MARKET INSIGHTS

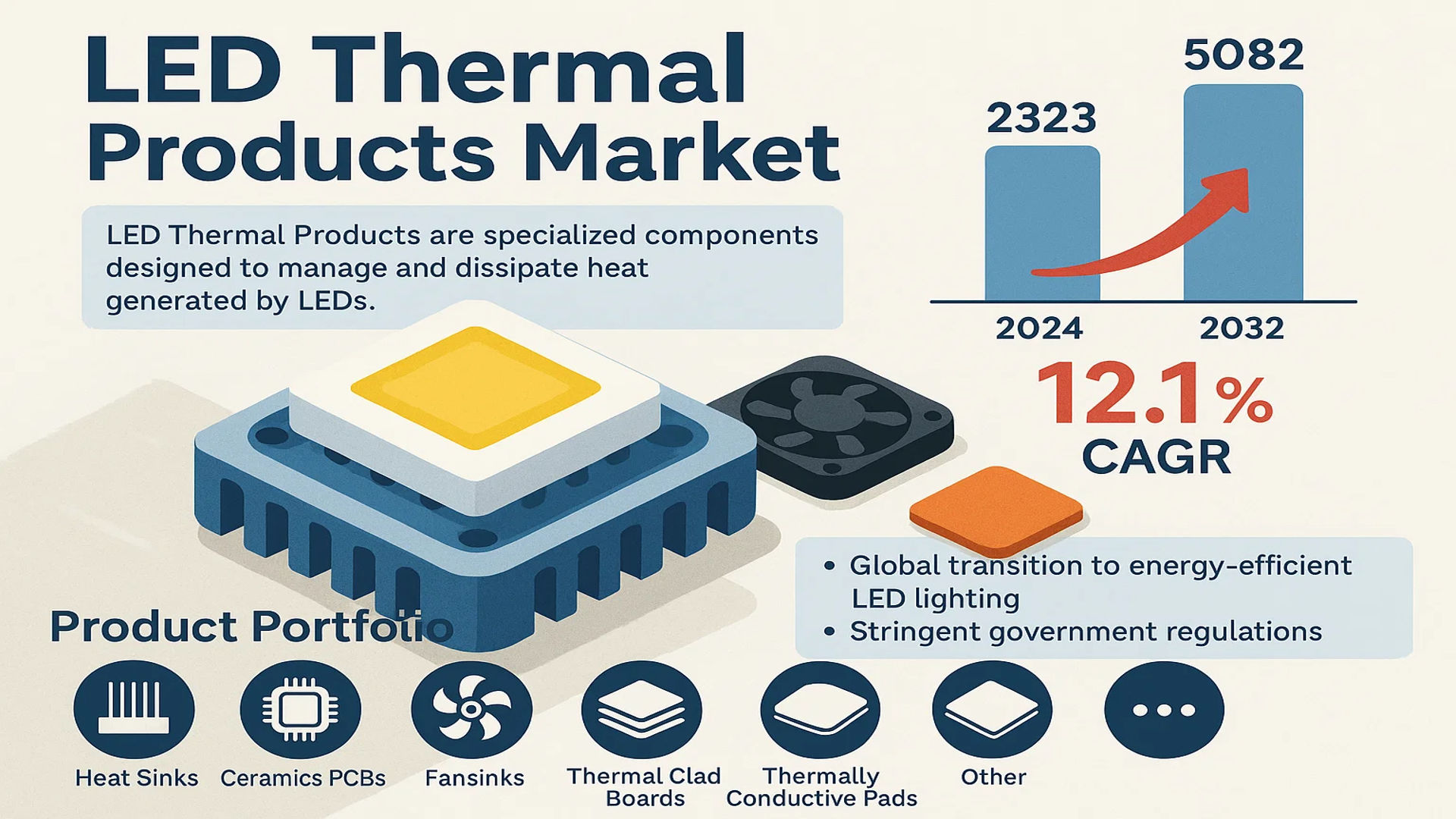

The global LED Thermal Products Market was valued at 2323 million in 2024 and is projected to reach US$ 5082 million by 2032, at a CAGR of 12.1% during the forecast period.

LED Thermal Products are specialized components designed to manage and dissipate heat generated by light-emitting diodes (LEDs). Because approximately 70% of the electrical energy in an LED is converted into heat rather than light, these products are critical for maintaining optimal operating temperatures. If this heat is not effectively removed, it can lead to reduced luminous efficacy, color shift, and a significantly shortened operational lifespan. The product portfolio includes Heat Sinks, Ceramic PCBs, Fansinks, Thermal Clad Boards, Thermally Conductive Pads, and other advanced thermal management solutions.

The market is experiencing robust growth driven by the global transition to energy-efficient LED lighting across residential, commercial, and industrial sectors. Furthermore, stringent government regulations phasing out inefficient lighting and the rapid adoption of LEDs in the automotive industry are key growth catalysts. China currently dominates as the largest regional market, holding nearly 30% of the global share, while Europe and North America collectively account for over 45%. Within product types, Heat Sinks are the dominant segment, capturing over 35% of the market share in 2024, due to their widespread use and effectiveness

MARKET DYNAMICS

MARKET DRIVERS

Global Energy Efficiency Regulations Accelerate LED Adoption and Thermal Management Demand

Stringent global energy efficiency standards are compelling manufacturers and consumers to transition toward LED lighting solutions, significantly driving the thermal management market. Over 40 countries have implemented minimum energy performance standards that phase out inefficient lighting technologies, creating a regulatory push for LEDs. Since approximately 70% of electrical energy in LEDs converts to heat rather than light, effective thermal management becomes critical for maintaining performance compliance and longevity. The European Union’s Ecodesign Directive and similar regulations in North America and Asia-Pacific mandate specific efficacy levels that can only be achieved with proper thermal dissipation. This regulatory landscape has created a sustained demand for advanced thermal products that ensure LEDs operate within optimal temperature ranges, maintaining luminosity and preventing premature failure.

Proliferation of High-Power LED Applications in Automotive and Industrial Sectors

The automotive industry’s rapid adoption of LED technology for headlights, interior lighting, and advanced display systems has created substantial growth opportunities for thermal management solutions. Modern vehicles incorporate over 300 LEDs per unit, with high-power applications generating significant thermal loads that require sophisticated cooling systems. The transition toward electric vehicles has further amplified this demand, as efficient thermal management directly impacts battery life and overall vehicle performance. Similarly, industrial applications including high-bay lighting, street lighting, and horticulture lighting utilize high-power LED arrays that generate considerable heat. These applications require robust thermal solutions capable of maintaining junction temperatures below critical thresholds, typically 120°C for most high-power LEDs, to ensure rated lifespan exceeding 50,000 hours.

Technological Advancements in Thermal Interface Materials and Heat Sink Designs

Continuous innovation in thermal management technologies is driving market expansion through improved performance and cost efficiency. Advanced thermal interface materials now achieve thermal conductivity ratings exceeding 15 W/mK, significantly enhancing heat transfer from LED chips to heat sinks. Composite materials incorporating graphene and carbon nanotubes are emerging with conductivity values reaching 1500-2000 W/mK, though currently limited to premium applications. Simultaneously, manufacturing advancements in heat sink production, including die-casting optimization and additive manufacturing techniques, have reduced production costs while improving thermal performance. These innovations enable thermal management solutions to keep pace with increasing LED power densities, which have grown from approximately 3W/cm² to over 10W/cm² in advanced applications, necessitating corresponding improvements in cooling capacity.

MARKET CHALLENGES

High Material and Manufacturing Costs Constrain Market Penetration in Price-Sensitive Segments

The LED thermal products market faces significant cost-related challenges, particularly in price-sensitive market segments and developing regions. Advanced thermal management solutions utilizing premium materials such as copper alloys, ceramic substrates, and high-performance thermal interface materials contribute substantially to overall system costs. Copper-based heat sinks, while offering superior thermal conductivity of approximately 400 W/mK, can increase product costs by 25-40% compared to aluminum alternatives. Similarly, ceramic PCBs provide excellent thermal performance but cost 3-5 times more than standard FR4 substrates. These cost pressures are particularly acute in residential and general lighting applications where consumers demonstrate high price sensitivity. Manufacturers must balance thermal performance requirements against cost constraints, often resulting in compromised solutions that may affect product reliability and lifespan.

Other Challenges

Thermal Performance Limitations in Miniaturized Applications

The trend toward miniaturization in LED applications creates significant thermal management challenges as power densities increase while available surface area for heat dissipation decreases. Compact consumer electronics, automotive lighting modules, and architectural lighting fixtures provide limited space for conventional cooling solutions, forcing designers to employ innovative but often insufficient thermal strategies. This spatial constraint frequently results in junction temperatures exceeding recommended limits, potentially reducing LED lifespan by up to 75% according to Arrhenius-based reliability models. The industry continues to struggle with developing cost-effective miniature thermal solutions that can handle power densities exceeding 15W/cm² while maintaining form factor requirements.

Complex Supply Chain and Raw Material Availability Issues

Global supply chain disruptions and raw material availability present ongoing challenges for thermal product manufacturers. Copper and aluminum prices have experienced volatility exceeding 30% year-over-year, directly impacting production costs and pricing stability. Specialty materials including thermal greases, phase change materials, and ceramic substrates face supply constraints due to limited manufacturing capacity and geopolitical factors. These supply chain complexities are compounded by increasing lead times and transportation costs, particularly affecting just-in-time manufacturing operations. The market must navigate these challenges while maintaining product quality and meeting delivery commitments to LED manufacturers.

MARKET RESTRAINTS

Technical Complexity in Thermal Design Integration Limits Widespread Adoption

The integration of thermal management solutions into LED products presents substantial technical challenges that restrain market growth. Effective thermal design requires sophisticated engineering capabilities and specialized knowledge of heat transfer principles, material science, and manufacturing processes. Many LED manufacturers, particularly smaller players, lack the in-house expertise to properly design and implement advanced thermal solutions, leading to suboptimal product performance or excessive reliance on external consultants. The complexity increases with higher power applications where thermal resistance paths must be meticulously calculated and optimized. A typical high-power LED system may involve multiple thermal interfaces – from junction to package, package to board, board to heat sink, and heat sink to environment – each contributing to the overall thermal resistance that must be minimized through careful design and material selection.

Standardization Gaps and Performance Verification Challenges

The absence of comprehensive industry standards for thermal performance testing and verification creates significant market restraints. While organizations including JEDEC and CIE have established some guidelines, implementation varies widely across manufacturers and regions. This standardization gap leads to performance claims that are difficult to compare and verify, creating uncertainty among buyers and specifiers. Thermal performance data provided in datasheets often lacks sufficient detail about testing conditions, making accurate system-level thermal predictions challenging. The situation is particularly problematic for comparative assessments between products, as different testing methodologies can yield significantly different results. This ambiguity forces conservative design approaches and additional safety margins, increasing system costs and potentially limiting adoption of more advanced thermal solutions.

Limited Awareness and Understanding Among End-Users

Many end-users and specifiers lack adequate understanding of thermal management’s critical role in LED performance and longevity, restraining market development. While professionals recognize that overheating reduces LED lifespan, the quantitative relationship between junction temperature and reliability remains poorly understood outside engineering circles. For every 10°C increase in junction temperature above recommended levels, LED lifespan typically decreases by approximately 50%, yet this crucial information often fails to influence purchasing decisions. The market suffers from prioritization of initial cost over lifetime performance, particularly in price-sensitive segments where thermal management is viewed as an unnecessary expense rather than a critical investment. This knowledge gap prevents wider adoption of advanced thermal solutions and encourages cost-cutting measures that compromise long-term performance.

MARKET OPPORTUNITIES

Emerging Applications in Electric Vehicles and Smart Infrastructure Create New Growth Frontiers

The rapid expansion of electric vehicle production and smart city infrastructure projects presents substantial growth opportunities for advanced thermal management solutions. Modern electric vehicles incorporate extensive LED lighting systems including adaptive headlights, interior ambient lighting, and status indicators that require sophisticated thermal management. The automotive sector’s transition toward higher luminance requirements and smaller form factors increases thermal density challenges, necessitating innovative cooling solutions. Simultaneously, smart city initiatives deploying intelligent street lighting networks with integrated sensors and communication systems require reliable thermal management to ensure continuous operation in varying environmental conditions. These applications typically prioritize reliability over cost, creating opportunities for premium thermal solutions with enhanced performance characteristics.

Development of Phase Change Materials and Advanced Thermal Interfaces

Technological innovations in phase change materials and advanced thermal interface materials offer significant market opportunities through performance enhancement and cost reduction. Phase change materials capable of absorbing and dissipating thermal energy through latent heat effects provide effective thermal buffering for transient high-power conditions. These materials typically exhibit thermal energy storage capacities ranging from 150-250 kJ/kg, effectively managing temperature spikes that would otherwise degrade LED performance. Concurrently, advancements in thermal interface materials including graphene-enhanced compounds and metal-based thermal pads are achieving thermal conductivity values exceeding 20 W/mK while reducing application complexity. These materials help minimize thermal resistance at critical interfaces, improving overall system efficiency and enabling higher power densities without proportional increases in heat sink size.

Growing Demand for Retrofit Solutions and Aftermarket Services

The extensive installed base of LED lighting systems creates substantial opportunities for retrofit thermal solutions and aftermarket services. Many early-generation LED installations experienced premature failure due to inadequate thermal management, creating a market for upgrade solutions that enhance existing systems’ reliability and performance. Additionally, the trend toward luminaire-level maintenance and refurbishment rather than complete replacement drives demand for compatible thermal components. This aftermarket segment requires thermal solutions that can be integrated into existing form factors while improving performance, often necessitating custom designs and engineering services. The opportunity extends to thermal management upgrades for legacy systems seeking to extend operational life or increase luminous output through improved cooling capacity.

LED THERMAL PRODUCTS MARKET TRENDS

Rising Demand for High-Power LEDs Drives Thermal Management Innovation

The global LED Thermal Products market, valued at $2323 million in 2024, is experiencing significant growth due to the escalating demand for high-power and high-brightness LEDs across multiple sectors. Because approximately 70% of the electrical energy in an LED is converted into heat, effective thermal management is not merely an option but a critical requirement for ensuring performance, longevity, and reliability. This has catalyzed a wave of innovation in thermal interface materials, advanced heat sink designs, and active cooling solutions like integrated fansinks. The market is projected to reach $5082 million by 2032, growing at a CAGR of 12.1%, driven by the need to dissipate heat from increasingly powerful LED packages used in applications ranging from automotive headlights to industrial lighting and high-resolution displays.

Other Trends

Miniaturization and Integration in Consumer Electronics

The relentless trend towards thinner, lighter, and more powerful consumer electronics is placing immense pressure on thermal management solutions. In devices like smartphones, tablets, and ultra-slim laptops that incorporate high-luminance LED backlights and indicators, the available space for heat dissipation is extremely limited. This has led to the increased adoption of sophisticated thermal products such as thermally conductive pads, which offer excellent conformability and heat spreading in tight spaces, and ceramic PCBs, which provide superior thermal conductivity and electrical insulation compared to traditional FR4 boards. The demand for these compact, high-performance solutions is a major growth driver, as failure to manage heat in such confined environments directly impacts device performance and user safety.

Expansion of Automotive LED Applications

The automotive industry represents one of the fastest-growing segments for LED thermal products, driven by the rapid adoption of LEDs for exterior lighting, interior ambient lighting, and advanced driver-assistance systems (ADAS). Modern vehicles can contain hundreds of LEDs, with high-power units used in headlights generating substantial heat that must be effectively managed to prevent lumen depreciation and color shift. This has resulted in a surge in demand for robust thermal management systems, including aluminum heat sinks and active cooling assemblies. Furthermore, the emergence of electric vehicles (EVs), where energy efficiency is paramount, has intensified the focus on thermal management to maximize the range and lifespan of all electronic components, including LED lighting systems. This sector’s growth is a key contributor to the overall market expansion.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Global Reach Define Market Leadership

The global LED Thermal Products market exhibits a fragmented yet competitive structure, characterized by the presence of established multinational corporations and agile specialized manufacturers. Sunonwealth Electric Machine Industry Co., Ltd. has emerged as a dominant force, leveraging its extensive manufacturing capabilities in Asia and a comprehensive portfolio that includes high-performance heat sinks and cooling fans. Their significant market share is further bolstered by strong supply chain relationships and cost-effective production.

Similarly, Aavid Thermalloy LLC (a part of Boyd Corporation) and 3M Company hold considerable influence, particularly in the North American and European markets. Their leadership is attributed to deep-rooted expertise in thermal management technologies and a continuous stream of innovative product developments, such as advanced thermal interface materials and custom-designed heat dissipation solutions. These companies benefit from long-standing relationships with major LED manufacturers across automotive, consumer electronics, and industrial lighting sectors.

Market growth is further propelled by strategic activities such as mergers, acquisitions, and geographic expansion. For instance, the acquisition of specialized thermal solution firms by larger entities has been a key trend, enabling portfolio diversification and access to new customer segments. Furthermore, companies are heavily investing in research and development to create more efficient, compact, and environmentally sustainable thermal products to meet the evolving demands of next-generation high-lumen LED applications.

Meanwhile, other significant players like the ebm-papst Group and TE Connectivity are strengthening their positions through technological differentiation and strategic partnerships. Their focus on developing intelligent thermal management systems that integrate active cooling with smart monitoring capabilities is setting new industry standards and creating additional growth avenues within the competitive framework.

List of Key LED Thermal Products Companies Profiled

- Sunonwealth Electric Machine Industry Co., Ltd. (Taiwan)

- Aavid Thermalloy LLC (Boyd Corporation) (U.S.)

- Cree Inc. (Wolfspeed) (U.S.)

- 3M Company (U.S.)

- ebm-papst Group (Germany)

- Bergquist Company (U.S.)

- t-Global Technology Co., Ltd. (Taiwan)

- Molex, LLC (U.S.)

- Dialight PLC (U.K.)

- Wakefield-Vette, Inc. (U.S.)

- Ohmite Manufacturing Co. (U.S.)

- TE Connectivity Ltd. (Switzerland)

- Advanced Thermal Solutions, Inc. (U.S.)

- LEDdynamics, Inc. (U.S.)

Segment Analysis:

By Type

Heat Sink Segment Dominates the Market Due to its Superior Heat Dissipation Capabilities and Cost-Effectiveness

The market is segmented based on type into:

- Heat Sink

- Ceramic PCB

- Fansink

- Thermal Clad Board

- Thermally Conductive Pad

- Others

By Application

Residential Segment Leads Due to High Adoption of Energy-Efficient LED Lighting Solutions

The market is segmented based on application into:

- Residential

- Office

- Industrial

- Shop

- Automotive

- Others

Regional Analysis: LED Thermal Products Market

Asia-Pacific

The Asia-Pacific region is the dominant force in the global LED Thermal Products market, accounting for nearly 30% of the total market share, with China being the single largest market globally. This leadership is fueled by the region’s massive manufacturing base for LED components and finished lighting products. The widespread adoption of LED lighting in residential and commercial construction, driven by rapid urbanization and government energy efficiency initiatives, creates sustained demand for thermal management solutions. While cost sensitivity keeps demand high for established products like heat sinks, which hold over 35% of the product segment, there is a growing trend toward more advanced and efficient thermal interface materials and ceramic PCBs, particularly in high-power and automotive applications. The presence of major global players and a dense network of local suppliers ensures a highly competitive and innovative market landscape.

Europe

Europe represents a mature and technologically advanced market for LED Thermal Products, characterized by stringent regulations and a strong focus on energy efficiency and product longevity. EU directives, such as the Ecodesign Directive, push for higher-performing and more reliable LED systems, which in turn drives the demand for superior thermal management. The market is particularly strong in industrial and automotive applications, where performance and reliability are paramount. Innovation is a key driver, with a significant emphasis on developing eco-friendly and high-efficiency thermal solutions. Countries like Germany, the UK, and France are at the forefront, hosting leading research facilities and manufacturing operations for several key global players in the thermal management space.

North America

The North American market is a significant and stable contributor, driven by high consumer awareness, strict energy codes, and a robust replacement market for traditional lighting. The United States is the largest market within the region. Demand is particularly strong from the residential and office sectors, which are the largest application segments. The market is characterized by a preference for high-quality, reliable, and innovative thermal products that ensure long LED lifespans and maintain luminous efficacy. Recent infrastructure investments and a growing focus on smart city projects are also creating new opportunities for advanced LED lighting systems, which rely on effective thermal management to perform reliably in integrated and often demanding environments.

South America

The South American market for LED Thermal Products is in a growth phase, albeit at a slower pace compared to other regions. Economic volatility in key countries like Brazil and Argentina has historically impacted investment in new infrastructure and delayed widespread adoption. However, gradual economic recovery and increasing awareness of the long-term cost savings of LED technology are driving demand. The market currently leans toward more cost-effective thermal solutions, such as basic heat sinks, due to budget constraints. As the region’s infrastructure modernizes and environmental regulations potentially tighten, a shift toward more advanced thermal management products is expected over the long term.

Middle East & Africa

This region presents an emerging market with significant long-term potential, though its development is uneven. Growth is primarily concentrated in more economically developed nations like Saudi Arabia, the UAE, and Israel, where large-scale urban development, smart city projects, and infrastructure modernization are underway. These projects create demand for durable and reliable LED lighting, necessitating effective thermal products. However, progress across the broader region is often hampered by funding limitations, a lack of stringent enforcement of energy standards, and political instability in certain areas. Despite these challenges, the fundamental drivers of urbanization and the global shift toward energy-efficient lighting indicate a positive growth trajectory for the LED Thermal Products market in the Middle East and Africa over the coming decade.

Report Scope

This market research report provides a comprehensive analysis of the global LED Thermal Products market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging thermal management technologies, material science advancements, integration of IoT for smart thermal monitoring, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global LED Thermal Products Market?

-> LED Thermal Products Market was valued at 2323 million in 2024 and is projected to reach US$ 5082 million by 2032, at a CAGR of 12.1% during the forecast period.

Which key companies operate in Global LED Thermal Products Market?

-> Key players include Sunonwealth, Aavid Thermalloy, Cree Inc., 3M, ebm-papst Group, Bergquist, t-Global Technology, Molex LLC, Dialight, Wakefield-Vette, Ohmite, TE Connectivity, Advanced Thermal Solutions Inc., and LEDdynamics Inc., among others.

What are the key growth drivers?

-> Key growth drivers include increasing LED adoption across residential and commercial sectors, stringent energy efficiency regulations, rising demand for high-power LEDs, and the critical need for thermal management to ensure LED longevity and performance.

Which region dominates the market?

-> China is the largest market with a share of nearly 30%, followed by Europe and North America which collectively account for over 45% of the global market share.

What are the emerging trends?

-> Emerging trends include development of advanced thermal interface materials, miniaturization of thermal solutions, integration of phase-change materials, and growing adoption of ceramic-based PCBs for superior thermal conductivity.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...