Market Insights

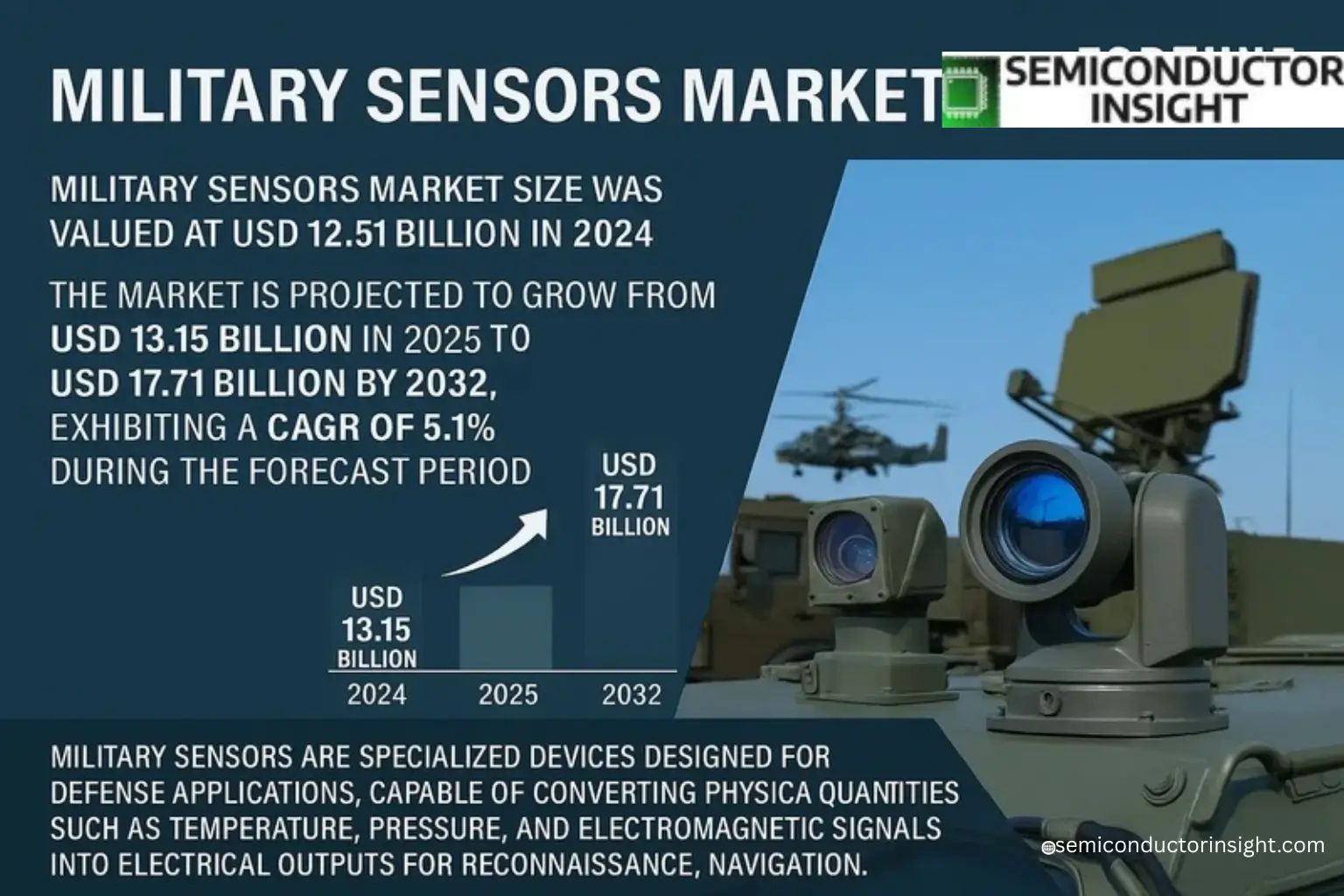

Global Military Sensors Market size was valued at USD 12.51 billion in 2024. The market is projected to grow from USD 13.15 billion in 2025 to USD 17.71 billion by 2032, exhibiting a CAGR of 5.1% during the forecast period.

Military sensors are specialized devices designed for defense applications, capable of converting physical quantities such as temperature, pressure, and electromagnetic signals into electrical outputs for reconnaissance, navigation, and weapon guidance. These sensors play a critical role in modern warfare by enhancing situational awareness and operational efficiency.

The market growth is driven by increasing defense budgets worldwide, advancements in sensor technologies like MEMS and quantum sensing, and rising demand for unmanned systems such as drones and missiles. For instance, North America dominates the market with a 40% share due to high defense spending, followed by Asia Pacific (30%) and Europe (20%). Key players like Lockheed Martin and BAE Systems plc collectively hold over 30% of the global market share.

MARKET DRIVERS

Geopolitical Instability and Modernization Programs

Escalating geopolitical tensions worldwide are compelling nations to invest significantly in advanced military capabilities. This has accelerated the procurement and development of sophisticated Military Sensors to enhance situational awareness, threat detection, and overall defense readiness. Global Military Sensors Market is directly fueled by the ongoing modernization of land, air, and naval platforms, which requires the integration of next-generation sensing technologies.

Advancements in Sensor Technology

Technological innovation is a primary catalyst for growth in the Military Sensors Market. The development of multi-spectral imaging, hyperspectral sensors, advanced radar, and LiDAR systems provides unprecedented capabilities for intelligence, surveillance, and reconnaissance (ISR) missions. These technologies enable forces to operate effectively in contested environments and adverse weather conditions.

The proliferation of artificial intelligence and machine learning is transforming the Military Sensors Market. AI-powered sensors can autonomously identify targets, reduce false alarms, and process vast amounts of data from multiple sources in real-time. This capability for enhanced data fusion is critical for network-centric warfare, making sensor systems more intelligent and responsive to dynamic battlefield conditions.

MARKET CHALLENGES

High Development Costs and Budgetary Constraints

The research, development, and testing of cutting-edge Military Sensors involve substantial financial investment and extended timelines. Budgetary pressures within defense departments can lead to program delays or cancellations, posing a significant challenge for market growth. Balancing performance requirements with cost-effectiveness remains a persistent hurdle for both manufacturers and procurers in the Military Sensors Market.

Other Challenges

Cybersecurity Vulnerabilities

As Military Sensors become more networked and software-defined, they are increasingly vulnerable to cyber-attacks, jamming, and spoofing. Securing these critical systems against sophisticated electronic warfare threats is a major technical and operational challenge.

Integration and Interoperability

Integrating new sensor systems with legacy platforms and ensuring interoperability across different branches of the military and allied forces creates significant complexity. Standardization issues can hinder the seamless flow of information, limiting the effectiveness of sensor networks.

MARKET RESTRAINTS

Stringent Regulatory and Export Control Policies

Global Military Sensors Market is subject to strict international arms trafficking regulations and export controls, such as the International Traffic in Arms Regulations (ITAR). These compliance requirements can restrict market access, complicate international collaborations, and lengthen the sales cycle, thereby acting as a significant restraint on market expansion for defense contractors.

Complex Supply Chain Dynamics

The specialized nature of components used in Military Sensors, including rare-earth materials and advanced semiconductors, creates a complex and sometimes fragile supply chain. Disruptions, whether from geopolitical events or supplier concentration, can delay production and increase costs, restraining the timely delivery of critical systems to the end-users.

MARKET OPPORTUNITIES

Growth in Unmanned Systems and C4ISR

The rapid expansion of unmanned aerial, ground, and maritime vehicles presents a major opportunity for the Military Sensors Market. These platforms are heavily reliant on advanced sensors for autonomy, navigation, and mission execution. The increasing demand for comprehensive Command, Control, Communications, Computers, Intelligence, Surveillance, and Reconnaissance (C4ISR) systems further drives the need for integrated and resilient sensor suites.

Miniaturization and Development of Wearable Sensors

Advancements in micro-electromechanical systems (MEMS) and nanotechnology are enabling the miniaturization of sensors without compromising performance. This trend opens opportunities for developing lightweight, low-power wearable sensors for dismounted soldiers, enhancing their situational awareness, health monitoring, and overall survivability on the modern battlefield.

Current Military Sensors Market Trends

Technological Integration and Intelligence

The Military Sensors Market is being significantly shaped by the demand for advanced military technology, particularly through intelligence and integration. The application of MEMS (micro-electromechanical systems) and nanotechnology is enhancing sensor performance, driving a trend toward higher precision and reliability. This evolution supports the development of intelligent sensors with autonomous compensation, detection, and diagnostic functions, which are critical for modern defense platforms like unmanned aerial vehicles (UAVs) and smart munitions. Concurrently, the rise of quantum sensors and LiDAR technology is bolstering battlefield situational awareness, representing a key trend in the market’s advancement.

Other Trends

Policy and Regulatory Support

Government policies and international cooperation are pivotal trends influencing the Military Sensors Market. National initiatives, such as the U.S. National Defense Authorization Act and China’s “14th Five-Year Plan,” provide fiscal and policy support that accelerates research and development. These efforts are complemented by international standardization through organizations like NATO and the ISO, which foster technical exchanges and promote the global, standardized development of sensor technology, thereby influencing market growth trajectories.

Geopolitical and Security Dynamics

The complexity of the international security environment is a major trend driving the Military Sensors Market. Regional conflicts and heightened concerns over terrorism are increasing the demand for advanced sensing capabilities. This is particularly evident in the Asia-Pacific region, where security complexities are a significant market driver. Furthermore, the increasing importance of electronic warfare and information security is expanding the role of sensors, such as radio frequency types used to identify adversary signal characteristics, in addressing modern security challenges.

Competitive Landscape and Future Outlook

Intensified competition and the localization of production are key trends within the Military Sensors Market. Competition among global firms spurs innovation, while policies in countries like China are accelerating the domestic production of critical components, thereby reshaping the competitive landscape. Looking forward, the market is trending toward deeper technological integration, including the fusion of artificial intelligence with quantum sensing for autonomous decision-making. Material innovations and increased global cooperation are expected to further propel the market, which is projected to grow from USD 12510 million in 2024 to USD 17710 million by 2032.

COMPETITIVE LANDSCAPE

Key Industry Players

A Consolidated Market Driven by Technological Prowess and Strategic Positioning

Global Military Sensors Market is characterized by a significant level of consolidation, with the top three companies collectively holding over 30% of the market share. North America dominates as the largest regional market, accounting for approximately 40% of global revenue, largely propelled by the substantial defense budgets and advanced technological base of the United States. Lockheed Martin Corporation and Raytheon Technologies (which now includes the former Raytheon Company) are preeminent leaders, leveraging their extensive experience in developing integrated defense systems for applications ranging from missile guidance to spacecraft avionics. Their market position is reinforced by continuous investment in R&D, particularly in areas like quantum sensing, artificial intelligence integration, and advanced MEMS technologies, which are critical for next-generation intelligence, surveillance, and reconnaissance (ISR) capabilities.

Beyond the dominant players, a diverse group of specialized and geographically significant companies competes in key segments and regions. BAE Systems plc maintains a strong presence in Europe, offering a comprehensive portfolio of electronic warfare and sensing solutions. Honeywell International Inc. is a critical supplier of inertial sensors and navigation systems for military aircraft and UAVs. In the Asia-Pacific region, which holds about 30% of the market, China Electronics Technology Group Corporation (CETC) is a major force, supported by national policies accelerating technological localization. Other significant players focus on niche applications, such as TE Connectivity Ltd. with its robust connector and sensor solutions, Curtiss-Wright Corporation with its harsh-environment sensors for defense platforms, and TransDigm Group, which supplies proprietary sensors for aerospace systems. This competitive environment is further intensified by ongoing international collaborations and regional defense initiatives.

List of Key Military Sensors Companies Profiled

- Lockheed Martin Corporation

- BAE Systems plc

- Raytheon Technologies

- Honeywell International Inc.

- China Electronics Technology Group Corporation (CETC)

- TE Connectivity Ltd.

- TransDigm Group Inc.

- Curtiss-Wright Corporation

- General Dynamics Corporation

- Thales Group

- L3Harris Technologies, Inc.

- Northrop Grumman Corporation

- Safran S.A.

- Leidos Holdings, Inc.

- Aerospace Long March Launch Vehicle Technology Co., Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Physical Quantity Sensors represent the most significant market segment, driven by their extensive and foundational role in modern military operations.

|

| By Application |

|

Spacecraft is a leading application segment, reflecting the strategic military emphasis on space-based assets for global dominance.

|

| By End User |

|

Air Force constitutes a primary end-user segment due to the intense technological requirements of modern aerial warfare and surveillance.

|

| By Technology |

|

MEMS & Nanotechnology is the dominant technological foundation, enabling a new generation of miniaturized and high-performance sensors.

|

| By Operational Domain |

|

Airborne operations represent a leading domain, characterized by an exceptionally high demand for sophisticated sensor suites.

|

Regional Analysis: Military Sensors Market

North America’s Military Sensors Market is characterized by its role as a global innovation hub. Leading defense contractors and numerous specialized technology firms are concentrated here, developing sophisticated sensor systems. These include hyperspectral imaging, advanced LiDAR, and AI-integrated sensor suites that provide critical data fusion capabilities, directly responding to the Pentagon’s focus on network-centric warfare and information superiority.

Large-scale, multi-year procurement initiatives from the U.S. Department of Defense are a primary market driver. Programs aimed at upgrading fighter jets, unmanned systems, and naval fleets mandate the integration of state-of-the-art sensors for targeting, surveillance, and threat detection. This sustained demand creates a predictable and lucrative market for sensor manufacturers within the North American Military Sensors Market.

A stringent yet supportive regulatory environment governs the Military Sensors Market in North America. Robust intellectual property protection and controlled export policies ensure technological advantages are maintained. Collaboration between defense agencies and manufacturers on standards and interoperability requirements ensures that sensor systems are seamlessly integrated into larger defense networks, enhancing their effectiveness and market viability.

The strategic emphasis on Command, Control, Communications, Computers, Intelligence, Surveillance, and Reconnaissance (C4ISR) systems is a significant growth vector. Sensors are the foundational element of these systems, driving demand for intelligence-gathering and situational awareness technologies. Investments in space-based surveillance and cyber-physical systems further expand the scope and sophistication of the Military Sensors Market in the region.

Europe

The European Military Sensors Market is a significant and technologically advanced segment, driven by collective defense initiatives through NATO and individual national modernization programs. Countries like the UK, France, and Germany are leading investors, focusing on enhancing interoperability among allied forces. Key trends include the development of multi-spectral and multi-functional sensors for next-generation platforms such as the Eurofighter Typhoon and Future Combat Air System. There is a growing emphasis on sensor systems that can operate effectively in contested electronic warfare environments. Collaborative projects between European defense giants facilitate shared technology development, reducing costs and standardizing capabilities across the continent’s military forces. The market is also seeing increased investment in unmanned systems and soldier modernization programs, which rely heavily on advanced sensing technologies for navigation, targeting, and survival, positioning Europe as a strong and innovative competitor in the global Military Sensors Market.

Asia-Pacific

The Asia-Pacific region represents the most rapidly expanding market for military sensors, fueled by escalating territorial disputes, increasing defense budgets, and a drive for military self-sufficiency. China’s extensive modernization efforts and indigenous development programs are a primary catalyst, creating substantial demand for a wide array of sensor technologies. India’s large-scale procurement and ‘Make in India’ initiative are also major contributors to regional growth. Countries like Japan, South Korea, and Australia are actively investing in advanced ISR capabilities to counter regional threats, focusing on maritime domain awareness and integrated air defense systems. This dynamic environment, characterized by both competition and indigenous development, makes the Asia-Pacific Military Sensors Market a focal point for global suppliers and a hub for significant technological advancement and market growth in the coming years.

Middle East & Africa

The Military Sensors Market in the Middle East & Africa is primarily driven by high defense spending in the Gulf Cooperation Council countries, which are procuring advanced military hardware to address regional security challenges. There is a strong demand for sensors suited for harsh desert environments, including robust electro-optical/infrared systems for border surveillance and missile defense. The market is characterized by large-scale imports of sophisticated platforms from the U.S. and Europe, which come integrated with advanced sensor suites. In Africa, the market is more fragmented, with growth driven by peacekeeping operations and counter-insurgency efforts, creating demand for lighter, more portable sensor systems for infantry and unmanned aerial vehicles. Political instability and the need for maritime security in key waterways further influence procurement trends in this region.

South America

The South American Military Sensors Market is comparatively smaller but demonstrates steady growth focused on border security, counter-narcotics operations, and maritime patrol. Countries like Brazil, with its indigenous defense industry, lead regional developments, particularly in surveillance systems for its vast Amazon territory and offshore resources. Budget constraints are a limiting factor, leading to a focus on cost-effective upgrades and lifecycle extensions of existing platforms rather than large-scale new acquisitions. Regional collaborations for border monitoring and the need to combat illicit activities drive demand for ground surveillance radars, communication intelligence sensors, and coastal radar systems. While not a primary driver of global innovation, the market remains essential for regional security dynamics within the broader global Military Sensors Market landscape.

Report Scope

This market research report provides a comprehensive analysis of the Military Sensors Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of military sensors in enhancing defense capabilities across applications such as UAVs, spacecraft, missiles, and other defense systems.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, material innovations, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Military Sensors Market?

-> Military Sensors Market size was valued at USD 12.51 billion in 2024. The market is projected to grow from USD 13.15 billion in 2025 to USD 17.71 billion by 2032, exhibiting a CAGR of 5.1% during the forecast period.

Which key companies operate in Military Sensors Market?

-> Key players include Lockheed Martin, BAE Systems plc, Raytheon Company, Honeywell International Inc., China Electronics Technology Group Corporation, TE Connectivity Ltd., TransDigm Group, Aerospace Long March Launch Vehicle Technology CO.,LTD, and Curtiss-Wright Corporation, among others.

What are the key growth drivers?

-> Key growth drivers include advancements in military technology (MEMS, quantum sensors), increasing defense budgets, policy support for sensor R&D, and rising demand for intelligent sensors in modern defense systems.

Which region dominates the market?

-> North America is the largest market with 40% share, followed by Asia-Pacific (30%) and Europe (20%).

What are the emerging trends?

-> Emerging trends include integration of AI in sensor systems, quantum sensing technology, multifunctional sensor arrays, and international collaborations for technology sharing.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...