O-RAN service management and orchestration (SMO) non-RT RIC Market Insights

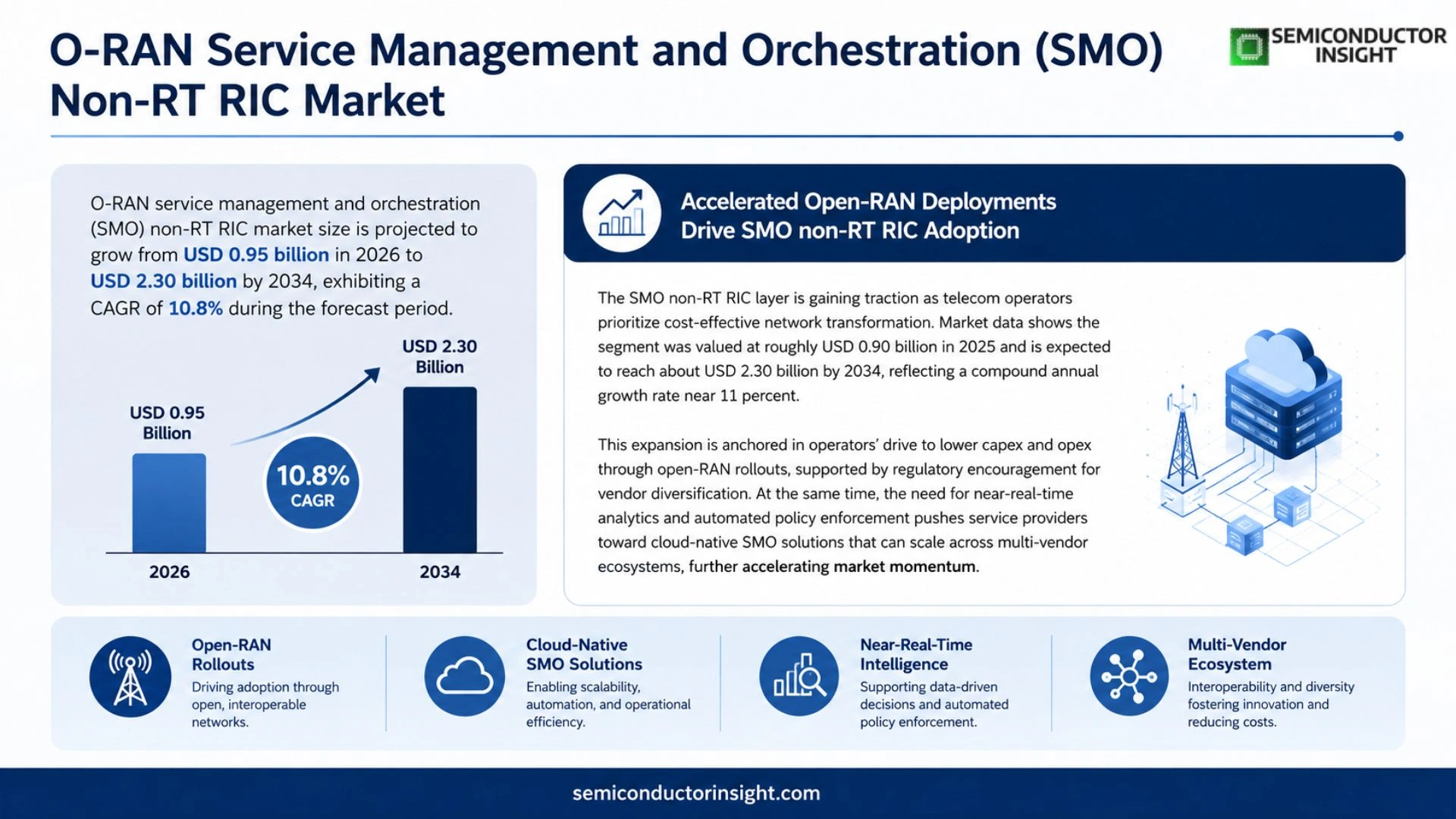

Global O-RAN service management and orchestration (SMO) non‑RT RIC market size was valued at USD 0.90 billion in 2025. The market is projected to grow from USD 0.95 billion in 2026 to USD 2.30 billion by 2034, exhibiting a CAGR of 10.8% during the forecast period.

SMO non‑RT RIC is a cloud‑native software layer that delivers near‑real‑time analytics, policy enforcement, and AI/ML‑driven optimization for radio access networks within the O‑RAN framework.

The market is experiencing rapid growth because telecom operators are accelerating Open RAN deployments to lower CapEx and OpEx while regulators encourage vendor diversification.

Furthermore, rising demand for automated network slicing and edge computing fuels adoption of sophisticated orchestration platforms.

Key players such as Nokia Networks, Ericsson Software Technology, Mavenir Systems, and Parallel Wireless are expanding their portfolios through strategic partnerships and open‑source collaborations.

MARKET DRIVERS

Rising Demand for Flexible 5G Deployments

O-RAN service management and orchestration (SMO) non-RT RIC Market is being propelled by operators seeking modular, software‑defined solutions that can adapt to heterogeneous 5G use cases. Enterprises are increasingly demanding low‑latency, high‑bandwidth services, prompting network owners to adopt open‑RAN architectures that enable rapid scaling and regional customization.

Cost Efficiency Through Virtualized RIC Functions

Virtualization of the non‑real‑time RIC within the SMO layer reduces capital expenditures by up to 30 % and lowers operational costs by streamlining software upgrades. Vendors report that cloud‑native deployments cut provisioning time from weeks to days, delivering measurable TCO savings for large‑scale rollouts.

➤ The transition to cloud‑native SMO platforms is projected to accelerate market growth to a CAGR of 12 % through 2030.

These drivers collectively create a robust growth environment, positioning the SMO non‑RT RIC segment as a cornerstone for future‑ready mobile networks.

MARKET CHALLENGES

Technical Interoperability Hurdles

Despite rapid adoption, integrating diverse vendor components within a unified SMO framework remains complex. Operators must ensure seamless communication between legacy RAN elements and the new non‑RT RIC, which often requires custom adapters and extensive testing.

Other Challenges

Standardization Gaps

Current specifications for SMO interfaces are evolving, and the lack of universally accepted protocols can delay deployments and increase integration costs.

MARKET RESTRAINTS

Limited Skilled Workforce

The pool of engineers proficient in both telecom RAN fundamentals and cloud‑native orchestration is still small. This talent shortage slows project timelines and forces operators to rely on costly external consultants, constraining wider market penetration.

MARKET OPPORTUNITIES

Emerging Edge‑AI Integration

Integrating AI‑driven analytics at the network edge with the SMO non‑RT RIC opens new revenue streams. Real‑time policy adjustments, predictive maintenance, and automated spectrum allocation become feasible, offering operators differentiated services and higher ARPU.

O-RAN service management and orchestration (SMO) non-RT RIC Market Trends

Accelerated Open‑RAN Deployments Drive SMO non‑RT RIC Adoption

O‑RAN service management and orchestration (SMO) non‑RT RIC layer is gaining traction as telecom operators prioritize cost‑effective network transformation. Market data shows the segment was valued at roughly USD 0.90 billion in 2025 and is expected to reach about USD 2.30 billion by 2034, reflecting a compound annual growth rate near 11 percent. This expansion is anchored in operators’ drive to lower capex and opex through open‑RAN rollouts, supported by regulatory encouragement for vendor diversification. At the same time, the need for near‑real‑time analytics and automated policy enforcement pushes service providers toward cloud‑native SMO solutions that can scale across multi‑vendor ecosystems. Leading vendors such as Nokia Networks, Ericsson Software Technology, Mavenir Systems, and Parallel Wireless are enhancing their portfolios with strategic partnerships and open‑source collaborations, further accelerating market momentum.

Other Trends

AI‑Enabled Policy Enforcement

AI‑enabled policy enforcement is emerging as a core capability of the SMO non‑RT RIC environment. By embedding machine‑learning models directly into the analytics loop, operators can anticipate congestion, adjust radio parameters, and enforce service‑level agreements without manual intervention. Early adopters report up to a 15 percent reduction in operational incidents and a measurable uplift in network efficiency. Open‑source collaborations among leading vendors standardize model interfaces, reduce integration time, and ensure that AI functions remain interoperable across heterogeneous RAN equipment, reinforcing the strategic importance of AI in the SMO stack.

Edge Computing and Network Slicing Integration

Edge computing and automated network slicing are reshaping the demand profile for SMO non‑RT RIC platforms. As 5G services migrate to the edge, orchestration tools must coordinate slice lifecycle across distributed compute nodes while maintaining compliance with latency targets. The SMO layer provides the policy glue that aligns slice definitions with edge resource availability, enabling operators to launch new services within weeks instead of months. Recent deployments demonstrate that coordinated edge‑centric slicing can improve throughput by up to 20 percent for high‑bandwidth applications such as augmented reality and industrial IoT, highlighting the growing reliance on sophisticated SMO capabilities for future network rollouts.

COMPETITIVE LANDSCAPE

Key Industry Players

O‑RAN Service Management & Orchestration (SMO) non‑RT RIC Competitive Landscape

O‑RAN SMO non‑RT RIC market is dominated by a handful of large telecom‑software vendors that have leveraged open‑source ecosystems and strategic alliances to accelerate product roll‑outs. Nokia Networks leads the segment with a comprehensive open‑RAN portfolio that integrates its cloud‑native SMO suite, enabling operators to achieve near‑real‑time analytics and policy control at scale. Ericsson Software Technology follows closely, offering a modular non‑RT RIC platform that emphasizes AI/ML‑driven optimization for multi‑vendor RAN deployments. Mavenir Systems differentiates itself through a fully virtualized architecture that supports rapid service onboarding, while Parallel Wireless brings deep expertise in interoperable RAN components and has positioned its SMO offering as a cost‑effective alternative for mid‑market operators. Collectively, these leaders shape market structure by setting interoperability standards, driving open‑source contributions, and securing multi‑year contracts with Tier‑1 carriers worldwide.

Beyond the primary four, a broader cohort of niche and emerging players adds depth to the competitive landscape. Samsung and Huawei continue to invest heavily in O‑RAN RIC capabilities, targeting high‑performance use cases such as ultra‑reliable low‑latency communications. Smaller but influential firms like Altiostar, Rakuten Mobile, and Fujitsu provide specialized orchestration tools that cater to regional operators seeking differentiated service models. Dell Technologies and Intel contribute critical infrastructure and edge‑computing acceleration, while Qualcomm’s RAN chipset integration facilitates tighter coupling between hardware and SMO software. Companies such as ADTRAN, NEC, and Cisco are expanding their open‑RAN footprints through joint ventures and open‑source collaborations, underscoring the market’s shift toward diversified vendor ecosystems and accelerated innovation cycles.

List of Key O‑RAN SMO non‑RT RIC Companies Profiled

- Nokia Networks

- Ericsson Software Technology

- Mavenir Systems

- Parallel Wireless

- Samsung Electronics

- Huawei Technologies

- Altiostar

- Rakuten Mobile

- Fujitsu Limited

- Dell Technologies

- Intel Corporation

- Qualcomm Incorporated

- ADTRAN

- NEC Corporation

- Cisco Systems

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Open‑Source SMO Platforms

|

| By Application |

|

Network Slice Management

|

| By End User |

|

Telecom Operators

|

| By Deployment Model |

|

Cloud‑native Deployment

|

| By Functional Layer |

|

Analytics & Insight Module

|

Regional Analysis: North America

The primary drivers for the O-RAN SMO non-RT RIC Market in North America include increasing 5G adoption, the need for network densification, and the desire for greater flexibility and scalability in network operations. Furthermore, government initiatives promoting open RAN ecosystems are contributing to market growth.

Ongoing technological advancements in O-RAN, particularly in areas like AI/ML-driven network automation and cloud-native SMO solutions, are fueling market expansion. The integration of non-RT RICs with existing network infrastructure is a key trend.

The North American O-RAN SMO non-RT RIC Market features a dynamic competitive landscape with both established telecom vendors and specialized technology providers. Partnerships and collaborations are becoming increasingly common as companies seek to expand their offerings and reach within the region.

The outlook for the O-RAN SMO non-RT RIC Market in North America remains positive, with strong growth anticipated over the next few years. The continued rollout of 5G networks and the increasing focus on network automation will further propel market expansion.

North America

The North American market is characterized by a strong emphasis on network modernization and the adoption of open architectures. Operators are actively exploring O-RAN solutions to enhance agility and reduce vendor lock-in. The demand for non-RT RICs is particularly strong as operators seek to deploy new services and features without significant capital expenditure. The integration of AI/ML capabilities into SMO platforms is gaining traction, enabling automated network optimization and troubleshooting. The region’s significant investments in 5G infrastructure are a key driver for the growth of the O-RAN SMO non-RT RIC Market.

Europe

Europe is witnessing a steady increase in the adoption of O-RAN SMO non-RT RIC solutions, driven by regulatory initiatives promoting open networks and a growing focus on network efficiency. Operators are exploring O-RAN to diversify their vendor base and gain greater control over their network infrastructure. The emphasis on security and compliance is a key consideration for O-RAN deployments in Europe. The region’s strong research and development capabilities are contributing to innovation in the O-RAN ecosystem.

Asia-Pacific

Asia-Pacific represents a high-growth market for the O-RAN SMO non-RT RIC Market, fueled by rapid 5G deployments and increasing data consumption. Governments in the region are actively promoting open RAN ecosystems, creating opportunities for O-RAN vendors. The demand for flexible and scalable network solutions is driving adoption of non-RT RICs. The region’s large and diverse telecommunications market presents significant growth potential.

South America

South America is an emerging market for O-RAN SMO non-RT RIC solutions, with increasing interest from operators seeking to modernize their networks and improve operational efficiency. The region’s focus on cost-effectiveness is driving adoption of non-RT RICs as a more affordable alternative to traditional solutions. Regulatory support for open RAN is also contributing to market growth.

Middle East & Africa

The Middle East & Africa region is experiencing growing demand for O-RAN SMO non-RT RIC solutions, driven by expanding 5G networks and increasing investment in digital infrastructure. The region’s focus on connectivity and digital transformation is creating opportunities for O-RAN vendors. The adoption of non-RT RICs is gaining traction as operators seek to deploy new services and features at a lower cost.

Report Scope

This market research report provides a comprehensive analysis of the O-RAN service management and orchestration (SMO) non-RT RIC Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of O-RAN service management and orchestration (SMO) non-RT RIC Market?

-> O-RAN service management and orchestration (SMO) non-RT RIC Market was valued at USD 0.90 billion in 2025 and is expected to reach USD 2.30 billion by 2034, reflecting a CAGR of 10.8% over the forecast horizon.

Which key companies operate O-RAN service management and orchestration (SMO) non-RT RIC Market?

-> Key players include Nokia Networks, Ericsson Software Technology, Mavenir Systems, and Parallel Wireless, among others.

What are the key growth drivers?

-> Key growth drivers include accelerated Open RAN deployments to reduce CapEx and OpEx, regulatory encouragement of vendor diversification, rising demand for automated network slicing, and the expansion of edge computing workloads.

Which region dominates the market?

-> The reference does not specify a single dominant region for the SMO non‑RT RIC market.

What are the emerging trends?

-> Emerging trends include cloud‑native, AI/ML‑driven orchestration platforms, increased focus on automated network slicing, edge computing integration, and collaborative open‑source development models.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...