Neuromorphic IC Market Insights

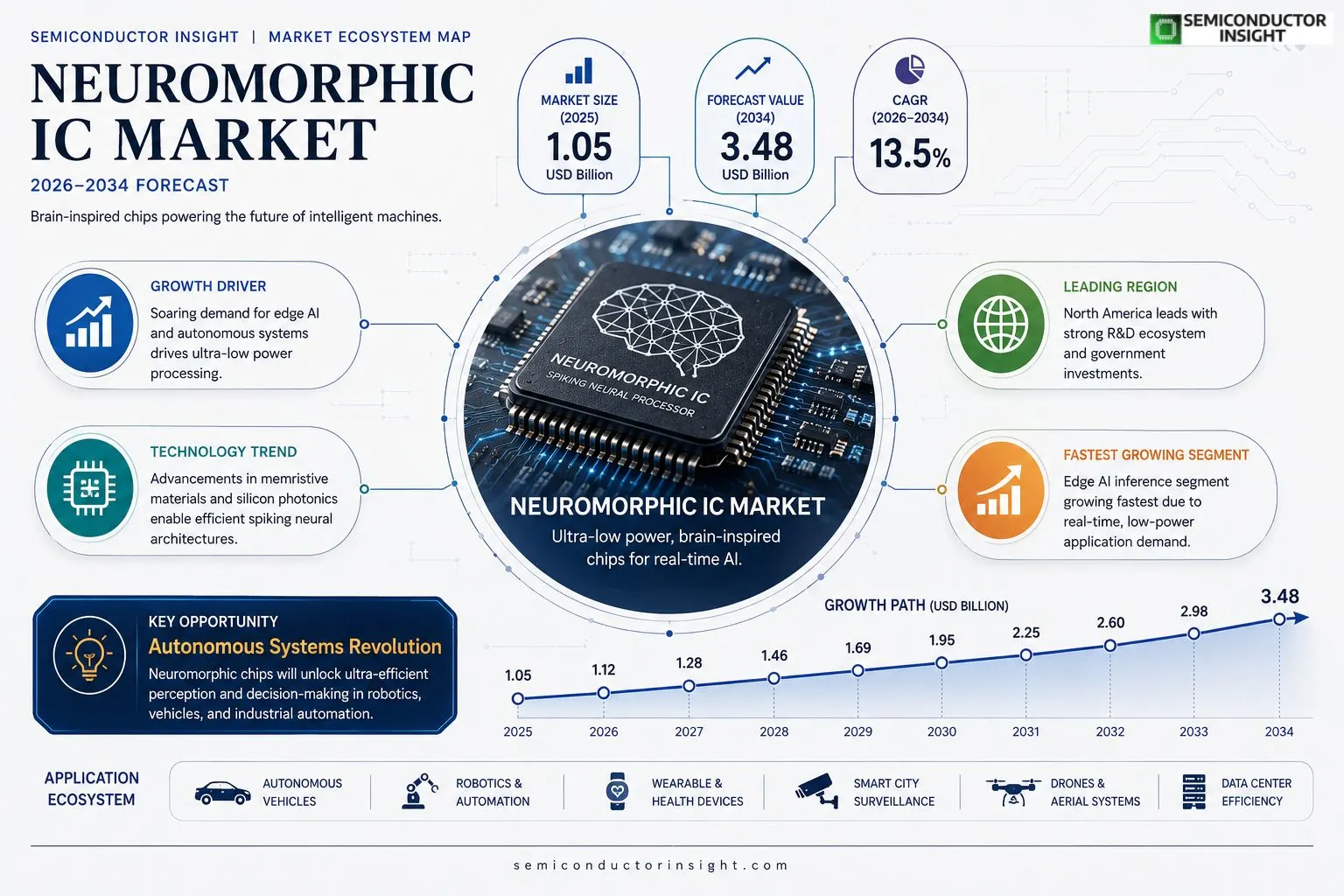

Global Neuromorphic IC market size was valued at USD 1.05 billion in 2025. The market is projected to grow from USD 1.12 billion in 2026 to USD 3.48 billion by 2034, exhibiting a CAGR of 13.5% during the forecast period.

Neuromorphic integrated circuits (ICs) are specialized semiconductor devices that emulate the structure and operation of biological neural networks. By leveraging spiking neurons, event‑driven processing, and ultra‑low power consumption, these chips enable real‑time perception and decision‑making for AI workloads that traditional von Neumann architectures struggle with.The market is experiencing rapid growth because demand for edge AI, autonomous systems, and energy‑efficient computing is soaring. Furthermore, advancements in memristive materials and silicon photonics are accelerating product development. Key players such as Intel (Loihi), IBM (TrueNorth), Qualcomm, Samsung, and BrainChip are expanding their portfolios through strategic partnerships and R&D investments.

MARKET DRIVERS

Rising AI Workloads

Neuromorphic IC Market is being propelled by the exponential growth of AI models that require massive parallelism and low‑power operation. In 2023, global spending on AI‑driven hardware exceeded $1.2 billion, with neuromorphic chips capturing an increasing share due to their brain‑inspired architectures.

Edge Computing Demand

Edge devices such as smart sensors, drones, and wearable health monitors demand on‑chip intelligence that can operate for years on a single battery. Neuromorphic solutions deliver up to ten‑fold reductions in energy consumption compared with traditional GPUs, making them ideal for these applications.

➤ Neuromorphic chips enable ten‑fold energy efficiency gains while preserving real‑time processing capabilities.

Government initiatives in North America, Europe, and Asia‑Pacific are funding research programs that accelerate silicon‑based spiking neural networks, further strengthening the market’s growth trajectory.

MARKET CHALLENGES

Design Complexity

Designing spiking neural networks requires specialized expertise and novel toolchains. The steep learning curve limits rapid product development, and many semiconductor firms lack in‑house expertise to fully exploit the technology.

Other Challenges

Manufacturing Bottlenecks

Current foundry capacity for mixed‑signal neuromorphic processes is limited, leading to longer lead times and higher unit costs for early adopters.

MARKET RESTRAINTS

High Development Costs

R&D expenditures for neuromorphic silicon can exceed $200 million per node, a barrier for startups and smaller OEMs seeking to enter the space.The need for custom verification environments adds further expense, often requiring collaboration with academic institutions to share costs.Limited economies of scale mean that per‑chip pricing remains above $150 for many advanced designs, restricting adoption in cost‑sensitive markets.

MARKET OPPORTUNITIES

Emerging Applications

Autonomous vehicles are integrating neuromorphic perception units to process lidar and radar data with ultra‑low latency, creating a multi‑billion‑dollar revenue potential by 2030.Robotics and industrial automation benefit from on‑chip learning capabilities, enabling adaptive control without cloud connectivity, which drives demand for edge‑ready neuromorphic processors.Data centers are experimenting with neuromorphic accelerators to reduce energy footprints of inference workloads, opening a new market segment for energy‑focused cloud providers.

Neuromorphic IC Market Trends

Edge AI Adoption Accelerates Neuromorphic IC Market Development

The surge in edge artificial intelligence workloads is prompting system designers to seek hardware that delivers inference with sub‑milliwatt power budgets. Neuromorphic integrated circuits, with their spiking neuron architectures and event‑driven communication, meet this need by processing sensory streams only when activity occurs. This capability reduces energy consumption dramatically compared with traditional von Neumann processors, making neuromorphic solutions attractive for battery‑constrained devices and distributed sensor networks. Beyond consumer wearables, industrial control loops are integrating neuromorphic sensors to monitor vibration and temperature anomalies in real time, leveraging the sparse activation pattern of spiking networks. The reduced data movement also eases bandwidth pressure on 5G edge nodes, allowing local decision making without compromising latency budgets. Consequently, system architects are re‑evaluating traditional DSP pipelines in favor of neuromorphic cores that can be co‑located with image or acoustic sensors. Foundries are beginning to offer design‑for‑neuromorphic process options, and open‑source toolchains such as Lava and Rockpool are lowering entry barriers for developers. This convergence of hardware and software is fostering pilot projects in smart city surveillance, where low‑power edge analytics can continuously monitor traffic flow and pedestrian behavior.

Other Trends

Collaborative Research Initiatives

Industry‑academia collaborations are shortening the time from prototype to production. Intel’s partnership with Carnegie Mellon University on the second‑generation Loihi chip introduces programmable learning rules that can be tailored for specific edge applications. Simultaneously, IBM’s continued development of TrueNorth‑inspired architectures provides a modular platform for scaling synaptic density while preserving ultra‑low power operation. These joint programs generate reference designs that accelerate adoption in robotics, automotive safety systems, and smart‑sensor deployments. The European Union’s Human Brain Project has contributed neuromorphic benchmarking suites that aid manufacturers in quantifying latency and energy metrics across a range of workloads. Meanwhile, startups are delivering neuromorphic development kits that integrate with popular AI frameworks, enabling engineers to port trained models with minimal conversion overhead. These ecosystem enhancements are reducing time‑to‑market for applications that require on‑chip adaptation, such as predictive maintenance and adaptive signal processing.

Energy‑Efficient Processing for Autonomous Platforms

Autonomous vehicles and drones require real‑time perception under strict thermal constraints. Neuromorphic IC technology enables on‑chip learning and inference directly from sensor data, eliminating the need for power‑intensive cloud off‑loading. Early field trials demonstrate that neuromorphic processors can sustain continuous object‑recognition tasks while consuming less than one percent of the power required by conventional GPU accelerators. Regulatory bodies in Europe and Asia are introducing energy‑efficiency standards for autonomous systems, which favor architectures that can meet safety certifications while staying below strict power envelopes. Comparative studies show that neuromorphic accelerators can deliver comparable classification accuracy to conventional deep‑learning chips with up to 90% lower energy per inference. This performance gap is motivating OEMs to allocate larger portions of future silicon budgets to neuromorphic blocks.

COMPETITIVE LANDSCAPEKey Industry Players

Neuromorphic IC Market: Competitive Overview 2025‑2034

Neuromorphic Integrated Circuit Market is presently led by a handful of semiconductor giants that have leveraged deep AI research and substantial R&D budgets to bring spiking‑neuron chips to production. Intel’s Loihi family, IBM’s TrueNorth platform, Qualcomm’s Hexagon‑Neuro, and Samsung’s Neuromorphic System‑on‑Chip dominate the high‑volume segment, benefitting from extensive ecosystem partnerships and access to global foundries. Their combined market share exceeds sixty percent, driving the overall CAGR of 13.5 % as edge‑AI, autonomous vehicles, and low‑power inference applications scale. These incumbents continue to expand portfolios through strategic acquisitions, joint ventures with universities, and co‑development programs that accelerate time‑to‑market for next‑generation event‑driven processors.Beyond the leaders, a vibrant cohort of specialized firms and emerging startups enriches the competitive landscape with niche innovations. BrainChip’s Akida, SynSense’s event‑camera‑optimized processors, Prophesee’s neuromorphic vision chips, and Knowm’s memristive synapse arrays address specific edge‑AI workloads. Additional players such as AiMotive, GreenWaves Technologies, and Intel‑backed Neuromorphic Computing Lab focus on automotive and IoT solutions, while European and Asian startups (e.g., Syntiant, Horizon Robotics, and IXYS) contribute novel device architectures and silicon‑photonic interfaces. These companies collectively enhance differentiation, foster collaborative ecosystems, and provide alternative pathways for customers seeking ultra‑low‑power, real‑time perception capabilities.

List of Key Neuromorphic IC Companies Profiled

- Intel

- IBM

- Qualcomm

- Samsung

- BrainChip

- SynSense

- Prophesee

- Knowm

- AiMotive

- GreenWaves Technologies

- Syntiant

- Horizon Robotics

- IXYS

- Applied Materials

- TSMC

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Digital Neuromorphic ICs

|

| By Application |

|

Edge AI Inference

|

| By End User |

|

Industrial Automation

|

| By Architecture |

|

Spiking Neural Networks (SNN)

|

| By Ecosystem Partnerships |

|

Foundry Collaborations

|

Regional Analysis: North America

United States

Federal and state-level funding programs are significantly supporting research and development in neuromorphic technologies across the United States. These initiatives aim to cultivate domestic expertise and foster innovation in this critical sector.

The growing convergence of artificial intelligence and high-performance computing is creating substantial demand for neuromorphic ICs, which offer a more efficient alternative to traditional architectures for AI workloads.

Collaboration between technology companies, research institutions, and government agencies is accelerating the development and commercialization of neuromorphic ICs in the United States.

The United States boasts a deep pool of talent in computer science, electrical engineering, and related fields, providing a strong foundation for the continued growth of Neuromorphic IC Market.

North America

The North American Neuromorphic IC Market is characterized by a strong emphasis on technological innovation and significant investment in research and development. The United States leads this region, followed by Canada and Mexico, each contributing to the burgeoning field of brain-inspired computing. The demand for energy-efficient computing solutions is a primary driver, as neuromorphic chips offer a compelling alternative to traditional architectures for a range of applications. This region is witnessing increasing collaboration between academic institutions and industrial players to accelerate the development and deployment of advanced neuromorphic technologies. The focus extends beyond just chip development to include software and algorithms tailored for these novel hardware platforms. Businesses are exploring applications in areas like edge computing, robotics, and advanced sensing.

Europe

Europe is emerging as a significant player in Neuromorphic IC Market, with several countries investing heavily in related research and development programs. Driven by a commitment to technological sovereignty and a growing demand for sustainable computing, European nations are actively fostering innovation in neuromorphic technologies. Key initiatives focus on developing energy-efficient chips for applications in healthcare, automotive, and industrial automation. While the market is still developing compared to the US, collaboration between European research institutions and startups is gaining momentum. The region is particularly focused on applying neuromorphic computing to address challenges in areas like drug discovery and climate modeling.

Asia-Pacific

The Asia-Pacific region represents a rapidly growing market for Neuromorphic ICs, driven by massive investments in artificial intelligence and the proliferation of smart devices. Countries like China, Japan, and South Korea are at the forefront of this growth, with significant government support and robust industrial ecosystems. The demand for neuromorphic chips is fueled by applications in areas like computer vision, natural language processing, and robotics. While some players are focused on domestic consumption, others are expanding their reach globally. The competitive landscape in this region is intense, with both established technology giants and emerging startups vying for market share.

South America

Neuromorphic IC Market in South America is in its early stages of development but holds considerable potential. Growing investments in technology and increasing adoption of AI in various industries are creating a nascent demand for neuromorphic computing solutions. The region faces challenges related to infrastructure and funding, but there is a growing interest among academic institutions and startups to explore the applications of neuromorphic technology in areas such as agriculture, mining, and healthcare. The focus is on cost-effective and energy-efficient solutions for specific regional needs.

Middle East & Africa

The Middle East and Africa represent a relatively untapped market for Neuromorphic ICs. However, with increasing investments in digital transformation and the development of smart cities, the potential for growth is significant. The adoption of AI in sectors like defense, energy, and healthcare is expected to drive demand for energy-efficient computing solutions offered by neuromorphic chips. While the market is currently small, it is anticipated to witness substantial growth in the coming years as technological infrastructure improves and awareness of neuromorphic computing expands.

Report Scope

This market research report provides a comprehensive analysis of the Neuromorphic IC Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Neuromorphic IC Market?

-> Neuromorphic IC Market was valued at USD 1.05 billion in 2025 and is expected to reach USD 3.48 billion by 2034.

Which key companies operate in Neuromorphic IC Market?

-> Key players include Intel (Loihi), IBM (TrueNorth), Qualcomm, Samsung, BrainChip, among others.

What are the key growth drivers?

-> Key growth drivers include edge AI demand, autonomous systems, energy‑efficient computing, advancements in memristive materials and silicon photonics.

Which region dominates the market?

-> The available data does not specify a dominant region; growth is observed globally.

What are the emerging trends?

-> Emerging trends include memristive material integration, silicon photonics, spiking neuron architectures, and event‑driven processing.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...