MARKET INSIGHTS

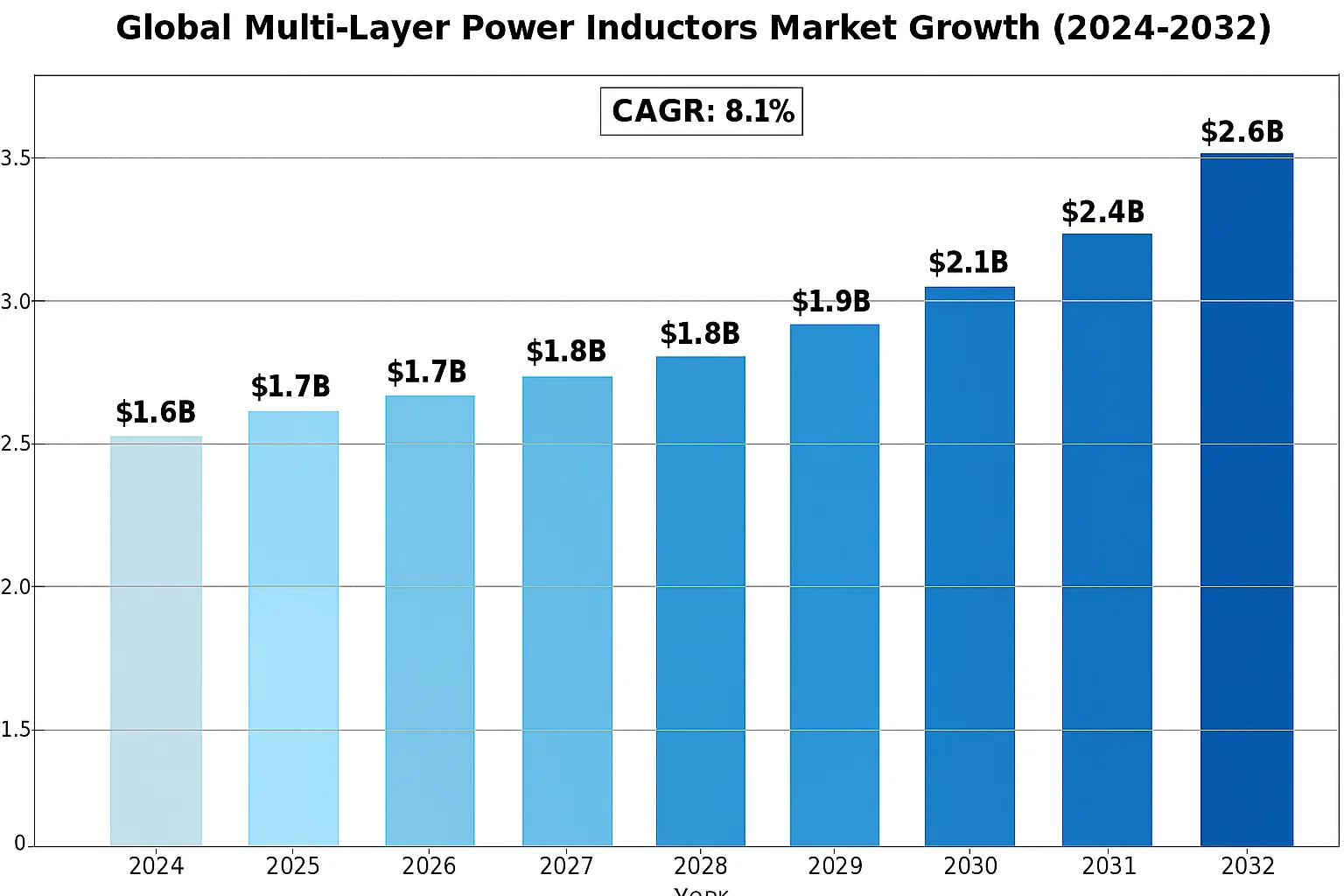

The global Multi-Layer Power Inductors market was valued at 1553 million in 2024 and is projected to reach US$ 2647 million by 2032, at a CAGR of 8.1% during the forecast period.

Multi-Layer Power Inductors are passive electronic components designed for energy storage and filtering in power management applications. These inductors utilize stacked magnetic layers to achieve higher inductance values while minimizing DC resistance and size. They play a critical role in voltage regulation, noise suppression, and energy conversion across various electronic systems including DC-DC converters, power supplies, and RF circuits.

The market growth is primarily driven by increasing demand for compact, high-efficiency power solutions across industries. Emerging applications in 5G infrastructure, electric vehicles, and IoT devices are creating new opportunities, while traditional sectors like consumer electronics continue to demonstrate strong demand. Leading manufacturers are focusing on material innovations and miniaturization techniques to address evolving industry requirements for higher power density and thermal performance.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Consumer Electronics and IoT Devices to Accelerate Market Growth

The rapid proliferation of consumer electronics and IoT devices is significantly driving demand for multi-layer power inductors. With over 29 billion IoT devices expected to be connected globally by 2030, the need for compact, efficient power management components has surged. Multi-layer power inductors, known for their high power density and miniaturized form factors, are becoming indispensable in smartphones, wearables, and smart home devices. Their ability to maintain stable voltage regulation while occupying minimal PCB space makes them ideal for space-constrained applications. Recent product launches featuring improved inductance stability and lower DC resistance are further propelling adoption rates across these sectors.

Electrification of Automotive Systems Creating Substantial Demand

The automotive industry’s shift toward electrification represents a major growth driver, with the electric vehicle market projected to account for over 30% of new car sales by 2030. Multi-layer power inductors play a critical role in EV power systems including battery management, DC-DC converters, and onboard chargers. Their superior thermal characteristics and high-current handling capabilities make them preferred components in these demanding applications. Major automotive manufacturers are increasingly specifying these inductors for their reliability under harsh operating conditions and wide temperature ranges. Tier 1 suppliers have responded by developing specialized product lines with enhanced vibration resistance and reliability specifications tailored for automotive applications.

Advancements in 5G Infrastructure Driving High-Frequency Applications

The global rollout of 5G networks is creating new opportunities for multi-layer power inductor manufacturers. These components are essential in 5G base stations, small cells, and network equipment where they enable efficient power conversion at higher frequencies. With the 5G infrastructure market expected to grow at a CAGR of approximately 65% from 2024-2030, demand for inductors capable of operating effectively in the GHz range has surged. Recent material science breakthroughs have yielded inductors with improved high-frequency characteristics and reduced insertion losses, making them ideal for next-generation telecommunications equipment. The transition to mmWave technologies is further amplifying this demand as network operators require components that can handle increased power densities at higher frequencies.

MARKET RESTRAINTS

Raw Material Price Volatility Creating Margin Pressures

The multi-layer power inductor market faces significant challenges from fluctuating raw material costs. Ferrite powders and specialty alloys used in core manufacturing have experienced price increases of 15-20% annually since 2022 due to supply chain disruptions and geopolitical factors. These materials account for approximately 45-50% of total production costs, making manufacturers vulnerable to market fluctuations. While some companies have implemented strategic inventory management and long-term supply agreements, the inability to fully pass these cost increases to customers puts pressure on profitability. This situation is particularly acute for mid-sized manufacturers who lack the purchasing power of industry leaders.

Design Complexity Increases Time-to-Market Challenges

As application requirements become more demanding, the engineering complexity of multi-layer power inductors has increased substantially. New designs must simultaneously address conflicting demands for smaller sizes, higher currents, and better thermal performance. Each parameter change requires extensive testing and validation cycles, often extending development timelines by 30-40% compared to five years ago. This extended time-to-market creates several challenges: first-mover advantages diminish, opportunity windows for new products narrow, and R&D expenses rise disproportionately. Some manufacturers are responding by investing in advanced simulation tools and automated testing equipment, but these solutions require significant capital expenditure that may be prohibitive for smaller players.

Intense Competition from Alternative Technologies

The market faces growing competition from alternative power conversion technologies that threaten to displace traditional inductor-based solutions. Switching power supplies incorporating GaN and SiC semiconductors can achieve higher efficiencies with smaller passive component footprints. While multi-layer inductors still dominate in cost-sensitive applications, premium segments are gradually adopting these emerging technologies. Some estimates suggest hybrid solutions combining wide-bandgap semiconductors with specialized inductors could capture 15-20% of the power conversion market by 2030. This competitive pressure underscores the need for continued innovation in inductor materials and manufacturing techniques to maintain market relevance.

MARKET OPPORTUNITIES

Emerging Renewable Energy Applications Open New Growth Avenues

The expanding renewable energy sector presents significant opportunities for multi-layer power inductor manufacturers. Solar microinverters, wind turbine control systems, and energy storage solutions all require reliable power conversion components that can operate for decades in challenging environments. With global renewable energy capacity expected to grow by over 60% by 2030, demand for specialized inductors capable of handling high voltages and currents with minimal losses is increasing rapidly. Several leading manufacturers have already developed product lines specifically optimized for these applications, featuring enhanced insulation properties and improved thermal dissipation designs. The trend toward distributed energy generation further amplifies these opportunities as installations require more localized power conversion points.

Miniaturization Trend in Medical Electronics Creates Specialized Demand

Medical electronics represent a high-growth vertical where multi-layer power inductors can create substantial value. The portable medical device market, growing at approximately 8% annually, demands components that combine modest power handling with extreme reliability and miniaturization. Implantable devices, wearable monitors, and point-of-care diagnostic equipment all utilize these inductors in their power subsystems. Unlike consumer applications, medical-grade inductors command substantial price premiums due to their stringent reliability requirements and certification processes. Several manufacturers have established dedicated medical product lines with enhanced quality control and traceability features to capitalize on this opportunity while meeting the industry’s rigorous standards.

Advancements in Manufacturing Technologies Enable New Applications

Breakthroughs in additive manufacturing and advanced materials are creating opportunities to address previously inaccessible market segments. New 3D printing techniques allow for complex internal geometries that improve magnetic flux control while reducing eddy current losses. These innovations enable inductors with performance characteristics suitable for aerospace, defense, and high-performance computing applications where traditional designs fall short. The ability to create customized form factors also opens possibilities for system-in-package designs where inductors integrate directly with other components. While these technologies currently represent a small portion of overall production, they’re expected to grow significantly as manufacturing processes mature and costs decrease.

MULTI-LAYER POWER INDUCTORS MARKET TRENDS

Miniaturization and High-Power Density Drive Market Innovation

The global Multi-Layer Power Inductors market is projected to grow at a CAGR of 8.1%, reaching a valuation of US$ 2.65 billion by 2032. A key driver of this growth is the rising demand for miniaturized yet high-power-density components in modern electronics. As devices shrink in size—from smartphones to EVs—manufacturers are optimizing inductor designs to balance performance with space constraints. Innovations like thin-film deposition techniques and advanced ferrite materials have enabled inductors to achieve higher inductance values in smaller footprints, making them indispensable in compact power modules and DC-DC converters.

Other Trends

5G and IoT Adoption Accelerates Demand

The rollout of 5G infrastructure and the proliferation of IoT devices are creating unprecedented demand for efficient power management solutions. Multi-layer inductors, with their low electromagnetic interference (EMI) and high-frequency stability, are critical for 5G base stations and IoT edge devices. For instance, the average 5G small cell requires 30–40% more inductors than 4G counterparts due to increased power regulation needs. Meanwhile, IoT sensors leverage these components to optimize energy harvesting and battery life, further fueling market growth.

Automotive Electrification as a Growth Catalyst

The automotive sector is emerging as a dominant end-user, driven by the electrification of vehicles and ADAS (Advanced Driver-Assistance Systems). Modern EVs incorporate over 5,000 power inductors per vehicle for functions ranging from battery management to onboard charging. With the EV market expected to grow at a CAGR of 21.7% through 2030, manufacturers are prioritizing inductors with high-temperature resilience and AEC-Q200 compliance. Collaborations between tier-1 suppliers and inductor producers are also intensifying to meet automotive-grade reliability standards.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Product Innovation and Market Expansion Drive Competitive Intensity

The global Multi-Layer Power Inductors market exhibits moderate consolidation, with TDK Corporation, Murata Manufacturing and Taiyo Yuden collectively holding over 35% market share in 2024. These Japanese electronics giants maintain dominance through their vertically integrated production capabilities and continuous innovation in miniaturized power solutions. TDK alone commands approximately 14% revenue share, owing to its proprietary NanoCrystalline and Ferrite core technologies.

While established players lead the high-frequency and automotive-grade segments, Chinese manufacturers like Sunlord Electronics and Fenghua Advanced Technology are gaining traction in consumer electronics applications. Their competitive pricing strategies – sometimes 20-30% lower than Japanese counterparts – coupled with improving technical specifications are enabling significant inroads into mid-range power applications.

The competitive dynamics are further intensified by recent capacity expansions across Southeast Asia. Both Murata and TDK have inaugurated new production facilities in Malaysia and Philippines respectively during 2023-2024, aiming to reduce manufacturing lead times for global OEM clients. Meanwhile, Taiwan-based Chilisin Electronics has allocated $50 million towards automated production lines to enhance its high-current inductor capabilities.

Notable technological differentiators include Murata’s LQM series achieving 50% smaller footprint compared to conventional designs, and Vishay’s IHLP technology delivering 30% lower DC resistance. Such innovations are becoming critical as automotive and 5G infrastructure applications demand higher power densities with thermal stability up to 150°C operation.

List of Key Multi-Layer Power Inductor Manufacturers Profiled

- TDK Corporation (Japan)

- Murata Manufacturing Co., Ltd. (Japan)

- Sunlord Electronics (China)

- Vishay Intertechnology, Inc. (U.S.)

- Taiyo Yuden Co., Ltd. (Japan)

- Chilisin Electronics (Taiwan)

- Fenghua Advanced Technology (China)

- Kyocera AVX Components Corporation (Japan)

- INPAQ Technology Co., Ltd. (Taiwan)

Segment Analysis:

By Type

Ferrite Material Segment Leads the Market Due to Wide Adoption in High-Frequency Applications

The market is segmented based on type into:

- Magnetic Metal Material

- Ferrite Material

- Subtypes: MnZn ferrite, NiZn ferrite, and others

- Ceramic Material

- Others

By Application

Automotive Electronics Segment Shows Strong Growth Driven by EV Adoption

The market is segmented based on application into:

- Information Technology Equipments

- Telecommunications

- Radar Detectors

- Automotive Electronics

- Subtypes: EV powertrain, ADAS, infotainment systems

- Keyless Remote Systems

- Others

By End User

Consumer Electronics Remain Dominant Due to Proliferation of Smart Devices

The market is segmented based on end user into:

- Consumer Electronics

- Subtypes: Smartphones, wearables, home appliances

- Automotive

- Industrial

- Telecom Infrastructure

- Others

Regional Analysis: Multi-Layer Power Inductors Market

North America

North America remains a critical market for multi-layer power inductors, driven by advanced electronics manufacturing and robust demand from key sectors like automotive, telecommunications, and IT. The region’s strong emphasis on miniaturization and power efficiency has led to significant adoption of high-performance inductors, particularly in 5G infrastructure, electric vehicles (EVs), and IoT devices. The U.S. accounts for over 60% of the regional market, supported by substantial R&D investments by companies like TDK and Vishay. Strict electromagnetic compatibility (EMC) regulations further reinforce the need for superior inductor technologies.

Europe

Europe’s market is shaped by stringent EU environmental directives and a thriving industrial automation sector. Germany, the largest consumer, leads in automotive electronics, with inductor demand surging for EVs and advanced driver-assistance systems (ADAS). Meanwhile, France and the U.K. are prioritizing renewable energy applications, boosting demand for inductors in power conversion systems. European manufacturers like Murata and Würth Elektronik are focusing on high-reliability, low-loss materials, aligning with the region’s sustainability goals. However, supply chain disruptions and material shortages post-2022 have posed challenges.

Asia-Pacific

Asia-Pacific dominates the global market, contributing over 50% of revenue in 2024, fueled by China, Japan, and South Korea. China’s booming consumer electronics and EV sectors drive demand, while Japan’s expertise in ferrite-based inductors keeps it competitive. India’s market is rising due to local manufacturing incentives (e.g., PLI schemes) and telecom infrastructure expansion. The region benefits from cost-competitive production but faces pricing pressure due to local players like Sunlord Electronics. Automation and 5G rollouts will sustain long-term growth, though tariff disputes risk supply stability.

South America

South America’s market is nascent but growing, with Brazil leading in automotive and industrial applications. However, economic volatility and limited R&D investments hinder adoption of advanced inductor technologies. Local manufacturers rely on imports for high-end components, though lower labor costs attract assembly operations. The renewable energy sector, particularly solar power, offers niche opportunities. Infrastructure constraints and currency fluctuations remain barriers, but trade agreements could improve access to global supply chains.

Middle East & Africa

The MEA market is emerging, with growth concentrated in the UAE, Saudi Arabia, and Turkey. Telecom expansions and smart city projects (e.g., Saudi Vision 2030) are driving demand for power management solutions. However, reliance on imports and low local production capacity limit market expansion. South Africa’s automotive sector presents incremental opportunities. While geopolitical risks and underdeveloped electronics ecosystems slow progress, partnerships with Asian suppliers could accelerate market development in the long term.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Multi-Layer Power Inductors market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Multi-Layer Power Inductors market was valued at USD 1,553 million in 2024 and is projected to reach USD 2,647 million by 2032, growing at a CAGR of 8.1%.

- Segmentation Analysis: Detailed breakdown by product type (Magnetic Metal Material, Ferrite Material, Ceramic Material, Others), technology, application (Information Technology Equipments, Telecommunications, Automotive Electronics, etc.), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. Asia-Pacific currently dominates with over 45% market share due to strong electronics manufacturing presence.

- Competitive Landscape: Profiles of leading players including TDK, Murata, Sunlord Electronics, Vishay, and Taiyo Yuden, covering their product portfolios, R&D investments, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging inductor technologies, miniaturization trends, and integration with power management solutions for 5G, IoT, and automotive applications.

- Market Drivers & Restraints: Analysis of growth drivers like rising demand for compact power solutions in EVs and 5G devices, along with challenges like raw material price volatility.

- Stakeholder Analysis: Strategic insights for component manufacturers, OEMs, and investors regarding emerging opportunities in high-growth application segments.

The research methodology combines primary interviews with industry experts and analysis of verified market data from authoritative sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Multi-Layer Power Inductors Market?

-> Multi-Layer Power Inductors market was valued at 1553 million in 2024 and is projected to reach US$ 2647 million by 2032, at a CAGR of 8.1% during the forecast period.

Which key companies operate in Global Multi-Layer Power Inductors Market?

-> Key players include TDK, Murata, Sunlord Electronics, Vishay, Taiyo Yuden, Kyocera, and Chilisin Electronics, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand from 5G infrastructure, electric vehicles, and consumer electronics miniaturization trends.

Which region dominates the market?

-> Asia-Pacific dominates the market, accounting for over 45% share, driven by electronics manufacturing hubs in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include development of high-frequency inductors for 5G, integration with advanced power modules, and adoption of new magnetic materials.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...