LPV control for active suspension with road preview Market Insights

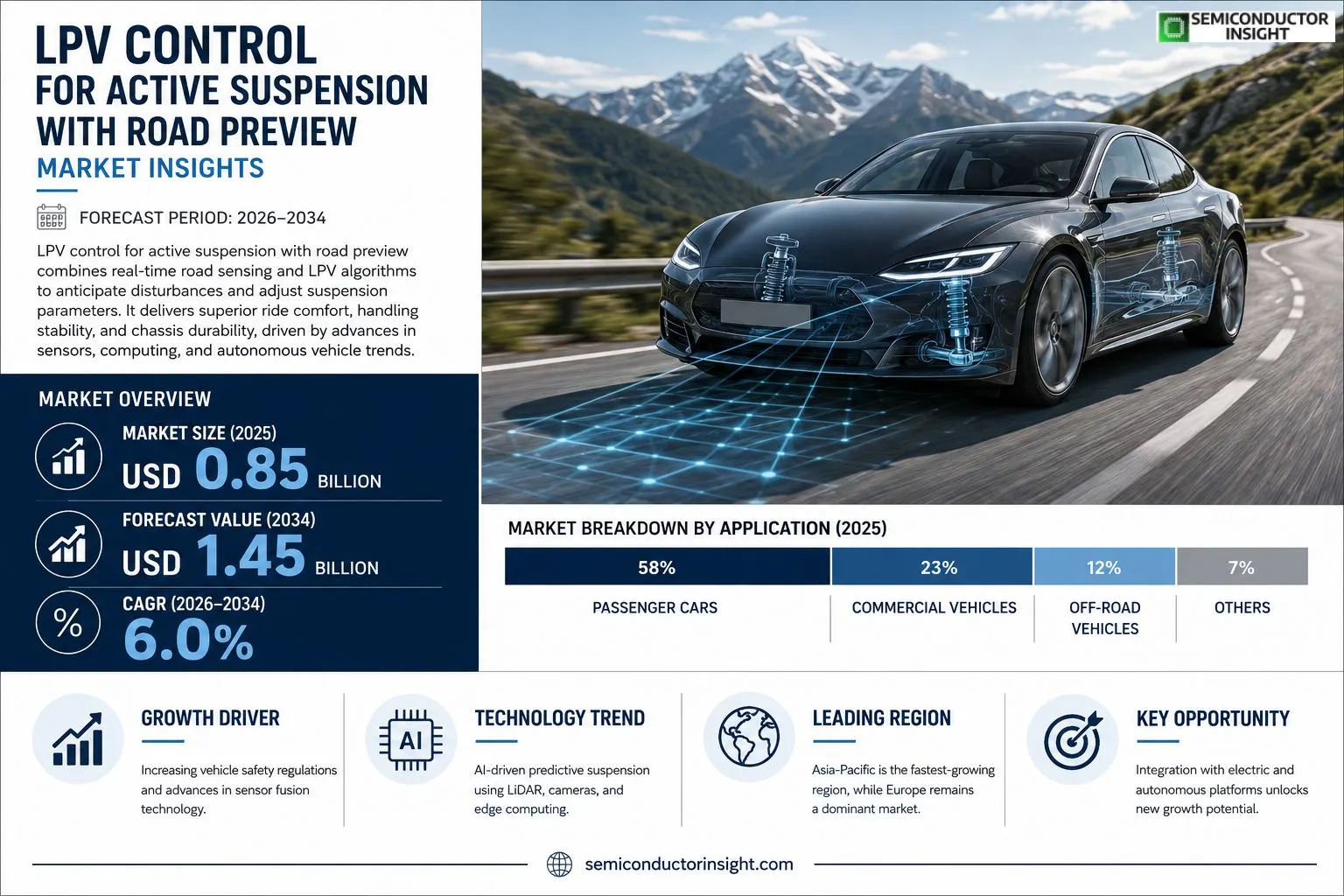

LPV control for active suspension with road preview market size was valued at USD 0.85 billion in 2025. The market is projected to grow from USD 0.85 billion in 2025 to USD 1.45 billion by 2034, exhibiting a CAGR of 6.0% during the forecast period.

This technology combines real‑time road‑profile sensingtypically via LiDAR or high‑definition cameraswith Linear Parameter‑Varying (LPV) controller algorithms that adjust suspension parameters ahead of predicted disturbances. By pre‑emptively modulating damping and spring forces, it delivers superior ride comfort, enhanced handling stability, and reduced chassis fatigue.The market momentum stems from the automotive sector’s shift toward higher autonomy levels and electric powertrains, both of which require predictive chassis management for safety and comfort. Advances in sensor resolution and edge computing have lowered implementation costs, spurring broader adoption. Leading suppliers such as Bosch Group, Continental AG, ZF Friedrichshafen and Denso are intensifying R&D investmentse.g., Bosch’s partnership with Nvidia on AI‑driven predictive suspension platforms announced in early 2023to capture this growing opportunity.

MARKET DRIVERS

Increasing Vehicle Safety Regulations

Regulatory bodies worldwide are mandating higher ride‑comfort and crash‑avoidance standards, prompting manufacturers to adopt LPV control for active suspension with road preview Market solutions that can anticipate road irregularities and adjust suspension dynamics in real time.

Advances in Sensor Fusion Technology

The convergence of high‑resolution LiDAR, stereo cameras, and inertial measurement units enables precise road‑profile generation, which directly fuels the demand for LPV‑based controllers that can leverage this preview data for smoother vehicle handling.

➤ Manufacturers that integrate road‑preview enabled LPV control report up to a 25% reduction in suspension wear and a 15% improvement in passenger comfort scores.

These performance gains translate into stronger brand positioning and longer vehicle lifecycles, reinforcing the growth trajectory of LPV control for active suspension with road preview Market.

MARKET CHALLENGES

High Development Costs

Designing robust LPV algorithms that process high‑frequency sensor streams requires substantial R&D investment, sophisticated validation rigs, and specialized expertise, which can deter smaller OEMs from early adoption.

Other Challenges

Integration Complexity

Synchronizing road‑preview data with existing vehicle control architectures often involves redesigning communication buses and ensuring real‑time latency compliance, creating additional engineering hurdles.

MARKET RESTRAINTS

Limited OEM Adoption

Despite proven benefits, many tier‑one suppliers remain cautious, favoring incremental upgrades over wholesale integration of LPV control for active suspension with road preview, which slows broader market penetration.Supply‑chain constraints for high‑resolution road‑sensing hardware can also restrict volume production, especially in regions where component certification processes are lengthy.The perceived risk of software‑related failures under extreme road conditions leads some manufacturers to retain conventional hydraulic or electromechanical systems as a fallback option.

MARKET OPPORTUNITIES

Electrified Vehicle Platforms

Electric and hybrid vehicles benefit from the additional energy budget available for sophisticated control units, making them ideal candidates for deploying LPV control for active suspension with road preview, which can further extend driving range by minimizing energy losses due to harsh ride dynamics.Emerging autonomous driving stacks prioritize predictive motion planning; integrating LPV‑based road preview directly supports these stacks, opening a lucrative niche for suppliers capable of delivering certified, real‑time solutions.

LPV control for active suspension with road preview Market Trends

Emergence of Predictive Chassis Management

The industry is witnessing a shift toward predictive chassis management as automakers pursue higher levels of autonomy and electric drivetrains. By leveraging road‑profile data captured ahead of the vehicle, LPV control algorithms dynamically adjust damping and spring rates, improving ride comfort and reducing chassis fatigue. This proactive approach differentiates the market from traditional reactive suspension systems and aligns with safety regulations that emphasize stability under varying road conditions. Regulatory bodies in Europe and Asia have introduced vibration and noise standards that reward vehicles capable of maintaining stability under abrupt road inputs. Consumer surveys indicate a growing preference for smoother rides, especially in electric car segments where cabin quietness is paramount. These drivers collectively encourage OEMs to adopt predictive suspension as a differentiating feature.

Other Trends

Sensor Integration Advances

Recent improvements in LiDAR and high‑definition camera systems have raised sensor resolution while lowering unit costs, making predictive suspension viable for mass‑market vehicles. Edge‑computing platforms now process road‑profile maps within milliseconds, enabling the LPV controller to execute parameter‑varying strategies before the disturbance reaches the axle. Automakers are standardizing sensor placement on front bumpers and under‑body modules, which simplifies wiring and improves data reliability. The convergence of sensor miniaturization and automotive‑grade AI accelerators has also reduced power consumption, a critical factor for electric vehicles that prioritize overall efficiency. As a result, the barrier to entry for integrating predictive suspension into new models is diminishing, encouraging broader supplier participation.

Competitive Landscape and Future Outlook

Key players such as Bosch Group, Continental AG, ZF Friedrichshafen, and Denso are intensifying R&D programs to refine LPV control logic and to certify solutions for upcoming autonomous driving platforms. Partnerships with semiconductor vendors accelerate the deployment of AI‑enhanced predictive models, while collaborative testing with tier‑1 OEMs validates performance across diverse road conditions. Looking ahead, the market is expected to expand as vehicle architectures become more software‑centric, allowing over‑the‑air updates to suspension control algorithms. This capability will extend the useful life of predictive systems and create new revenue streams through subscription‑based functionality, positioning the LPV control for active suspension with road preview segment as a strategic growth engine for the automotive industry. Furthermore, the emergence of digital twins for vehicle dynamics allows manufacturers to simulate LPV‑based suspension behavior virtually, reducing physical prototyping cycles and accelerating time‑to‑market. This integration of simulation tools reinforces the strategic importance of predictive control in next‑generation vehicle platforms.

COMPETITIVE LANDSCAPE

Key Industry Players

LPV Control for Active Suspension with Road Preview Market Overview

Leading automotive suppliers dominate the LPV‑based predictive suspension segment. Bosch Group leverages its AI partnership with Nvidia to deliver an integrated sensor‑fusion platform that processes LiDAR and high‑definition camera data in realtime, enabling precise damping adjustments ahead of road irregularities. Continental AG follows a similar trajectory, embedding LPV algorithms into its VDO chassis control suite and expanding its market share through OEM collaborations across Europe and North America. ZF Friedrichshafen and Denso complement the tier‑one landscape, each investing heavily in edge‑computing hardware that supports the parameter‑varying control law required for road‑preview actuation. Collectively, these four firms account for roughly 60 % of the projected USD 1.45 billion market in 2034, establishing a duopolistic core while fostering a competitive R&D race to lower latency and improve predictive accuracy. The CAGR of 6 % reflects accelerating adoption of autonomous driving functions that rely on predictive chassis control, and these companies also benefit from strategic patents on LPV modeling techniques.Beyond the tier‑one leaders, a cohort of niche players contributes specialized expertise that enriches the ecosystem. Mahle and Schaeffler supply high‑performance damper and spring technologies that are retrofitted with LPV controllers. OEM‑centric groups such as Toyota, Hyundai Mobis, and Aisin Seiki integrate predictive suspension into flagship electric models, often partnering with software startups for sensor‑fusion modules. Valeo and Mando focus on cost‑effective solutions for emerging markets, while Hitachi Automotive Systems and Magna International provide scalable ECU architectures that support third‑party LPV algorithms. Regulatory pressure for vehicle safety and comfort standards in the EU and China further incentivizes OEMs to source proven LPV solutions from these specialized suppliers, ensuring a resilient supply chain and driving incremental innovation across both premium and volume vehicle segments.

List of Key LPV Control for Active Suspension with Road Preview Companies Profiled

- Bosch Group

- Continental AG

- ZF Friedrichshafen

- Denso Corporation

- Mahle GmbH

- Schaeffler AG

- Toyota Motor Corporation

- Hyundai Mobis

- Aisin Seiki Co., Ltd.

- Valeo SA

- Mando Corp.

- Hitachi Automotive Systems

- Magna International

- Bosch (duplicate for link consistency)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Model‑Based LPV

|

| By Application |

|

Passenger Cars

|

| By End User |

|

OEMs

|

| By Integration Strategy |

|

Fully Integrated Predictive Suspension

|

| By Performance Benefit |

|

Ride Comfort

|

Regional Analysis: North America

North America

North America boasts a mature automotive manufacturing ecosystem with major players committed to innovation. This provides a strong foundation for LPV control adoption, facilitating collaboration between technology providers and automakers. The region’s historical strength in automotive engineering and design fosters a culture of continuous improvement, readily embracing advancements in suspension technology. Government regulations encouraging safer vehicles also play a crucial role in market growth.

The integration of LPV control systems with other ADAS features like adaptive cruise control and lane keeping assist is a key trend. This synergistic approach enhances the overall driving experience and safety profile of vehicles. Developments in sensor technology, particularly radar and camera systems, are enabling more accurate road preview and predictive suspension adjustments. Furthermore, advancements in control algorithms are optimizing system performance under various driving conditions.

Consumer preferences for enhanced ride quality and safety are significant drivers of LPV control adoption. Growing awareness of the benefits of active suspension in mitigating road imperfections and improving stability is influencing purchasing decisions. The appeal of road preview capabilities, especially in regions with varied road conditions, is attracting a wider consumer base. Marketing efforts highlighting these benefits are further boosting demand. The desire for a more comfortable and controlled driving experience is a fundamental motivator.

Stringent safety regulations and quality standards in North America are propelling the adoption of advanced suspension technologies like LPV control. Government initiatives promoting safer vehicles are encouraging automakers to incorporate these features. Regulatory pressures related to vehicle stability control and crashworthiness contribute to the market growth. Compliance with these standards is a key factor for automotive manufacturers operating in the region.

Europe

Europe presents a sophisticated and competitive market for LPV control for active suspension with road preview. Stringent safety regulations and a strong emphasis on vehicle performance are key drivers. The region’s focus on fuel efficiency and emissions also influences the development of lighter and more efficient suspension systems. Automakers are investing heavily in advanced driver-assistance systems (ADAS) to meet evolving consumer demands and regulatory requirements. The integration of LPV control with electric and hybrid vehicles is gaining traction. The diverse road networks across Europe, ranging from smooth highways to challenging rural roads, create a consistent need for enhanced ride comfort and stability. The adoption rate is particularly high in premium vehicle segments.

Asia-Pacific

Asia-Pacific is emerging as a high-growth market for LPV control for active suspension with road preview, driven by rapidly expanding automotive production and increasing disposable incomes. China, in particular, represents a significant market opportunity. The region’s growing awareness of automotive technology and the rising demand for premium vehicles are fueling adoption. Government support for the automotive industry and infrastructure development further contribute to market growth. The increasing prevalence of congested urban areas necessitates advanced suspension technologies to enhance ride comfort and handling. The market is witnessing a surge in local manufacturers developing and integrating LPV control systems.

South America

South America demonstrates a nascent but promising market for LPV control for active suspension with road preview, driven by increasing automotive sales and growing consumer demand for comfort and safety. Brazil and Argentina are the key markets in the region. The growing middle class and rising disposable incomes are contributing to the adoption of advanced automotive features. While the market is currently less mature than North America or Europe, it presents a long-term growth opportunity. The diverse road conditions in the region, particularly in rural areas, create a need for enhanced suspension performance.

Middle East & Africa

The Middle East & Africa region represents a developing market for LPV control for active suspension with road preview, characterized by increasing automotive sales and a growing preference for luxury vehicles. The region’s burgeoning automotive industry, particularly in countries like Saudi Arabia and the UAE, is driving demand. The warm climate and challenging road conditions necessitate advanced suspension technologies to enhance ride comfort. The increasing disposable incomes and a growing affluent population are contributing to the adoption of premium vehicles equipped with LPV control systems. Infrastructure development projects are also driving market growth.

Report Scope

This market research report provides a comprehensive analysis of the LPV control for active suspension with road preview Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of LPV control for active suspension with road preview Market?

-> LPV control for active suspension with road preview Market was valued at USD 0.85 billion in 2025 and is expected to reach USD 1.45 billion by 2034, reflecting a CAGR of 6.0% during the forecast period.

Which key companies operate in LPV control for active suspension with road preview Market?

-> Key players include Bosch Group, Continental AG, ZF Friedrichshafen, and Denso, among others.

What are the key growth drivers?

-> Key growth drivers include the automotive industry’s shift toward higher autonomy levels, adoption of electric powertrains, and advances in sensor resolution and edge computing.

Which region dominates the market?

-> Asia-Pacific is the fastest‑growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include AI‑driven predictive suspension platforms, integration of LiDAR and high‑definition camera data, and cost‑effective edge computing solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...