MARKET INSIGHTS

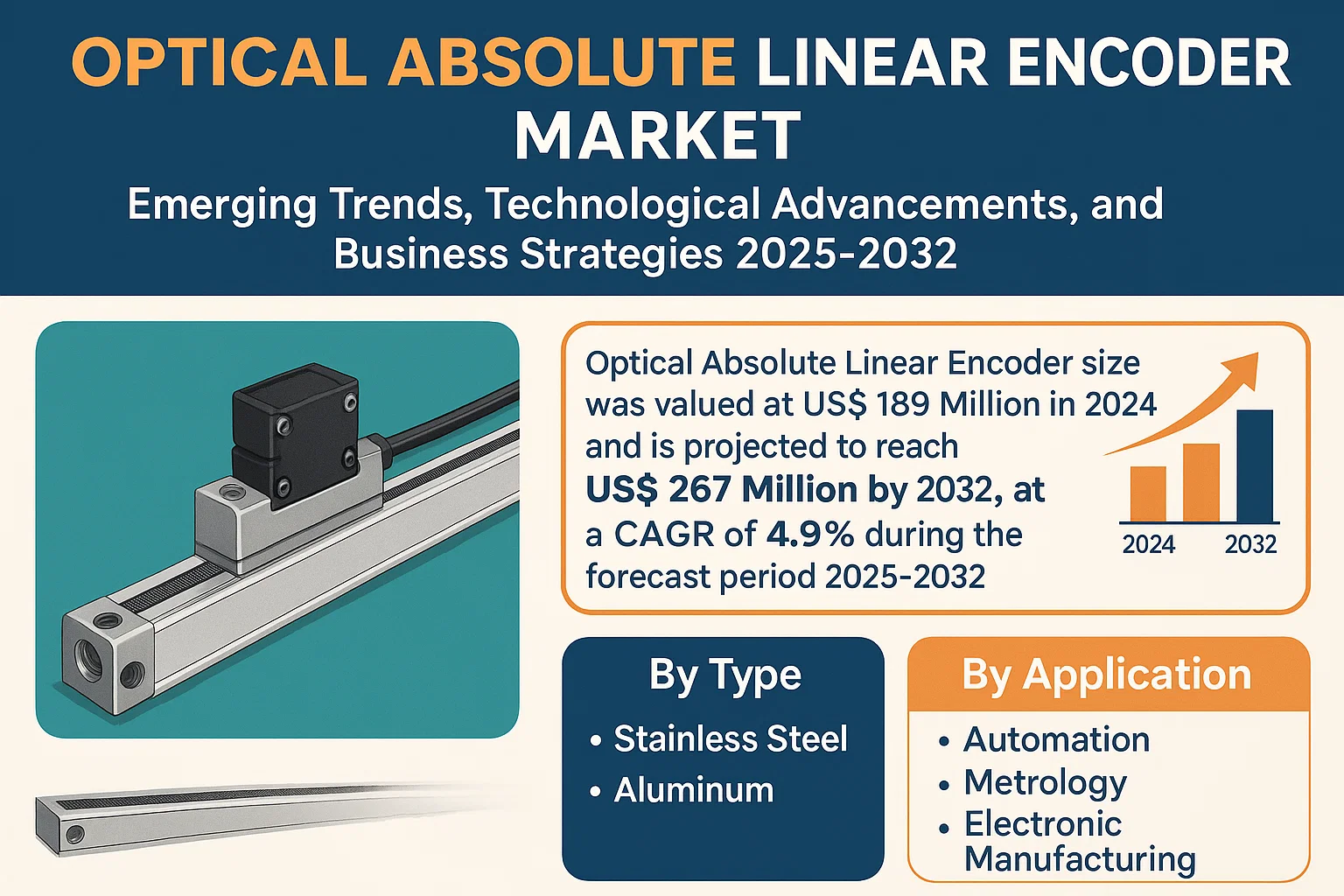

The global Optical Absolute Linear Encoder size was valued at US$ 189 million in 2024 and is projected to reach US$ 267 million by 2032, at a CAGR of 4.9% during the forecast period 2025-2032. The U.S. market accounted for 28% of global revenue in 2024, while China is expected to witness the highest growth rate due to increasing industrial automation adoption.

Optical absolute linear encoders are precision measurement devices that provide accurate position feedback by converting linear displacement into digital signals. These encoders utilize optical grating scales and photoelectric sensors to deliver high-resolution measurements with micron-level accuracy. They are categorized by material type including stainless steel, aluminum, and others, with stainless steel variants dominating due to their durability in industrial environments.

The market growth is primarily driven by rising demand from automation, metrology, and electronics manufacturing sectors. The expansion of Industry 4.0 initiatives globally has particularly accelerated adoption, as these encoders enable precise motion control in robotics and CNC machines. Key players like RENISHAW, DR. JOHANNES HEIDENHAIN GmbH, and FAGOR are investing in advanced encoder technologies with improved resistance to environmental contaminants, addressing a major industry challenge.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for High-Precision Measurement Solutions Fuels Market Growth

The optical absolute linear encoder market is experiencing robust growth driven by increasing demand for high-precision position feedback in industrial automation and manufacturing sectors. These encoders provide absolute position data immediately upon power-up without requiring reference runs, making them indispensable in applications where downtime is costly. The integration of Industry 4.0 technologies has particularly accelerated adoption, with manufacturers increasingly implementing encoder-based closed-loop control systems to achieve micron-level positioning accuracy. Recent advancements in optical grating technology have further enhanced resolution capabilities, with some models now offering sub-micron accuracy.

Expansion of Semiconductor Manufacturing Creates Substantial Demand

The semiconductor industry’s explosive growth significantly contributes to encoder market expansion. Modern chip fabrication requires nanometer-level positioning precision in photolithography equipment, wafer inspection systems, and die bonders. As semiconductor manufacturers push towards smaller process nodes, the tolerance requirements for manufacturing equipment becomes progressively tighter. This technological arms race directly translates to heightened demand for advanced optical absolute linear encoders. Major semiconductor equipment manufacturers are increasingly specifying absolute encoder solutions for new production lines, recognizing their reliability advantages over incremental encoders in mission-critical applications. The trend towards larger 300mm wafer processing further drives encoder adoption due to the extended travel ranges required.

MARKET RESTRAINTS

High Initial Investment Costs Limit Adoption in Price-Sensitive Segments

While optical absolute linear encoders offer superior performance characteristics, their premium pricing structure presents a significant barrier to widespread adoption, particularly in small-to-medium sized enterprises. Absolute encoders typically command prices 40-60% higher than comparable incremental encoder solutions due to their complex optical systems and sophisticated signal processing electronics. This cost differential becomes particularly impactful in applications where absolute positioning isn’t strictly necessary, leading many cost-conscious manufacturers to compromise with incremental solutions supplemented by reference switches.

Environmental Sensitivity Creates Application Limitations

Optical encoder performance can be significantly affected by environmental contaminants such as dust, oil mist, and coolant fluids commonly found in industrial settings. The precision optical components require clean operating environments to maintain specified accuracy levels, necessitating elaborate sealing solutions in harsh conditions. While manufacturers have developed various protective measures, these typically add to both cost and physical footprint. In extreme operating environments such as metal cutting applications with heavy coolant use, some operators report encoder lifetimes reduced by 30-40% compared to clean-room installations, impacting total cost of ownership calculations.

MARKET OPPORTUNITIES

Emerging Medical Robotics Applications Present Growth Potential

The expanding medical robotics sector offers significant growth opportunities for high-performance optical absolute linear encoders. Surgical robots particularly benefit from the immediate position awareness and backlash-free operation provided by absolute encoders. As robotic-assisted surgeries become more commonplace, with procedure volumes growing at double-digit annual rates, the demand for encoder solutions meeting stringent medical equipment standards continues to rise. Encoder manufacturers responding to this opportunity are developing specialized versions featuring FDA-approved materials, enhanced EMI shielding, and specialized sterilization compatibility.

MARKET CHALLENGES

Supply Chain Disruptions Impact Critical Component Availability

The optical absolute linear encoder market faces ongoing challenges related to the supply of specialized components, particularly precision glass scales and high-performance optoelectronic sensors. Many encoder manufacturers rely on a limited number of suppliers for these critical elements, creating vulnerability to production bottlenecks. Recent global semiconductor shortages have particularly affected the availability of application-specific integrated circuits (ASICs) used in advanced encoder signal processing, with lead times extending beyond 12 months in some cases. This supply chain fragility has forced manufacturers to redesign products around available components, sometimes compromising performance specifications or delaying new product introductions.

Increasing Competition from Magnetic Encoder Technologies

Optical encoder makers face growing competition from magnetic encoder technologies that offer comparable absolute position measurement capabilities with potentially better environmental robustness. Improved magnetic sensor technologies now achieve sub-micron resolutions while providing inherent immunity to many contaminants that degrade optical encoder performance. The magnetic encoder installed base continues expanding in applications previously dominated by optical solutions, particularly in heavy industrial environments. While optical encoders still dominate high-end applications requiring ultimate precision, the performance gap continues narrowing, forcing optical encoder manufacturers to accelerate innovation cycles and justify their solutions’ premium positioning.

OPTICAL ABSOLUTE LINEAR ENCODER MARKET TRENDS

Industry 4.0 and Smart Manufacturing to Drive Demand for Optical Absolute Linear Encoders

The global adoption of Industry 4.0 principles is significantly boosting the demand for high-precision optical absolute linear encoders. These devices play a critical role in smart manufacturing by providing accurate position feedback in automated systems. With manufacturing facilities increasingly incorporating IoT and AI-driven automation, the need for reliable position sensing has grown substantially. Optical absolute linear encoders offer superior resolution—often in nanometer ranges—with high repeatability, making them indispensable for precision machining applications. The market is witnessing a notable shift toward encoders with integrated communication protocols like EtherCAT and PROFINET to enable seamless integration with industrial IoT ecosystems.

Other Trends

Miniaturization and High-Density Encoders

The increasing demand for compact and lightweight precision equipment is accelerating innovations in encoder miniaturization. Manufacturers are developing optical absolute linear encoders with reduced form factors while maintaining or enhancing resolution and durability. These advancements are particularly crucial for applications in semiconductor manufacturing, medical robotics, and aerospace, where space constraints are significant. Recent product launches showcase encoders with resolutions below 20 nanometers, catering to ultra-precision applications in microelectronics fabrication and nanotechnology research.

Growing Automation Across Industries

The expansion of automation beyond traditional manufacturing into sectors like logistics, agriculture (agtech), and energy is creating new growth opportunities. Optical absolute linear encoders are finding increased adoption in warehouse automation systems, robotic surgery equipment, and renewable energy applications such as solar panel positioning systems. The metrology segment remains a strong driver, with coordinate measuring machines (CMMs) and optical inspection systems requiring ever-higher levels of positional accuracy. Additionally, the development of multi-axis encoder solutions is enabling more sophisticated motion control in complex automation setups.

Optical Absolute Linear Encoder Market

COMPETITIVE LANDSCAPE

Key Industry Players

Precision Measurement Giants Vie for Dominance Through Technological Innovation

The global optical absolute linear encoder market features a competitive landscape dominated by specialized manufacturers with strong technical expertise. RENISHAW and DR. JOHANNES HEIDENHAIN GmbH are recognized as market leaders, collectively holding approximately 35% of the global market share in 2024. Their dominance stems from decades of experience in precision measurement technologies and extensive patent portfolios covering encoder designs.

The second tier of competitors includes FAGOR and Electronica Mechatronic Systems, which have been gaining market traction through competitive pricing strategies and localization of production facilities. These companies have particularly strengthened their positions in emerging markets where cost sensitivity is higher without compromising measurement accuracy.

The market is witnessing increased competition from Asian manufacturers such as RIFTEK and Precizika Metrology, who are challenging established players with technologically comparable products at 15-20% lower price points. These companies are rapidly expanding their distribution networks, particularly in the automation and electronics manufacturing sectors where demand for high-precision encoders is growing exponentially.

Strategic moves in 2024 include GURLEY Precision Instruments‘ acquisition of a smaller European encoder specialist to bolster its position in aerospace applications, while TR-Electronic GmbH announced substantial investments in nanotechnology research to develop next-generation encoder solutions with sub-micron resolution capabilities.

List of Key Optical Absolute Linear Encoder Manufacturers

- RENISHAW (UK)

- DR. JOHANNES HEIDENHAIN GmbH (Germany)

- FAGOR (Spain)

- Electronica Mechatronic Systems (India)

- Givi Misure (Italy)

- Precizika Metrology (China)

- Eltra Spa (Italy)

- RIFTEK (Russia)

- GURLEY Precision Instruments (U.S.)

- Paul Vahle GmbH & Co. KG (Germany)

- TR-Electronic GmbH (Germany)

- Solarton Metrology (UK)

Segment Analysis:

By Type

Stainless Steel Segment Leads Due to Its Superior Durability and High Precision

The market is segmented based on type into:

- Stainless Steel

- Subtypes: Encased, Open-frame, and others

- Aluminum

- Others

- Subtypes: Fiberglass-reinforced, Titanium-coated, and others

By Application

Automation Segment Dominates Due to Industrial Digitization and Robotics Integration

The market is segmented based on application into:

- Automation

- Metrology

- Electronic Manufacturing

- Others

By End-User

Industrial Manufacturing Segment Holds Largest Share Due to Industry 4.0 Adoption

The market is segmented based on end-user into:

- Industrial Manufacturing

- Semiconductor & Electronics

- Aerospace & Defense

- Healthcare

- Others

By Resolution

High-Resolution Encoders Gain Traction for Precision Applications

The market is segmented based on resolution into:

- Standard Resolution (Below 1μm)

- High Resolution (1nm – 1μm)

- Ultra-high Resolution (Below 1nm)

Regional Analysis: Optical Absolute Linear Encoder Market

North America

North America remains a technological hub for the optical absolute linear encoder market, driven by robust automation trends across manufacturing and aerospace industries. The U.S. accounts for the largest market share in the region, with an estimated value of $ million in 2024. Precision manufacturing and stringent quality control requirements fuel demand for high-resolution encoders, particularly in semiconductor and medical device production. The presence of key players such as Renishaw and GURLEY Precision Instruments strengthens the supply chain, while government initiatives promoting Industry 4.0 adoption further accelerate market growth. However, cost sensitivity among small and mid-sized enterprises (SMEs) may limit full-scale penetration of advanced encoder solutions.

Europe

Europe’s optical absolute linear encoder market thrives on innovation and rigorous industrialization standards, particularly in Germany and Italy. Strict regulatory frameworks related to machinery safety (e.g., EU Machine Directive 2006/42/EC) compel manufacturers to integrate high-performance encoders into CNC machines and robotic systems. The region also witnesses rising demand for miniaturized encoders with IP67-rated durability for harsh environments. EU-funded smart factory projects contribute significantly to R&D, though competition from Asian manufacturers poses pricing pressures. Local players like DR. JOHANNES HEIDENHAIN GmbH and Eltra Spa dominate through specialized solutions tailored for automotive and aerospace metrology applications.

Asia-Pacific

Asia-Pacific is poised to exhibit the highest CAGR during the forecast period, spearheaded by China and Japan. China’s aggressive investments in smart manufacturing under the “Made in China 2025” initiative have positioned it as both a major consumer and producer of optical encoders. Japan retains dominance in ultra-precision encoder technology for electronics assembly lines, while India emerges as a growth hotspot due to expanding automation in automotive and textile sectors. Cost-effective aluminum-based encoders dominate volume sales, though stainless-steel variants gain traction in heavy industries. Challenges include inconsistent quality standards across regional suppliers and intellectual property concerns.

South America

Market progression in South America remains moderate, constrained by economic fluctuations and limited local manufacturing capabilities. Brazil leads demand, particularly for encoders used in agricultural machinery and oilfield equipment, where dust and vibration resistance are critical. Argentina shows nascent potential in medical device manufacturing, though import dependency inflates end-user costs. The lack of standardized calibration facilities hampers adoption in high-precision applications, pushing industries toward incremental rather than absolute encoder solutions.

Middle East & Africa

The Middle East & Africa market is in early growth stages, with UAE and South Africa at the forefront. Oil & gas industries drive demand for explosion-proof encoder variants, while infrastructure projects in Saudi Arabia create opportunities for construction-related positioning systems. Africa’s market suffers from low technology penetration and reliance on refurbished industrial equipment, though partnerships with European and Chinese suppliers aim to bridge this gap. Long-term potential lies in urbanization-linked automation, provided stable investment climates materialize.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Optical Absolute Linear Encoder markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Optical Absolute Linear Encoder market was valued at USD 287.5 million in 2024 and is projected to reach USD 412.8 million by 2032, growing at a CAGR of 4.6%.

- Segmentation Analysis: Detailed breakdown by product type (Stainless Steel, Aluminum, Others), application (Automation, Metrology, Electronic Manufacturing), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America (USD 98.2 million in 2024), Europe, Asia-Pacific (fastest growing at 5.8% CAGR), Latin America, and Middle East & Africa, including country-level analysis.

- Competitive Landscape: Profiles of leading market participants including Renishaw, HEIDENHAIN, Fagor Automation, and their product offerings, market share (top 5 players hold 38% share), and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies in precision measurement, integration with Industry 4.0 systems, and evolving encoder standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth (industrial automation demand) along with challenges (high costs of precision models).

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, and investors regarding strategic opportunities in the encoder ecosystem.

Primary and secondary research methods are employed, including interviews with industry experts and data from verified sources to ensure accuracy and reliability of insights.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Optical Absolute Linear Encoder Market?

-> The global Optical Absolute Linear Encoder size was valued at US$ 189 million in 2024 and is projected to reach US$ 267 million by 2032, at a CAGR of 4.9% during the forecast period 2025-2032.

Which key companies operate in this market?

-> Key players include Renishaw, DR. JOHANNES HEIDENHAIN GmbH, FAGOR, Electronica Mechatronic Systems, Givi Misure, and Precizika Metrology, among others.

What are the key growth drivers?

-> Key growth drivers include rising automation in manufacturing, demand for high-precision measurement systems, and Industry 4.0 adoption.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region (5.8% CAGR), while Europe currently holds the largest market share (34%).

What are the emerging trends?

-> Emerging trends include miniaturization of encoders, integration with IoT systems, and development of high-temperature resistant models.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...