MARKET INSIGHTS

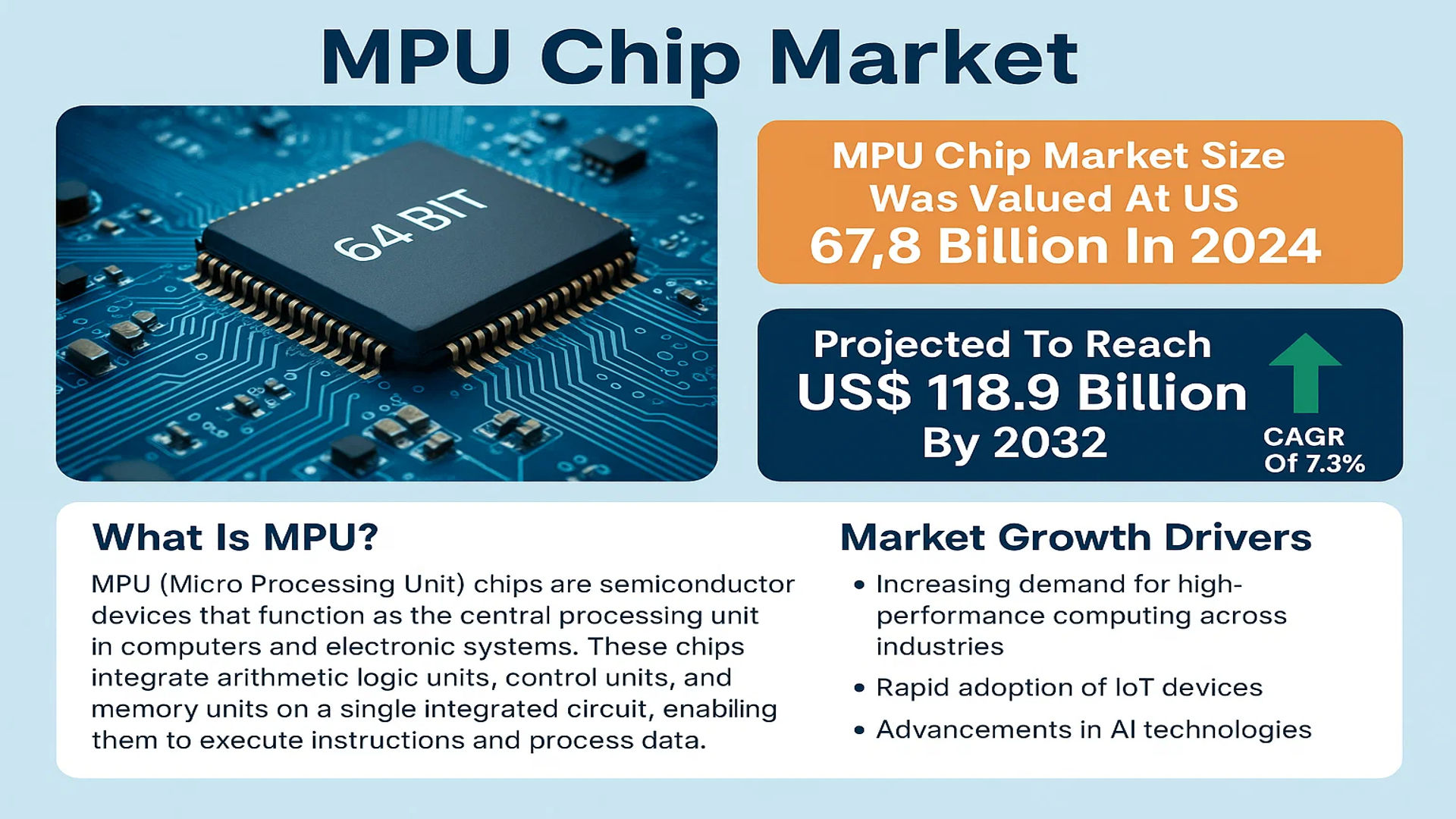

The global MPU Chip Market size was valued at US$ 67.8 billion in 2024 and is projected to reach US$ 118.9 billion by 2032, at a CAGR of 7.3% during the forecast period 2025-2032.

MPU (Micro Processing Unit) chips are semiconductor devices that function as the central processing unit in computers and electronic systems. These chips integrate arithmetic logic units, control units, and memory units on a single integrated circuit, enabling them to execute instructions and process data. Modern MPUs are categorized by their architecture (8-bit, 32-bit, 64-bit) with 64-bit processors dominating high-performance computing applications.

The market growth is driven by increasing demand for high-performance computing across industries, rapid adoption of IoT devices, and advancements in AI technologies. However, supply chain disruptions and geopolitical tensions have created volatility in semiconductor supply. The Asia-Pacific region remains the dominant market, accounting for over 60% of global MPU production, with major fabs located in Taiwan, South Korea, and China. Key players including Intel, AMD, and Qualcomm continue to invest heavily in R&D to develop more efficient and powerful chips, particularly for AI and edge computing applications.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for AI and IoT Applications Fueling MPU Chip Market Expansion

The global MPU chip market is experiencing robust growth driven by the rapid adoption of artificial intelligence (AI) and Internet of Things (IoT) technologies across industries. With AI applications requiring increasingly powerful processing capabilities, MPU chips have become critical components in edge computing devices, smart appliances, and industrial automation systems. The AI chip market, which depends heavily on advanced MPU technologies, is projected to maintain double-digit growth through 2032, creating sustained demand for high-performance processing solutions. Leading manufacturers are responding with innovations like neuromorphic computing architectures that blur the traditional boundaries between MPUs and specialized AI accelerators.

Automotive Digital Transformation Accelerating MPU Adoption

Modern vehicles are transforming into sophisticated computing platforms, with advanced driver-assistance systems (ADAS), digital cockpits, and vehicle-to-everything (V2X) communication driving unprecedented demand for automotive-grade MPUs. The average premium vehicle now contains over 100 million lines of code—more than a fighter jet—requiring powerful processing capabilities. This technological arms race in automotive electronics has created fierce competition among semiconductor manufacturers to develop MPUs that meet stringent automotive safety standards while delivering superior performance. The trend toward centralized vehicle architectures and software-defined vehicles will continue pushing MPU requirements to new levels through the decade.

➤ With electric vehicle sales projected to account for over 30% of global car sales by 2030, the demand for high-performance automotive MPUs shows no signs of slowing down.

Beyond automotive applications, the 5G revolution continues to create new opportunities for MPU adoption. Both network infrastructure equipment and 5G-enabled devices require advanced processing capabilities to handle increased data throughput and low-latency requirements. This technological transition is pushing MPU manufacturers to innovate in areas like heterogeneous computing and advanced packaging technologies.

MARKET RESTRAINTS

Semiconductor Supply Chain Disruptions Creating Market Volatility

While demand for MPU chips remains strong, the market faces significant constraints from ongoing supply chain challenges. The global semiconductor industry continues grappling with material shortages, manufacturing capacity constraints, and geopolitical tensions affecting supply reliability. These disruptions have led to extended lead times and allocation challenges across the MPU market, particularly for automotive and industrial applications. The concentration of advanced semiconductor manufacturing in specific geographic regions creates systemic vulnerabilities that could impact market stability through the mid-term.

Other Key Restraints

Design Complexity and Rising Development Costs

Developing cutting-edge MPU designs has become increasingly capital-intensive, with state-of-the-art 5nm and below process nodes requiring multi-billion dollar investments. This rising barrier to entry has accelerated industry consolidation and made it increasingly difficult for smaller players to compete in the high-performance MPU segment. The growing complexity of chip designs also extends development cycles, creating challenges in meeting rapidly evolving market demands.

Thermal and Power Constraints

As MPU performance continues scaling upward, power consumption and thermal management have emerged as critical limiting factors. These constraints are particularly acute in mobile and edge computing applications where battery life and form factor considerations impose strict power budgets. While architectural innovations like chiplet designs and advanced power management techniques help mitigate these challenges, they remain a fundamental restraint on performance scaling.

MARKET CHALLENGES

Intensifying Competition and Market Saturation in Consumer Segments

The MPU market faces growing challenges from increasing competition and slowing demand growth in traditional consumer segments. The smartphone market, historically a major driver of MPU innovation, has entered a period of maturity with lengthening replacement cycles and declining shipment volumes. This has forced MPU manufacturers to diversify into higher-growth segments while simultaneously facing intensified price competition in established markets. The situation is further complicated by the emergence of competitive ARM-based architectures challenging the traditional x86 dominance in PC and server markets.

Workforce and Skills Shortages

The semiconductor industry is experiencing acute shortages of qualified engineering talent capable of designing next-generation MPU architectures. This skills gap has become a critical bottleneck, particularly for companies pursuing cutting-edge process technologies and architectural innovations. With experienced semiconductor professionals retiring and educational pipelines struggling to keep pace with industry demands, the talent shortage could potentially slow the pace of MPU innovation over the coming decade unless addressed effectively.

Intellectual Property and Geopolitical Risks

Growing technology nationalism and export controls have introduced new complexities to the global MPU ecosystem. Restrictions on technology transfer, concerns about supply chain security, and the potential for market fragmentation along geopolitical lines present significant challenges for multinational semiconductor companies. These dynamics require MPU manufacturers to develop more resilient and regionally balanced strategies while navigating an increasingly complex regulatory environment.

MARKET OPPORTUNITIES

Emerging Applications in Edge AI and TinyML Creating New Growth Frontiers

The rapid evolution of edge AI and Tiny Machine Learning (TinyML) applications represents one of the most promising opportunities for MPU market expansion. As AI inference moves closer to the data source, demand grows for power-efficient MPUs capable of running sophisticated algorithms at the edge. This trend is creating opportunities across diverse applications—from smart sensors and wearables to industrial predictive maintenance systems. Leading MPU manufacturers are responding with products that combine traditional processing capabilities with specialized AI acceleration in compact, low-power packages.

Chiplet Revolution Opening New Design Possibilities

The semiconductor industry’s shift toward chiplet-based architectures presents transformative opportunities for MPU design innovation. By enabling the mixing and matching of different processing elements built on optimized process nodes, chiplet approaches allow MPU designers to overcome traditional scaling limitations. This modular design paradigm not only improves performance and power efficiency but also reduces development risks and costs. As chiplet interoperability standards mature and advanced packaging technologies improve, we expect to see accelerated innovation in MPU architectures leveraging this approach.

The growing emphasis on digital transformation across industries—from manufacturing and healthcare to agriculture and smart cities—continues to create new avenues for MPU adoption. As businesses increasingly rely on data-driven decision making and automation, the demand for reliable, high-performance processing solutions will continue expanding beyond traditional computing markets into diverse industrial and commercial applications.

MPU CHIP MARKET TRENDS

Shift Towards AI and Edge Computing Driving Demand for High-Performance MPUs

The increasing adoption of artificial intelligence (AI) and edge computing applications is accelerating demand for higher-performance microprocessing units (MPUs). As workloads shift toward AI-driven analytics and real-time processing, semiconductor manufacturers are prioritizing MPU designs optimized for machine learning and low-latency computations. The need for faster data processing at the edge of networks, particularly in autonomous vehicles, IoT devices, and smart infrastructure, is pushing chipmakers to enhance power efficiency and computational throughput. With edge computing expected to account for over 75% of enterprise-generated data processing by 2025, MPU innovations are critical in meeting these evolving demands. Leading manufacturers such as Intel and AMD have already introduced processors with dedicated AI accelerators, reinforcing this market shift.

Other Trends

Automotive Industry Adoption of Advanced MPUs

The automotive sector is emerging as a key growth driver for the MPU market, particularly with the rise of electric vehicles (EVs) and advanced driver-assistance systems (ADAS). Modern vehicles increasingly rely on high-performance MPUs to manage complex functions like autonomous driving, battery management, and infotainment systems. The automotive MPU segment is projected to grow at a double-digit CAGR over the next five years, fueled by stringent safety regulations and consumer demand for connected car technologies. Semiconductor suppliers are actively developing ruggedized MPUs capable of withstanding automotive environments while delivering the processing power required for next-gen vehicular applications.

Supply Chain Stabilization and Capacity Expansion

After recent semiconductor shortages caused widespread disruptions, MPU manufacturers are now focusing on supply chain diversification and capacity expansion. Major foundries have announced substantial investments in new fabrication facilities, with over $200 billion pledged globally for semiconductor manufacturing expansion through 2025. This includes significant capacity increases for advanced MPU production nodes. While the industry has largely recovered from pandemic-related supply constraints, the emphasis remains on building resilience through geographical diversification and strategic inventory management. The transition to more localized production in North America and Europe, supported by government incentives like the U.S. CHIPS Act, is creating a more balanced global supply landscape for critical MPU components.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Market Expansion Drive Competition in the MPU Chip Segment

The global MPU Chip market is characterized by intense competition, with dominant players leveraging their technological expertise and extensive distribution networks to maintain market leadership. While the semiconductor industry faced macroeconomic headwinds in 2022 with growth slowing to 4.4%, the MPU segment remains critical for computing applications across consumer electronics, automotive, and industrial sectors.

Intel Corporation continues to lead the market with its x86 architecture maintaining over 60% unit share in PC and server processors. However, the company faces growing pressure from AMD, whose innovative chiplet-based designs and TSMC manufacturing partnership helped capture 30% market share in desktops by Q4 2023. Meanwhile, ARM-based processors from Qualcomm and MediaTek are gaining traction in mobile and emerging IoT applications due to their power efficiency advantages.

The competitive dynamics are further shaped by regional specialization. Samsung Electronics and HiSilicon dominate smartphone applications in Asia-Pacific markets, while European players like STMicroelectronics and NXP Semiconductors maintain strong positions in automotive MPUs. The latter two companies jointly controlled 45% of the automotive MPU market in 2023, according to recent industry reports.

Strategic investments in next-generation technologies are reshaping the competitive landscape. Several players are racing to develop chips using advanced 3nm and 5nm process nodes, with Intel and TSMC committing over $40 billion collectively to new fabrication facilities in Arizona and Taiwan. Furthermore, the rising demand for AI-optimized processors has led companies like AMD and Qualcomm to acquire specialized AI chip startups to enhance their offerings.

List of Key MPU Chip Companies Profiled

- Intel Corporation (U.S.)

- Advanced Micro Devices (AMD) (U.S.)

- STMicroelectronics (Switzerland)

- Samsung Electronics (South Korea)

- Qualcomm Incorporated (U.S.)

- MediaTek Inc. (Taiwan)

- Microchip Technology Incorporated (U.S.)

- TDK Corporation (Japan)

- UNISOC (China)

- HiSilicon (China)

- NXP Semiconductors (Netherlands)

Segment Analysis:

By Type

64-bit MPU Chips Dominate the Market Due to High Performance in Computing-Intensive Applications

The market is segmented based on type into:

- 8-bit

- 32-bit

- 64-bit

By Application

3C Products Segment Leads Due to Rising Demand for Consumer Electronics and Smart Devices

The market is segmented based on application into:

- 3C Product (Computer, Communication, Consumer Electronics)

- Automobile

- Industrial

- Aerospace & Defense

- Others

By Architecture

ARM Architecture Gains Significant Traction in Mobile and Embedded Systems

The market is segmented based on architecture into:

- x86

- ARM

- RISC-V

- MIPS

- Others

By Power Consumption

Low-Power MPUs Witness Growing Adoption in IoT and Portable Devices

The market is segmented based on power consumption into:

- High Performance

- Low Power

- Ultra-Low Power

Regional Analysis: MPU Chip Market

Asia-Pacific

The Asia-Pacific region dominates the MPU chip market, accounting for the largest revenue share due to rapid technological advancements and strong demand from key economies like China, Japan, and South Korea. China remains the epicenter of semiconductor manufacturing, driving significant demand for MPUs across consumer electronics, automotive, and industrial applications. Moreover, initiatives such as China’s “Made in China 2025” policy bolster domestic semiconductor production, reducing reliance on imports. Japan and South Korea, home to global tech giants like Samsung and Toshiba, continue to lead in high-performance MPU development, particularly for 64-bit processors. However, supply chain disruptions and geopolitical tensions pose challenges to sustained market expansion in the region.

North America

North America holds a prominent position in the MPU chip market, primarily driven by the U.S., home to industry leaders like Intel and AMD. The region benefits from advanced R&D capabilities, high demand for data-heavy applications, and strong adoption of AI-driven computing solutions. The automotive sector’s increasing reliance on MPUs for electric vehicles (EVs) and autonomous driving further fuels market growth. Additionally, government incentives, such as the CHIPS and Science Act, aim to strengthen domestic semiconductor manufacturing, countering supply chain vulnerabilities. However, high production costs and stiff competition from Asia-based manufacturers remain significant challenges.

Europe

Europe’s MPU chip market is characterized by steady growth, supported by strong demand from the automotive and industrial sectors, particularly in Germany, France, and the U.K. The EU’s Digital Decade strategy emphasizes semiconductor self-sufficiency, fostering investments in local chip manufacturing. Companies like STMicroelectronics and NXP Semiconductors lead innovation in low-power and embedded MPUs, catering to IoT and smart devices. However, the region faces hurdles such as fragmented regulatory policies and heavy reliance on imports, limiting its ability to compete at scale with Asia and North America.

South America

South America’s MPU chip market is emerging, with Brazil and Argentina showing rising demand due to expanding digital infrastructure and consumer electronics adoption. However, economic instability, limited local manufacturing capabilities, and import dependency hinder market expansion. Despite these challenges, the region presents long-term opportunities, particularly in automotive and telecommunications applications, provided foreign investment and policy support improve semiconductor supply chain resilience.

Middle East & Africa

The Middle East & Africa region shows promising but nascent growth in MPU chip adoption, led by nations like the UAE, Saudi Arabia, and Israel. Increasing digitization, smart city initiatives, and government-backed technology investments drive demand. However, lack of local semiconductor production and weak R&D infrastructure slow market development. Strategic partnerships with global chip manufacturers could unlock potential, especially for telecom and defense applications, though macroeconomic uncertainties remain a constraint.

Report Scope

This market research report provides a comprehensive analysis of the Global MPU Chip Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (8-bit, 32-bit, 64-bit), application (3C Product, Automobile, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global MPU Chip Market?

-> MPU Chip market size was valued at US$ 67.8 billion in 2024 and is projected to reach US$ 118.9 billion by 2032, at a CAGR of 7.3% during the forecast period 2025-2032.

Which key companies operate in Global MPU Chip Market?

-> Key players include Intel, AMD, STMicroelectronics, Samsung, Qualcomm, MediaTek, Microchip Technology Incorporated, TDK, UNISOC, HiSilicon, and NXP, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for high-performance computing, growth in AI/ML applications, expansion of IoT devices, and advancements in automotive electronics.

Which region dominates the market?

-> Asia-Pacific is the largest market for MPU chips, accounting for 48% of global revenue in 2024, while North America leads in innovation and high-end MPU development.

What are the emerging trends?

-> Emerging trends include chiplet-based designs, RISC-V architecture adoption, advanced packaging technologies, and energy-efficient processor development.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...