limitations of battery chemistry restrict how quickly energy can be safely stored. This misalignment between IC capabilities and battery constraints creates inefficiencies in the charging ecosystem.

MARKET CHALLENGES

Increasing Complexity of Charging Standards Creates Integration Hurdles

The smartphone charging landscape has become increasingly fragmented with multiple competing fast-charge standards. Charge IC manufacturers must support various protocols including USB Power Delivery, Qualcomm Quick Charge, MediaTek Pump Express, and proprietary solutions from major OEMs. This complexity drives up development costs and complicates the component selection process for device makers. The challenge is further compounded by regional differences in preferred standards and the need for backward compatibility with older devices.

Other Challenges

Miniaturization Pressures

As smartphones continue shrinking in thickness while increasing battery capacity, charge ICs must occupy less board space while handling more power. This requires innovative packaging technologies like wafer-level chip scale packaging (WLCSP) that add to manufacturing complexity and costs.

Regulatory Compliance

Evolving safety and efficiency regulations in key markets require constant updates to charge IC architectures. Meeting multiple regional requirements while maintaining competitive performance characteristics presents a significant design challenge for IC manufacturers.

MARKET OPPORTUNITIES

Emergence of GaN-Based Solutions Opens New Frontiers in Power Efficiency

Gallium Nitride (GaN) technology represents a significant opportunity for the charge IC market, offering superior efficiency and power density compared to traditional silicon-based solutions. GaN charge ICs can operate at higher frequencies with lower switching losses, enabling more compact power management systems. This technology is particularly valuable for space-constrained applications like foldable smartphones, where board real estate is at a premium. Early adoption in premium devices is paving the way for broader market penetration as production scales and costs decrease.

AI-Driven Smart Charging Creates Differentiation Potential

The integration of machine learning algorithms into charge ICs presents notable opportunities for market differentiation. Smart charging systems can analyze usage patterns to optimize charging cycles, extending battery lifespan by avoiding unnecessary full charges. Some implementations can even predict when a device will next be used and complete charging just beforehand, minimizing time spent at full charge. These intelligent features provide OEMs with valuable product differentiation points while delivering tangible benefits to end-users.

Additionally, the growing ecosystem of IoT devices and wearables presents complementary opportunities. Many of these devices use similar charging technologies but with different power requirements, creating a diversified market for charge IC solutions. Manufacturers that can offer scalable, adaptable charge IC architectures stand to benefit from this expanding application space.

PHONE BATTERY CHARGE IC MARKET TRENDS

Rapid Adoption of Fast-Charging Technologies Accelerates Market Demand

The global phone battery charge IC market is experiencing significant growth driven by the increasing demand for fast-charging solutions in smartphones. Consumers now expect charging speeds that minimize downtime, pushing manufacturers to develop charge ICs capable of handling higher power delivery—up to 100W or more in some flagship devices. These advanced ICs incorporate sophisticated thermal management systems to dissipate heat efficiently while ensuring battery longevity. The transition from 5V/2A charging to protocols like USB Power Delivery (PD) and Qualcomm Quick Charge 5.0 demonstrates this shift, with charge ICs now supporting multiple voltage and current profiles dynamically. Furthermore, the rise of GaN-based charge ICs enables higher efficiency conversions at smaller footprints, addressing both performance and space constraints in modern smartphone designs.

Other Trends

Wireless Charging Integration

Wireless charging technology has evolved beyond the traditional 5W Qi standard, with newer implementations supporting 15W to 50W power levels. Charge ICs now integrate resonant and inductive charging topologies, along with foreign object detection (FOD) to enhance safety. The growing adoption of reverse wireless charging—where smartphones power accessories like earbuds—further diversifies the application scope. This trend is particularly prominent in premium smartphones, where charge ICs must manage bidirectional power flow efficiently while maintaining compliance with evolving wireless charging standards.

AI-Powered Battery Management Systems

Artificial Intelligence is increasingly being embedded in charge ICs to optimize charging cycles based on usage patterns and battery health. Machine learning algorithms analyze historical data to adjust charging speeds, reducing stress on battery cells during overnight charging or high-temperature conditions. Some implementations can predict battery lifespan degradation and suggest calibration cycles, effectively delaying the need for replacements. This intelligence layer, combined with real-time voltage/temperature monitoring, positions modern charge ICs as proactive guardians of battery health rather than passive regulators.

Sustainability and Power Efficiency Pressures

Regulatory pressures and consumer demand for eco-friendly devices are driving innovations in charge IC power efficiency. New designs target <1mW standby power consumption—a 60% reduction compared to previous generations—through advanced power gating techniques. There’s also growing emphasis on supporting renewable energy inputs, with some charge ICs now incorporating MPPT (Maximum Power Point Tracking) algorithms for optimal solar charging. These developments align with broader industry goals to reduce electronic waste through extended battery lifespans and energy-conscious designs.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Expand Through Innovation and Strategic Partnerships

The global Phone Battery Charge IC market exhibits a dynamic competitive landscape dominated by semiconductor giants and specialized power management IC manufacturers. With the market projected to grow at 7.5% CAGR through 2032, companies are aggressively investing in next-generation charging technologies to capture greater market share. The competitive environment remains moderately concentrated, with the top five players accounting for approximately 42% of 2024’s market revenue.

Qualcomm Technologies maintains significant market leadership, particularly through its Quick Charge technology portfolio adopted by major smartphone OEMs. Their advanced charge ICs support power delivery up to 100W, giving them competitive advantage in the fast-charging segment. Meanwhile, Texas Instruments has strengthened its position through robust R&D investments, with their portfolio including highly efficient buck-boost charger ICs supporting multiple battery chemistries.

Asian manufacturers are rapidly gaining ground, with MediaTek Inc. and Samsung Electro-Mechanics expanding their market presence through cost-effective solutions tailored for mid-range smartphones. These companies benefit from strong relationships with regional smartphone manufacturers and faster adoption cycles for new charging standards.

The competitive intensity is further amplified by smaller specialized players like Richtek Technology and Monolithic Power Systems, who compete through technological differentiation in areas like high-efficiency GaN-based charge ICs and advanced thermal management solutions.

List of Key Phone Battery Charge IC Companies Profiled

- Qualcomm Technologies, Inc. (U.S.)

- Texas Instruments Incorporated (U.S.)

- MediaTek Inc. (Taiwan)

- NXP Semiconductors N.V. (Netherlands)

- Samsung Electro-Mechanics Co., Ltd. (South Korea)

- Richtek Technology Corporation (Taiwan)

- Monolithic Power Systems Inc. (U.S.)

- STMicroelectronics N.V. (Switzerland)

- ON Semiconductor Corporation (U.S.)

Segment Analysis:

By Type

Switching Battery Chargers Lead the Market Due to High Efficiency and Fast-Charging Capabilities

The market is segmented based on type into:

- Linear Battery Chargers

- Switching Battery Chargers

- Others

By Application

Smartphones Dominate the Market Owing to Increasing Demand for Fast and Efficient Charging Solutions

The market is segmented based on application into:

- Smartphones

- Tablets

- Wearable Devices

- Others

By Charging Technology

Fast Charging Segment Drives Growth Due to Rising Consumer Demand for Quick Battery Replenishment

The market is segmented based on charging technology into:

- Standard Charging

- Fast Charging

- Wireless Charging

- Others

By Protection Feature

Overvoltage Protection Gains Prominence with Increasing Focus on Battery Safety

The market is segmented based on protection feature into:

- Overvoltage Protection

- Overcurrent Protection

- Thermal Protection

- Others

Regional Analysis: Phone Battery Charge IC Market

Asia-Pacific

Asia-Pacific dominates the global Phone Battery Charge IC market, accounting for over 60% of the total revenue share. China, as the world’s largest smartphone manufacturer, drives this growth through both domestic consumption and exports. Major OEMs like Huawei, Xiaomi, and Oppo fuel demand for high-efficiency charging solutions, particularly fast-charging ICs capable of handling power outputs up to 120W. The region benefits from robust semiconductor fabrication capabilities and a vertically integrated supply chain. While affordability remains a key consideration, there’s increasing adoption of GaN-based charging solutions in premium segments. Government initiatives promoting indigenous semiconductor manufacturing, such as India’s PLI scheme, are expected to further strengthen regional production capabilities.

North America

North America maintains a technology leadership position in advanced charging IC development, with key players like Texas Instruments and Qualcomm driving innovation. The market emphasizes premium features such as AI-powered charging optimization and support for multiple fast charging protocols (USB PD, Quick Charge 4+). There’s growing demand for wireless charging ICs compatible with both Qi and proprietary standards. Strict FCC regulations on power efficiency and electromagnetic interference compliance influence product designs. The region also sees increasing integration of charging ICs with renewable energy systems for eco-conscious consumers, particularly in California where energy efficiency standards are most stringent.

Europe

European demand centers on sophisticated charging solutions that balance performance with energy efficiency. The EU’s Ecodesign Directive and energy labeling requirements push manufacturers toward low-power standby modes and higher conversion efficiency. Germany leads in industrial applications where ruggedized charging ICs are needed for enterprise devices. Nordic countries show particular interest in wireless charging infrastructure development. The market is characterized by strong preference for standardized solutions (USB-IF certified) over proprietary technologies. Recent focus on right-to-repair legislation may impact IC design towards more modular and serviceable architectures.

South America

The South American market remains price-sensitive but shows gradual adoption of fast charging technologies, particularly in Brazil and Mexico. Economic challenges have slowed premium segment growth, leading to demand for cost-optimized linear charger ICs in entry-level smartphones. There’s notable grey market activity in charging components, complicating quality control. Recent investments in local assembly plants by Chinese manufacturers may stimulate the regional supply chain. Infrastructure limitations, including unstable power grids in some areas, necessitate charging ICs with robust voltage regulation capabilities.

Middle East & Africa

This emerging market shows divergent trends – Gulf Cooperation Council countries demand high-end charging solutions compatible with flagship devices, while Sub-Saharan Africa prioritizes durability and compatibility with varied power conditions. The lack of standardized power infrastructure drives need for charging ICs with wide input voltage ranges (3V-15V). Solar charging compatibility is gaining importance in off-grid areas. Local assembly initiatives in Egypt and South Africa indicate growing regional manufacturing potential, though currently most components are imported from Asia.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Phone Battery Charge IC markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Phone Battery Charge IC Market?

-> Phone Battery Charge IC Market was valued at 472 million in 2024 and is projected to reach US$ 748 million by 2032, at a CAGR of 7.5% during the forecast period.

Which key companies operate in Global Phone Battery Charge IC Market?

-> Key players include Texas Instruments, Qualcomm, ON Semiconductor, NXP Semiconductors, STMicroelectronics, and Renesas Electronics, among others.

What are the key growth drivers?

-> Key growth drivers include rising smartphone adoption, demand for fast-charging solutions, and advancements in battery technologies.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by high smartphone production and consumption, while North America leads in technological innovation.

What are the emerging trends?

-> Emerging trends include GaN-based charge ICs, AI-driven power management, and ultra-fast wireless charging technologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...