Market Insights

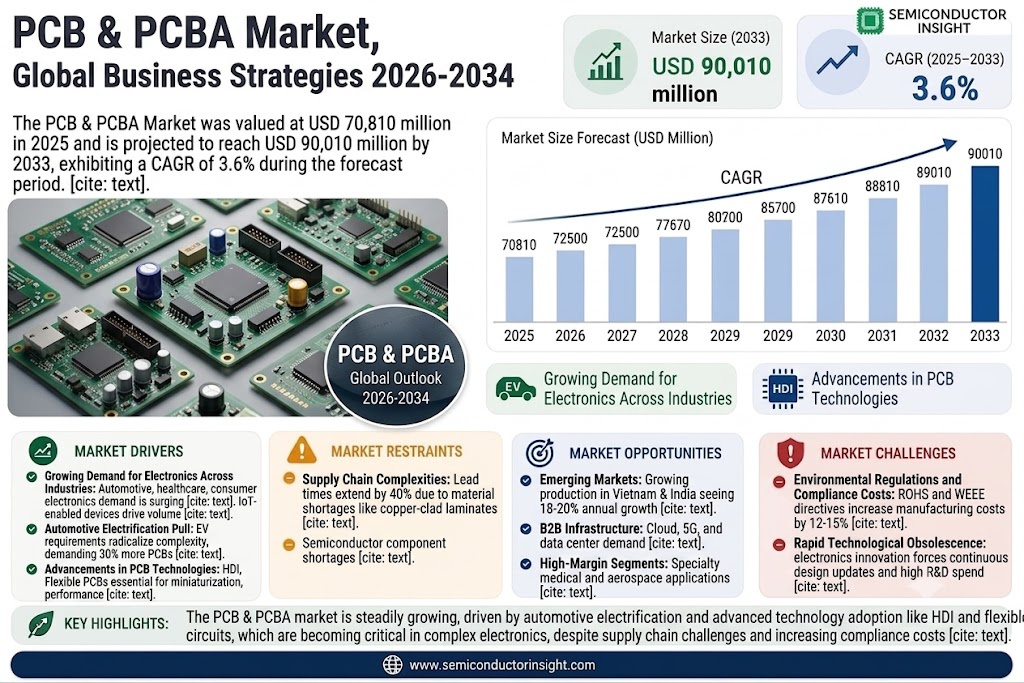

Global PCB & PCBA Market was valued at USD 70,810 million in 2025 and is projected to reach USD 90,010 million by 2033, exhibiting a CAGR of 3.6% during the forecast period.

A printed circuit board (PCB) mechanically supports and electrically connects electronic components using conductive tracks, pads, and other features etched from copper sheets laminated onto a non-conductive substrate. Components such as capacitors, resistors, or active devices are generally soldered onto the PCB. PCBA refers to Printed Circuit Board Assembly, where the bare board is populated with electronic components to form a functional printed circuit assembly (PCA), commonly called a printed circuit board assembly (PCBA).

The market growth is driven by increasing demand for consumer electronics, automotive electronics, and advancements in communication technologies. China dominates the market with a share of approximately 50%, followed by Taiwan and South Korea, which collectively hold around 25%. Standard Multilayer PCBs account for the largest product segment at 35%, while communications represent the leading application segment.

MARKET DRIVERS

Growing Demand for Electronics Across Industries

PCB & PCBA Market is experiencing significant growth due to increasing demand across automotive, healthcare, and consumer electronics sectors. The rise of smart devices and IoT-enabled products has created unprecedented demand for high-quality printed circuit boards. Global PCB production has grown by 8.3% annually since 2020.

Advancements in PCB Technologies

Innovations in high-density interconnect (HDI) and flexible PCB technologies are driving market expansion. The shift toward miniaturization and higher performance in electronics has made advanced PCB solutions essential. Global HDI PCB market is projected to reach USD 15.7 billion by 2026.

Automotive electrification represents another key driver, with EV manufacturers requiring 30% more PCBs per vehicle compared to traditional automobiles.

MARKET CHALLENGES

Supply Chain Complexities

PCB & PCBA Market faces significant challenges from global supply chain disruptions. Raw material shortages, particularly for copper-clad laminates and semiconductor components, have caused lead times to extend by 40% since 2021.

Other Challenges

Rapid Technological Obsolescence

The fast pace of innovation in electronics requires continuous PCB design updates, creating production inefficiencies and increasing R&D costs for manufacturers.

MARKET RESTRAINTS

Environmental Regulations and Compliance Costs

Stringent environmental regulations regarding hazardous materials in PCB production have increased manufacturing costs by 12-15%. Compliance with RoHS and WEEE directives requires significant investment in alternative materials and processes.

MARKET OPPORTUNITIES

Expansion in Emerging Markets

Growing electronics manufacturing in Southeast Asia presents lucrative opportunities for PCB & PCBA providers. Countries like Vietnam and India are experiencing 18-20% annual growth in PCB consumption as production shifts from China.

Automotive Electronics Boom

The automotive PCB market is projected to grow at 9.4% CAGR through 2030, driven by increasing ADAS implementations and vehicle electrification. Premium vehicles now contain over 100 PCBs compared to just 30 a decade ago.

PCB & PCBA Market Trends

Steady Growth in PCB & PCBA Market Projected Through 2033

Global PCB & PCBA Market is experiencing consistent expansion, with current valuations at USD 70.8 billion in 2025 and projected to reach USD 90 billion by 2033. This represents a compound annual growth rate of 3.6%, driven by increasing demand across communication, automotive, and consumer electronics sectors. China dominates the landscape with 50% market share, while Taiwan and South Korea collectively account for 25%.

Other Trends

Standard Multilayer PCBs Lead Product Segments

Standard multilayer PCBs currently hold 35% of the market share due to their widespread use in complex electronic devices. The segment is expected to maintain dominance as manufacturers seek balance between performance and cost-effectiveness for mid-range applications.

Regional Market Dynamics

Asia-Pacific continues as the production epicenter, accounting for over 75% of global PCB & PCBA output. North America and Europe are focusing on high-value specialized applications like aerospace and medical electronics, creating opportunities for premium PCB solutions.

Emerging Applications Drive Innovation

Automotive electrification and 5G infrastructure development are creating new demand vectors for advanced PCB technologies. The industry is responding with innovations in HDI and flexible circuit designs to meet these specialized requirements.

Competitive Landscape Consolidation

The top five manufacturers control more than 10% of the global PCB & PCBA Market, with companies like Nippon Mektron and Unimicron leading through technological differentiation and scaled production capabilities. Strategic acquisitions are expected to intensify as players seek to expand geographic and technical portfolios.

COMPETITIVE LANDSCAPE

Key Industry Players

Asia-Pacific Dominates with Over 75% Market Share in PCB & PCBA Production

Global PCB & PCBA Market is highly concentrated with the top 5 manufacturers holding over 10% market share collectively. Nippon Mektron leads the industry with strong capabilities in HDI and flexible PCBs, followed closely by Taiwan’s Unimicron which specializes in high-layer count PCBs for advanced applications. These players maintain dominance through continuous R&D investments in advanced packaging technologies and strategic partnerships with global electronics OEMs.

Regional players like China’s ZDT and Tripod are gaining market share through cost-competitive manufacturing and expanding automotive electronics portfolios. South Korean firms SEMCO and Daeduck Group excel in high-density interconnect (HDI) boards for smartphones, while European specialist AT&S maintains leadership in IC substrates for semiconductor packaging. The market sees increasing competition from emerging players like TopCB and Kinwong, who are rapidly scaling up production capacities.

List of Key PCB & PCBA Companies Profiled

- Nippon Mektron

- Unimicron

- SEMCO

- Young Poong Group

- Ibiden

- ZDT

- Tripod

- TTM Technologies

- Shinko Electric Ind

- Daeduck Group

- HannStar Board (GBM)

- AT&S

- Kingboard

- Compeq

- MEIKO ELECTRONICS

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Standard Multilayer dominates due to its widespread adoption across industries

|

| By Application |

|

Communications leads demand driven by 5G infrastructure and IoT devices

|

| By End User |

|

EMS Providers demonstrate strongest growth as outsourcing trends accelerate

|

| By Complexity Level |

|

Medium Complexity boards generate highest revenue across industries

|

| By Production Process |

|

Etching Process remains fundamental to PCB manufacturing

|

Regional Analysis: PCB & PCBA Market

Asia-Pacific

China maintains PCB & PCBA dominance through vertically integrated electronics clusters in Shenzhen and Kunshan, supported by comprehensive component supply networks and advanced SMT capabilities that enable rapid prototyping and mass production.

Japanese PCB manufacturers lead in high-reliability boards for automotive and industrial applications, with specialty materials and precision manufacturing techniques that command premium pricing in the PCB & PCBA Market.

Malaysia, Vietnam, and Thailand are attracting PCB & PCBA investments with competitive labor costs and free trade agreements, developing into important secondary hubs for consumer electronics assembly and testing operations.

India’s PCB & PCBA sector is growing through smartphone manufacturing initiatives and defense electronics localization policies, though still faces challenges in developing comprehensive domestic supply chains for advanced substrates and components.

North America

The North American PCB & PCBA Market focuses on high-value, low-volume production for aerospace, defense, and medical applications. U.S. manufacturers lead in advanced packaging technologies and quick-turn prototyping services, supported by strong R&D ecosystems in Silicon Valley and Boston’s Route 128 corridor. Recent reshoring initiatives and CHIPS Act funding are strengthening domestic PCB capabilities, particularly for military-grade and high-frequency RF applications. The region maintains leadership in PCB design software and testing equipment, influencing global PCB & PCBA standards and manufacturing practices.

Europe

Europe’s PCB & PCBA Market emphasizes automotive and industrial applications, with Germany at the forefront of automotive electronics manufacturing. The region maintains strict quality standards and specializes in high-reliability multilayer boards for automotive systems and industrial automation. Eastern European countries are developing as cost-effective alternatives for PCBA services, while Western European firms invest in sustainable manufacturing practices and lead-free soldering technologies to meet stringent environmental regulations.

South America

The South American PCB & PCBA Market remains relatively small but shows growth potential in Brazil and Mexico, supported by expanding consumer electronics markets and proximity to North American supply chains. Local manufacturers primarily serve domestic demand, with limited capabilities in high-volume production. Regional trade agreements are helping develop more integrated electronics manufacturing ecosystems, though infrastructure challenges continue to constrain large-scale PCB fabrication investments.

Middle East & Africa

The Middle East & Africa region is developing PCB & PCBA capabilities through technology transfer initiatives and economic diversification programs. Israel leads in specialized military and telecommunications applications, while Gulf Cooperation Council countries are investing in electronics manufacturing zones. African nations show emerging potential for PCB assembly operations, particularly in North Africa, though the regional market remains highly dependent on imports for advanced PCB substrates and components.

Report Scope

This market research report provides a comprehensive analysis of the PCB & PCBA Market , covering the forecast period 2025–2033. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of PCB & PCBA Market?

-> PCB & PCBA Market was valued at USD 70,810 million in 2025 and is projected to reach USD 90,010 million by 2033, exhibiting a CAGR of 3.6% during the forecast period.

Which key companies operate in PCB & PCBA Market?

-> Key players include Nippon Mektron, Unimicron, SEMCO, Young Poong Group, Ibiden, ZDT, Tripod, TTM, SEI, Daeduck Group, among others. Global top five manufacturers hold a share over 10%.

What are the key growth drivers?

-> Key growth drivers include increasing demand from communications and consumer electronics sectors, technological advancements in PCB manufacturing, and rising automotive electronics applications.

Which region dominates the market?

-> China is the largest market with about 50% share, followed by China Taiwan and South Korea with about 25% combined share.

What are the emerging trends?

-> Emerging trends include growth in HDI and flexible PCBs, increasing adoption of IC substrates, and rising demand for PCBAs in IoT devices.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...