MARKET INSIGHTS

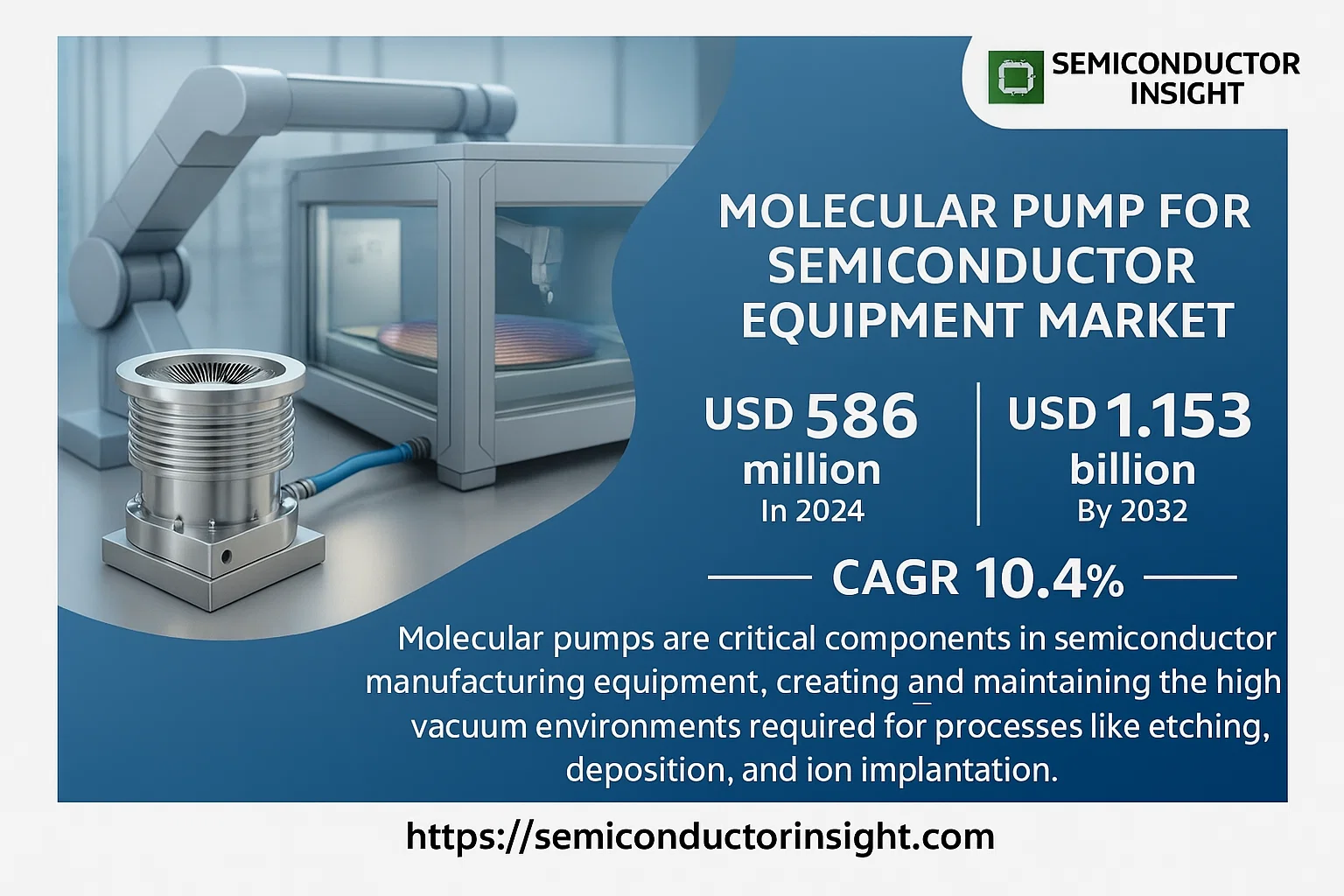

Global Molecular Pump for Semiconductor Equipment Market was valued at USD 586 million in 2024 and is projected to reach USD 1.153 billion by 2032, exhibiting a CAGR of 10.4% during the forecast period.

Molecular pumps are critical components in semiconductor manufacturing equipment, creating and maintaining the high vacuum environments required for processes like etching, deposition, and ion implantation. They operate by transferring momentum to gas molecules through high-speed rotation, effectively “sweeping” them towards the exhaust port. The market’s robust growth is primarily driven by the exponential expansion of the global semiconductor industry itself, fueled by demand for advanced electronics, artificial intelligence, and the Internet of Things (IoT). This, in turn, fuels demand for the manufacturing equipment that relies on these vacuum pumps.

Furthermore, the push towards more advanced process nodes below 10nm, and the increasing adoption of EUV lithography, requires even more precise vacuum control, further propelling the market. The market is also benefiting from significant government investments and initiatives aimed at establishing domestic semiconductor supply chains, particularly in the United States, Europe, and across Asia. While the market is global, the Asia-Pacific region, led by China, Taiwan, South Korea, and Japan, represents the largest consumer, holding over 70% of the market share, due to its concentration of semiconductor fabrication plants (fabs) and assembly facilities.

Key players in the market include Atlas Copco, Shimadzu Co., Ltd., Osaka Vacuum, Ltd., Agilent Technologies, Inc., Pfeiffer Vacuum GmbH, and Beijing Sihai Xiangyun Fluid Technology, among others.

MARKET DRIVERS

Expansion of Semiconductor Manufacturing Capacity

The global push for semiconductor self-sufficiency and the establishment of new fabrication plants, particularly in North America and Asia-Pacific, is a primary driver. Governments are investing heavily in domestic chip production, which directly fuels demand for advanced vacuum solutions like molecular pumps that are essential for processes such as etching, deposition, and ion implantation. The ongoing construction of new fabs requires a significant number of pumps per facility, creating sustained market growth.

Demand for Advanced Process Nodes

The transition to more advanced semiconductor process nodes below 10nm and the rise of 3D NAND and GAAFET technologies necessitate ultra-high vacuum (UHV) and high-purity environments. Molecular pumps are critical for achieving and maintaining the clean, particle-free vacuum levels required. As chipmakers pursue smaller features and complex 3D structures, the performance requirements for vacuum pumps intensify, driving the adoption of more sophisticated and reliable molecular drag pumps.

➤ The market for molecular pumps is projected to grow at a CAGR of approximately 6-8% over the next five years, largely driven by capital expenditure in leading-edge logic and memory fabs.

Furthermore, the increased adoption of compound semiconductors (e.g., GaN, SiC) for power electronics and electric vehicles represents another significant driver. The manufacturing of these materials often requires specialized vacuum processes where molecular pumps are indispensable.

MARKET CHALLENGES

High Initial and Operational Costs

Molecular pumps represent a significant capital investment for semiconductor equipment manufacturers and fabrication plants. Beyond the high acquisition cost, operational expenses related to maintenance, power consumption, and potential downtime for repairs can be substantial. For smaller foundries or research facilities, these costs can be a major barrier to entry or upgrading to the latest pump technologies.

Other Challenges

Technical Complexity and Contamination Risks

The extreme precision required in semiconductor manufacturing means that any failure or contamination from a molecular pump can lead to catastrophic yield loss. Particles generated by bearing wear or lubricants can ruin entire batches of wafers. This risk necessitates rigorous quality control, complex monitoring systems, and highly skilled personnel for maintenance, adding layers of operational complexity and cost.

Intense Competition and Price Pressure

The market is dominated by a few key global players, but competition remains fierce. This, combined with the cyclical nature of semiconductor capital spending, puts constant pressure on manufacturers to reduce prices while simultaneously investing in R&D for next-generation products with higher pumping speeds and better reliability.

MARKET RESTRAINTS

Cyclical Nature of the Semiconductor Industry

The molecular pump market is inherently tied to the capital expenditure cycles of the semiconductor industry. During downturns, chipmakers delay or cancel new equipment purchases, directly impacting the demand for molecular pumps. This cyclicality makes long-term planning and consistent revenue streams challenging for pump manufacturers, as seen during periods of inventory correction and reduced fab utilization.

Technological Maturation and Long Lifespan

High-quality molecular pumps are designed for durability and can have operational lifespans of several years. While this is a benefit for end-users, it acts as a market restraint by extending the replacement cycle. The pace of innovation, while steady, does not always necessitate a full pump replacement, as upgrades or refurbishments can often extend the service life of existing equipment, thereby tempering new unit sales.

MARKET OPPORTUNITIES

Growth in Specialty Applications

Beyond traditional logic and memory fabs, significant opportunities exist in the manufacturing of MEMS, sensors, and photonic devices. These applications often require vacuum processes and are experiencing rapid growth due to trends in IoT, automotive, and healthcare. Molecular pump suppliers can target these emerging segments with tailored solutions.

Development of Dry and Magnetic Levitation Pumps

The shift towards dry vacuum technology and magnetically levitated (maglev) molecular pumps presents a major opportunity. These pumps eliminate the risk of oil contamination, reduce maintenance needs, and offer higher reliability. As the industry’s purity standards become more stringent, the demand for these advanced, clean pumping solutions is expected to accelerate significantly.

Integration with Industry 4.0 and Predictive Maintenance

The integration of IoT sensors and data analytics for predictive maintenance is a key opportunity. Smart molecular pumps that can monitor their own health, predict failures before they occur, and optimize performance remotely can provide immense value by reducing unplanned downtime in high-cost semiconductor fabrication environments, creating a new revenue stream through service-based models.

Molecular Pump for Semiconductor Equipment Market Trends

Strong Market Growth Driven by Semiconductor Demand

The global Molecular Pump for Semiconductor Equipment market is on a robust growth trajectory, reflecting the broader expansion of the semiconductor industry. The market was valued at 586 million in 2024 and is projected to reach US$ 1153 million by 2032, exhibiting a compound annual growth rate (CAGR) of 10.4% during the forecast period. This significant growth is propelled by the increasing demand for advanced semiconductor devices, which require sophisticated fabrication processes like deposition and etching, processes that heavily rely on high and ultra-high vacuum environments provided by molecular pumps. The push for smaller, more powerful chips necessitates cleaner and more stable vacuum conditions, directly fueling demand for these critical components.

Other Trends

Dominance of Asia-Pacific Region

A defining trend in the market is the overwhelming concentration of demand and manufacturing in the Asia-Pacific region. This region accounts for approximately 70% of the global Molecular Pump for Semiconductor Equipment market. The dominance is primarily driven by the presence of major semiconductor fabrication plants (fabs) and the world’s leading semiconductor manufacturers in countries such as China, Taiwan, South Korea, and Japan. As these countries continue to invest heavily in expanding their semiconductor production capacities to secure supply chains and meet global demand, the need for associated equipment, including molecular pumps, remains exceptionally high.

Market Consolidation and Leading Players

The competitive landscape is characterized by a high degree of consolidation, with the top two companies, Atlas Copco and Shimadzu Co., Ltd., collectively holding about 50% of the total market share. This concentration of market power underscores the importance of technological expertise, extensive product portfolios, and strong global service and support networks. These leading players compete on factors including pump reliability, energy efficiency, maintenance intervals, and the ability to meet the stringent contamination control requirements of next-generation semiconductor manufacturing processes.

Segmentation by Technology and Application

Market segmentation reveals key insights into technology adoption. Molecular pumps are categorized primarily by their bearing technology, including Magnetic Levitation, Oil Lubricated, and Grease Lubricated types. Each type caters to specific requirements concerning vibration, contamination risk, and maintenance. In terms of application, molecular pumps are critical in various semiconductor tools. The major application segments include Deposition systems (such as CVD, PVD, ALD), Lithography Machines, Etching Machines, and Ion Implantation equipment. The continuous advancements in these semiconductor manufacturing processes directly influence the performance specifications and demand for molecular pumps.

COMPETITIVE LANDSCAPE

Key Industry Players

Dominant Duo Holds Half the Market, Niche Innovators Drive Specialization

The global Molecular Pump for Semiconductor Equipment market exhibits a concentrated competitive structure, dominated by two major players, Atlas Copco and Shimadzu Co., Ltd., which collectively command approximately 50% of the total market share. These industry leaders leverage extensive R&D capabilities, global service networks, and long-standing relationships with major semiconductor equipment manufacturers to maintain their stronghold. Their product portfolios are comprehensive, covering various pump types like magnetic levitation, oil-lubricated, and grease-lubricated models essential for critical semiconductor fabrication processes including deposition, etching, and ion implantation. The market’s geographic concentration in the Asia-Pacific region, which accounts for about 70% of global demand, further solidifies the position of established players with a strong regional presence and manufacturing footprint.

Beyond the top tier, the market includes several other significant players who compete by focusing on technological innovation, cost-effectiveness, and specialization in niche application areas. Companies such as Pfeiffer Vacuum GmbH, ULVAC, and EBARA CORPORATION have carved out substantial market positions with their advanced vacuum technology expertise. A growing number of specialized manufacturers, particularly from China, including Beijing Sihai Xiangyun Fluid Technology and Shanghai Canter Vacuum Technology, are increasingly influential, offering competitive products and capturing market share. These companies often compete by providing tailored solutions for specific process requirements, regional support, and aggressive pricing strategies, contributing to a dynamic and evolving competitive environment.

List of Key Molecular Pump for Semiconductor Equipment Companies Profiled

- Atlas Copco

- Shimadzu Co., Ltd

- Osaka Vacuum, Ltd

- Agilent Technologies, Inc

- Pfeiffer Vacuum GmbH

- Beijing Sihai Xiangyun Fluid Technology

- Shanghai Canter Vacuum Technology

- Beijing Zhongke Instrument

- ULVAC

- Tianjin Feixuan Technology

- Zhongke Jiuwei Technology Co., Ltd.

- EBARA CORPORATION

- BUSCH

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Magnetic Levitation Molecular Pump are the most dominant technology in the semiconductor equipment space due to their superior performance characteristics. Their primary advantage lies in the complete absence of mechanical contact and oil contamination, which is absolutely critical for maintaining the ultra-high vacuum purity required in modern semiconductor fabrication processes such as extreme ultraviolet lithography. This contamination-free operation directly translates to higher process yields and superior device performance. Furthermore, this technology offers significantly lower vibration and noise levels, along with enhanced reliability and longer maintenance intervals, which are vital for minimizing downtime in high-cost semiconductor manufacturing facilities. The demand for these high-performance pumps is consistently strong, driven by the ongoing technological advancements and the increasing complexity of semiconductor nodes. |

| By Application |

|

Deposition equipment, encompassing critical processes like Chemical Vapor Deposition (CVD), Physical Vapor Deposition (PVD), and Atomic Layer Deposition (ALD), represents the most significant application segment. These processes are fundamental for building the intricate layers of thin films on silicon wafers and demand extremely stable and clean vacuum environments to ensure film uniformity, purity, and precise thickness control. The aggressive growth in 3D NAND flash memory and advanced logic chips, which require a multitude of deposition steps, is a major driver for this segment. Molecular pumps are indispensable in these tools for achieving the necessary vacuum levels and ensuring that no contaminants compromise the delicate film structures, making their performance a key determinant of the overall process capability and final chip quality. |

| By End User |

|

Semiconductor Foundries are the primary and most influential end-users, particularly large-scale pure-play foundries and major memory manufacturers. Their dominance is driven by massive capital expenditures dedicated to building and expanding state-of-the-art fabrication facilities for leading-edge nodes. These facilities operate 24/7 and require a vast number of highly reliable molecular pumps across hundreds of toolsets. The relentless push for miniaturization and increased wafer throughput places immense pressure on equipment uptime and performance, making the reliability and service support for molecular pumps a critical operational consideration. Foundries maintain stringent qualification processes for pump suppliers, prioritizing long-term reliability, low cost of ownership, and superior technical support over initial purchase price. |

| By Technology Node |

|

Advanced Nodes represent the most demanding and high-growth segment, driving the adoption of the latest molecular pump technologies. Manufacturing at nodes below 10nm, such as 7nm, 5nm, and 3nm, requires unprecedented levels of vacuum purity and stability to prevent defects that can ruin complex, multi-billion-transistor chips. Processes like EUV lithography are particularly sensitive and necessitate molecular pumps with exceptional performance to handle hydrogen gas and maintain a pristine environment. The technical specifications for pumps used in these fabs are the most rigorous, focusing on ultra-low contamination, vibration control, and energy efficiency. This segment is characterized by collaboration between pump manufacturers and semiconductor leaders to co-develop next-generation pump solutions. |

| By Pumping Speed |

|

High Speed molecular pumps are the leading category, essential for meeting the throughput requirements of modern semiconductor manufacturing. Larger wafer sizes and the need to minimize pump-down times in process chambers to maximize tool utilization are key factors driving demand for pumps with high volumetric pumping speeds. These pumps are critical for applications with high gas loads, such as certain deposition and etching processes, where they ensure rapid evacuation and stable process pressure. The ability to handle these demanding conditions without sacrificing vacuum integrity is a significant competitive advantage. This segment sees continuous innovation aimed at increasing pumping speeds while maintaining or improving reliability and energy efficiency, directly impacting overall fab productivity. |

Regional Analysis: Molecular Pump for Semiconductor Equipment Market

These two sub-regions are the core of advanced semiconductor manufacturing. Taiwan, led by foundry giant TSMC, and South Korea, dominated by Samsung and SK Hynix, are at the forefront of developing sub-5nm process technologies. Their aggressive capital expenditure on new fabs for leading-edge logic and high-bandwidth memory creates the most stringent requirements for vacuum integrity, driving demand for the most advanced, high-throughput, and reliable turbo-molecular and hybrid pump systems to maintain the critical ultra-high vacuum environments essential for atomic-level deposition and etching processes.

Japan remains a critical player with its deep-rooted expertise in precision engineering and dominance in key semiconductor materials and components. Japanese companies like Ebara, a major player in vacuum pump manufacturing, supply high-reliability pumps to fabs globally. The market is supported by strong domestic chipmakers and equipment suppliers, with demand driven by investments in specialized semiconductors, including power devices and image sensors, which require highly stable and clean vacuum processes. Japan’s focus on quality and reliability aligns perfectly with the long-lifecycle requirements of semiconductor tools.

China represents the most dynamic and fast-growing market, fueled by a national strategy to achieve semiconductor self-sufficiency. Massive government-backed investments are leading to the construction of numerous new fabs. While initially trailing in leading-edge technology, this expansion drives enormous demand for molecular pumps across a wide range of process nodes. A strong parallel drive to localize the supply chain is creating opportunities for domestic vacuum pump manufacturers, though international suppliers still play a crucial role in providing high-end technology for the most advanced production lines being developed.

Countries like Singapore, Malaysia, and Vietnam are growing in importance as hubs for semiconductor assembly, testing, and packaging (ATP), as well as for more mature node fabrication. While the vacuum requirements for ATP are less extreme than for front-end processes, they still necessitate reliable vacuum solutions. The region benefits from the diversification of the global supply chain, attracting investment and creating a steady, growing demand for durable and cost-effective molecular pumps suitable for these specific applications, supplementing the region’s overall market strength.

North America

North America, primarily the United States, holds a significant position as a center for semiconductor R&D and the home of leading semiconductor equipment manufacturers like Applied Materials and Lam Research. Demand for molecular pumps is driven by massive investments in new domestic fabrication facilities, such as those by Intel and TSMC in Arizona, aimed at bolstering the regional supply chain. These state-of-the-art fabs require the latest vacuum pump technologies. Furthermore, the region’s strong focus on research into next-generation chips, including those for AI and quantum computing, creates a specialized demand for pumps capable of supporting highly experimental and demanding processes in university and corporate research labs, ensuring a market for cutting-edge vacuum solutions.

Europe

Europe’s market is characterized by its strength in specialized semiconductor sectors rather than high-volume manufacturing. The region is a leader in research institutions like IMEC and Fraunhofer, and is home to key suppliers such as VAT Group and Pfeiffer Vacuum. Demand is driven by investments in power semiconductors, automotive chips, and micro-electromechanical systems (MEMS), which require precise and reliable vacuum conditions. Major projects like the European Chips Act aim to increase production capacity, which will spur demand. The market is defined by a need for high-quality, highly reliable pumps that offer precision control and low contamination, catering to the region’s focus on specialized, high-value semiconductor applications.

South America

The molecular pump market in South America is nascent and relatively small compared to other regions. The semiconductor industry is limited, with no major advanced fabrication facilities. Demand is primarily driven by maintenance, repair, and operations (MRO) activities for existing industrial and research equipment, as well as small-scale operations in universities and research centers. The market is characterized by replacement demand rather than new tool installations. While countries like Brazil have some industrial base, the region’s overall impact on the global molecular pump market for semiconductor equipment is minimal, with growth potential heavily dependent on future broader industrial and technological development policies.

Middle East & Africa

This region represents a minor segment of the global market. Demand is sporadic and primarily tied to specific high-tech projects, research universities, and small-scale electronics manufacturing. There are no significant semiconductor fabrication plants. Countries like Israel, with a strong technology sector, and Saudi Arabia, with its ambitious diversification plans, show potential for future growth in high-tech industries, which could eventually generate demand for semiconductor equipment and associated vacuum pumps. Currently, however, the market is characterized by very limited volume, focusing mainly on supplying pumps for research, development, and niche industrial applications rather than large-scale semiconductor production.

Report Scope

This market research report provides a comprehensive analysis of the Molecular Pump for Semiconductor Equipment Market , covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Molecular Pump for Semiconductor Equipment Market?

->Molecular Pump for Semiconductor Equipment Market was valued at USD 586 million in 2024 and is projected to reach USD 1.153 billion by 2032, exhibiting a CAGR of 10.4% during the forecast period.

Which key companies operate in Molecular Pump for Semiconductor Equipment Market?

-> Key players include Atlas Copco, Shimadzu Co., Ltd, Osaka Vacuum, Ltd, Agilent Technologies, Inc, and Pfeiffer Vacuum GmbH, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for semiconductors, advancements in fabrication technologies, and expansion of electronics manufacturing, particularly in the Asia-Pacific region.

Which region dominates the market?

-> Asia-Pacific is the dominant market, accounting for around 70% of the global market share.

What are the emerging trends?

-> Emerging trends include the development of advanced molecular pump technologies, integration in critical semiconductor manufacturing processes like deposition and etching, and increasing R&D investments.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...