Low- to Mid-Range Intelligent Driving Chips Market Insights

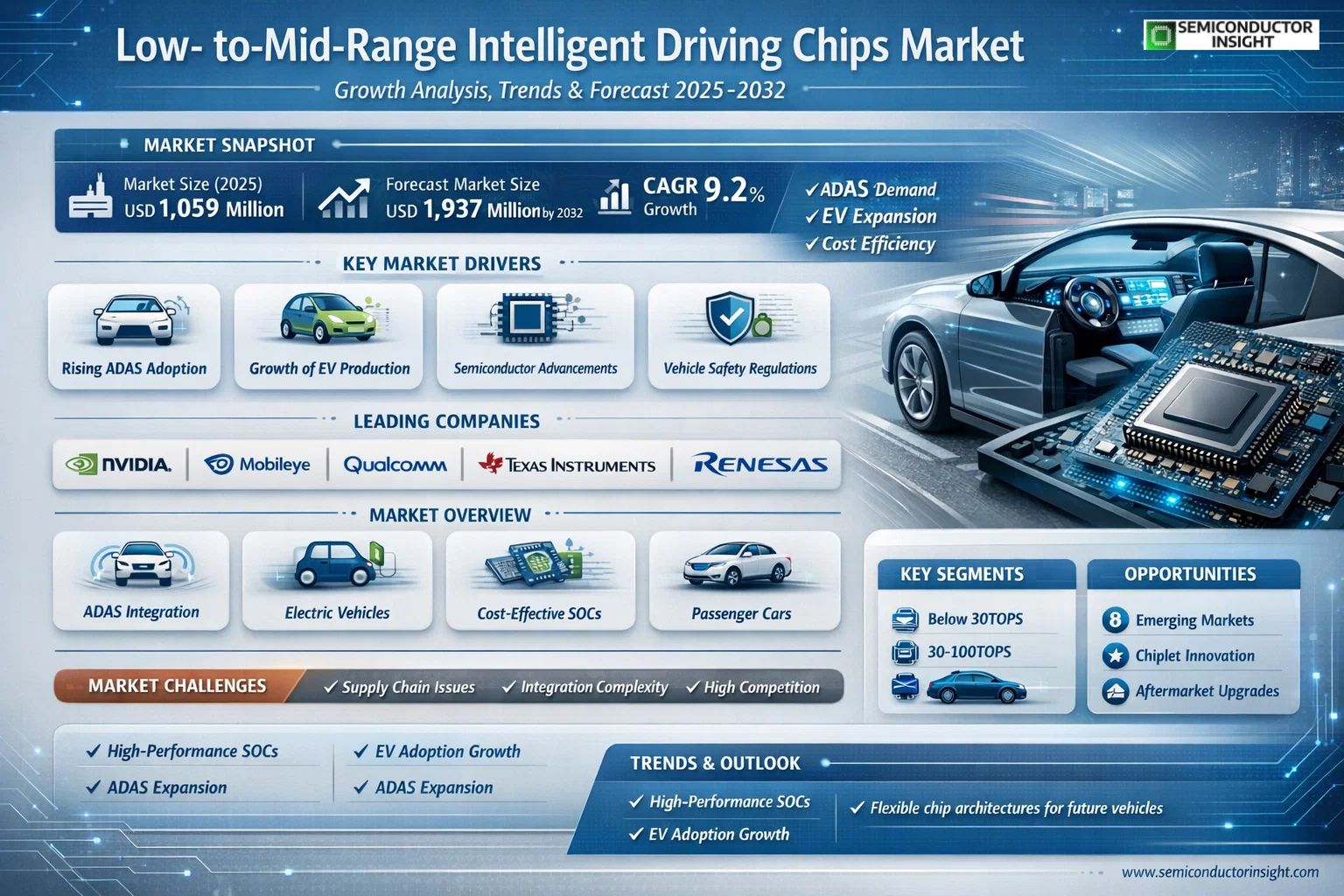

Global Low- to Mid-Range Intelligent Driving Chips market was valued at USD 1,059 million in 2025. The market is projected to reach USD 1,937 million by 2032, exhibiting a CAGR of 9.2% during the forecast period.

Low- to Mid-Range Intelligent Driving Chips refer to intelligent driving chips with a computing power below 100TOPS. They are usually composed of high-performance SOCs (system-on-chips) and integrate multiple processors such as CPUs and GPUs to meet different computing power requirements. Below the 30TOPS dividing line is a low-level intelligent driving chip, and between 30-100TOPS is a mid-range intelligent driving chip.

The market is experiencing rapid growth due to several factors, including surging demand for advanced driver assistance systems (ADAS), expansion of electric vehicle production, and regulatory pushes for vehicle safety features. Furthermore, advancements in cost-effective semiconductor technologies enable broader adoption in mass-market vehicles. Initiatives by key players are fueling further expansion. Nvidia, Mobileye, Qualcomm, Texas Instruments, Renesas, Horizon Robotics, and Black Sesame Technologies are some of the key players operating in the market with diverse portfolios.

MARKET DRIVERS

Rising Adoption of ADAS in Mass-Market Vehicles

Low- to Mid-Range Intelligent Driving Chips Market is propelled by increasing integration of advanced driver assistance systems (ADAS) in entry-level and mid-segment passenger vehicles. Automakers are prioritizing Level 2 autonomy features like adaptive cruise control and lane-keeping assistance to meet consumer demand for enhanced safety without premium pricing. Global vehicle production incorporating these chips reached approximately 15 million units in 2023, reflecting a 22% year-over-year growth driven by regulatory mandates in regions like Europe and China.

Cost Reductions in Chip Manufacturing

Advancements in process nodes, such as 7nm and 5nm technologies tailored for low- to mid-range applications, have significantly lowered production costs, making intelligent driving chips viable for broader market penetration. This has enabled suppliers to offer solutions priced 30-40% lower than high-end counterparts, fostering partnerships with OEMs targeting volume sales in emerging economies. The scalability of these chips supports hybrid architectures combining CPUs, GPUs, and NPUs optimized for real-time perception tasks.

➤ Market projections indicate Low- to Mid-Range Intelligent Driving Chips Market will expand at a 28% CAGR through 2030, fueled by electrification trends in affordable EVs.

Furthermore, government incentives for intelligent transportation systems amplify demand, as chips enable features compliant with safety standards like Euro NCAP 5-star ratings, positioning the market for sustained momentum.

MARKET CHALLENGES

Supply Chain Vulnerabilities

Low- to Mid-Range Intelligent Driving Chips Market faces persistent supply chain disruptions, exacerbated by geopolitical tensions and raw material shortages for semiconductors. In 2023, lead times for critical components extended to 6-9 months, impacting production ramps for major automakers and delaying ADAS deployments in mid-range models.

Other Challenges

Integration Complexity

Melding low- to mid-range chips with diverse vehicle ECUs demands extensive validation, often resulting in 20-25% higher engineering costs and prolonged time-to-market. Compatibility issues with legacy systems in older platforms further complicate adoption.

Heightened competition from established players intensifies pricing pressures, while talent shortages in AI algorithm optimization hinder innovation pace across the value chain.

MARKET RESTRAINTS

Regulatory and Certification Hurdles

Strict safety regulations, including ISO 26262 ASIL-B/D compliance, impose rigorous testing on low- to mid-range intelligent driving chips, escalating development expenses by up to 35%. Delays in type approvals from bodies like NHTSA and China’s MIIT slow market entry, particularly for cross-border deployments.

Performance limitations in edge computing scenarios, such as adverse weather conditions, restrict chip efficacy compared to premium segments, capping adoption in safety-critical applications. Limited thermal management in compact designs also poses reliability concerns under prolonged high-load operations.

Intellectual property disputes and ecosystem fragmentation among fabless designers further restrain scalability, as standardized interfaces remain underdeveloped for mid-range solutions.

MARKET OPPORTUNITIES

Expansion into Emerging Markets

Low- to Mid-Range Intelligent Driving Chips Market holds substantial potential in Asia-Pacific and Latin America, where mid-segment vehicle sales are surging at 18% annually. Localized manufacturing and tailored features for regional road conditions could capture 40% additional market share by 2028.

Shift toward chiplet-based architectures promises modular, cost-effective upgrades, enabling OEMs to future-proof platforms without full redesigns. Collaborations with Tier-1 suppliers for V2X integration open avenues for enhanced connectivity in urban mobility fleets.

Additionally, aftermarket retrofitting for existing vehicles presents a $2.5 billion opportunity, driven by software-defined vehicle trends and over-the-air updates optimizing low- to mid-range chip performance.

Low- to Mid-Range Intelligent Driving Chips Market Trends

Integration of High-Performance SOCs Driving Efficiency

Low- to Mid-Range Intelligent Driving Chips Market is witnessing significant evolution through the integration of high-performance system-on-chips (SOCs) that combine CPUs and GPUs to deliver computing power under 100TOPS. These chips, categorized as low-range below 30TOPS and mid-range between 30-100TOPS, are enabling more accessible advanced driver assistance systems (ADAS) in vehicles, enhancing real-time processing for features like adaptive cruise control and lane-keeping assistance without the complexity of high-end solutions.

Other Trends

Expansion in Passenger Vehicle Applications

Low- to Mid-Range Intelligent Driving Chips Market shows strong momentum in passenger vehicles, where demand for cost-effective intelligent driving solutions is accelerating adoption. Manufacturers are prioritizing these chips to support Level 2+ autonomy, balancing performance and affordability amid rising consumer expectations for safety features.

Growth in Commercial Vehicle Segments

In commercial vehicles, Low- to Mid-Range Intelligent Driving Chips Market trends indicate a shift towards robust SOC designs for fleet management and logistics, improving operational efficiency through predictive maintenance and collision avoidance tailored to mid-range computing needs.

Regional Dynamics and Competitive Landscape

Asia, particularly China, is emerging as a pivotal hub in Low- to Mid-Range Intelligent Driving Chips Market, with local players like Horizon Robotics and Black Sesame Technologies challenging global leaders such as Nvidia, Mobileye, and Qualcomm. This competition fosters innovation in chip architectures, while North America and Europe focus on regulatory-compliant integrations, driving overall market maturation through diverse regional demands and strategic partnerships.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Overview of Top Manufacturers in Low- to Mid-Range Intelligent Driving Chips

Low- to Mid-Range Intelligent Driving Chips Market, defined by computing power below 100 TOPS, is dominated by a few semiconductor leaders such as Nvidia, Mobileye, and Qualcomm, which collectively hold a substantial revenue share among the global top five players in 2025. These companies provide high-performance SoCs integrating CPUs, GPUs, and specialized AI accelerators tailored for L2+ ADAS and basic autonomous driving in passenger and commercial vehicles. The market structure remains concentrated yet competitive, with established players leveraging extensive ecosystems, automotive partnerships, and scalable architectures to capture demand in regions like North America, Europe, and Asia. Nvidia’s Jetson and Drive Orin variants, Mobileye’s EyeQ series, and Qualcomm’s Snapdragon Ride platforms exemplify optimized solutions below 100 TOPS, driving market growth projected at a 9.2% CAGR to US$1937 million by 2032.

Beyond the frontrunners, niche and emerging players like Horizon Robotics, Black Sesame Technologies, Texas Instruments, and Renesas are carving significant positions, particularly in cost-sensitive segments such as below-30 TOPS chips for entry-level applications. Chinese firms Horizon Robotics and Black Sesame Technologies are rapidly expanding in Asia-Pacific, offering Journey and Huashan series chips with competitive pricing and localization advantages. Established suppliers including NXP Semiconductors, STMicroelectronics, and Ambarella contribute specialized automotive-grade processors focused on vision processing and sensor fusion, while HiSilicon and SemiDrive target regional OEMs. This diverse competitive landscape fosters innovation amid challenges like supply chain constraints and regulatory demands for safety-certified chips.

List of Key Low- to Mid-Range Intelligent Driving Chips Companies Profiled

- Nvidia

- Mobileye

- Qualcomm

- Texas Instruments

- Renesas

- Horizon Robotics

- Black Sesame Technologies

- NXP Semiconductors

- STMicroelectronics

- Ambarella

- HiSilicon

- SemiDrive Technologies

- Canaan Inc.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

30-100TOPS

|

| By Application |

|

Passenger Vehicle

|

| By End User |

|

Passenger Car OEMs

|

| By Autonomy Level |

|

Level 2+

|

| By Chip Architecture |

|

GPU-Accelerated

|

Regional Analysis: Low- to Mid-Range Intelligent Driving Chips Market

Asia-Pacific

Leading players in Asia-Pacific concentrate on versatile low- to mid-range intelligent driving chips, integrating AI accelerators for efficient perception tasks. Firms emphasize modular designs compatible with diverse vehicle architectures, driving economies of scale in high-volume production.

Mass-market adoption surges as automakers embed these chips in entry-level models for features like adaptive cruise control and lane-keeping. Regional fleets prioritize affordability, spurring growth in aftermarket upgrades and fleet retrofits.

Robust domestic sourcing minimizes disruptions, with fabs scaling output for radar and vision processors. Partnerships with foundries ensure steady supply of mid-range nodes, balancing cost and performance for intelligent driving applications.

R&D targets energy-efficient architectures for extended battery life in EVs, alongside over-the-air update compatibility. Emphasis on software-defined vehicles enhances chip longevity and adaptability in Low- to Mid-Range Intelligent Driving Chips Market.

North America

North America exhibits steady growth in Low- to Mid-Range Intelligent Driving Chips Market, fueled by tech-savvy consumers and stringent safety regulations. Automakers integrate these chips into mainstream sedans and SUVs, emphasizing reliable ADAS functionalities like automatic emergency braking. Innovation hubs in Silicon Valley collaborate with Detroit OEMs, developing chips with superior cybersecurity features. The market benefits from strong venture funding for next-gen processors, though higher development costs temper rapid scaling. Focus remains on interoperability with existing fleets, supporting gradual autonomy upgrades. Supply chain diversification mitigates risks, positioning the region as a quality leader despite intense global competition.

Europe

Europe advances cautiously in Low- to Mid-Range Intelligent Driving Chips Market, prioritizing compliance with Euro NCAP standards and emissions goals. German and French manufacturers lead deployments in compact vehicles, favoring chips with precise localization for urban navigation. Collaborative EU initiatives drive standardization, enhancing cross-border compatibility. The emphasis on sustainable manufacturing attracts investments in low-power designs. Challenges include fragmented regulations, yet premium engineering expertise ensures high reliability, fostering trust among consumers and paving the way for broader intelligent driving adoption.

South America

South America shows emerging potential in Low- to Mid-Range Intelligent Driving Chips Market, driven by rising middle-class demand for safer vehicles. Brazil and Mexico host assembly plants adopting cost-sensitive chips for basic ADAS in pickups and city cars. Local partnerships with Asian suppliers accelerate technology transfer, addressing infrastructure limitations. Government incentives for road safety bolster market entry, though economic volatility poses hurdles. Incremental integrations focus on affordability, gradually elevating regional intelligent driving capabilities.

Middle East & Africa

The Middle East & Africa region lags but gains traction in Low- to Mid-Range Intelligent Driving Chips Market via Gulf diversification efforts and African urbanization. Luxury fleets in the UAE incorporate advanced chips, trickling down to mid-range models. Harsh climates demand rugged designs with thermal resilience. Investments in smart city projects spur demand, while import dependencies highlight localization needs. Strategic alliances promise future growth, tailoring solutions for diverse terrains and enhancing regional mobility safety.

Report Scope

This market research report provides a comprehensive analysis of Low- to Mid-Range Intelligent Driving Chips Market, covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Low- to Mid-Range Intelligent Driving Chips Market?

-> Global Low- to Mid-Range Intelligent Driving Chips market was valued at USD 1,059 million in 2025 and is expected to reach USD 1,937 million by 2032, at a CAGR of 9.2% during the forecast period.

Which key companies operate in Low- to Mid-Range Intelligent Driving Chips Market?

-> Key players include Nvidia, Mobileye, Qualcomm, Texas Instruments, Renesas, Horizon Robotics, Black Sesame Technologies, among others.

What are the key growth drivers?

-> Key growth drivers include demand for advanced driver assistance systems, growth in passenger and commercial vehicles, and advancements in SOC technology integrating CPUs and GPUs.

Which region dominates the market?

-> Asia is the fastest-growing region, while China holds a significant market share.

What are the emerging trends?

-> Emerging trends include development of low-range (<30 TOPS) and mid-range (30-100 TOPS) chips, focus on cost-effective intelligent driving solutions, and expansion in automotive applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...