MARKET INSIGHTS

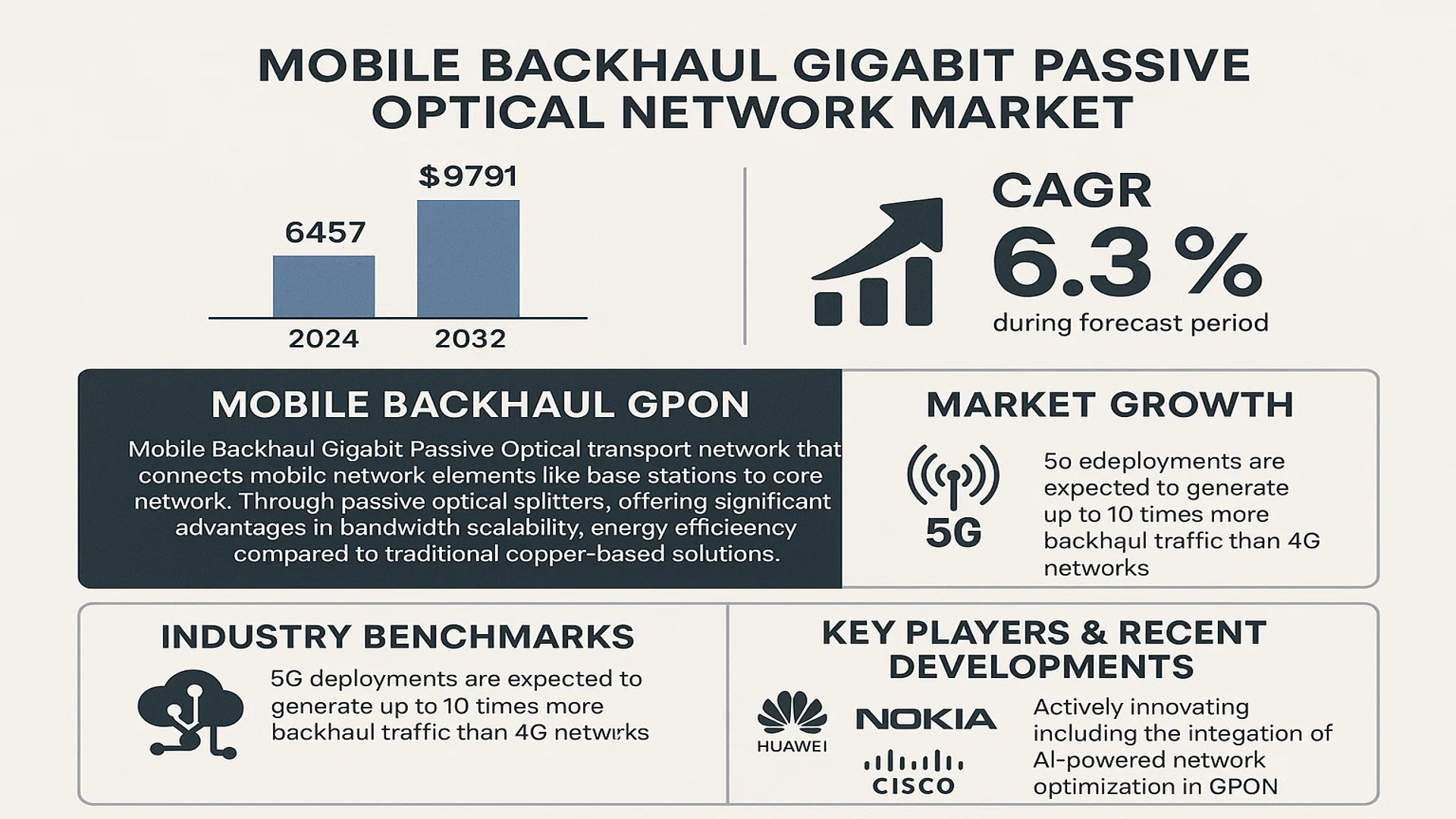

The global Mobile Backhaul Gigabit Passive Optical Network market was valued at 6457 million in 2024 and is projected to reach US$ 9791 million by 2032, at a CAGR of 6.3% during the forecast period.

Mobile Backhaul GPON refers to the high-capacity optical transport network that connects mobile network elements like base stations to the core network. This technology enables efficient data transmission through passive optical splitters, offering significant advantages in bandwidth scalability, energy efficiency, and cost-effectiveness compared to traditional copper-based solutions.

The market growth is primarily driven by the rapid expansion of 5G networks, which require robust backhaul solutions to handle increased data traffic. According to industry benchmarks, 5G deployments are expected to generate up to 10 times more backhaul traffic than 4G networks. Furthermore, the rising adoption of cloud services and IoT applications is creating additional demand for high-speed, low-latency connectivity solutions. Key players like Huawei, Nokia, and Cisco are actively innovating in this space, with recent developments including the integration of AI-powered network optimization in GPON systems.

MARKET DYNAMICS

MARKET DRIVERS

5G Network Expansion Driving Demand for GPON Backhaul Solutions

The global rollout of 5G networks is significantly accelerating the adoption of Gigabit Passive Optical Network (GPON) solutions for mobile backhaul. With 5G requiring up to 10 times higher bandwidth capacity compared to 4G networks, traditional copper-based backhaul solutions are proving insufficient. Mobile operators are increasingly turning to GPON technology, which offers fiber-optic transmission speeds exceeding 2.5 Gbps downstream and 1.25 Gbps upstream. By 2025, over 60% of new mobile backhaul deployments are expected to utilize fiber-based solutions, with GPON emerging as a cost-effective alternative to point-to-point fiber.

Rising Data Traffic from Smart Devices Fueling Network Upgrades

Global mobile data traffic has grown at a compound annual growth rate of approximately 45% since 2020, driven by increased smartphone penetration and streaming services. This exponential growth creates unprecedented demands on mobile networks, forcing operators to upgrade their backhaul infrastructure. GPON technology provides the necessary bandwidth and scalability to support this traffic surge while maintaining low latency requirements for emerging applications like autonomous vehicles and augmented reality. Furthermore, the technology’s passive architecture significantly reduces power consumption compared to active optical networks, making it attractive for sustainability-focused operators.

➤ Network operators investing in GPON backhaul report up to 40% reduction in total cost of ownership compared to traditional solutions, while simultaneously improving network reliability and future-proofing their infrastructure.

MARKET RESTRAINTS

High Initial Deployment Costs Limiting Adoption in Emerging Markets

While GPON offers long-term operational savings, the substantial upfront investment required for fiber infrastructure presents a significant barrier, particularly in developing regions. Deploying GPON backhaul requires complete fiber optic network overhauls in many cases, involving costly civil works and right-of-way negotiations. In price-sensitive markets where ARPU remains low, operators often opt for less-capable but more immediately affordable solutions like microwave backhaul. This is particularly evident in regions where subscriber densities cannot justify the infrastructure investment, creating a chicken-and-egg scenario for network modernization.

Other Restraints

Regulatory and Permitting Challenges

Navigating complex regulatory environments and obtaining permits for fiber deployment can delay GPON backhaul projects by 12-18 months in some markets. Stringent environmental regulations, municipal franchise agreements, and complex right-of-way processes create implementation bottlenecks that discourage some operators from pursuing fiber-based solutions.

Technology Migration Complexities

Transitioning existing networks to GPON architecture requires careful planning to avoid service disruptions. Many operators face challenges integrating new passive optical components with legacy active equipment, requiring expensive network management upgrades and staff retraining. These migration complexities can temporarily reduce network reliability during transition periods, creating hesitancy among risk-averse operators.

MARKET OPPORTUNITIES

Emerging XGS-PON Standards Opening New Revenue Streams

The evolution from traditional GPON to next-generation XGS-PON (10G Symmetrical GPON) presents substantial growth opportunities for equipment vendors and service providers. XGS-PON delivers symmetrical 10 Gbps speeds while maintaining backward compatibility with existing GPON infrastructure, allowing for gradual network upgrades. This technology enables mobile operators to support advanced backhaul scenarios like distributed cell sites and cloud RAN architectures. Market projections indicate that XGS-PON will account for over 30% of all PON equipment shipments by 2026, creating a $2.5 billion addressable market for compatible backhaul solutions.

Smart City Initiatives Driving Municipal Backhaul Deployments

Global smart city projects are generating significant demand for robust backhaul infrastructure to connect distributed IoT sensors and municipal networks. GPON’s point-to-multipoint architecture makes it ideal for these deployments, enabling single fiber connections to serve multiple endpoints across urban areas. Many municipalities are partnering with telecom operators to deploy shared GPON infrastructure that supports both mobile backhaul and smart city applications, creating new public-private partnership models. These initiatives are particularly active in Asia-Pacific and European markets, where government funding for digital transformation remains strong.

MARKET CHALLENGES

Fiber Availability Gaps Creating Digital Divide in Rural Areas

While GPON backhaul offers compelling technical advantages, limited fiber availability in rural and remote regions presents a persistent challenge. The economics of fiber deployment become increasingly unfavorable in low-density areas, leaving many regional mobile operators dependent on inferior backhaul solutions. This creates a growing performance disparity between urban and rural networks that regulatory interventions have struggled to resolve. Even in developed markets, approximately 25% of mobile base stations still lack fiber connectivity, forcing operators to implement hybrid backhaul architectures that compromise on performance.

Other Challenges

Workforce Shortages Hampering Deployment Timelines

The telecommunications industry faces a critical shortage of skilled fiber technicians capable of deploying and maintaining GPON networks. Training programs have failed to keep pace with industry demand, leading to project delays and quality control issues. Some major operators report deployment timelines extended by 20-30% due to workforce constraints, particularly in specialized areas like fusion splicing and optical network testing.

Security Vulnerabilities in Passive Networks

The shared nature of GPON architecture introduces potential security risks that require sophisticated mitigation strategies. While point-to-point encryption addresses many concerns, operators must implement additional measures like optical layer monitoring and physical security to prevent signal tapping and denial-of-service attacks. These requirements add complexity to network operations and increase the importance of comprehensive security policies for backhaul networks.

MOBILE BACKHAUL GIGABIT PASSIVE OPTICAL NETWORK MARKET TRENDS

5G Network Expansion Driving Demand for High-Capacity Backhaul Solutions

The rapid global rollout of 5G networks is creating unprecedented demand for high-bandwidth mobile backhaul solutions, with GPON emerging as a key enabler. As mobile operators upgrade their infrastructure to support 5G’s low-latency applications, the market for GPON-based backhaul is projected to grow at a 6.3% CAGR through 2032. This growth is particularly evident in dense urban environments where fiber-based backhaul provides the necessary capacity and reliability that traditional microwave links cannot match. Recent deployments show that GPON solutions can deliver up to 10 Gbps symmetrical bandwidth, making them ideal for supporting the massive IoT deployments and enhanced mobile broadband services enabled by 5G.

Other Trends

Cloud Service Migration Accelerates Fiber Demand

The migration of enterprise workloads to cloud platforms is forcing network operators to rethink their backhaul strategies. With over 70% of enterprises now adopting hybrid cloud architectures, there’s growing pressure on mobile networks to provide seamless connectivity between edge devices and cloud data centers. GPON technology addresses this need by offering cost-effective, high-bandwidth connections that scale easily to meet fluctuating demand. This trend is particularly impactful in emerging markets where telecom operators are leapfrogging legacy copper infrastructure to deploy fiber-based mobile backhaul from the outset.

Network Virtualization and SDN Integration

The convergence of software-defined networking (SDN) principles with GPON architectures is creating more adaptable backhaul solutions. Network operators are increasingly adopting virtualized OLT (Optical Line Terminal) platforms that can be centrally managed and dynamically reconfigured. This shift allows for more efficient resource allocation across mobile and fixed networks, with some implementations showing 30-40% improvements in operational efficiency. The integration of AI-driven network analytics is further enhancing this capability, enabling predictive maintenance and automatic capacity planning in GPON backhaul networks.

COMPETITIVE LANDSCAPE

Key Industry Players

Network Providers Expand Fiber Infrastructure to Meet Surging 5G Demand

The global Mobile Backhaul GPON market exhibits a dynamic competitive landscape where telecom giants, equipment manufacturers, and specialized fiber optics providers compete for market share. Currently valued at $6.46 billion in 2024, this market is projected to grow at 6.3% CAGR through 2032, driven by escalating bandwidth requirements for 5G networks and IoT applications.

Huawei Technologies maintains a dominant position with approximately 22% market share, owing to its comprehensive GPON product ecosystem and strong presence across emerging APAC markets. However, recent geopolitical tensions have prompted many Western operators to diversify their supplier base toward Nokia, Cisco, and NEC Corporation, which collectively account for nearly 30% of the market.

Meanwhile, North American players like Verizon and AT&T Intellectual Property are accelerating fiber deployments through public-private partnerships, with the US accounting for 38% of global GPON backhaul investments in 2024. Their strategy focuses on leveraging existing infrastructure while integrating SDN/NFV capabilities for next-gen networks.

The competitive intensity is further amplified by Chinese manufacturers ZTE Corporation and FiberHome, who are undercutting traditional vendors with cost-optimized solutions. This pricing pressure has compelled European players like Telefonaktiebolaget LM Ericsson and Adtran to differentiate through energy-efficient designs and AI-driven network management tools.

List of Key Mobile Backhaul GPON Solution Providers

- Huawei Technologies Co., Ltd (China)

- Nokia Corporation (Finland)

- Cisco Systems, Inc (U.S.)

- NEC Corporation (Japan)

- Verizon Communications (U.S.)

- AT&T Intellectual Property (U.S.)

- ZTE Corporation (China)

- FiberHome (China)

- Telefonaktiebolaget LM Ericsson (Sweden)

- Adtran Holdings, Inc. (U.S.)

- DZS, Inc (U.S.)

- Mitsubishi Electric (Japan)

Segment Analysis:

By Type

XGS-Passive Optical Network Segment Dominates Due to High Bandwidth and Scalability

The market is segmented based on type into:

- 5G-Passive Optical Network

- Subtypes: Symmetric, Asymmetric, and others

- XG-Passive Optical Network

- Subtypes: XG-PON1, XG-PON2, and others

- XGS-Passive Optical Network

- Subtypes: XGS-PON, XGS-PON Plus, and others

- NG-Passive Optical Network

- Subtypes: NG-PON2, NG-PON3, and others

By Application

Telecom Sector Leads Due to Rising 5G Deployment and Network Modernization

The market is segmented based on application into:

- Telecom

- Subtypes: Mobile backhaul, Fixed broadband, and others

- Internet Service Providers (ISPs)

- Subtypes: Residential, Enterprise, and others

- Data Centers

- Subtypes: Cloud, Hyperscale, and others

- Others

By Technology

Wavelength Division Multiplexing (WDM) Gains Traction for High-Capacity Transmission

The market is segmented based on technology into:

- Time Division Multiplexing (TDM)

- Wavelength Division Multiplexing (WDM)

- Subtypes: CWDM, DWDM, and others

- Ethernet

- Others

By End User

Enterprise Segment Accelerates GPON Adoption for High-Speed Connectivity

The market is segmented based on end user into:

- Residential

- Commercial

- Subtypes: Small & Medium Enterprises (SMEs), Large Enterprises, and others

- Government & Defense

- Others

Regional Analysis: Mobile Backhaul Gigabit Passive Optical Network Market

North America

North America leads in Mobile Backhaul GPON adoption due to advanced telecom infrastructure and strong demand for high-speed connectivity. The U.S. dominates with over 40% of regional market share, driven by 5G network rollouts and cloud service expansions from providers like Verizon and AT&T. Canada follows closely, with significant investments in fiber-optic backhaul to support rural connectivity initiatives. Strict data regulations and the need for low-latency networks in financial hubs further accelerate deployment. However, high infrastructure costs and complex approval processes for new installations remain bottlenecks for smaller operators.

Europe

Europe’s market thrives on robust regulatory support for fiber networks and sustainable telecom solutions. The EU’s Digital Decade 2030 targets incentivize GPON adoption to achieve universal broadband coverage. Germany and France lead in deployments, with Nokia and Deutsche Telekom actively upgrading backhaul networks for smart city applications. Eastern Europe shows slower growth due to legacy copper network dependencies, though EU funding is bridging this gap. Energy efficiency standards like the Eco-Design Directive push vendors toward greener optical solutions, influencing procurement decisions across the region.

Asia-Pacific

As the fastest-growing region, APAC accounts for nearly 50% of global Mobile Backhaul GPON demand. China’s “Broadband China” strategy and India’s National Digital Communications Policy drive mass deployments, with Huawei and ZTE supplying cost-optimized solutions. Southeast Asian nations prioritize GPON to support surging mobile data consumption—Indonesia and Vietnam see 20%+ annual growth in fiber backhaul installations. Japan and South Korea focus on next-gen XGS-PON for ultra-low latency applications like autonomous vehicles. While urban areas advance rapidly, rural coverage gaps persist due to challenging terrain and ROI concerns.

South America

Market growth here is uneven, with Brazil leading at 60% regional share thanks to telecom privatization and 5G spectrum auctions. Argentina and Chile follow with metro network upgrades, though currency volatility impacts equipment imports. The Andes region faces geographical hurdles for fiber trenching, increasing reliance on wireless backhaul alternatives. Regulatory uncertainty in some countries delays large-scale investments, but submarine cable projects along the Pacific coast are improving international bandwidth availability for mobile operators.

Middle East & Africa

Gulf Cooperation Council (GCC) nations drive the market with smart city projects in Dubai and NEOM requiring high-capacity backhaul. Saudi Arabia’s Vision 2030 allocates $24 billion for digital infrastructure, with GPON as a key enabler. Africa’s growth is led by South Africa and Nigeria, where mobile operators leverage fiber to offset unreliable power grids. East Africa benefits from undersea cable landings, though inland deployment costs remain prohibitive. Political instability in some regions creates investment risks, while SAQ switching techniques help optimize existing GPON infrastructure under bandwidth constraints.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Mobile Backhaul Gigabit Passive Optical Network (GPON) markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Mobile Backhaul GPON market was valued at USD 6.457 billion in 2024 and is projected to reach USD 9.791 billion by 2032, growing at a CAGR of 6.3%.

- Segmentation Analysis: Detailed breakdown by product type (5G-PON, XG-PON, XGS-PON, NG-PON), application (Telecom, Internet, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific dominates with over 42% market share in 2024.

- Competitive Landscape: Profiles of leading market participants including Huawei, Nokia, ZTE, Cisco, and ADTRAN, including their product offerings, R&D focus, manufacturing capacity, and recent M&A activities.

- Technology Trends & Innovation: Assessment of emerging GPON technologies, integration with 5G networks, fiber optic advancements, and evolving industry standards like ITU-T G.984 and G.987.

- Market Drivers & Restraints: Evaluation of factors including 5G deployment, IoT expansion, and cloud computing growth, along with challenges like high deployment costs and regulatory hurdles.

- Stakeholder Analysis: Insights for telecom operators, network equipment providers, component manufacturers, and investors regarding strategic opportunities in the evolving mobile backhaul ecosystem.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Mobile Backhaul GPON Market?

-> Mobile Backhaul Gigabit Passive Optical Network market was valued at 6457 million in 2024 and is projected to reach US$ 9791 million by 2032, at a CAGR of 6.3% during the forecast period.

Which key companies operate in Global Mobile Backhaul GPON Market?

-> Key players include Huawei, Nokia, ZTE, Cisco, ADTRAN, Verizon, NEC Corporation, and Telefonaktiebolaget LM Ericsson, among others.

What are the key growth drivers?

-> Key growth drivers include 5G network expansion, increasing mobile data traffic, and demand for high-bandwidth applications.

Which region dominates the market?

-> Asia-Pacific dominates the market, accounting for over 42% share in 2024, driven by rapid digital transformation in China and India.

What are the emerging trends?

-> Emerging trends include convergence of GPON with 5G networks, software-defined networking integration, and AI-driven network optimization.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...