MARKET INSIGHTS

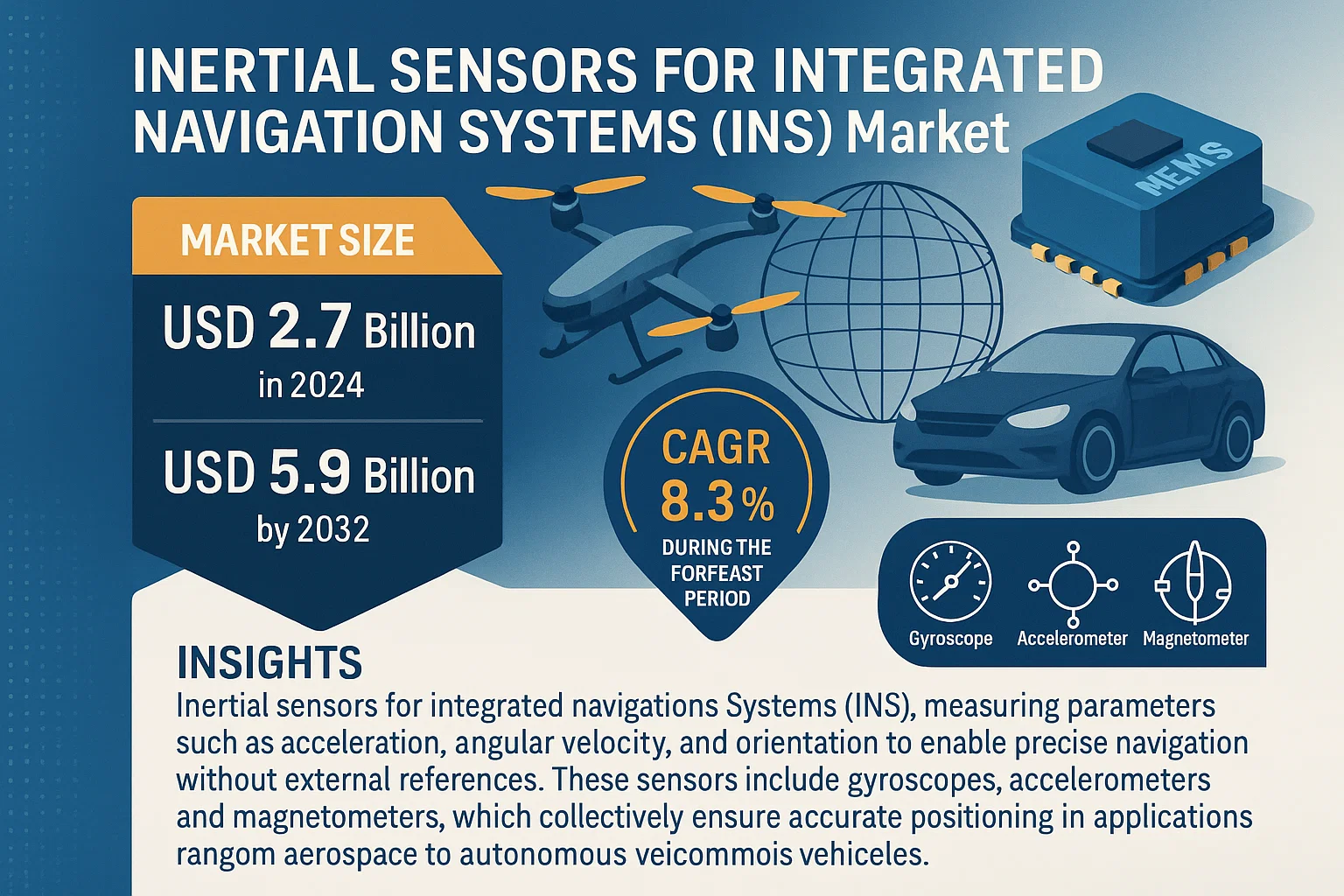

The global Inertial Sensors for Integrated Navigations Systems (INS) Market size was valued at USD 2.7 billion in 2024 to USD 5.9 billion by 2032, exhibiting a CAGR of 8.3% during the forecast period.

Inertial sensors are critical components in INS, measuring parameters such as acceleration, angular velocity, and orientation to enable precise navigation without external references. These sensors include gyroscopes, accelerometers, and magnetometers, which collectively ensure accurate positioning in applications ranging from aerospace to autonomous vehicles. The integration of micro-electromechanical systems (MEMS) technology has further enhanced their precision and affordability.

The market is expanding due to rising demand in aerospace and defense, where INS are indispensable for missile guidance and unmanned aerial vehicles (UAVs). The automotive sector is also a key driver, with increasing adoption of advanced driver-assistance systems (ADAS) and autonomous vehicles. In 2024, the gyroscopes segment accounted for the largest market share at 42%, driven by their use in high-precision applications. Leading players like STMicroelectronics, TDK (InvenSense), and Analog Devices are investing in R&D to develop next-generation sensors with improved accuracy and lower power consumption.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Aerospace and Defense Applications to Drive Market Growth

The aerospace and defense sectors are primary drivers for inertial sensors in integrated navigation systems, accounting for over 40% of global demand. Modern aircraft, unmanned aerial vehicles (UAVs), and missile guidance systems require highly precise navigation capabilities that can function in GPS-denied environments. Recent military conflicts have demonstrated the critical importance of resilient navigation systems, driving increased investment in inertial sensor technology. The commercial aviation sector is simultaneously upgrading navigation systems to meet next-generation air traffic management requirements, with major aircraft manufacturers integrating advanced INS solutions into new production models. This dual demand from both military and commercial aviation sectors creates a robust growth foundation for the market.

Autonomous Vehicle Development Accelerating Market Expansion

The rapid advancement of autonomous vehicle technology represents a significant growth driver for inertial sensors in integrated navigation systems. Automotive manufacturers are incorporating increasingly sophisticated INS solutions to enable precise positioning, navigation, and timing capabilities essential for autonomous operation. These systems provide continuous positioning data during GPS signal interruptions in urban canyons, tunnels, and adverse weather conditions. The automotive industry’s transition toward higher levels of autonomy requires inertial sensors that can maintain positioning accuracy within centimeters, driving demand for high-performance MEMS-based solutions. Major automotive suppliers are developing specialized INS packages specifically designed for autonomous driving applications, creating substantial market opportunities.

Furthermore, regulatory developments supporting autonomous vehicle testing and deployment are accelerating market adoption. Several countries have established frameworks allowing expanded autonomous vehicle operations on public roads, necessitating reliable navigation systems. These regulatory advancements are complemented by significant investments in autonomous vehicle technology, with industry leaders allocating substantial resources toward developing robust navigation solutions that incorporate advanced inertial sensors.

➤ For instance, recent industry analysis indicates that the autonomous vehicle sector is projected to require approximately 15 million high-performance inertial measurement units annually by 2028, representing a compound annual growth rate of over 30% from current deployment levels.

The convergence of technological advancement and regulatory support creates a favorable environment for market expansion, with inertial sensors becoming increasingly critical for safe and reliable autonomous navigation across various vehicle platforms.

MARKET CHALLENGES

High Development and Manufacturing Costs Present Significant Market Challenges

The inertial sensors market faces substantial challenges related to development and manufacturing costs, particularly for high-performance applications. Developing precision-grade inertial sensors requires significant investment in specialized fabrication facilities, calibration equipment, and testing infrastructure. The manufacturing process for tactical and navigation-grade sensors involves complex procedures including wafer-level packaging, hermetic sealing, and extensive calibration routines that contribute to elevated production costs. These economic factors create barriers for new market entrants and limit adoption in cost-sensitive applications.

Other Challenges

Technical Performance Limitations

Achieving the required performance levels for critical applications remains challenging, particularly regarding bias stability, scale factor accuracy, and noise characteristics. While MEMS technology has advanced significantly, higher-grade applications often still require fiber optic or ring laser gyroscopes that come with substantially higher costs and manufacturing complexities.

Integration Complexities

Integrating inertial sensors with other navigation systems presents technical challenges related to sensor fusion algorithms, calibration procedures, and system alignment. These integration complexities require specialized expertise and can increase development timelines and costs for end-users implementing INS solutions.

MARKET RESTRAINTS

Supply Chain Constraints and Component Shortages Restricting Market Growth

The inertial sensors market faces significant restraints from ongoing supply chain challenges and component shortages affecting the broader electronics industry. The specialized nature of inertial sensor manufacturing relies on specific materials, fabrication equipment, and testing instruments that have experienced supply disruptions and extended lead times. These constraints impact production capacity and ability to meet growing market demand, particularly for high-performance sensors used in critical applications.

Additionally, the market is experiencing limitations in manufacturing capacity for advanced MEMS devices, with only a limited number of foundries capable of producing the required precision components. This capacity constraint is exacerbated by the lengthy qualification processes required for aerospace and defense applications, which can take several years and involve rigorous testing protocols. The combination of supply chain challenges and manufacturing capacity limitations creates significant headwinds for market expansion.

Geopolitical factors further complicate the supply situation, with export controls and trade restrictions affecting the global availability of certain high-performance inertial sensors. These factors collectively restrain market growth by limiting product availability, increasing costs, and extending delivery timelines for end-users across various application sectors.

MARKET OPPORTUNITIES

Emerging Industrial and Robotics Applications Creating New Growth Frontiers

The expanding adoption of industrial automation and robotics presents substantial growth opportunities for inertial sensors in integrated navigation systems. Modern manufacturing facilities increasingly utilize autonomous mobile robots for material handling, logistics, and assembly operations, requiring precise navigation capabilities. These applications demand reliable positioning systems that can operate in environments where GPS signals are unavailable or unreliable, creating ideal use cases for INS solutions incorporating inertial sensors.

Industrial IoT applications are driving demand for inertial sensors in equipment monitoring, predictive maintenance, and operational analytics. The ability to accurately track equipment position, orientation, and movement patterns enables more efficient operations and maintenance scheduling. This market segment is experiencing rapid growth as industries seek to improve operational efficiency through digital transformation initiatives.

Furthermore, the development of advanced robotics for healthcare, logistics, and service applications is creating additional opportunities for precision inertial sensors. These applications require high-accuracy navigation capabilities in diverse environments, driving innovation in sensor technology and creating new market segments beyond traditional aerospace and automotive applications. The convergence of industrial automation, robotics, and IoT technologies represents a significant growth vector for the inertial sensors market in integrated navigation systems.

INERTIAL SENSORS FOR INTEGRATED NAVIGATION SYSTEMS (INS) MARKET TRENDS

Miniaturization and Enhanced Performance of MEMS Technology to Emerge as a Dominant Trend

The relentless drive towards miniaturization, coupled with significant performance enhancements in Micro-Electro-Mechanical Systems (MEMS) technology, is fundamentally reshaping the INS market. While traditional fiber-optic and ring-laser gyroscopes offer superior accuracy, their high cost and large size have historically limited their deployment to high-end aerospace and defense applications. The evolution of MEMS-based inertial sensors, however, has successfully bridged this gap by delivering a compelling combination of small form factor, low power consumption, ruggedness, and increasingly competitive performance. This technological leap is directly fueling market expansion into cost-sensitive, high-volume sectors such as automotive, consumer electronics, and industrial robotics. The performance of these sensors is often quantified by key parameters like angle random walk (ARW) and bias instability, with leading MEMS gyroscopes now achieving ARW values below 0.1 °/√h, a figure that was once the exclusive domain of much larger and more expensive technologies. This trend is critical because it enables the proliferation of precise navigation and stabilization in applications where it was previously economically unfeasible.

Other Trends

Integration with Complementary Technologies for Robust Positioning

The growing necessity for uninterrupted and accurate positioning, especially in challenging urban and indoor environments where Global Navigation Satellite System (GNSS) signals are weak or entirely absent, is driving the strategic integration of INS with other sensing technologies. This sensor fusion approach is becoming a standard methodology to overcome the inherent drift limitations of standalone inertial systems. INS are increasingly being coupled not only with GNSS but also with computer vision systems, LiDAR, odometry, and even cellular 5G signals to create resilient navigation solutions. This trend is particularly pronounced in the development of autonomous vehicles, advanced driver-assistance systems (ADAS), and automated guided vehicles (AGVs) for smart warehouses. The fusion algorithms, often powered by sophisticated Kalman filters and AI, intelligently weigh the inputs from each sensor to provide a continuous, reliable, and precise pose estimation (position and orientation), making this integration a cornerstone for the next generation of autonomous systems.

Rising Defense Expenditures and Modernization Programs

Geopolitical tensions and the global modernization of military assets are acting as a powerful catalyst for the INS market, particularly for high-performance sensor segments. Nations are investing heavily in upgrading their defense capabilities, which includes the procurement of advanced missile guidance systems, unmanned aerial vehicles (UAVs), military aircraft, and naval vessels—all of which are critically dependent on precise inertial navigation. These systems require sensors that can operate with extreme reliability and accuracy in GNSS-denied environments, often under demanding conditions. This has led to sustained investment in research and development for next-generation gyroscopes and accelerometers that offer improved performance, reduced size, weight, and power (SWaP), and enhanced resistance to jamming and spoofing. The defense sector’s unwavering demand for cutting-edge, reliable INS technology ensures a steady stream of innovation and market growth for manufacturers capable of meeting these stringent requirements.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Alliances Drive Market Positioning

The global inertial sensors for integrated navigation systems (INS) market exhibits a fragmented yet dynamic competitive structure, characterized by a mix of established semiconductor giants, specialized defense contractors, and emerging technology firms. While the market is populated by numerous players, a core group of companies consistently leads through technological superiority, extensive manufacturing capabilities, and deep-rooted relationships in key end-markets like aerospace, defense, and automotive.

STMicroelectronics and Analog Devices, Inc. are pivotal forces, commanding significant market share. Their dominance is largely attributable to their vertically integrated manufacturing processes and massive R&D investments in Micro-Electro-Mechanical Systems (MEMS) technology. These companies provide high-performance, miniaturized sensors that are critical for modern INS applications, from consumer drones to advanced driver-assistance systems (ADAS). Their global distribution networks ensure a steady supply to OEMs worldwide.

Meanwhile, defense-oriented entities like Norinco Group (China North Industries Group Corporation Limited) and SDI (System Dynamics International) hold substantial influence, particularly within the Asia-Pacific region and in government contracts. Their growth is fueled by robust national defense budgets and a strategic focus on developing sovereign navigation technologies that are independent of foreign supply chains. These players often excel in producing high-grade, ruggedized sensors designed for the most demanding military and aerospace environments.

The competitive intensity is further amplified by the strategic movements of other key participants. Companies such as TDK Corporation (through its subsidiary InvenSense) and NXP Semiconductors are aggressively strengthening their market presence. This is achieved through continuous product portfolio enhancements aimed at improving accuracy and reducing power consumption, alongside strategic partnerships with automotive tier-1 suppliers and consumer electronics manufacturers. Their focus on innovation ensures they remain at the forefront of addressing the evolving needs of autonomous navigation.

Furthermore, specialized manufacturers like Honeywell (often a key player though not listed in the initial roster, their presence is well-known in high-accuracy segments) and Murata Manufacturing Co., Ltd. compete by offering highly reliable components. They cater to niche applications that require exceptional performance, thereby securing a loyal customer base and maintaining healthy margins in a price-sensitive market.

List of Key Companies Profiled in the Inertial Sensors for INS Market

- STMicroelectronics (Switzerland)

- Analog Devices, Inc. (U.S.)

- TDK Corporation (InvenSense) (Japan)

- NXP Semiconductors N.V. (Netherlands)

- Murata Manufacturing Co., Ltd. (Japan)

- Norinco Group (China)

- Navgnss (China)

- AVIC-Gyro (Aviation Industry Corporation of China) (China)

- SDI (System Dynamics International) (U.S.)

- HY Technology (China)

- Baocheng (China)

- Right M&C (China)

- Chinastar (China)

- Chenxi (China)

- FACRI (China)

- StarNeto (U.S.)

Segment Analysis:

By Type

Gyroscopes Segment Dominates the Market Due to Critical Role in Measuring Angular Velocity and Maintaining Orientation

The market is segmented based on type into:

- Gyroscopes

- Subtypes: Fiber-optic gyroscopes (FOG), Ring laser gyroscopes (RLG), MEMS gyroscopes, and others

- Accelerometers

- Subtypes: MEMS accelerometers, Piezoelectric accelerometers, and others

- Others

- Subtypes: Inertial measurement units (IMUs), Attitude and heading reference systems (AHRS), and others

By Application

Aerospace Segment Leads Due to High Demand for Precision Navigation in Commercial and Defense Aircraft

The market is segmented based on application into:

- Aerospace

- Subtypes: Commercial aviation, Military aircraft, Unmanned aerial vehicles (UAVs), and others

- Automotive

- Subtypes: Advanced driver-assistance systems (ADAS), Autonomous vehicles, and others

- Others

- Subtypes: Marine navigation, Industrial automation, Robotics, and others

By Technology

MEMS Technology Segment Gains Traction Due to its Miniaturization, Cost-Effectiveness, and High Volume Manufacturing

The market is segmented based on technology into:

- MEMS (Micro-Electro-Mechanical Systems)

- FOG (Fiber-Optic Gyroscopes)

- RLG (Ring Laser Gyroscopes)

- Others

- Subtypes: Mechanical gyroscopes, Hemispherical resonator gyroscopes (HRG), and others

By End User

Defense and Military Segment Holds Significant Share Owing to Extensive Use in Missile Guidance, Naval Vessels, and Ground Vehicles

The market is segmented based on end user into:

- Defense and Military

- Commercial Aviation

- Automotive

- Industrial

- Others

- Subtypes: Maritime, Surveying and mapping, and others

Regional Analysis: Inertial Sensors for Integrated Navigation Systems (INS) Market

Asia-Pacific

The Asia-Pacific region is the dominant force in the global INS market, driven by massive manufacturing capabilities and extensive adoption across aerospace, automotive, and consumer electronics sectors. China, as the world’s largest producer and consumer, leads this growth, supported by substantial government investment in defense modernization and autonomous vehicle initiatives. Japan and South Korea are critical hubs for high-precision MEMS (Micro-Electro-Mechanical Systems) sensor production, supplying global automotive giants and consumer electronics firms. The region’s expansion is further fueled by rapid urbanization, increasing demand for unmanned aerial vehicles (UAVs), and the proliferation of advanced driver-assistance systems (ADAS) in the automotive industry. While cost-competitive MEMS sensors are widely used, there is a growing investment in higher-accuracy fiber-optic gyroscopes (FOGs) and ring laser gyroscopes (RLGs) for defense and aerospace applications, indicating a maturing technological landscape.

North America

North America represents a technologically advanced and innovation-driven market, characterized by stringent performance requirements and significant defense expenditure. The United States, with its robust aerospace and defense sector, is a major consumer of high-performance inertial sensors. Key drivers include modernization programs for military aircraft, naval vessels, and missile systems, alongside burgeoning applications in autonomous vehicles and space exploration initiatives led by NASA and private companies. The region is a leader in the development and adoption of sophisticated technologies like Hemispherical Resonator Gyroscopes (HRGs) and advanced MEMS for their superior reliability and precision. Furthermore, substantial R&D investments from both established players and startups continue to push the boundaries of miniaturization and accuracy, ensuring North America remains at the forefront of INS technological advancement.

Europe

Europe’s market is shaped by a strong aerospace industry, rigorous regulatory standards for safety and performance, and active participation in global defense and space programs. Countries like Germany, France, and the U.K. host leading manufacturers and are integral to pan-European projects such as the Galileo satellite navigation system, which creates sustained demand for highly reliable INS components. The automotive sector, particularly in Germany, is a significant driver, integrating inertial sensors for electronic stability control, navigation, and emerging autonomous driving functions. The region’s focus is on achieving high levels of accuracy, durability, and compliance with international standards, fostering a competitive environment for both MEMS and optical gyroscope technologies. Collaborative research initiatives between academia and industry further bolster innovation and maintain Europe’s position as a key market for quality and precision.

Middle East & Africa

The market in the Middle East & Africa is emerging, primarily propelled by defense modernization programs and infrastructure development. Nations like Israel, Turkey, and Saudi Arabia are investing heavily in military applications, including guided munitions, UAVs, and naval systems, which require dependable inertial navigation solutions. Israel, in particular, has a well-developed defense technology sector with several indigenous manufacturers. While the market volume is smaller compared to other regions, the demand is for high-value, performance-critical systems. Growth is also supported by increasing activities in the oil & gas sector for surveying and drilling applications. However, the market’s expansion faces challenges from geopolitical instability and varying levels of technological infrastructure across different countries, though long-term potential remains significant.

South America

South America’s INS market is in a developing phase, with growth opportunities primarily linked to defense procurement and gradual industrial automation. Brazil and Argentina are the most active markets, with Brazil’s aerospace ambitions, including its defense and space programs, generating demand for inertial sensors. Agricultural automation and mining operations also present niche applications for these systems. However, the market’s growth is tempered by economic volatility, which can delay large-scale defense and infrastructure projects, and limited local manufacturing capabilities, leading to a reliance on imports. Despite these challenges, the region represents a potential growth area as economies stabilize and invest more in technological modernization across various sectors.

Report Scope

This market research report provides a comprehensive analysis of the global Inertial Sensors for Integrated Navigation Systems (INS) market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD million in 2024 and is projected to reach USD million by 2032.

- Segmentation Analysis: Detailed breakdown by product type (gyroscopes, accelerometers, others), application (aerospace, automotive, others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America (U.S., Canada, Mexico), Europe (Germany, France, U.K.), Asia-Pacific (China, Japan, India), and other regions with country-level analysis.

- Competitive Landscape: Profiles of leading players including Navgnss, STMicroelectronics, Analog Devices, TDK (InvenSense), and NXP Semiconductors, covering their product portfolios and market strategies.

- Technology Trends: Assessment of MEMS technology advancements, AI integration in navigation systems, and miniaturization trends in inertial sensors.

- Market Drivers & Restraints: Evaluation of factors such as increasing defense budgets, autonomous vehicle adoption, and challenges like high development costs.

- Stakeholder Analysis: Strategic insights for sensor manufacturers, system integrators, and investors in the INS ecosystem.

The research methodology combines primary interviews with industry experts and analysis of verified market data to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Inertial Sensors for INS Market?

->Inertial Sensors for Integrated Navigations Systems (INS) Market size was valued at USD 2.7 billion in 2024 to USD 5.9 billion by 2032, exhibiting a CAGR of 8.3% during the forecast period.

Which key companies operate in this market?

-> Major players include STMicroelectronics, Analog Devices, TDK (InvenSense), NXP Semiconductors, Murata, and Navgnss, among others.

What are the key growth drivers?

-> Growth is driven by increasing defense spending, autonomous vehicle development, and demand for precision navigation in aerospace applications.

Which region dominates the market?

-> North America currently leads in market share, while Asia-Pacific is expected to show the highest growth rate during the forecast period.

What are the emerging trends?

-> Emerging trends include MEMS technology miniaturization, AI-enhanced navigation algorithms, and integration with GNSS systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...