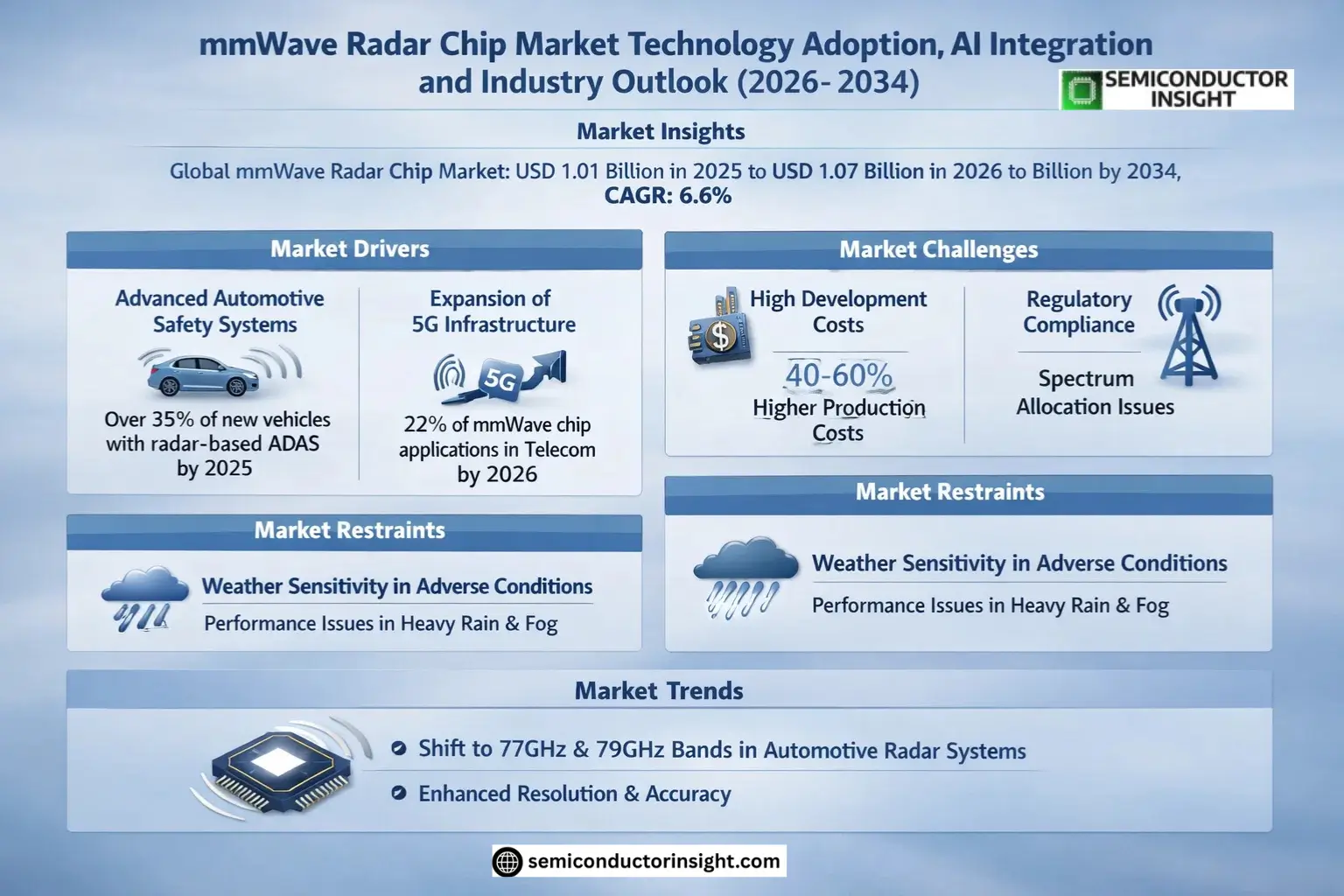

Market Insights

Global mmWave Radar Chip Market size was valued at USD 1.01 billion in 2025. The market is projected to grow from USD 1.07 billion in 2026 to USD 1.56 billion by 2034, exhibiting a CAGR of 6.6% during the forecast period.

Millimeter wave (mmWave) radar chips are highly integrated semiconductor devices designed for radar systems operating in the 24GHz to 79GHz frequency bands. These chips combine RF front-end components, signal processing modules, and analog-to-digital converters to enable precise detection of distance, velocity, and angle for applications such as automotive advanced driver-assistance systems (ADAS), drones, and industrial automation.

The market growth is primarily driven by increasing adoption of autonomous vehicles, with automotive radar shipments expected to exceed 140 million units annually by 2024. Technological advancements are accelerating the shift from multi-chip designs to single-chip radar SoCs (System-on-Chip), particularly in the 77GHz-79GHz bands which offer superior resolution compared to legacy 24GHz systems. Key players including Infineon, NXP Semiconductors, and Texas Instruments are driving innovation through higher integration levels and improved anti-interference capabilities for next-generation L4 autonomous driving applications.

MARKET DRIVERS

Rising Demand for Advanced Automotive Safety Systems

mmWave Radar Chip Market is experiencing significant growth due to increasing adoption in automotive safety applications. Advanced driver-assistance systems (ADAS) and autonomous vehicles rely heavily on mmWave radar technology for precise object detection. Over 35% of new vehicles will be equipped with radar-based ADAS by 2025, driving chip demand.

Expansion of 5G Infrastructure

Global 5G network deployments are creating adjacent opportunities for mmWave radar chips in telecom infrastructure. These chips enable high-frequency signal processing essential for 5G small cells and backhaul systems. The telecom sector is projected to account for 22% of mmWave radar chip applications by 2026.

The combination of automotive and industrial automation applications continues to fuel sector growth, with smart factories increasingly deploying mmWave solutions for precision monitoring.

MARKET CHALLENGES

High Development and Production Costs

mmWave radar chips face adoption barriers due to complex manufacturing processes requiring specialized semiconductor fabrication. The average production cost for automotive-grade mmWave chips is 40-60% higher than conventional radar solutions, impacting price sensitivity in cost-conscious markets.

Other Challenges

Regulatory Compliance Hurdles

Differing frequency allocation regulations across regions create fragmentation in mmWave radar chip design. The 60GHz vs 77GHz spectrum debate continues to impact global product standardization.

MARKET RESTRAINTS

Technical Limitations in Adverse Conditions

While mmWave radar chips offer superior resolution, they face performance degradation in heavy rain or fog environments. This weather sensitivity restricts adoption in certain geographic markets and applications where reliability is critical.

MARKET OPPORTUNITIES

Emerging Industrial IoT Applications

mmWave Radar Chip Market stands to benefit significantly from Industry 4.0 adoption, with predictive maintenance systems and automated quality control systems driving demand. The industrial sector is projected to represent 28% of new mmWave chip deployments by 2027.

mmWave Radar Chip Market Trends

Shift to Higher Frequency Bands in Automotive Applications

mmWave Radar Chip Market is witnessing a significant transition from 24GHz to 77GHz and 79GHz bands in automotive radar systems. Regulatory changes and the need for improved resolution are accelerating this shift. Wider bandwidth utilization in these higher frequencies enables better object detection and classification, critical for advanced driver assistance systems (ADAS) and autonomous driving technologies.

Other Trends

Growing Demand for Integrated Radar SoCs

Industry leaders are rapidly moving from multi-chip architectures to single-chip radar system-on-chip (SoC) solutions. This transition improves performance while reducing size, power consumption, and overall system costs. The integration of RF front-end, baseband processing, and ADC components on a single chip is particularly valuable for automotive and industrial applications where space constraints exist.

Expansion into Non-Automotive Applications

Beyond automotive uses, mmWave Radar Chips are gaining traction in drones, robotics, and industrial automation. These applications benefit from the precise distance, velocity, and angle measurement capabilities of mmWave technology. High-resolution radar systems are particularly valuable for obstacle detection and navigation in dynamic environments.

Other Trends

China’s Growing Role in mmWave Radar Development

Chinese firms like Nanjing Maikeke Microelectronics Technology and Gatlin Microelectronics Technology are emerging as significant players in the mmWave Radar Chip space. The domestic industry is developing competitive solutions across multiple frequency bands, supported by government initiatives and growing local demand for automotive and industrial radar systems.

Increasing Focus on System-Level Performance

The competitive landscape is evolving from simple RF performance metrics to comprehensive system-level evaluations. Manufacturers now emphasize link budgets, algorithm compatibility, and vehicle-grade reliability. This shift reflects the maturing of mmWave radar technology and its expanding role in safety-critical applications across multiple industries.

COMPETITIVE LANDSCAPE

Key Industry Players

Global mmWave Radar Chip Market Dominated by Automotive Semiconductor Giants

mmWave Radar Chip Market is led by established semiconductor players with strong automotive sector penetration. Infineon Technologies and NXP Semiconductors collectively hold over 45% market share, leveraging their advanced 77GHz and 79GHz solutions for ADAS applications. Texas Instruments follows closely with its highly integrated radar SoCs, while STMicroelectronics gains traction through partnerships with European automakers. The competitive landscape shows accelerating consolidation as major players acquire specialized radar tech firms – exemplified by Infineon’s acquisition of Innoluce for beam-steering technology.

Several Chinese manufacturers are emerging as significant challengers in the 24GHz and 60GHz segments. Nanjing Maikeke Microelectronics and Gatlin Microelectronics have secured design wins in domestic automotive and industrial markets. Specialty players like indie Semiconductor focus on cost-optimized solutions for entry-level vehicles, while Stormicro and SGR Semiconductors target niche industrial applications. The market also sees increasing participation from defense technology firms such as CETC 38th Research Institute, transferring mmWave expertise from military to commercial applications.

List of Key mmWave Radar Chip Companies Profiled

- Infineon Technologies

- NXP Semiconductors

- Texas Instruments

- STMicroelectronics

- indie Semiconductor

- Nanjing Maikeke Microelectronics Technology

- Gatlin Microelectronics Technology

- CETC 38th Research Institute

- Skyrelay (Beijing) Technology

- Hangzhou Andar Technologies

- SGR Semiconductors

- Zhuhai Microcreative Technology

- Ningbo Gekong Intelligent Technology

- Stormicro

- Renesas Electronics

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

77 GHz & 79 GHz dominate the market due to:

|

| By Application |

|

Automotive segment leads with notable trends:

|

| By End User |

|

Tier 1 Suppliers represent the primary demand drivers because:

|

| By Platform |

|

Vehicle Mounted platforms show strongest growth potential due to:

|

| By Integration Level |

|

System-on-Chip solutions are gaining dominance through:

|

Regional Analysis: mmWave Radar Chip Market

Detroit and Silicon Valley emerge as dual hubs for mmWave radar integration in vehicles, with OEMs prioritizing 4D imaging radar chips for Level 4 autonomy. Strategic partnerships between automotive manufacturers and fabless chip companies drive proprietary radar solutions.

Pentagon-funded projects accelerate mmWave radar chip deployment in perimeter security systems. Advanced packaging techniques enable ruggedized radar modules for battlefield surveillance applications, with significant R&D focused on anti-jamming capabilities.

Warehouse robotics and AGV manufacturers increasingly adopt 60GHz radar chips for proximity sensing in logistics centers. The region sees growing implementation of mmWave-based personnel detection systems in hazardous industrial environments.

Edge AI integration with mmWave radar chips enables real-time micro-Doppler analysis for gesture recognition. Startups are developing neural network-optimized radar SoCs specifically for North American smart infrastructure projects.

Europe

European mmWave radar chip adoption grows steadily through stringent automotive safety regulations and smart city initiatives. Germany leads with automotive-grade radar solutions, while Nordic countries focus on industrial IoT applications. The EU’s C-V2X deployment roadmap creates opportunities for 79GHz radar-communication fusion chips. Challenges include complex RF certification processes and competition from LiDAR solutions in premium vehicle segments.

Asia-Pacific

China’s mmWave radar chip market expands rapidly through government-backed autonomous driving programs and 5G infrastructure projects. Japan maintains leadership in high-frequency radar components, while South Korea invests heavily in automotive radar-AI fusion. The region benefits from dense semiconductor manufacturing clusters but faces IP protection concerns in emerging markets.

South America

Brazil emerges as regional leader in mmWave radar deployment for urban security and mining applications. Automotive adoption remains limited to premium imports, but growing interest emerges in agricultural radar systems for precision farming. Infrastructure constraints and import dependencies slow market maturation compared to other regions.

Middle East & Africa

Gulf countries drive demand through smart city projects and border surveillance systems, with Israel emerging as radar tech exporter. Africa shows nascent growth in traffic monitoring applications, though market development is hindered by limited local semiconductor expertise and infrastructure gaps.

Report Scope

This market research report provides a comprehensive analysis of the mmWave Radar Chip Market, covering the forecast period 2025–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of mmWave Radar Chip Market?

-> mmWave Radar Chip Market size was valued at USD 1.01 billion in 2025. The market is projected to grow from USD 1.07 billion in 2026 to USD 1.56 billion by 2034, exhibiting a CAGR of 6.6% during the forecast period.

What is the growth rate of mmWave Radar Chip Market?

-> The market is expected to grow at a CAGR of 6.6% during the forecast period (2025-2034).

Which key companies operate in mmWave Radar Chip Market?

-> Key players include Infineon, NXP, TI, STMicroelectronics, indie, Nanjing Maikeke Microelectronics Technology, Gatlin Microelectronics Technology, CETC 38th Research Institute, and others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for vehicle ADAS and autonomous driving radar, shift towards 77GHz/79GHz bands, and adoption of highly integrated radar SoCs.

Which region dominates the market?

-> Asia holds significant market share, driven by strong demand from countries like China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include transition to single-chip radar SoCs, high-resolution imaging radars, and advanced algorithm stack adaptation.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...