MARKET INSIGHTS

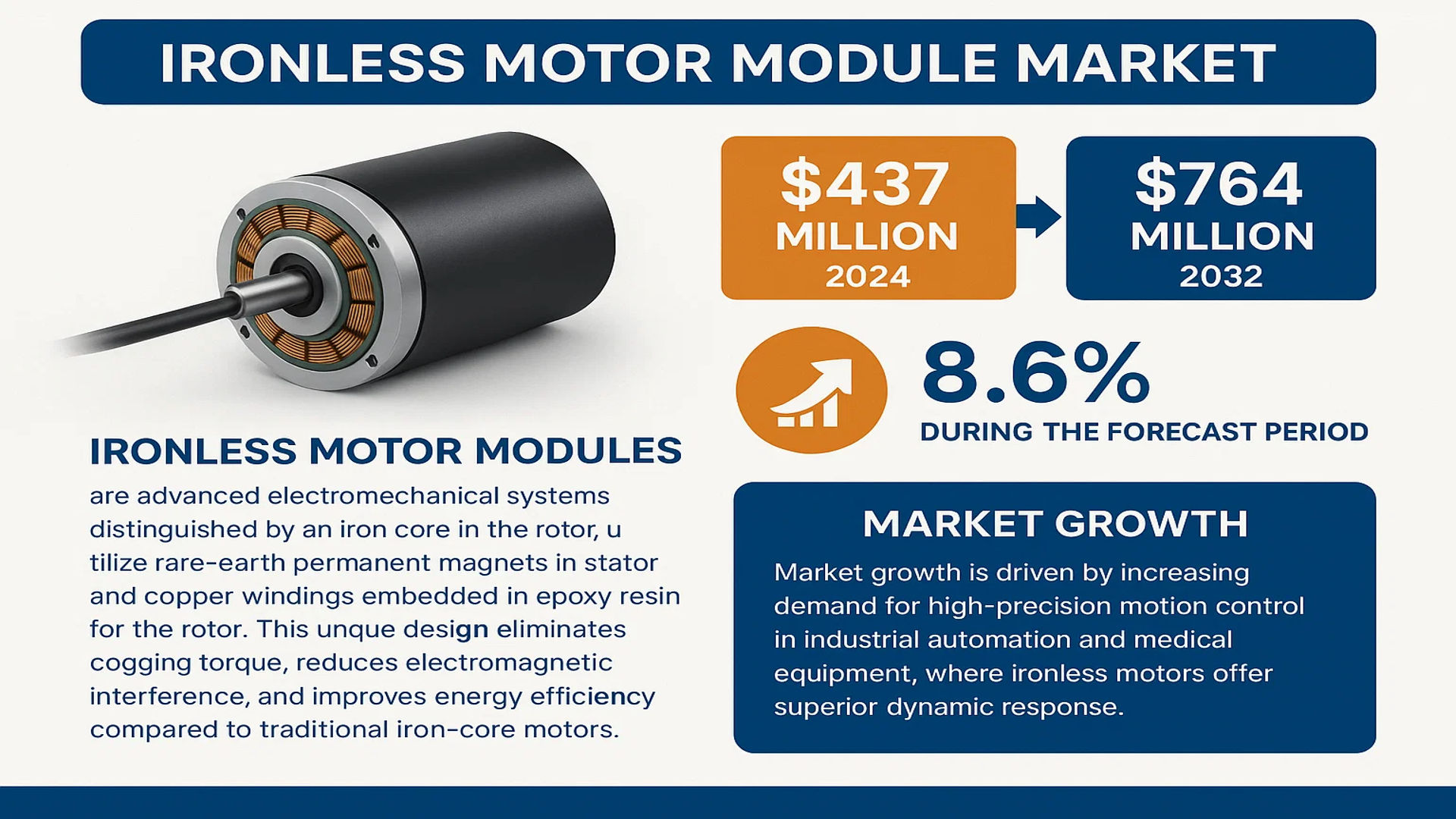

The global Ironless Motor Module Market was valued at 437 million in 2024 and is projected to reach US$ 764 million by 2032, at a CAGR of 8.6% during the forecast period.

Ironless motor modules are advanced electromechanical systems distinguished by their lack of an iron core in the rotor. Instead, these modules utilize rare-earth permanent magnets (such as neodymium or samarium cobalt) in the stator and copper windings embedded in epoxy resin for the rotor. This unique design eliminates cogging torque, reduces electromagnetic interference, and improves energy efficiency compared to traditional iron-core motors.

The market growth is driven by increasing demand for high-precision motion control in industrial automation and medical equipment, where ironless motors offer superior dynamic response. While North America currently leads in technological adoption, Asia-Pacific is emerging as the fastest-growing region due to expanding manufacturing sectors. Major players like Siemens, ABB, and Yaskawa Electric are investing in R&D to enhance torque density and thermal performance, further accelerating market expansion.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Industrial Automation to Accelerate Adoption of Ironless Motor Modules

The rapid expansion of industrial automation across manufacturing, robotics, and logistics is a key driver for ironless motor modules. These motors offer superior precision and responsiveness compared to traditional core motors, making them ideal for applications requiring high-speed and high-accuracy motion control. The global industrial automation market is projected to grow considerably, with heavy investments in smart factories and Industry 4.0 technologies. Ironless motors, with their reduced cogging and enhanced torque-to-weight ratio, are increasingly favored in pick-and-place robots, CNC machines, and semiconductor manufacturing equipment where micron-level precision is critical.

Growing Demand for Miniaturization in Medical Equipment to Fuel Market Prospects

Medical device manufacturers are increasingly adopting ironless motor modules to meet the demand for compact, lightweight, and energy-efficient components. Unlike conventional motors, ironless designs eliminate magnetic saturation and eddy current losses, making them perfect for portable medical equipment like surgical robots, MRI systems, and catheter navigation devices. The medical equipment sector is witnessing significant growth due to aging populations and rising healthcare spending, with projections indicating strong expansion in diagnostic imaging and robotic-assisted surgery segments where ironless motors excel.

The superior thermal management of ironless motors also allows for longer operational periods without overheating – a critical requirement for medical applications where equipment reliability directly impacts patient outcomes. This combination of technical advantages and market demand positions ironless motor modules for sustained adoption in the healthcare sector.

MARKET RESTRAINTS

High Production Costs and Complex Manufacturing to Limit Market Penetration

While ironless motor modules offer superior performance characteristics, their manufacturing complexity and material costs present significant barriers to widespread adoption. The use of rare earth magnets and precision-wound copper coils in construction increases production costs substantially compared to traditional iron-core motors. This price premium can deter cost-sensitive applications, particularly in price-competitive markets where performance advantages may not justify the additional investment.

The assembly process requires specialized equipment and skilled technicians, as the delicate rotor construction without iron support demands extreme precision. Production yields can be affected by minute variations in winding tension or alignment, leading to higher rejection rates and additional quality control expenses. These manufacturing challenges limit the ability to scale production quickly to meet growing demand.

MARKET CHALLENGES

Thermal Management Issues in High-Performance Applications

Ironless motors face thermal limitations that challenge their use in demanding continuous-duty applications. Without the iron core to help dissipate heat, concentrated thermal loads can develop in the windings during extended operation. This becomes particularly problematic in aerospace and industrial automation applications where motors must maintain peak performance over long periods without cooling interruptions.

Other Challenges

Supply Chain Vulnerability

The reliance on rare earth materials like neodymium makes manufacturers vulnerable to geopolitical supply chain disruptions. Price volatility in these critical materials can significantly impact production costs and profit margins.

Technical Expertise Shortage

The specialized nature of ironless motor design and integration has created a skills gap in the workforce. Companies struggle to find engineers with expertise in these advanced motor technologies, slowing development cycles.

MARKET OPPORTUNITIES

Emerging Electric Vehicle Applications to Create New Growth Potential

The electric vehicle industry presents significant opportunities for ironless motor modules, particularly in high-performance applications. Their power density and efficiency advantages make them ideal candidates for electric power steering systems, brake-by-wire actuators, and other precision motion control applications in EVs. As automakers push for greater energy efficiency and responsive vehicle dynamics, ironless motors are gaining attention for their ability to deliver precise torque control without cogging artifacts.

Major automotive suppliers are actively developing next-generation ironless motor solutions tailored for the unique requirements of electric and autonomous vehicles. The transition to electric powertrains across all vehicle segments is expected to drive considerable demand for advanced motor technologies that can operate efficiently across wide speed ranges while meeting stringent automotive reliability standards.

Furthermore, the aerospace industry’s shift toward more-electric aircraft creates parallel opportunities for ironless motors in flight control systems and auxiliary power units where weight savings and reliability are paramount. These emerging high-value applications could significantly expand the addressable market beyond traditional industrial uses.

IRONLESS MOTOR MODULE MARKET TRENDS

Adoption in High-Precision Applications to Drive Market Growth

The ironless motor module market is witnessing robust growth due to the rising demand for high-precision motion control in industries such as medical equipment, aerospace, and semiconductor manufacturing. Without the iron core, these motors eliminate cogging torque and deliver smoother motion, making them ideal for applications requiring ultra-fine positioning. In medical equipment, for instance, the adoption rate of ironless motors has surged by over 12% annually, driven by their use in surgical robots and imaging systems where precision is non-negotiable. Furthermore, advancements in rare-earth permanent magnets, such as neodymium-based alloys, have significantly enhanced motor efficiency, contributing to their wider adoption.

Other Trends

Energy Efficiency and Sustainability

The global push toward energy efficiency is accelerating the transition from traditional iron-core motors to ironless variants. These modules demonstrate up to 30% higher efficiency in energy conversion, reducing operational costs and aligning with stringent environmental regulations. Industries such as industrial automation are increasingly integrating ironless motors into servo systems, where reduced heat generation and lower electromagnetic interference (EMI) provide additional operational benefits. Governments in Europe and North America are also incentivizing the adoption of energy-efficient motors, further propelling market expansion.

Expansion in Robotics and Automation

The proliferation of robotics across manufacturing and logistics is a key catalyst for the ironless motor module market. Collaborative robots (cobots), which require lightweight and high-torque motors, are particularly reliant on ironless designs for seamless human-machine interaction. The robotics sector accounted for nearly 25% of total ironless motor demand in 2024, with projections indicating a doubling of this share by 2030. Additionally, innovations in brushless motor modules—now dominating over 60% of the market—are enhancing durability and reducing maintenance needs in automated systems, further solidifying their position in modern industrial ecosystems.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic R&D Investments and Technological Advancements Define Market Dynamics

The global ironless motor module market exhibits a moderately consolidated landscape, dominated by multinational corporations with extensive technical expertise in precision motor manufacturing. Siemens AG leads the market share, leveraging its industrial automation dominance and recent innovations in high-efficiency brushless ironless motor designs. The company’s significant presence across Europe, Asia-Pacific, and North American markets strengthens its competitive position.

Japanese conglomerate Yaskawa Electric Corporation follows closely, particularly strong in robotics and medical equipment applications where ironless motors provide critical advantages. Their patented MAGNUS series motors demonstrate superior torque density, helping capture 18% of the specialized medical motor segment as of 2024.

Market competition intensifies as Parker Hannifin accelerates development of ironless motor modules for aerospace applications, capitalizing on their lightweight advantages over traditional motors. Simultaneously, Moog Inc. has made notable strides in defense sector applications through customized ironless motor solutions that meet stringent military specifications.

Emerging players are disrupting traditional segments through cost optimization. Delta Electronics and Shenzhen FGS Mechanical Electrical Equipment have gained traction in industrial automation by offering competitively priced ironless motor modules without compromising on energy efficiency benchmarks. This price-performance balance is reshaping procurement strategies among mid-tier manufacturers.

List of Key Ironless Motor Module Manufacturers

- Siemens AG (Germany)

- ABB Ltd. (Switzerland)

- Yaskawa Electric Corporation (Japan)

- Bosch Rexroth AG (Germany)

- Schneider Electric SE (France)

- Parker Hannifin Corp (U.S.)

- Mitsubishi Electric Corporation (Japan)

- Fanuc Corporation (Japan)

- Moog Inc. (U.S.)

- Delta Electronics (Taiwan)

- Aimega (China)

- Shenzhen FGS Mechanical Electrical Equipment (China)

Segment Analysis:

By Type

Brushless Motor Module Segment Leads Due to High Efficiency and Low Maintenance Requirements

The market is segmented based on type into:

- Brushed Motor Module

- Brushless Motor Module

By Application

Industrial Automation Represents the Largest Application Segment Due to Growing Manufacturing Automation Trends

The market is segmented based on application into:

- Industrial Automation

- Medical Equipment

- Transportation

- Aerospace

- Others

By Power Rating

Medium Power Segment Holds Significant Share Due to Diverse Industrial Applications

The market is segmented based on power rating into:

- Low Power (Below 1 kW)

- Medium Power (1-10 kW)

- High Power (Above 10 kW)

By Cooling Method

Air-Cooled Modules Dominate Market Share Owing to Simplicity and Cost-Effectiveness

The market is segmented based on cooling method into:

- Air-Cooled

- Liquid-Cooled

Regional Analysis: Ironless Motor Module Market

Asia-Pacific

The Asia-Pacific region leads the ironless motor module market, driven by rapid industrialization and technological advancements in manufacturing hubs like China, Japan, and South Korea. China, accounting for over 40% of regional demand, is investing heavily in industrial automation and high-precision medical equipment, where ironless motors excel due to their superior efficiency and low vibration. The growth of robotics and semiconductor manufacturing further accelerates adoption. However, competition from conventional motor suppliers remains a challenge in price-sensitive markets like India. Japan’s focus on miniaturization and energy efficiency in automotive and electronics applications provides sustained demand, particularly for brushless motor modules.

North America

North America’s market is characterized by stringent performance requirements in aerospace, medical devices, and automation sectors. The U.S. dominates with innovations in direct-drive technologies, where ironless modules eliminate backlash in robotic applications. Major players like Moog and Parker Hannifin are expanding production capacities to meet demand from defense and commercial aviation sectors. Canadian manufacturers are increasingly adopting these motors for renewable energy systems. While technological expertise drives premium adoption, higher costs compared to traditional motors limit penetration in small and medium enterprises.

Europe

Europe’s mature industrial base emphasizes energy efficiency and precision, creating strong demand in Germany, Italy, and Switzerland. The region’s strict EU Ecodesign regulations favor ironless motors in HVAC and packaging machinery applications. Siemens and ABB lead in developing integrated motor-drive solutions for factory automation. However, the market faces supply chain challenges for rare-earth magnets and copper materials. Recent investments in electric vehicle components and wind turbine pitch control systems are opening new growth avenues, though adoption rates vary significantly between Western and Eastern European countries.

South America

The South American market shows moderate growth, primarily concentrated in Brazil’s automotive and mining equipment sectors. Limited local manufacturing capabilities result in reliance on imports from Asia and North America. While awareness of ironless motor advantages grows, economic instability and preference for low-cost alternatives hinder market expansion. Argentina’s developing medical device industry presents niche opportunities, but infrastructure limitations and volatile raw material prices create operational challenges for suppliers. Regional collaborations with global manufacturers could stimulate future market development.

Middle East & Africa

This emerging market sees gradual adoption in oil/gas automation and select industrial applications. The UAE and Saudi Arabia drive demand through smart city initiatives and diversification from oil dependence. South Africa’s manufacturing sector shows potential for ironless motors in precision equipment. However, low technology penetration, inadequate technical expertise, and prioritization of basic infrastructure over advanced automation limit market growth. Strategic partnerships with European and Asian suppliers are helping bridge the knowledge gap, but the region remains a long-term growth prospect rather than immediate opportunity.

Report Scope

This market research report provides a comprehensive analysis of the global Ironless Motor Module market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Ironless Motor Module market was valued at USD 437 million in 2024 and is projected to reach USD 764 million by 2032, growing at a CAGR of 8.6%.

- Segmentation Analysis: Detailed breakdown by product type (Brushed Motor Module, Brushless Motor Module), application (Industrial Automation, Medical Equipment, Transportation, Aerospace, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. and China are key markets, with Asia-Pacific expected to exhibit the highest growth rate.

- Competitive Landscape: Profiles of leading market participants including Siemens, ABB, Yaskawa Electric, Bosch, Schneider Electric, Parker Hannifin, Mitsubishi Electric Corporation, Fanuc Corporation, Moog, and Delta, covering their product portfolios, market share, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging motor technologies, efficiency improvements, integration with smart systems, and advancements in material science for enhanced performance.

- Market Drivers & Restraints: Evaluation of factors such as increasing automation in industries, demand for high-precision motion control, and challenges related to raw material costs and supply chain dynamics.

- Stakeholder Analysis: Strategic insights for motor manufacturers, system integrators, component suppliers, and investors regarding market opportunities and competitive positioning.

The research employs both primary and secondary methodologies, including interviews with industry leaders, analysis of financial reports, and validation through multiple data sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Ironless Motor Module Market?

-> Ironless Motor Module Market was valued at 437 million in 2024 and is projected to reach US$ 764 million by 2032, at a CAGR of 8.6% during the forecast period.

Which key companies operate in Global Ironless Motor Module Market?

-> Key players include Siemens, ABB, Yaskawa Electric, Bosch, Schneider Electric, Parker Hannifin, Mitsubishi Electric Corporation, and Fanuc Corporation.

What are the key growth drivers?

-> Key growth drivers include increasing industrial automation, demand for energy-efficient motors, and growth in medical and aerospace applications.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region due to manufacturing expansion, while North America leads in technological adoption.

What are the emerging trends?

-> Emerging trends include miniaturization of motor modules, integration with IoT systems, and development of high-torque density designs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...