Passivity-based control for DC microgrid converters with CPL Market Insights

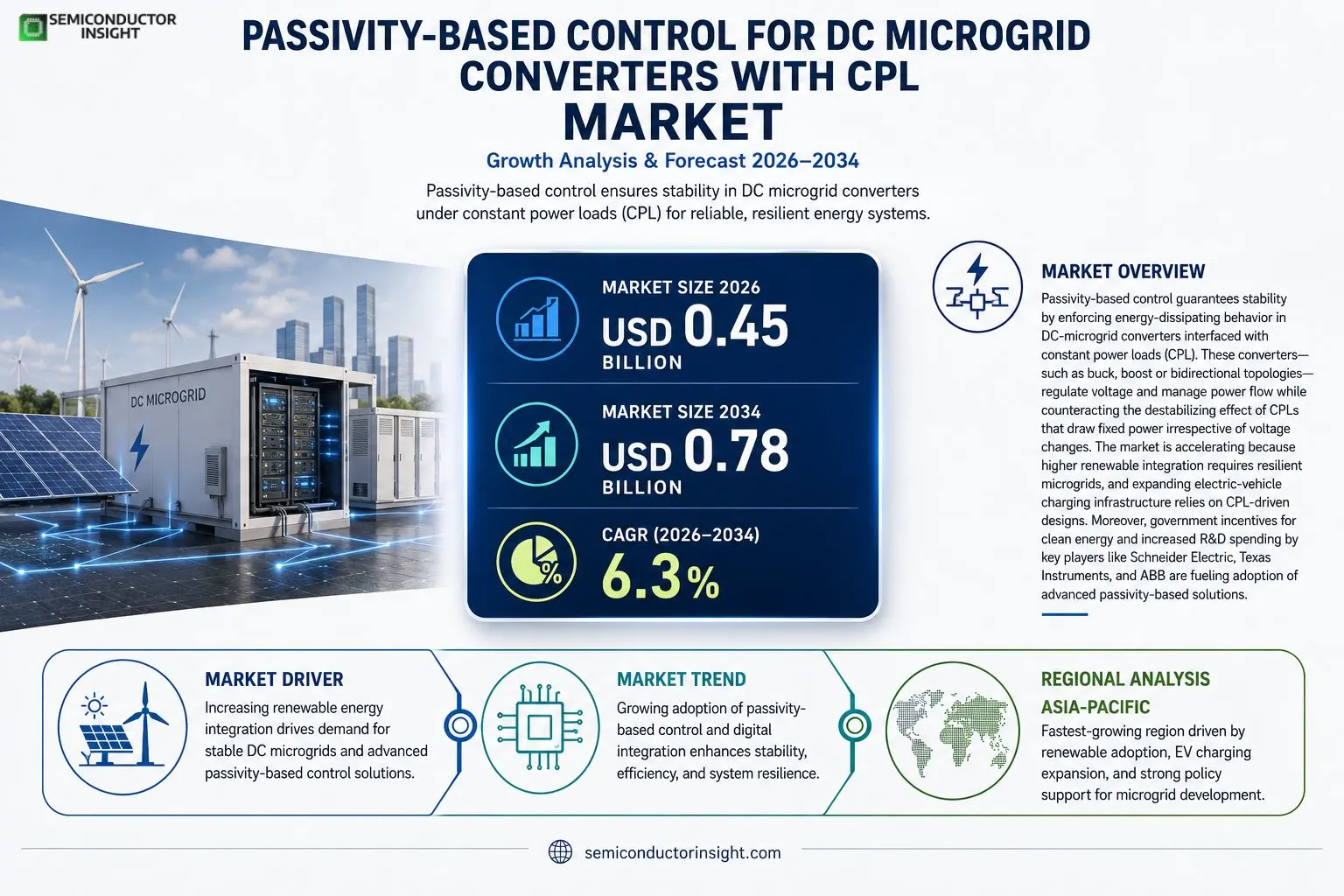

Passivity-based control for DC microgrid converters with CPL market size was valued at USD 0.45 billion in 2025. The market is projected to grow from USD 0.45 billion in 2025 to USD 0.78 billion by 2034, exhibiting a CAGR of 6.3% during the forecast period.

Passivity‑based control is a robust methodology that guarantees stability by enforcing energy‑dissipating behavior in DC‑microgrid converters interfaced with constant power loads (CPL). These converterssuch as buck, boost or bidirectional topologiesregulate voltage and manage power flow while counteracting the destabilizing effect of CPLs that draw fixed power irrespective of voltage changes.The market is accelerating because higher renewable integration requires resilient microgrids, and expanding electric‑vehicle charging infrastructure relies on CPL‑driven designs. Moreover, government incentives for clean energy and increased R&D spending by key players like Schneider Electric, Texas Instruments, and ABB are fueling adoption of advanced passivity‑based solutions.

MARKET DRIVERS

Increasing Renewable Energy Integration

The surge in solar and wind installations drives demand for stable DC microgrids, prompting designers to adopt passivity‑based control strategies that enhance voltage regulation under variable generation. Robust performance in the face of fluctuating input makes these controllers attractive for modern power networks.

Regulatory Incentives and Standards

Governments worldwide are introducing guidelines that favor high‑efficiency, low‑loss converters. Compliance with emerging standards encourages manufacturers to integrate advanced control algorithms, accelerating market adoption. Policy support reduces perceived risk for early adopters.

➤ “Passivity‑based methods deliver up to 15% improvement in transient stability compared with conventional PI controllers.”

Together, these factors create a favorable environment for Passivity-based control for DC microgrid converters with CPL Market, positioning it as a cornerstone technology for future resilient energy systems.

MARKET CHALLENGES

Technical Complexity and Design Expertise

Implementing passivity‑based algorithms requires deep knowledge of nonlinear dynamics and careful tuning of controller parameters. Many firms lack in‑house expertise, leading to longer development cycles and higher engineering costs.

Other Challenges

Compatibility with Legacy Infrastructure

Older converter platforms often rely on linear control loops, making retrofitting with passivity‑based schemes costly and time‑consuming. Integration hurdles can deter investment despite demonstrated performance gains.

MARKET RESTRAINTS

High Up‑Front Investment

Initial capital outlays for hardware that supports advanced control, combined with the need for specialized software tools, create a financial barrier for small and midsize enterprises. This cost premium limits rapid market penetration in price‑sensitive regions.

MARKET OPPORTUNITIES

Emerging Smart‑Grid Applications

As utilities transition toward decentralized architectures, there is growing interest in microgrids that can autonomously balance load and generation. Passivity‑based control offers a scalable solution that can be embedded in next‑generation DC converters, opening avenues for new product lines and service contracts. Strategic partnerships between converter manufacturers and software developers are expected to accelerate commercialization over the next five years.

Passivity-based control for DC microgrid converters with CPL Market Trends

Accelerating Adoption of Passivity‑Based Control in Renewable‑Rich Microgrids

The adoption of passivity‑based control strategies is gaining momentum as utilities and industrial operators seek reliable voltage regulation in DC microgrids that host constant power loads. By enforcing energy‑dissipating behavior, this control approach stabilizes converters such as buck, boost, and bidirectional topologies even when CPLs draw fixed power independent of voltage fluctuations. The trend is reinforced by the expanding deployment of renewable generationsolar photovoltaic panels and wind turbineswhose intermittent nature requires resilient microgrid architectures. Simultaneously, the growth of electric‑vehicle charging stations, many of which incorporate CPL‑driven power electronics, creates a direct demand for control solutions that can mitigate the destabilizing effects of high‑power‑density loads. Government incentive programs that target clean‑energy integration and the increased research investment from leading firms like Schneider Electric, Texas Instruments, and ABB further accelerate market momentum.

Other Trends

Technology Adoption and Standardization

Passivity‑based control is moving from laboratory prototypes to commercial products through the standardization of control algorithms and the integration of embedded sensor networks. Vendors are embedding passivity‑aware firmware into next‑generation DC‑DC converters, enabling automatic tuning of control parameters based on real‑time load conditions. This shift reduces engineering lead time and improves system uptime, a critical factor for applications ranging from offshore wind substations to campus‑scale microgrids. Open‑source initiatives and industry consortiums are also contributing reference models that streamline certification processes and promote interoperability across different converter manufacturers.

Competitive Landscape and Product Innovation

Competitive dynamics are shaped by a handful of players that have deep expertise in power electronics and control theory. Schneider Electric has launched a modular converter series that incorporates built‑in passivity‑based algorithms, targeting renewable integration projects in Europe and North America. Texas Instruments offers integrated driver chips with programmable passivity controls, facilitating rapid deployment in EV charging racks. ABB’s recent product roadmap emphasizes bidirectional converters capable of grid‑forming functions while maintaining stability under CPL stress. Partnerships between semiconductor firms and system integrators are yielding bundled solutions that combine hardware, software, and analytics, delivering end‑to‑end value for customers seeking to future‑proof their DC infrastructure.

COMPETITIVE LANDSCAPEKey Industry Players

Passivity‑Based Control in DC Microgrids with CPL: Competitive Overview

The market is currently dominated by a few large technology firms that have integrated passivity‑based control algorithms into their power‑electronic converter portfolios. Schneider Electric leverages its extensive grid‑automation suite and recent R&D spend to offer turnkey DC‑microgrid solutions that embed stability‑ensuring controllers for constant‑power loads. Texas Instruments supplies highly integrated mixed‑signal ICs that enable fast, low‑latency implementation of passivity‑based schemes across buck, boost and bidirectional converters, positioning it as a preferred supplier for EV‑charging infrastructure. ABB’s reach and deep expertise in industrial power systems allow it to deliver robust converter platforms with built‑in passive‑control modules, reinforcing its leadership in the expanding renewable‑integration segment. Collectively, these leaders shape market structure through extensive OEM partnerships, large‑scale deployments, and continuous firmware upgrades that keep pace with the forecasted CAGR of 6.3 %.Beyond the top tier, a diverse set of niche innovators contributes specialized technologies and regional market coverage. Siemens and Eaton focus on modular converter architectures that incorporate passivity‑based techniques for grid‑forming applications. Delta Electronics, Mitsubishi Electric and Hitachi provide high‑efficiency converter families targeting data‑center and telecom back‑up power, while NXP Semiconductors and Analog Devices deliver precision analog front‑ends that support energy‑dissipating control loops. Infineon Technologies, TDK, and National Instruments supply semiconductor and instrumentation solutions that enable advanced stability analysis and rapid prototyping. Emerging players such as Huawei, Altair Engineering and General Electric are advancing digital twin and AI‑enhanced control strategies that complement traditional passive designs, widening the competitive landscape.

List of Key Passivity‑Based Control for DC Microgrid Converters with CPL Companies Profiled

- Schneider Electric

- Texas Instruments

- ABB

- Siemens

- Eaton

- Delta Electronics

- Mitsubishi Electric

- Hitachi

- NXP Semiconductors

- Analog Devices

- Infineon Technologies

- TDK

- National Instruments

- Huawei

- Altair Engineering

- General Electric

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Voltage‑mode control

|

| By Application |

|

Renewable energy integration

|

| By End User |

|

Utility operators

|

| By Topology |

|

Bidirectional converters

|

| By Market Driver |

|

R&D investments by key manufacturers

|

Regional Analysis: North America

North America

The United States is a key driver of the passivity-based control market in North America. Government policies promoting renewable energy and grid modernization are creating a favorable environment for adoption. Private sector investments in microgrid infrastructure, particularly in remote areas and critical facilities, are further boosting demand. Innovations in CPL technology are also contributing to improved performance and cost-effectiveness.

Canada’s commitment to clean energy and its extensive hydroelectric resources are driving the growth of DC microgrids. The country’s supportive regulatory framework and focus on energy efficiency are creating opportunities for passivity-based control solutions. Significant investments in infrastructure projects are further contributing to market expansion.

Mexico’s growing energy demands and increasing adoption of renewable energy technologies are fueling the need for advanced grid management solutions. The expansion of microgrid deployments in industrial and commercial sectors presents a significant opportunity for passivity-based control in DC microgrid converters with CPL technology.

Following the natural disasters, Puerto Rico has been actively rebuilding its energy infrastructure with a strong emphasis on resilience and distributed generation. Passivity-based control for DC microgrids is crucial for enhancing grid stability and reliability in this context, making it a significant regional focus.

Europe

Europe is demonstrating robust growth in the passivity-based control market, propelled by stringent environmental regulations and a strong push towards decarbonization. The region’s focus on energy efficiency and the integration of renewable energy sources are key drivers. Several countries are actively promoting the deployment of microgrids for enhanced energy security and grid resilience.

Asia-Pacific

The Asia-Pacific region presents a dynamic and rapidly expanding market for passivity-based control. Rapid urbanization, increasing industrialization, and a growing focus on renewable energy are creating significant demand for advanced grid management solutions in countries like China, Japan, and Australia.

South America

South America is witnessing increasing interest in passivity-based control, particularly in countries with abundant renewable energy resources like Brazil and Chile. The need for reliable power supply in remote areas and the development of microgrids for industrial applications are driving market growth.

Middle East & Africa

The Middle East & Africa region is expected to experience steady growth in the passivity-based control market, driven by increasing investments in renewable energy projects and the development of microgrids in remote areas. The region’s focus on energy independence and grid diversification is creating new opportunities for this technology.

Report Scope

This market research report provides a comprehensive analysis of the Passivity-based control for DC microgrid converters with CPL Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Passivity-based control for DC microgrid converters with CPL Market?

-> Passivity-based control for DC microgrid converters with CPL Market was valued at USD 0.45 billion in 2025 and is expected to reach USD 0.78 billion by 2034.

Which key companies operate in Passivity-based control for DC microgrid converters with CPL Market?

-> Key players include Schneider Electric, Texas Instruments, ABB, among others.

What are the key growth drivers?

-> Key growth drivers include higher renewable integration, expanding electric‑vehicle charging infrastructure, and government incentives for clean energy.

Which region dominates the market?

-> Asia-Pacific is the fastest‑growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include advanced passivity‑based control algorithms, AI‑enhanced stability monitoring, and integration with smart grid technologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...