MARKET INSIGHTS

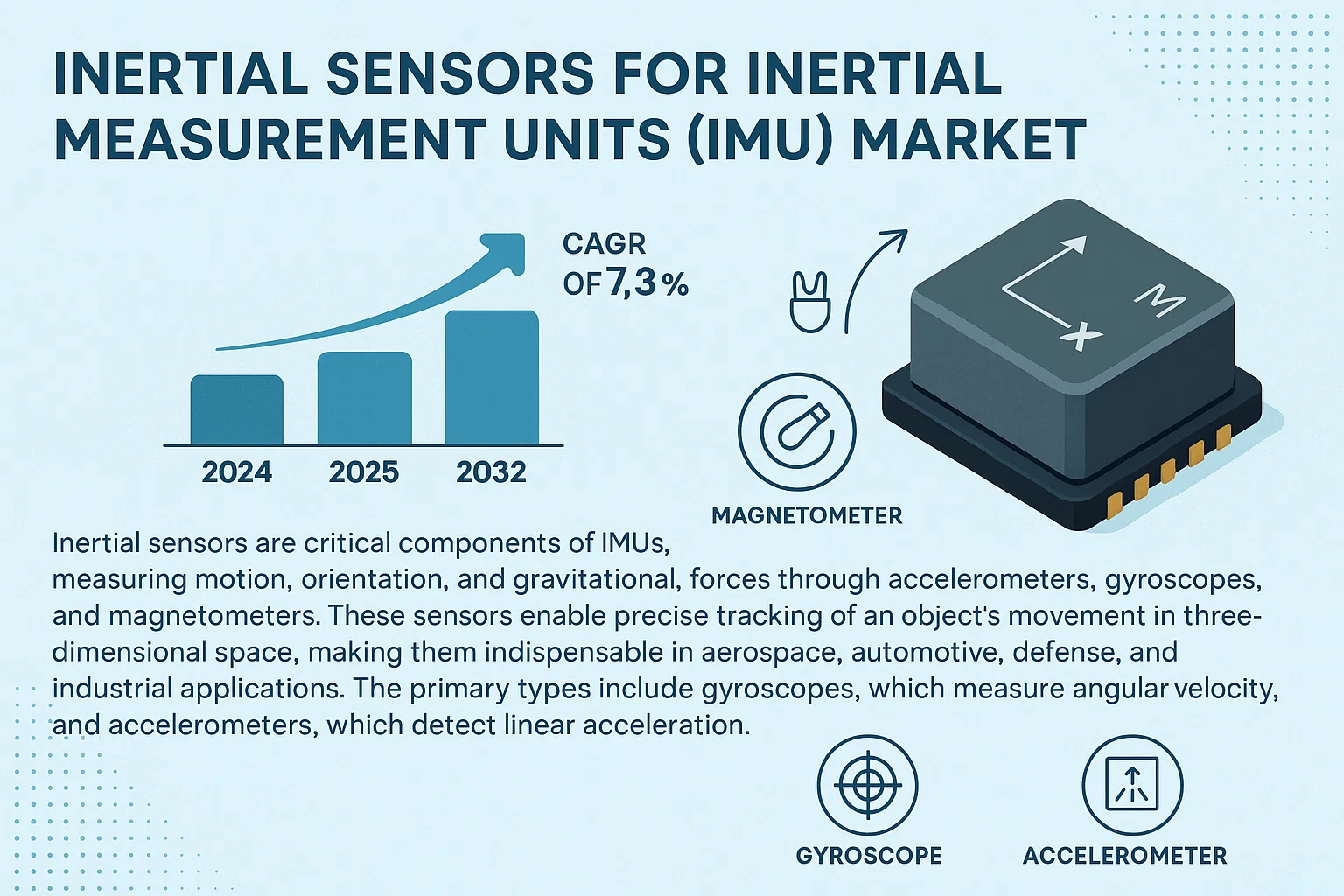

The global Inertial Sensors for Inertial Measurement Units (IMU) Market was valued at USD 4.2 billion in 2024 to USD 4.7 billion in 2025 to USD 8.1 billion by 2032, exhibiting a CAGR of 7.3% during the forecast period.

Inertial sensors are critical components of IMUs, measuring motion, orientation, and gravitational forces through accelerometers, gyroscopes, and magnetometers. These sensors enable precise tracking of an object’s movement in three-dimensional space, making them indispensable in aerospace, automotive, defense, and industrial applications. The primary types include gyroscopes, which measure angular velocity, and accelerometers, which detect linear acceleration.

Market growth is driven by increasing demand for autonomous vehicles, unmanned aerial vehicles (UAVs), and advanced navigation systems. The aerospace sector remains a key revenue contributor, accounting for over 35% of market share in 2024. However, the automotive segment is projected to grow at the fastest CAGR of 9.2% through 2032 due to rising adoption of advanced driver-assistance systems (ADAS). Recent developments include STMicroelectronics’ launch of its ISM330IS sensor in 2024, combining inertial measurement with edge computing capabilities for real-time processing. Key players like Analog Devices, TDK (InvenSense), and NXP Semiconductors continue to dominate the market through continuous R&D and strategic partnerships.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Autonomous Vehicles Accelerates Demand for High-Precision IMUs

The automotive industry is undergoing a seismic shift with the rapid development of autonomous driving technologies, which heavily rely on inertial sensors for precise navigation and stability control. The global autonomous vehicle market is projected to grow at a CAGR of over 20% through 2030, directly fueling demand for advanced IMUs. These sensors provide critical real-time data about vehicle orientation, acceleration, and directional changes – essential inputs for autonomous decision-making systems. Leading automotive manufacturers are increasingly integrating MEMS-based IMUs into ADAS (Advanced Driver Assistance Systems) to achieve Level 4 autonomy, with some premium models already featuring over 15 different inertial sensors per vehicle.

Defense Modernization Programs Drive Military-Grade IMU Adoption

Government investments in defense modernization are creating substantial opportunities for high-performance inertial sensors. Modern warfare systems including unmanned aerial vehicles (UAVs), precision-guided munitions, and inertial navigation systems for submarines all require rugged IMUs that maintain accuracy in GPS-denied environments. The defense sector currently accounts for approximately 35% of the high-end IMU market. Recent geopolitical tensions have accelerated spending, with major military powers increasing their defense budgets by 5-10% annually, much of which is allocated to navigation and guidance systems. Fiber optic gyroscopes and ring laser gyroscopes are seeing particularly strong demand for their exceptional stability and resistance to electromagnetic interference.

Industrial Automation Boom Creates New Applications for IMUs

The fourth industrial revolution is driving unprecedented adoption of inertial sensors in manufacturing and robotics applications. Modern industrial robots require precise motion tracking for functions like robotic arm control, automated guided vehicle (AGV) navigation, and equipment stabilization. The global industrial automation market is expected to exceed $300 billion by 2026, with IoT-enabled devices increasingly incorporating MEMS IMUs for vibration monitoring and predictive maintenance. In warehouse automation alone, the use of inertial sensors has grown by over 40% in the past three years, as e-commerce fulfillment centers deploy thousands of autonomous mobile robots equipped with multi-axis accelerometers and gyroscopes.

MARKET CHALLENGES

Precision Drift and Environmental Sensitivity Pose Technical Hurdles

While inertial sensors have made significant advancements, they still face fundamental physics limitations that challenge their accuracy over extended periods. MEMS devices particularly suffer from bias instability and angular random walk, causing measurement drift that accumulates over time. In critical navigation applications, even minute errors can result in substantial positional inaccuracies – a 0.01° bias in a tactical-grade IMU can lead to position errors exceeding 1 nautical mile after one hour of operation. Temperature variations, shock, and vibration further compound these errors, requiring complex compensation algorithms that increase system complexity and cost.

Other Significant Challenges

Miniaturization vs. Performance Tradeoffs

The market push for smaller, lower-power IMUs conflicts with the need for high performance in demanding applications. While consumer devices require compact sensors under 10mm³, these often sacrifice noise performance and dynamic range. Achieving high-performance metrics like bias stability below 0.1° per hour in small form factors remains an engineering challenge that limits applications in sectors like aerospace and defense.

Calibration Complexity

Advanced IMUs require extensive factory calibration and periodic alignment procedures to maintain accuracy. The calibration process for navigation-grade systems can take several hours and often requires expensive precision equipment, adding to production costs and lead times. Field recalibration of deployed units presents additional logistical challenges in remote or harsh environments.

MARKET RESTRAINTS

High Costs Limit Adoption in Price-Sensitive Markets

The inertial sensor market exhibits extreme price stratification, with consumer-grade MEMS devices costing under $5 each while aerospace-grade FOG (Fiber Optic Gyro) systems can exceed $100,000. This wide price disparity creates adoption barriers in mid-range applications where reliability requirements exceed MEMS capabilities but budget constraints prohibit high-end solutions. Commercial aviation GPS/INS systems, for example, often require performance characteristics between tactical and navigation grades, yet solutions in this “sweet spot” remain prohibitively expensive for many operators.

Supply Chain Constraints Impact Sensor Manufacturing

Recent semiconductor shortages have exposed vulnerabilities in IMU supply chains, particularly for specialized components like quartz MEMS timing references and precision mechanical parts. Lead times for certain high-performance gyroscopes have extended to 12-18 months as manufacturers struggle to source radiation-hardened electronics and rare earth materials. The industry also faces production bottlenecks in MEMS fabrication, where limited cleanroom capacity at 200mm fabs constrains output during periods of surging demand.

MARKET OPPORTUNITIES

Emerging AI/ML Algorithms Unlock New IMU Applications

Advancements in machine learning are revolutionizing how inertial sensor data is processed and utilized. Modern AI techniques can extract meaningful motion signatures from noisy MEMS data, enabling new use cases in fields like structural health monitoring and human activity recognition. The integration of neural networks with IMU data streams is particularly promising for wearable devices, where motion classification algorithms help detect falls in elderly care applications with over 95% accuracy. Sensor fusion with AI is also improving pedestrian dead reckoning systems, reducing navigation errors in smartphone applications by up to 60% compared to traditional Kalman filtering approaches.

Satellite Constellations Drive Demand for Space-Qualified IMUs

The booming satellite industry presents significant growth potential for radiation-hardened inertial sensors. With over 10,000 small satellites expected to launch in the next decade – many for low Earth orbit constellations – the demand for compact, reliable attitude control systems is surging. Modern microsatellites increasingly incorporate MEMS-based IMUs for coarse pointing and safe mode operations, complementing higher-precision star trackers. Recent developments in MEMS technology have achieved radiation tolerance up to 50 krad, making them viable for missions lasting 5-7 years without requiring bulky shielding.

Medical Robotics Creates New Precision IMU Requirements

The healthcare sector is emerging as a key growth area for specialized inertial sensors. Surgical robotics platforms require ultra-precise motion tracking for instrument positioning, with angular resolution requirements often below 0.01°. New applications in rehabilitation robotics and prosthetic limb control are driving innovation in low-latency IMU designs with high dynamic range. The medical robotics market is projected to grow at 17% CAGR through 2030, creating substantial opportunities for inertial sensor manufacturers who can meet stringent biocompatibility and EMI requirements for clinical environments.

INERTIAL SENSORS FOR INERTIAL MEASUREMENT UNITS (IMU) MARKET TRENDS

Miniaturization and Enhanced Precision to Emerge as a Dominant Trend

The relentless drive towards miniaturization and enhanced precision is fundamentally reshaping the inertial sensor landscape for IMUs. This trend is primarily fueled by the explosive growth in consumer electronics, drones, and advanced automotive systems like autonomous driving, all of which demand smaller, more power-efficient, and incredibly accurate sensors. The evolution from traditional mechanical gyroscopes and accelerometers to Micro-Electro-Mechanical Systems (MEMS) technology has been pivotal, enabling the production of sensors that are not only smaller and cheaper but also offer superior performance. Recent innovations are pushing the boundaries further with the development of 9-axis IMUs that integrate a 3-axis gyroscope, a 3-axis accelerometer, and a 3-axis magnetometer into a single, compact package. This high level of integration is critical for applications requiring complex motion tracking and orientation sensing in space-constrained environments. Furthermore, advancements in sensor fusion algorithms, which intelligently combine data from multiple inertial and other sensors, are drastically improving overall system accuracy and reliability, mitigating the inherent drift errors associated with individual sensor types.

Other Trends

Proliferation in Autonomous Vehicles and Advanced Driver-Assistance Systems (ADAS)

The automotive sector represents one of the most significant growth engines for IMU inertial sensors, driven by the rapid adoption of Autonomous Vehicles (AVs) and Advanced Driver-Assistance Systems (ADAS). These systems rely heavily on high-performance IMUs for critical functions such as electronic stability control, rollover detection, and, most importantly, navigation. An IMU provides vital dead reckoning capabilities, allowing a vehicle to accurately track its position, orientation, and velocity even when satellite signals from GPS are temporarily lost or degraded, such as in urban canyons or tunnels. The demand for higher-grade, automotive-qualified sensors that can operate reliably under harsh conditions and meet stringent safety standards is accelerating. This is evidenced by the increasing integration of these sensors into Level 2+ and Level 3 autonomous systems, with the market for automotive MEMS sensors projected to see substantial growth to support the millions of units required for mass-market autonomy.

Expansion into Industrial IoT and Robotics

Beyond consumer and automotive applications, the industrial Internet of Things (IoT) and robotics sectors are creating robust new demand vectors for inertial sensors. In industrial settings, IMUs are indispensable for asset tracking, monitoring the orientation and movement of heavy machinery, and ensuring operational safety. They enable predictive maintenance by detecting abnormal vibrations or tilts that could signal impending equipment failure. In robotics, the need for precise navigation, stabilization, and manipulator control is paramount. Inertial sensors provide the essential feedback for a robot to understand its own movement and orientation in space, which is a foundational requirement for everything from warehouse logistics robots to sophisticated surgical robotic systems. This expansion is driving the need for sensors that offer a compelling balance of performance, power consumption, and cost, suitable for deployment at scale across smart factories and automated workflows. The convergence of 5G connectivity and edge computing is further amplifying this trend, enabling real-time data processing from distributed IMU networks.

COMPETITIVE LANDSCAPE

Key Industry Players

Advancements in MEMS Technology Drive Competition Among Leading Manufacturers

The global inertial sensors for inertial measurement units (IMU) market features a mix of established multinational corporations and emerging regional players competing on technological innovation and production capabilities. STMicroelectronics leads the market with its cutting-edge MEMS-based gyroscopes and accelerometers, capturing approximately 22% revenue share in 2024 through its strong foothold in automotive and industrial applications across Europe and Asia-Pacific.

Analog Devices, Inc. and TDK (InvenSense) maintain significant market presence, collectively accounting for over 30% of total IMU sensor shipments in 2024. Their leadership stems from continuous research investments in high-precision navigation systems and strategic partnerships with aerospace manufacturers.

Chinese manufacturers including Navgnss and Norinco Group are rapidly expanding their market share through cost-competitive solutions for consumer electronics. These domestic players have increased production capacity by 35% since 2022 to meet growing demand from smartphone and drone manufacturers.

Meanwhile, Japanese firm Murata is strengthening its portfolio with next-generation vibration-resistant sensors, particularly targeting autonomous vehicle applications where reliability is mission-critical. Their recent collaboration with major European automakers has positioned them as a preferred supplier for advanced driver assistance systems (ADAS).

List of Key Inertial Sensor Manufacturers Profiled

- STMicroelectronics (Switzerland)

- Analog Devices, Inc. (U.S.)

- TDK Corporation (InvenSense) (Japan)

- Navgnss (China)

- Norinco Group (China)

- Murata Manufacturing Co., Ltd. (Japan)

- NXP Semiconductors (Netherlands)

- HY Technology (China)

- Right M&C (China)

- Avic-gyro (China)

- SDI Technologies (Taiwan)

- Baocheng (China)

- Chinastar (China)

- Chenxi (China)

- FACRI (China)

- StarNeto (Taiwan)

Segment Analysis:

By Type

Gyroscopes Segment Dominates Due to Critical Role in Navigation and Stabilization Systems

The market is segmented based on type into:

- Gyroscopes

- Subtypes: Fiber optic gyroscopes (FOG), Ring laser gyroscopes (RLG), MEMS gyroscopes, and others

- Accelerometers

- Subtypes: MEMS accelerometers, Piezoelectric accelerometers, and others

- Magnetometers

- Others

By Application

Aerospace Segment Leads Owing to Extensive Use in Flight Control and Navigation Systems

The market is segmented based on application into:

- Aerospace

- Sub-applications: Commercial aircraft, Military aircraft, UAVs, and space systems

- Automotive

- Sub-applications: Advanced driver assistance systems (ADAS), Autonomous vehicles, and vehicle stability control

- Industrial

- Marine

- Others

By Technology

MEMS Technology Gains Traction Due to Miniaturization and Cost Efficiency

The market is segmented based on technology into:

- MEMS (Micro-Electro-Mechanical Systems)

- FOG (Fiber Optic Gyroscopes)

- RLG (Ring Laser Gyroscopes)

- Others

Regional Analysis: Inertial Sensors for Inertial Measurement Units (IMU) Market

Asia-Pacific

The Asia-Pacific region dominates the global IMU market, driven by rapid industrialization and technological advancements in key economies like China and Japan. China, in particular, is a major manufacturing hub for inertial sensors, with companies like Navgnss, HY Technology, and Baocheng leading production. The region benefits from strong government support for aerospace and automotive sectors, which are primary end-users of IMUs. Additionally, increasing investments in autonomous vehicles and IoT applications further propel demand. Despite cost-sensitive markets like India favoring budget solutions, the shift toward high-precision MEMS-based sensors is accelerating due to smart city initiatives and defense modernization programs.

North America

North America, particularly the U.S., is a high-value market for IMUs, fueled by defense contracts and aerospace innovation. The region emphasizes MEMS technology, with firms like Analog Devices and TDK (InvenSense) spearheading R&D in miniaturized, high-accuracy sensors. The demand is further bolstered by autonomous vehicle projects and UAV applications, backed by strong venture capital funding. Regulatory standards for safety and precision in sectors like aviation create a stringent yet lucrative environment for IMU suppliers. Canada and Mexico are emerging as secondary markets, leveraging cross-border automotive supply chains.

Europe

Europe’s IMU market thrives on precision engineering and regulatory compliance, particularly in automotive (ADAS) and aerospace industries. Germany and France lead with robust R&D infrastructures, supported by players like STMicroelectronics and NXP Semiconductors. The EU’s focus on green mobility accelerates the adoption of IMUs in electric and hybrid vehicles. However, high manufacturing costs and competition from Asia pose challenges. Meanwhile, Eastern Europe is gaining traction as a cost-effective manufacturing base for mid-tier sensor solutions.

Middle East & Africa

This region shows nascent but growing demand, primarily driven by defense and oil & gas sectors. Countries like Israel and Saudi Arabia invest heavily in drones and navigation systems for geopolitical and industrial applications. Limited local production capabilities result in reliance on imports, though partnerships with global manufacturers are gradually fostering domestic expertise. Economic diversification initiatives, such as Saudi Vision 2030, are expected to unlock long-term growth potential.

South America

South America remains a smaller market, constrained by economic instability and fragmented industrial policies. Brazil leads in automotive applications, while Argentina focuses on agricultural drone technologies. The lack of localized R&D and dependence on imports hinder market expansion, though foreign investments in mining and logistics offer incremental opportunities for IMU adoption.

Key Trends: The IMU market is pivoting toward MEMS-based solutions for cost efficiency and scalability, with Asia-Pacific and North America at the forefront of this shift. Aerospace and automotive sectors collectively account for over 60% of global demand. Emerging applications in robotics and AR/VR present untapped growth avenues, though supply chain disruptions and geopolitical tensions remain critical challenges.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Inertial Sensors for Inertial Measurement Units (IMU) markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (gyroscopes, accelerometers, others), application (aerospace, automotive, others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with country-level analysis.

- Competitive Landscape: Profiles of leading manufacturers including Navgnss, STMicroelectronics, TDK (InvenSense), and Analog Devices, with analysis of their market strategies.

- Technology Trends & Innovation: Assessment of MEMS technology advancements, AI integration in IMUs, and miniaturization trends.

- Market Drivers & Restraints: Evaluation of autonomous vehicle adoption, defense spending, and supply chain challenges affecting the IMU sensor market.

- Stakeholder Analysis: Strategic insights for sensor manufacturers, system integrators, and investors in the IMU ecosystem.

The research combines primary interviews with industry experts and analysis of verified market data from regulatory bodies and company financial reports to ensure accuracy.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Inertial Sensors for IMU Market?

-> Inertial Sensors for Inertial Measurement Units (IMU) Market was valued at USD 4.2 billion in 2024 to USD 4.7 billion in 2025 to USD 8.1 billion by 2032, exhibiting a CAGR of 7.3% during the forecast period.

Which key companies operate in Global Inertial Sensors for IMU Market?

-> Key players include STMicroelectronics, TDK (InvenSense), Analog Devices, NXP Semiconductors, Murata, Navgnss, and Norinco Group.

What are the key growth drivers?

-> Key growth drivers include rising demand in autonomous vehicles, increased defense spending, and growth in industrial automation applications.

Which region dominates the market?

-> Asia-Pacific accounts for 42% of global market share in 2024, led by China’s manufacturing capabilities and defense sector investments.

What are the emerging trends?

-> Emerging trends include MEMS technology miniaturization, AI-enhanced sensor fusion algorithms, and quantum inertial sensing developments.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...