MARKET INSIGHTS

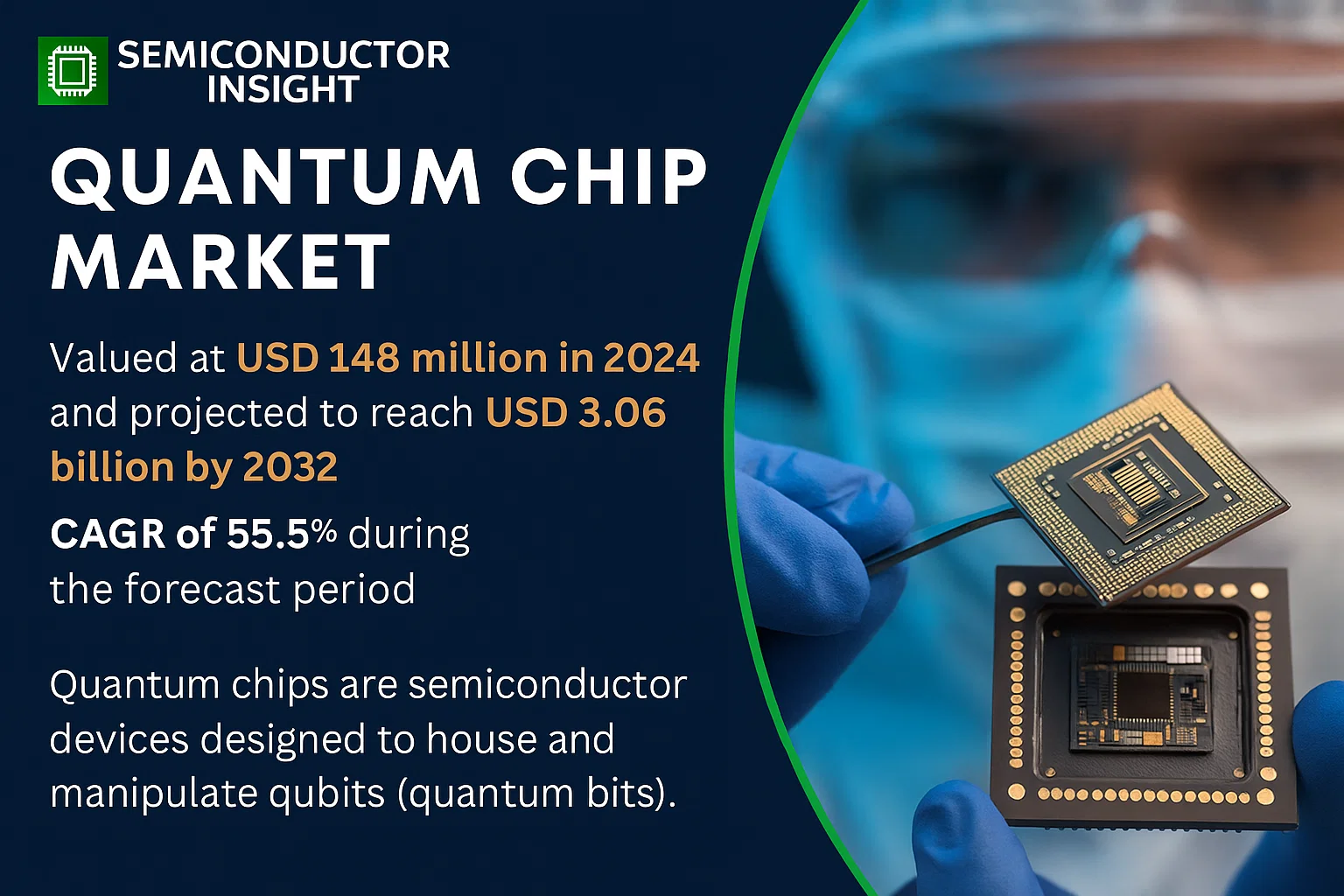

Global Quantum Chip Market was valued at USD 148 million in 2024 and is projected to reach USD 3.06 billion by 2032, exhibiting a CAGR of 55.5% during the forecast period.

Quantum chips are semiconductor devices that serve as the core hardware for quantum computing. They are designed to house and manipulate qubits (quantum bits), which are the fundamental units of information in quantum computing. Unlike classical bits, qubits can exist in multiple states simultaneously (superposition) and can be entangled with one another, enabling quantum computers to solve certain types of problems much faster than classical computers.

The market growth is driven by increasing investments in quantum computing research and development from both government entities and private corporations. Advancements in quantum algorithms and error correction techniques are making quantum computers more practical. The rise of cloud-based quantum computing services (Quantum-as-a-Service) is making this technology accessible to a wider range of users. Additionally, strategic partnerships between technology companies and research institutions are accelerating commercialization.

However, the market faces challenges such as the extremely high cost of developing and maintaining quantum computers, which require cryogenic cooling systems. There is also a significant shortage of skilled professionals with expertise in both quantum physics and computer science. Intense competition among key players could lead to market fragmentation.

MARKET DRIVERS

Exponential Growth in Demand for High-Performance Computing

The global quantum chip market is primarily driven by the escalating demand for computational power that surpasses the capabilities of classical supercomputers. Industries such as pharmaceuticals, finance, and materials science are investing heavily in quantum computing to solve complex optimization problems, perform advanced molecular simulations, and develop new drugs. Major technology firms and venture capital are pouring billions into quantum research annually, accelerating the transition from theoretical research to tangible hardware development.

Government and Defense Investments

Significant government initiatives worldwide are providing a substantial push to the market. For instance, national programs like the United States’ National Quantum Initiative and the European Union’s Quantum Flagship are allocating multi-billion-dollar budgets to fund research and development. These investments are aimed at achieving quantum advantage in areas of national security, cryptography, and strategic technological leadership, creating a stable and funded ecosystem for quantum chip manufacturers.

➤ Technological breakthroughs in qubit stability and error correction techniques are consistently reducing the error rates in quantum processors, marking a critical step towards building fault-tolerant quantum computers.

Furthermore, the rapid pace of technological innovation in qubit fabrication, such as the development of more stable superconducting qubits and trapped ions, is enabling the production of quantum chips with higher qubit counts and longer coherence times. This progress is directly fueling commercial interest and prototype development for practical applications.

MARKET CHALLENGES

Extreme Technical and Environmental Requirements

The fabrication and operation of quantum chips present immense technical hurdles. Qubits are notoriously fragile and require operating temperatures near absolute zero, typically achieved with complex and expensive dilution refrigerators. Maintaining this cryogenic environment and shielding the chips from the slightest electromagnetic interference is a significant engineering challenge that increases the cost and complexity of quantum computing systems.

Other Challenges

High Development Costs and Specialized Talent Shortage

The research and development cycle for quantum chips is exceptionally capital-intensive, often requiring billions in investment before reaching commercial viability. Compounding this is a critical global shortage of specialists with expertise in quantum physics, materials science, and advanced chip design, which slows down innovation and scaling efforts.

Scalability and Integration Issues

Scaling quantum processors from dozens to millions of qubits, as required for practical applications, remains a fundamental challenge. Interconnecting a large number of qubits while maintaining their quantum state (coherence) and managing crosstalk is a monumental task that current chip architectures are still struggling to overcome.

MARKET RESTRAINTS

Absence of a Clear Commercial “Killer Application”

A major factor restraining broader market growth is the current lack of a definitive, large-scale commercial application that demonstrably provides a quantum advantage over classical computing for everyday business problems. While promising for specific scientific tasks, quantum computing has yet to prove its economic value for mainstream enterprise applications, which limits immediate commercial investment and adoption beyond research institutions and well-funded tech giants.

Intellectual Property and Export Control Hurdles

The market is also constrained by stringent intellectual property regimes and international export controls, particularly concerning quantum technologies with potential dual-use (civilian and military) applications. These regulations can hinder global collaboration, slow down the pace of innovation, and create barriers to entry for companies operating across different national jurisdictions.

MARKET OPPORTUNITIES

Cloud-Based Quantum Computing Access (QCaaS)

The emergence of Quantum Computing as a Service (QCaaS) platforms presents a significant opportunity for market expansion. Companies like IBM, Google, and Amazon are offering cloud-based access to their quantum processors, allowing researchers and businesses to experiment with quantum algorithms without the prohibitive cost of owning hardware. This model is democratizing access and fostering a growing ecosystem of software developers and end-users.

Expansion into Logistics and Supply Chain Optimization

There is a substantial opportunity for quantum chips to revolutionize logistics, transportation, and supply chain management. Quantum algorithms are exceptionally well-suited for solving complex optimization problems, such as route planning and inventory management, which could lead to billions of dollars in operational savings for global industries. Early pilots in this area are already showing promising results.

Advancements in Drug Discovery and Materials Science

The potential for quantum chips to simulate molecular and atomic interactions with high accuracy opens up vast opportunities in pharmaceuticals and materials science. This capability could drastically reduce the time and cost associated with discovering new drugs, catalysts, and materials with tailored properties, representing a multi-billion dollar addressable market for quantum computing applications.

Quantum Chip Market Trends

Accelerating Market Growth Trajectory

The global Quantum Chip market is experiencing a period of unprecedented expansion. The market, valued at a baseline of $148 million in 2024, is projected to surge to approximately $3,064 million by the year 2032. This translates to a forecasted Compound Annual Growth Rate (CAGR) of 55.5% over the period, reflecting massive investment and a strong belief in the technology’s long-term potential. This remarkable growth is primarily driven by increasing research and development activities from both public and private sectors aiming to achieve quantum advantage.

Other Trends

Dominance of Superconducting Technology

In terms of product type, the market is currently dominated by Superconducting Quantum Chips, which hold a commanding share of over 84%. This technology is favored by leading industry players like IBM and Google for its current scalability and maturity. Other segments, such as Topological and Photonic Quantum Chips, represent areas of active research and future growth potential as the technology evolves beyond its current limitations.

Market Concentration and Regional Leadership

The competitive landscape is characterized by a high degree of concentration, with the top three players accounting for approximately 53% of the global market share. Key companies driving innovation and market development include IBM, Google, Microsoft, Intel, D-Wave, and Rigetti Computing. Geographically, North America is the largest market, with a substantial 62% share, attributed to strong government funding and a dense concentration of leading technology firms. This is followed by the Asia-Pacific region and Europe, which are also significant and rapidly growing markets.

Application Landscape and Future Outlook

The current application market is heavily skewed towards quantum computers with fewer than 39 qubits, which accounts for over 90% of the market. This reflects the nascent stage of the technology, where development and research are the primary applications. The ongoing challenge for the industry is to overcome significant technical obstacles like quantum decoherence and error rates to develop more stable, higher-qubit systems. As these challenges are addressed, the market for more powerful quantum computers is expected to expand, unlocking new commercial and scientific applications and sustaining the market’s high growth rate well into the next decade.

COMPETITIVE LANDSCAPE

Key Industry Players

A Market Defined by Technological Pioneers and Strategic Alliances

The global Quantum Chip market is currently dominated by a small number of well-established technology giants and specialized quantum computing firms, with the top three players collectively holding approximately 53% of the market share. IBM stands as a clear leader, renowned for its development of superconducting quantum processors and its extensive cloud-accessible quantum computing network. Google Quantum AI and Intel are also major forces, investing heavily in both superconducting and alternative qubit technologies. The market structure is characterized by intense research and development competition, significant capital investment, and a trend towards forming strategic partnerships with academic institutions and national research labs to accelerate progress. North America is the largest regional market, accounting for about 62% of the global share, largely driven by the concentration of these key players and supportive government funding.

Beyond the dominant players, a vibrant ecosystem of specialized companies is carving out significant niches. D-Wave Systems is a notable pioneer in quantum annealing with its adiabatic quantum computers, serving specific optimization problems. Companies like Rigetti Computing and IonQ are developing their own gate-based quantum processors, with IonQ focusing on trapped-ion technology, a promising alternative to superconducting chips. Emerging players such as PsiQuantum and Xanadu are advancing photonic quantum computing, aiming to build large-scale, fault-tolerant quantum computers. Firms like QC Ware and Zapata Computing operate in the quantum software and algorithms layer, complementing the hardware advancements. This diverse landscape also includes significant contributions from established tech companies like Microsoft, which is exploring topological qubits, and Fujitsu, which is developing hybrid quantum-classical computing solutions.

List of Key Quantum Chip Companies Profiled

- IBM

- Google (Quantum AI)

- Microsoft

- Intel

- D-Wave Systems

- Rigetti Computing

- Fujitsu

- Xanadu

- Origin Quantum Computing Technology

- IonQ

- PsiQuantum

- QC Ware

- Zapata Computing

- ColdQuanta

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Superconducting Quantum Chip technology is the established and predominant architecture in the current market landscape, benefiting from extensive research and development investments from major technology corporations. Its maturity and scalability make it the leading choice for early-stage quantum computing applications. Conversely, Topological Quantum Chip technology represents a promising future direction due to its inherent error-resistance properties, though it remains in earlier research phases. Photonic Quantum Chip technology is gaining significant attention for applications in quantum networking and communication, offering a different pathway for scalable quantum systems. |

| By Application |

|

Below 39-qubit Quantum Computer applications constitute the overwhelming majority of the current market deployment, as these systems are commercially available and accessible for research institutions, universities, and early corporate adopters to explore algorithms and use cases. This segment is characterized by intense activity in software development, algorithm testing, and foundational research. The Above 40-qubit Quantum Computer application segment, while smaller in current deployment, represents the critical frontier for achieving practical quantum advantage, attracting strategic investments aimed at solving complex optimization, simulation, and machine learning problems that are intractable for classical computers. |

| By End User |

|

Academic & Research Institutions are pivotal early adopters, driving fundamental research, developing quantum algorithms, and training the future quantum workforce. Their demand is focused on accessible, stable platforms for experimentation. Technology & IT Giants represent another dominant end-user segment, leveraging their vast resources to develop proprietary quantum hardware and software with the strategic goal of achieving long-term commercial supremacy in cloud computing and advanced problem-solving services. Defense & Government Agencies are significant investors, funding research for applications in cryptography, materials science, and complex system simulation, viewing quantum technology as a matter of national security and competitive advantage. |

| By Development Stage |

|

Research & Prototyping is the most active and expansive segment of the market, encompassing the majority of current activity as organizations across the globe work to overcome significant technical hurdles like qubit stability and error correction. This stage is characterized by high innovation and collaboration. The Early Commercialization segment involves making small-scale quantum processors available via cloud platforms, allowing a broader developer community to begin experimenting. Pilot Deployment represents the cutting edge, where select partners work with more advanced systems to test specific, high-value applications in fields like drug discovery and financial modeling, signaling the gradual transition toward practical utility. |

| By Material Platform |

|

Superconductor-based platforms, utilizing materials like niobium, are the undisputed leader in the current quantum chip market, favored for their relatively straightforward fabrication processes that borrow from classical computing and their ability to achieve the coherent quantum states necessary for computation. Semiconductor-based platforms, particularly those using silicon, are a major area of investigation due to the potential for leveraging the existing global semiconductor manufacturing infrastructure for mass production in the future. Photonic and Ion Trap platforms offer alternative approaches with distinct advantages for specific applications, such as long-distance quantum communication for photonics and high-fidelity qubit operations for ion traps, creating a diverse and competitive research landscape. |

Regional Analysis: Quantum Chip Market

The market is propelled by a powerful collaborative model where significant federal funding acts as a catalyst for massive private sector investment. This partnership accelerates the transition of quantum chip technologies from theoretical research in national laboratories to commercial prototypes and early-stage deployments, creating a vibrant and competitive landscape unmatched in other regions.

North American entities are at the forefront of multiple qubit modalities, particularly superconducting circuits, which are currently the most advanced and scalable. This leadership in a key technological pathway gives the region’s companies a significant first-mover advantage in building more stable and powerful quantum processing units, setting global performance benchmarks.

A critical success factor is the seamless flow of talent and ideas from world-class universities into corporate R&D. This ecosystem ensures a continuous supply of highly skilled quantum engineers and physicists, while also facilitating the rapid commercialization of academic breakthroughs, keeping the innovation cycle exceptionally short and productive.

The region’s tech giants are pioneering the quantum-as-a-service model, providing cloud access to their quantum processors. This strategy lowers the barrier to entry for a wide range of potential users, from researchers to enterprises, fostering a growing user community and generating valuable real-world usage data that informs further chip development.

Europe

Europe has established itself as a formidable and well-coordinated contender in the Quantum Chip Market, primarily through large-scale, multinational initiatives like the European Union’s ambitious Quantum Flagship program. This continent-wide strategy fosters collaboration between member states, pooling resources and expertise to compete effectively. The region exhibits particular strength in fundamental research and developing alternative qubit technologies, such as those based on photonics and spin qubits, offering a diverse technological portfolio. Strong national quantum programs in countries like Germany, the United Kingdom, and France provide additional momentum, creating multiple hubs of excellence. Europe’s approach is characterized by a focus on building a complete quantum technology ecosystem, from basic science to eventual manufacturing, ensuring long-term sustainability and reducing dependence on external technological supply chains.

Asia-Pacific

The Asia-Pacific region is a rapidly ascending force, characterized by intense national-level commitment and significant government-led investment strategies. China is pursuing quantum advancement with strategic determination, aiming for leadership through massive state-funded projects that target breakthroughs in all aspects of quantum technology. Japan and South Korea contribute with their renowned expertise in high-tech manufacturing and electronics, which is crucial for the precise fabrication requirements of quantum chips. Australia has also emerged as a key player, with notable strengths in quantum computing research, particularly in silicon-based qubit technologies. The region’s dynamic is defined by a blend of top-down strategic directives and strong industrial capabilities, making it a major incubator for future growth and innovation in the quantum chip space.

South America

South America’s participation in the Quantum Chip Market is currently in a nascent but developing stage, with growth primarily driven by academic research clusters and increasing regional cooperation. Countries like Brazil and Argentina are fostering small but dedicated research groups focused on theoretical advancements and experimental quantum information science. While the region lacks the large-scale industrial infrastructure and investment seen in leading markets, there is a growing recognition of quantum technology’s strategic importance. Efforts are underway to build regional networks and attract international partnerships to build foundational capabilities. The focus is on cultivating local expertise and positioning the continent to engage with global quantum developments, with potential for niche contributions in the longer term.

Middle East & Africa

The Middle East & Africa region is entering the Quantum Chip Market with a focus on strategic future-proofing and economic diversification, particularly among Gulf Cooperation Council nations. Countries like the United Arab Emirates and Saudi Arabia are making foundational investments by establishing research centers and forging partnerships with established global leaders to accelerate knowledge transfer. The initial emphasis is on building human capital and research infrastructure rather than immediate commercial production. In Africa, South Africa leads with existing strengths in scientific research, though quantum-specific initiatives are still emerging. The region’s journey is one of laying the groundwork, with a long-term view towards participating in the quantum economy and avoiding a future technological gap.

Report Scope

This market research report provides a comprehensive analysis of the Quantum Chip Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Quantum Chip Market?

-> Quantum Chip Market was valued at USD 148 million in 2024 and is projected to reach USD 3.06 billion by 2032, exhibiting a CAGR of 55.5% during the forecast period.

Which key companies operate in Quantum Chip Market?

-> Key players include IBM, Google, Microsoft, Intel, D-Wave, Rigetti Computing, Fujitsu, Xanadu, Origin Quantum Computing Technology, and Ion Q, among others. The top three players hold a combined market share of approximately 53%.

What are the key growth drivers?

-> Key growth drivers include advancements in quantum information processing technology, increasing research and development investments, and rising demand for high-performance computing solutions across various sectors.

Which region dominates the market?

-> North America is the largest market, accounting for a share of about 62%, followed by Asia-Pacific and Europe.

What are the emerging trends?

-> Emerging trends include the development of superconducting quantum chips, increased qubit counts in quantum computers, and strategic partnerships among leading technology companies to accelerate commercialization.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...