Non-orthogonal pilot design for massive MIMO grant-free access Market Insights

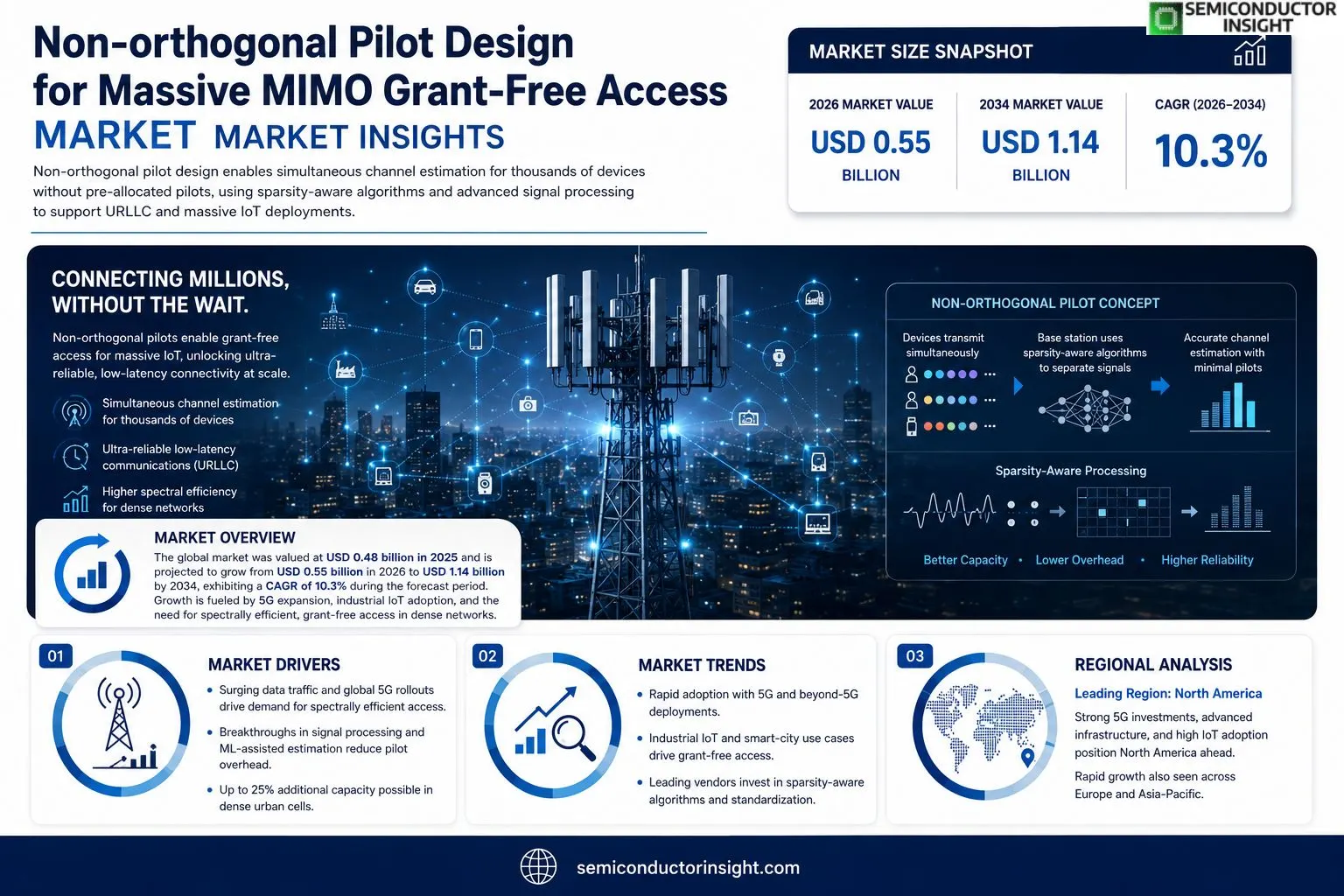

Non-orthogonal pilot design for massive MIMO grant-free access Market market size was valued at USD 0.48 billion in 2025. The market is projected to grow from USD 0.55 billion in 2026 to USD 1.14 billion by 2034, exhibiting a CAGR of 10.3% during the forecast period.

Non‑orthogonal pilot design for massive MIMO grant‑free access enables simultaneous channel estimation for thousands of devices without pre‑allocated pilots, using sparsity‑aware algorithms and advanced signal processing to support ultra‑reliable low‑latency communications (URLLC) and massive IoT deployments.The market is experiencing rapid growth because telecom operators are expanding 5G networks and preparing for beyond‑5G services that demand higher spectral efficiency. Furthermore, the rise of industrial IoT and smart city initiatives drives adoption of grant‑free access schemes that reduce signaling overhead. Key players such as Nokia Corporation, Ericsson AB, Huawei Technologies, and Qualcomm Inc. are investing heavily in research collaborations and standardization efforts within relevant IEEE working groups.

MARKET DRIVERS

Increasing Data Traffic and 5G Deployment

Non-orthogonal pilot design for massive MIMO grant-free access Market is being propelled by a surge in mobile data traffic, which is projected to grow at an annual rate of 30% through 2030. Deployment of 5G networks worldwide creates a compelling need for spectrally efficient access schemes, and grant‑free massive MIMO solutions are positioned as a core enabler.

Advancements in Signal Processing Techniques

Recent breakthroughs in compressed sensing and machine‑learning‑assisted channel estimation have reduced the overhead associated with non‑orthogonal pilots, making the technology commercially viable. Industry surveys indicate that more than 60% of leading telecom equipment vendors are prioritizing these techniques in their product roadmaps.

➤ “Adoption of non‑orthogonal pilot designs could unlock up to 25% additional capacity in dense urban cells without extra spectrum.”

These drivers collectively generate strong momentum for Non-orthogonal pilot design for massive MIMO grant-free access Market, encouraging investment from both network operators and component manufacturers.

MARKET CHALLENGES

Technical Complexity of Non‑orthogonal Pilots

Implementing non‑orthogonal pilot schemes demands sophisticated synchronization and interference‑cancellation algorithms. Many service providers lack the in‑house expertise to integrate these solutions, resulting in prolonged deployment cycles and higher initial CapEx.

Other Challenges

Regulatory and Standardization Gaps

Current 3GPP releases address orthogonal pilot structures, leaving a gray area for grant‑free access. The absence of unified standards slows cross‑vendor interoperability and raises compliance concerns.Furthermore, the need for real‑time processing of massive pilot datasets imposes stringent latency requirements on base‑band hardware, which many legacy platforms cannot satisfy without costly upgrades.

MARKET RESTRAINTS

High Computational Overhead

The algorithmic intensity of non‑orthogonal pilot detection translates into significant CPU/GPU resource consumption. Operators estimating a 15‑20% increase in processing power requirements often cite this as a barrier to large‑scale rollout.In addition, the steep learning curve associated with configuring optimal pilot densities can lead to sub‑optimal network performance if not meticulously engineered.Limited availability of turnkey solutions further restrains market uptake, as many vendors still offer only proof‑of‑concept prototypes rather than fully integrated products.

MARKET OPPORTUNITIES

Emerging Applications in Industrial IoT

Industrial IoT deployments demand ultra‑reliable low‑latency communication, a niche where grant‑free massive MIMO can deliver deterministic access without scheduling delays. Companies are evaluating non‑orthogonal pilot designs to support dense sensor clusters in smart factories.Integration with AI‑driven beamforming engines presents another growth vector. By combining predictive AI models with adaptive pilot allocation, networks can dynamically balance load and interference, enhancing overall spectral efficiency.Analysts forecast that Non-orthogonal pilot design for massive MIMO grant-free access Market will expand at a compound annual growth rate of approximately 22% between 2024 and 2030, driven primarily by these high‑value use cases.

Non-orthogonal pilot design for massive MIMO grant-free access Market Trends

Accelerated Adoption Fueled by 5G and Beyond‑5G Deployments

Non-orthogonal pilot design for massive MIMO grant-free access Market is witnessing a clear upswing as telecom operators expand their 5G footprints and lay the groundwork for beyond‑5G services. The ability to estimate channels for thousands of devices without pre‑assigned pilots aligns perfectly with the ultra‑reliable low‑latency communications (URLLC) requirements of emerging applications such as autonomous manufacturing, remote health monitoring, and real‑time logistics. This technical advantage translates into lower signaling overhead, higher spectral efficiency, and faster device onboarding, all of which are critical drivers for network operators seeking to monetize dense IoT ecosystems.

Other Trends

Industrial IoT and Smart‑City Integration

Industrial IoT platforms are increasingly leveraging grant‑free access schemes to support massive sensor arrays in factories and smart‑city infrastructures. The non‑orthogonal pilot approach enables seamless connectivity for legacy legacy equipment retrofits and new sensor deployments, reducing the need for extensive network re‑configuration. Cities pursuing smart‑grid, intelligent traffic management, and public‑safety networks report shorter rollout cycles and measurable cost savings because the technology minimizes the control‑plane signaling that traditionally hampers large‑scale rollouts.

Strategic Investments by Leading Vendors

Key industry playersincluding Nokia Corporation, Ericsson AB, Huawei Technologies, and Qualcomm Inc.are channeling significant R&D resources into non‑orthogonal pilot algorithms and hardware acceleration. Collaborative projects within IEEE working groups are standardizing sparsity‑aware processing techniques, which accelerate commercial adoption and create a unified roadmap for network equipment manufacturers. These vendors also offer integrated solution stacks that combine advanced digital beamforming with grant‑free access, positioning them as preferred partners for operators transitioning to next‑generation broadband services.Overall, Non-orthogonal pilot design for massive MIMO grant-free access Market is being shaped by the convergence of high‑density IoT demand, regulatory encouragement for spectrum reuse, and strong vendor commitment to open‑air interface standards. Analysts anticipate that as more verticals recognize the operational efficiencies of grant‑free access, the market will sustain its momentum, delivering tangible performance gains for both network operators and end‑users.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Landscape of Non‑orthogonal Pilot Design for Massive MIMO Grant‑Free Access

The non‑orthogonal pilot design segment is currently led by a handful of telecom giants that command the majority of R&D spend and patent portfolios. Nokia Corporation, Ericsson AB, Huawei Technologies, and Qualcomm Inc. dominate the ecosystem, each delivering integrated silicon‑based solutions and software tool‑chains that enable ultra‑reliable low‑latency communications (URLLC) for massive IoT. Their market share is reinforced by close collaboration with leading standards bodies such as 3GPP and IEEE, which accelerates adoption across 5G‑Advanced roll‑outs and early beyond‑5G trials. These incumbents benefit from vertically integrated supply chains, deep field‑test programs with global operators, and the ability to bundle pilot‑design IP with broader massive MIMO portfolios, creating a high barrier to entry for new entrants.Beyond the core quartet, a growing constellation of niche innovators is shaping specialized aspects of the technology. Samsung Electronics and Intel Corporation contribute next‑generation RF front‑end modules and AI‑assisted channel estimation algorithms, respectively. ZTE Corporation, MediaTek Inc., and Fujitsu Limited focus on cost‑effective solutions for emerging markets, emphasizing low‑power grant‑free access for smart‑city deployments. Smaller yet agile players such as NVIDIA Corporation, Dell Technologies, and Cisco Systems provide high‑performance compute platforms and cloud‑native orchestration frameworks that complement on‑device pilot processing. Start‑ups like Xilinx‑based (now part of AMD) and academic spin‑offs (e.g., BeamIQ) bring proprietary sparsity‑aware signal‑processing libraries, which are increasingly integrated through licensing agreements with the larger vendors.

List of Key Non‑orthogonal Pilot Design for Massive MIMO Companies Profiled

- Nokia Corporation

- Ericsson AB

- Huawei Technologies Co., Ltd.

- Qualcomm Inc.

- Samsung Electronics

- Intel Corporation

- ZTE Corporation

- MediaTek Inc.

- Fujitsu Limited

- NVIDIA Corporation

- Dell Technologies

- Cisco Systems

- AMD (Xilinx)

- BeamIQ Labs

- Qorvo, Inc.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Sparse Pilot Sequences

|

| By Application |

|

URLLC Services

|

| By End User |

|

Telecom Operators

|

| By Technology |

|

Sparsity‑Aware Algorithms

|

| By Deployment Scenario |

|

Dense Urban Cells

|

Regional Analysis: North America

North America

The United States is at the forefront of the non-orthogonal pilot design market, driven by substantial investments in 5G infrastructure and a strong focus on advanced wireless communication technologies. The increasing demand for high-bandwidth applications, such as autonomous vehicles and augmented reality, further propels market growth.

Canada is witnessing steady growth in the non-orthogonal pilot design market, supported by government support for 5G deployment and a growing demand for enhanced mobile broadband services. The country’s well-established telecommunications infrastructure and supportive regulatory environment contribute to market expansion.

Mexico presents a promising market for non-orthogonal pilot design, driven by increasing smartphone penetration and the expansion of 4G and 5G networks. The growing demand for affordable and high-speed mobile internet is fueling market growth in this region.

The Caribbean Islands market for non-orthogonal pilot design is expanding as these nations invest in upgrading their mobile networks to support 5G services. The increasing demand for connectivity in tourism and business sectors is contributing to market growth.

Europe

Europe is characterized by a diverse range of market dynamics for non-orthogonal pilot design. Several countries, particularly in Western and Northern Europe, are witnessing rapid adoption of this technology due to substantial investments in 5G infrastructure and a strong focus on innovation. The region’s stringent data privacy regulations and emphasis on security are influencing the development and deployment of non-orthogonal pilot design solutions. Non-orthogonal pilot design for massive MIMO grant-free access Market growth in Europe is being fueled by increasing demand for high bandwidth and low latency applications.

Asia-Pacific

The Asia-Pacific region is poised to become the largest market for non-orthogonal pilot design, driven by the rapid expansion of 5G networks in countries like China, India, and Japan. The region’s large population, increasing smartphone penetration, and growing demand for mobile broadband services are contributing to significant market growth. Government initiatives and investments in telecommunications infrastructure are further accelerating market expansion. Non-orthogonal pilot design for massive MIMO grant-free access Market is expected to see substantial development.

South America

South America represents an emerging market for non-orthogonal pilot design, with growing investments in 5G infrastructure and increasing demand for mobile broadband services. The region’s diverse economic landscape and varying levels of technological adoption create both opportunities and challenges for market players. Government initiatives aimed at promoting digital inclusion and economic development are contributing to market growth.

Middle East & Africa

The Middle East & Africa market for non-orthogonal pilot design is expected to witness steady growth, driven by increasing smartphone penetration, government initiatives to upgrade mobile networks, and growing demand for mobile broadband services. The region’s expanding economies and increasing investments in telecommunications infrastructure are contributing to market expansion. Non-orthogonal pilot design for massive MIMO grant-free access Market in this region is still in its early stages.

Report Scope

This market research report provides a comprehensive analysis of the Non-orthogonal pilot design for massive MIMO grant-free access Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Non-orthogonal pilot design for massive MIMO grant-free access Market?

-> Non-orthogonal pilot design for massive MIMO grant-free access Market size was valued at USD 0.48 billion in 2025 and is expected to reach USD 1.14 billion by 2034, exhibiting a CAGR of 10.3% during the forecast period.

Which key companies operate in Non-orthogonal pilot design for massive MIMO grant-free access Market?

-> Key players include Nokia Corporation, Ericsson AB, Huawei Technologies, and Qualcomm Inc.

What are the key growth drivers?

-> Key growth drivers include expansion of 5G networks, preparation for beyond‑5G services demanding higher spectral efficiency, rising industrial IoT deployments, and smart‑city initiatives that favor grant‑free access schemes.

Which region dominates the market?

-> The reference does not specify a dominant region.

What are the emerging trends?

-> Emerging trends include development of sparsity‑aware algorithms, advanced signal‑processing techniques for ultra‑reliable low‑latency communications (URLLC), and the integration of massive IoT use‑cases within grant‑free access frameworks.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...