Memory Foundry Market Insights

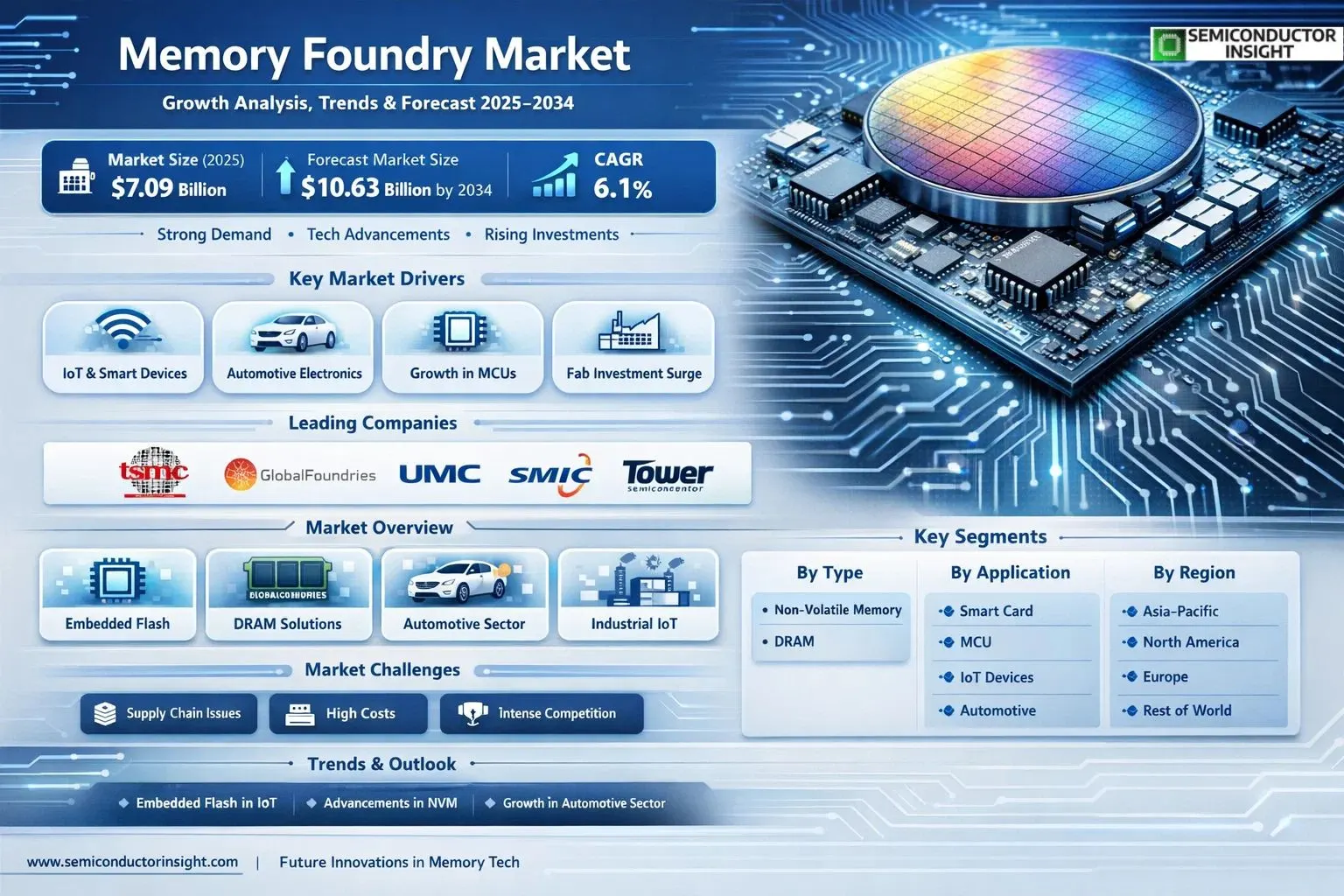

Global Memory Foundry market was valued at USD 7,087 million in 2025 and is projected to reach USD 10,630 million by 2034, exhibiting a CAGR of 6.1% during the forecast period

Memory foundries specialize in manufacturing memory products, covering DRAM processes and Flash processes. Embedded Flash (eFlash) memory serves as a key enabling technology for programmable semiconductor products that demand small form factors and low-power processing. For instance, microcontrollers rely on eFlash to store program instructions and data, with the updatability of code and data being essential. IoT devices leverage eFlash for smart, flexible, and secure operations, supporting wireless or over-the-air updates. This technology powers diverse applications, from smart cards and wearables to factory automation and autonomous vehicles. Key segments include Non-Volatile Memory (NVM) and DRAM processes.

The market is experiencing steady growth driven by surging demand in IoT applications, automotive electronics, and microcontroller units, alongside increased investments in semiconductor fabrication. Advancements in embedded memory technologies further propel expansion, enabling compact and efficient devices. Key players such as TSMC, GlobalFoundries, United Microelectronics Corporation (UMC), SMIC, Tower Semiconductor, PSMC, VIS (Vanguard International Semiconductor), Hua Hong Semiconductor, HLMC, and Samsung Foundry dominate with extensive portfolios and manufacturing capabilities.

MARKET DRIVERS

Surging Demand from AI and Hyperscale Data Centers

Memory Foundry Market is propelled by escalating requirements for high-bandwidth memory (HBM) in AI accelerators and GPUs. With global AI infrastructure investments exceeding $200 billion annually, foundries are ramping up production of HBM3 and upcoming HBM3E variants to meet throughput demands exceeding 1.2 TB/s per stack.

Growth in Mobile and Automotive Applications

Advancements in 5G-enabled smartphones and electric vehicles are fueling demand for low-power DDR5 and LPDDR5X memory solutions. The automotive sector alone anticipates a 25% compound annual growth rate through 2028, driven by ADAS and infotainment systems requiring robust, high-density memory chips.

➤ Industry projections indicate Memory Foundry Market will expand at over 12% CAGR, supported by NAND flash scaling to 200+ layers for enterprise SSDs.

Additionally, edge computing deployments are accelerating the need for embedded memory in IoT devices, positioning foundries to capture value in diversified portfolios beyond traditional servers.

MARKET CHALLENGES

Supply Chain Volatility and Raw Material Shortages

Memory Foundry Market faces persistent disruptions from semiconductor-grade silicon wafer shortages and rare earth dependencies. Recent events have led to 15-20% production delays, impacting delivery timelines for critical DRAM and NAND components.

Other Challenges

Intensifying Competition and Pricing Pressures

Leading players like Samsung and SK Hynix dominate with over 60% market share, squeezing margins for emerging foundries through aggressive pricing strategies amid cyclical oversupply phases.

Technological hurdles in scaling beyond 1z nm nodes further complicate yield optimization, with defect rates hovering at 5-10% for advanced processes, straining operational efficiencies across Memory Foundry Market.

Regulatory compliance for energy-efficient fabs adds compliance costs, estimated at 8% of capex, challenging smaller entrants.

MARKET RESTRAINTS

Escalating Capital Expenditures and Cyclicality

Building state-of-the-art Memory Foundry facilities demands investments surpassing $20 billion per fab, deterring new entrants and amplifying financial risks during downturns. The market’s inherent boom-bust cycles, with bit demand fluctuating 30-50% biennially, exacerbate underutilization.

Geopolitical tensions, including US-China trade restrictions on advanced equipment exports, limit technology access and force costly retooling, constraining global expansion in Memory Foundry Market.

Environmental regulations mandating net-zero emissions by 2030 impose retrofit expenses estimated at $5-10 billion industry-wide, slowing capacity additions and prioritizing sustainability over rapid scaling.

MARKET OPPORTUNITIES

High-Bandwidth Memory for AI and Emerging Tech

Memory Foundry Market stands to benefit from HBM4 development, targeting 2 TB/s bandwidth for next-gen AI training clusters, with demand projected to triple by 2027 as hyperscalers upgrade infrastructure.

Expansion into compute-in-memory architectures for neuromorphic chips offers differentiation, reducing data movement bottlenecks and appealing to edge AI applications in Memory Foundry Market.

Strategic partnerships for CXL-enabled memory pooling in data centers unlock $50 billion in addressable revenue, enabling foundries to provide disaggregated, scalable solutions amid cloud-native workloads.

Memory Foundry Market Trends

Embedded Flash Driving Innovation in IoT and Edge Computing

Embedded Flash (eFlash) memory serves as a foundational technology within Memory Foundry Market, enabling compact, low-power semiconductor solutions. Foundries specializing in eFlash production support microcontrollers that store program instructions and data, allowing essential updates for modern devices. In Memory Foundry Market, this capability fuels the development of smart, flexible products deployable across IoT ecosystems, where over-the-air updates enhance security and functionality. Applications span from wearables and smart cards to factory automation and autonomous vehicles, reflecting a shift toward integrated memory solutions that prioritize efficiency and adaptability.

Other Trends

Strengthening Non-Volatile Memory Processes

Non-Volatile Memory (NVM) segments in Memory Foundry Market continue to evolve, supporting persistent data storage without power. Foundries focus on refining NVM processes alongside DRAM, catering to demands from diverse applications. This trend underscores the market’s emphasis on reliable memory for embedded systems, where NVM’s endurance meets the needs of high-volume production in MCUs and IoT devices. Leading foundries invest in process optimizations to deliver superior performance, addressing challenges in scalability and cost-efficiency.

Growth in Automotive and Industrial Applications

Memory Foundry Market witnesses accelerated adoption in automotive sectors, driven by requirements for robust memory in advanced driver-assistance systems and electric vehicles. Foundries like TSMC, GlobalFoundries, UMC, SMIC, and Tower Semiconductor lead by providing specialized DRAM and Flash processes tailored for these high-reliability environments. Similarly, industrial IoT and factory automation benefit from eFlash integration, enabling real-time data processing and remote configurability. Regional dynamics, particularly in Asia with players such as VIS, Hua Hong, and HLMC, bolster supply chains, while North America and Europe emphasize innovation in secure memory solutions. This convergence of applications signals a broader trend toward diversified process technologies, enhancing the competitive landscape as manufacturers adapt to evolving demands in smart cards, MCUs, and beyond.

COMPETITIVE LANDSCAPEKey Industry Players

Leading Memory Foundry Manufacturers and Market Share Dynamics

Memory Foundry Market is characterized by a concentrated structure dominated by a few leading pure-play foundries and integrated device manufacturers (IDMs) offering advanced process technologies for DRAM and non-volatile memory (NVM) production. TSMC stands out as the preeminent leader, leveraging its cutting-edge nodes and massive capacity investments to capture significant revenue share, particularly in embedded flash (eFlash) for IoT, automotive, and MCU applications. GlobalFoundries and United Microelectronics Corporation (UMC) follow closely, focusing on specialty processes that cater to mature nodes essential for cost-sensitive memory segments. The top five players collectively command a substantial portion of the market, fostering an oligopolistic environment where scale, technological differentiation, and geographic proximity to key demand centers like Asia drive competitive advantages. Valued at approximately $7,087 million in 2025, the market’s projected growth to $10,630 million by 2034 at a 6.1% CAGR underscores the intensifying race for process leadership amid surging demand from smart cards, wearables, and autonomous systems.

Beyond the frontrunners, a robust ecosystem of niche players provides specialized capabilities in embedded memory foundry services, enhancing supply chain resilience. Companies like SMIC, Tower Semiconductor, and Powerchip Semiconductor Manufacturing Corporation (PSMC) excel in high-volume production for NVM and DRAM processes tailored to automotive and industrial IoT needs. Vanguard International Semiconductor (VIS), Hua Hong Semiconductor, and HLMC target regional strengths, particularly in China, with expertise in secure eFlash for OTA-updatable devices. Emerging challengers such as Samsung Foundry, Wuhan Xinxin, SK keyfoundry, and GTA Semiconductor further diversify the landscape, emphasizing innovations in low-power memory for MCUs and edge computing. These mid-tier firms navigate challenges like technological hurdles and geopolitical risks by forming strategic alliances and expanding capacity, ensuring a competitive balance that benefits end-users with varied technology options and pricing flexibility.

List of Key Memory Foundry Companies Profiled

- TSMC

- GlobalFoundries

- United Microelectronics Corporation (UMC)

- SMIC

- Tower Semiconductor

- PSMC

- VIS (Vanguard International Semiconductor)

- Hua Hong Semiconductor

- HLMC

- Samsung Foundry

- Wuhan Xinxin Semiconductor Manufacturing

- SK keyfoundry Inc.

- GTA Semiconductor Co., Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Non-Volatile Memory (NVM)

|

| By Application |

|

IoT Applications

|

| By End User |

|

Automotive

|

| By Process |

|

Flash Process

|

| By Technology |

|

Embedded Flash (eFlash)

|

Regional Analysis: Memory Foundry Market

Asia-Pacific

Asia-Pacific foundries pioneer cutting-edge nodes for memory chips, integrating EUV lithography to enhance density and speed. Innovations in 3D stacking address bandwidth bottlenecks, serving hyperscale data needs effectively.

Heavy capital inflows fund mega-fabs, expanding output for next-gen products. Public-private synergies drive sustainable scaling, fortifying Memory Foundry Market position amid global competition.

Localized raw material sourcing and diversified vendor networks mitigate risks, ensuring steady Memory Foundry Market supply. Advanced automation enhances operational agility in dynamic conditions.

World-class universities and vocational programs cultivate expertise in fab operations, sustaining innovation cycles. Cross-industry talent mobility strengthens Memory Foundry Market’s human capital edge.

North America

North America plays a pivotal role in Memory Foundry Market through innovation-driven strategies and headquarters of key players. Strong emphasis on R&D yields breakthroughs in specialty memories for automotive and edge computing. Proximity to tech ecosystems like Silicon Valley facilitates rapid prototyping and customer collaboration. Government incentives spur domestic fab constructions, aiming to diversify global dependencies. Challenges include higher operational costs, prompting efficiency-focused process optimizations. Strategic alliances with Asian partners enable technology access while building local capacity. The region’s focus on high-value niches, such as persistent memory, positions it for sustained influence despite scale limitations compared to Asia-Pacific leaders.

Europe

Europe advances steadily in Memory Foundry Market, leveraging regulatory frameworks that prioritize sustainability and data sovereignty. Specialized foundries target industrial IoT and automotive sectors with robust, low-power memory solutions. Collaborative EU-funded projects enhance yield improvements and green manufacturing practices. Skilled engineering talent drives customization for European OEMs, fostering loyalty. Infrastructure investments address capacity gaps, though energy costs pose hurdles. Emphasis on open standards promotes interoperability, aiding market penetration in smart grids and healthcare. Europe’s balanced approach integrates quality over volume, carving a niche amid competitive pressures.

South America

South America emerges as a nascent player in Memory Foundry Market, with growing electronics assembly driving local demand. Brazil and others invest in basic memory production to support consumer devices and agrotech. Partnerships with global foundries transfer know-how, building foundational capabilities. Infrastructure developments improve power reliability for fabs. Economic volatility encourages cost-effective strategies, focusing on mid-range products. Regional trade blocs facilitate exports, enhancing viability. Gradual workforce upskilling promises long-term competitiveness in Memory Foundry Market.

Middle East & Africa

Middle East & Africa show promise in Memory Foundry Market via diversification from oil economies. Gulf states fund advanced facilities for data center memories, leveraging energy abundance. Africa’s telecom boom spurs NAND demand, attracting pilot projects. Government visions for tech hubs draw FDI, establishing initial capacities. Logistical improvements and talent initiatives bridge gaps. Focus on resilient, heat-tolerant chips suits harsh climates. Strategic positioning taps into digital transformation waves across Memory Foundry Market landscape.

Report Scope

This market research report provides a comprehensive analysis of the Memory Foundry Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Memory Foundry Market?

-> Memory Foundry Market was valued at USD 7,087 million in 2025 and is expected to reach USD 10,630 million by 2034, at a CAGR of 6.1% during the forecast period.

Which key companies operate in Memory Foundry Market?

-> Key players include TSMC, GlobalFoundries, United Microelectronics Corporation (UMC), SMIC, Tower Semiconductor, PSMC, VIS (Vanguard International Semiconductor), Hua Hong Semiconductor, HLMC, and Samsung Foundry, among others.

What are the key growth drivers?

-> Key growth drivers include demand for embedded flash (eFlash) memory in microcontrollers, IoT devices, smart cards, wearables, factory automation, and autonomous vehicles, enabling low-power processing and over-the-air (OTA) updates.

Which region dominates the market?

-> Asia dominates the market, driven by key manufacturers in China, Japan, South Korea, and Taiwan, while North America holds significant share.

What are the emerging trends?

-> Emerging trends include advancements in Non-Volatile Memory (NVM) and DRAM processes, integration in IoT applications, automotive, and MCU segments for smart, secure, and flexible semiconductor products.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...