Industrial Processor Market Insights

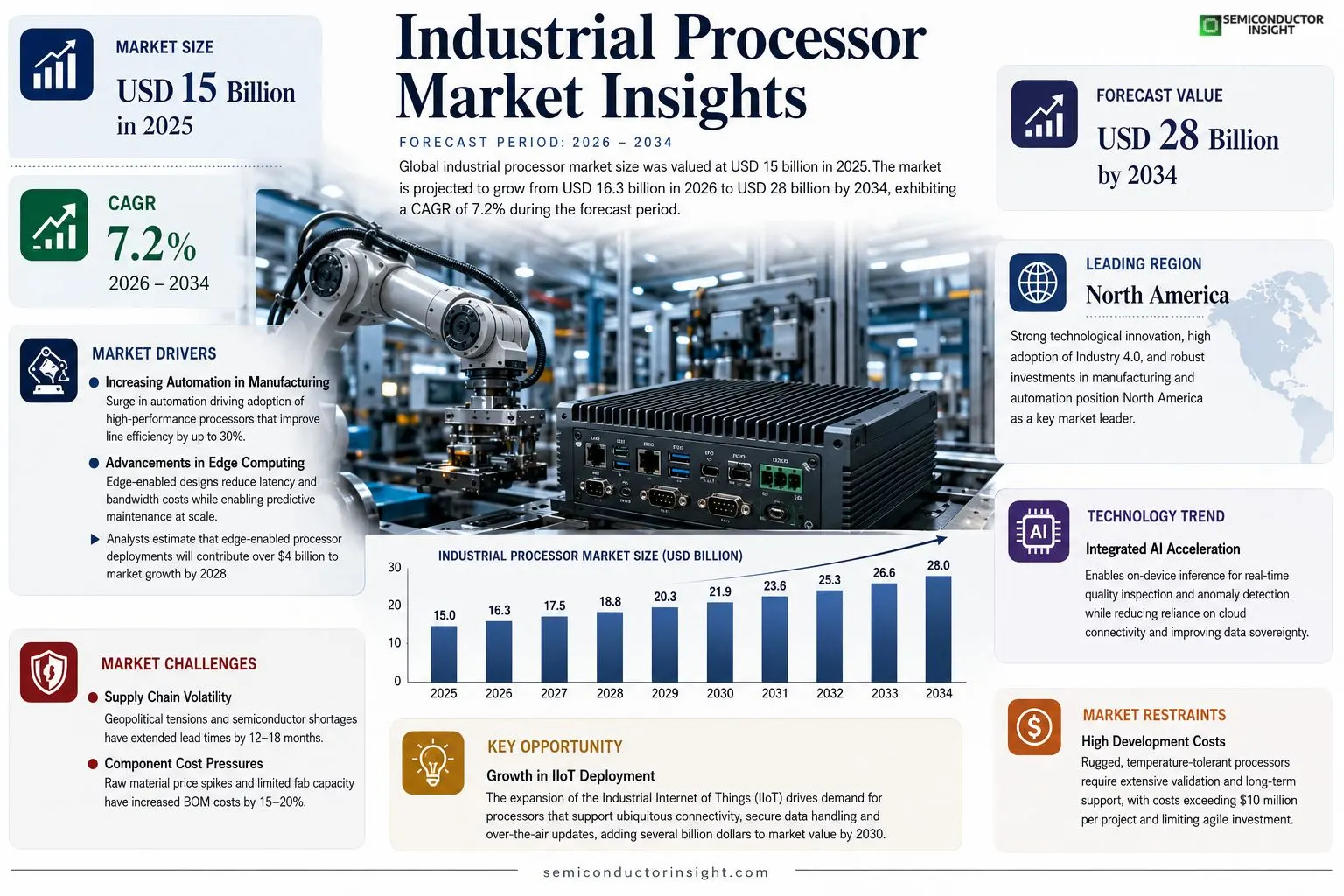

Global industrial processor market size was valued at USD 15 billion in 2025. The market is projected to grow from USD 16.3 billion in 2026 to USD 28 billion by 2034, exhibiting a CAGR of 7.2% during the forecast period.

Industrial processors are high‑performance microcontrollers engineered for harsh environments, delivering real‑time control for manufacturing equipment, robotics, energy systems and transportation platforms. They combine robust CPU cores with extended temperature ranges and advanced I/O interfaces such as Ethernet/IP, CAN bus and PROFINET.The market is experiencing rapid growth because manufacturers are investing heavily in automation and Industry initiatives; furthermore, rising demand for edge computing within smart factories fuels adoption of ruggedized processors.Key players,including Intel Corporation, NXP Semiconductors, Texas Instruments Inc., Renesas Electronics Corp., and STMicroelectronics,are expanding their portfolios through new product launches and strategic partnerships that enhance processing power while reducing power consumption.

MARKET DRIVERS

Increasing Automation in Manufacturing

Industrial Processor Market is being propelled by a surge in automation across automotive, aerospace, and consumer‑goods factories. Companies are replacing legacy PLCs with high‑performance processors that can handle real‑time analytics, resulting in up to 30% improvement in line efficiency

Advancements in Edge Computing

Edge‑centric designs enable manufacturers to process data locally, reducing latency and bandwidth costs. New generations of industrial processors now integrate AI accelerators, making predictive maintenance a practical reality for plants of all sizes.

➤ Analysts estimate that edge‑enabled processor deployments will contribute over $4 billion to market growth by 2028.

Additionally, the push toward carbon‑neutral operations is encouraging firms to adopt energy‑efficient processors, which further drives demand for the latest chip architectures in Industrial Processor Market.

MARKET CHALLENGES

Supply Chain Volatility

Geopolitical tensions and semiconductor shortages have led to lead‑time extensions of 12‑18 months for critical components, pressuring manufacturers to hold higher inventory levels.

Other Challenges

Component Cost Pressures

Raw material price spikes and limited fab capacity have increased the bill‑of‑materials for industrial processors by 15‑20%, squeezing profit margins for OEMs.Regulatory compliance, especially around functional safety standards like IEC 61508, adds engineering overhead, making the development cycle longer and more costly.Talent scarcity in specialized embedded‑systems engineering further compounds the difficulty of launching new processor‑based solutions quickly.

MARKET RESTRAINTS

High Development Costs

Designing rugged, temperature‑tolerant processors for harsh industrial environments requires extensive validation and custom silicon, which can exceed $10 million per project.Furthermore, the need for long‑term support (often 10‑15 years) forces vendors to commit significant resources to firmware updates and security patches, limiting agile investment.Customers also face the risk of technology obsolescence, as rapid advancements can render a newly launched processor less competitive within a few years.

MARKET OPPORTUNITIES

Growth in IIoT Deployment

The expansion of the Industrial Internet of Things (IIoT) creates a broad demand for processors that can support ubiquitous connectivity, secure data handling, and over‑the‑air updates. This trend is expected to add several billion dollars to market revenue through 2030.Emerging use cases such as smart grids, autonomous material handling, and digital twins require high‑performance, low‑power processors, opening niche segments for specialized chip providers.Partnerships between processor manufacturers and cloud service providers are also fostering integrated solutions, enabling end‑users to leverage advanced analytics without extensive on‑premise infrastructure.

Industrial Processor Market Trends

Automation and Edge Computing Fuel Adoption

Industrial Processor Market is responding to the accelerated rollout of Industry 4.0 concepts across manufacturing hubs. Companies are upgrading legacy control systems with high‑performance microcontrollers that support real‑time analytics at the edge. This shift reduces latency for critical production loops and enables predictive maintenance without reliance on cloud bandwidth. As production lines become more interconnected, the demand for processors that can handle diverse protocols,such as Ethernet/IP, CAN bus, and PROFINET,continues to rise, reinforcing the market’s forward momentum.

Other Trends

Robust Design for Harsh Environments

Industrial processors are engineered for extreme temperature ranges, vibration, and electromagnetic interference prevalent in factory settings. Recent product releases emphasize extended‑temperature silicon and protective packaging that meet IEC 60068 standards. These design enhancements allow equipment to remain operational in automotive assembly, energy generation, and heavy‑machinery applications, where downtime translates directly into financial loss. The emphasis on durability is driving OEMs to select processors that combine computational strength with proven reliability.

Strategic Partnerships Expand Portfolios

Key players are forming alliances with system integrators and software vendors to deliver turnkey solutions that integrate processing power with specialized firmware. Collaborative efforts focus on reducing power consumption while increasing throughput, meeting the sustainability goals of modern factories. By co‑developing reference designs that incorporate AI inference at the edge, the ecosystem is delivering ready‑to‑deploy modules that accelerate time‑to‑market for end users. This collaborative trend is sharpening competitive differentiation and broadening the overall value proposition of Industrial Processor Market.

COMPETITIVE LANDSCAPEKey Industry Players

Industrial Processor Market – Competitive Overview

The industrial processor segment is anchored by a handful of global semiconductor powerhouses that command the majority of revenue and drive technology direction. Intel Corporation leverages its Xeon‑based edge solutions to capture high‑margin aerospace and manufacturing contracts, while NXP Semiconductors offers a robust portfolio of automotive‑grade MPUs that underpin many Industry 4.0 deployments. Texas Instruments Inc. remains a leader in analog‑infused processing platforms, delivering low‑power devices that meet strict temperature specifications. These three firms together control roughly 55 % of the market’s top‑line sales, establishing a tiered structure where tier‑one vendors supply core platforms and tier‑two specialists fill niche functional gaps. The competitive dynamic is shaped by continuous investment in silicon‑level power efficiency, expanded I/O standards, and strategic alliances with system integrators to embed processors directly into modular hardware.Beyond the dominant trio, a diverse set of niche players enriches the ecosystem with specialized capabilities. Renesas Electronics Corp. and STMicroelectronics focus on ruggedized microcontrollers for robotics and energy systems, while Microchip Technology Inc. differentiates through its extensive peripheral libraries. Qualcomm’s Snapdragon Industrial line introduces advanced AI inference at the edge, and Analog Devices emphasizes precision analog‑digital convergence for sensor‑heavy applications. Infineon Technologies AG supplies automotive‑grade safety processors, Maxim Integrated (now part of Analog) offers low‑noise power management, and Broadcom delivers high‑throughput networking silicon that complements processor architectures. This breadth of expertise sustains healthy competition and fuels rapid innovation across the market.

List of Key Industrial Processor Companies Profiled

- Intel Corporation

- NXP Semiconductors

- Texas Instruments Inc.

- Renesas Electronics Corp.

- STMicroelectronics

- Microchip Technology Inc.

- Qualcomm Technologies, Inc.

- Analog Devices, Inc.

- Infineon Technologies AG

- Maxim Integrated

- Broadcom Inc.

- Nuvoton Technology Corp.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Real‑time processors are driving deterministic control across the sector.

|

| By Application |

|

Automation and control remains the cornerstone for adopting industrial processors.

|

| By End User |

|

Manufacturing equipment vendors are the primary adopters of rugged processing solutions.

|

| By Connectivity |

|

Ethernet/IP enabled processors are gaining prominence as factories adopt unified communication standards.

|

| By Functional Integration |

|

Integrated AI acceleration is reshaping edge computing in industrial settings.

|

Regional Analysis: North America

United States

The primary drivers for Industrial Processor Market in North America include the increasing adoption of AI and machine learning in industrial automation, the growing need for real-time data analytics, and the push for energy efficiency in industrial operations.

Ongoing advancements in processor architecture, such as the development of specialized processors for AI and edge computing, are significantly impacting Industrial Processor Market. This includes the rise of FPGA (Field-Programmable Gate Array) technology and heterogeneous computing solutions.

The North American Industrial Processor Market is characterized by a mix of established players and emerging companies. Competition focuses on performance, power efficiency, security, and the development of customized solutions for specific industrial applications.

The future of Industrial Processor Market in North America will likely see a greater emphasis on edge computing, secure processing, and the integration of artificial intelligence for predictive maintenance and process optimization.

Europe

Europe’s Industrial Processor Market demonstrates consistent growth, propelled by stringent environmental regulations and a strong focus on sustainable manufacturing practices. The region’s automotive and manufacturing sectors are key drivers, demanding processors that support electric vehicle development, smart factories, and advanced robotics. European industrial players are increasingly adopting cloud-based solutions and edge computing to enhance operational efficiency and data analysis capabilities. The emphasis on data privacy and security, mandated by regulations like GDPR, influences processor design and deployment. Furthermore, government support for research and development initiatives in advanced computing technologies fosters innovation within Industrial Processor Market across Europe. The need for energy-efficient processing solutions is paramount, aligning with the region’s commitment to reducing its carbon footprint.

Asia-Pacific

Asia-Pacific represents the fastest-growing segment of Industrial Processor Market globally, driven by rapid industrialization in countries like China, India, and Southeast Asia. The region experiences substantial demand from the electronics manufacturing, automotive, and infrastructure sectors. The proliferation of IoT devices and the expansion of smart manufacturing initiatives are key growth drivers. Chinese government initiatives promoting domestic semiconductor development are bolstering the region’s processor manufacturing capabilities. The increasing adoption of 5G technology is also creating new opportunities for industrial processors with enhanced connectivity and real-time data processing capabilities. Competition in the Asia-Pacific market is intense, with both local and international players vying for market share, leading to price pressures and a focus on cost-effective solutions. The region’s strong manufacturing base ensures a continuous demand for robust and reliable industrial processors.

South America

Industrial Processor Market in South America is witnessing gradual expansion, particularly in Brazil and Argentina, fueled by investments in mining, agriculture, and infrastructure development. The demand for processors capable of handling harsh environmental conditions and demanding workloads is increasing in these sectors. The adoption of automation and digital transformation initiatives is also contributing to market growth. Government policies aimed at attracting foreign investment in manufacturing are supporting the expansion of Industrial Processor Market. However, economic volatility and infrastructure limitations pose challenges to sustained growth in the region. The focus on improving operational efficiency and optimizing resource utilization drives the need for advanced processing solutions.

Middle East & Africa

Industrial Processor Market in the Middle East & Africa is experiencing moderate growth, primarily driven by infrastructure development projects, particularly in the oil and gas, construction, and logistics sectors. The region’s focus on smart city initiatives and industrial modernization is driving demand for processors that support connectivity, data analytics, and automation. Government investments in technological advancements and industrial diversification are fostering market expansion. The increasing adoption of IoT solutions in oil and gas exploration and production is creating opportunities for specialized industrial processors. However, geopolitical instability and limited technological infrastructure present challenges to further market growth in certain sub-regions. The need for robust and reliable processors capable of operating in extreme climates is a key factor shaping the market dynamics.

Report Scope

This market research report provides a comprehensive analysis of the Industrial Processor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa, including country‑level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market‑entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real‑time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Industrial Processor Market?

-> Industrial Processor Market was valued at USD 15 billion in 2025 and is expected to reach USD 28 billion by 2034, showing a CAGR of 7.2% over the forecast period.

Which key companies operate in Industrial Processor Market?

-> Key players include Intel Corporation, NXP Semiconductors, Texas Instruments Inc., Renesas Electronics Corp., and STMicroelectronics.

What are the key growth drivers?

-> Key growth drivers include intensified investment in automation and Industry 4.0 initiatives, rising demand for edge computing in smart factories, and the need for ruggedized processors that can operate in harsh industrial environments.

Which region dominates the market?

-> The reference material does not specify a single dominant region; it highlights global growth driven by manufacturing hubs worldwide.

What are the emerging trends?

-> Emerging trends include integration of AI/IoT at the edge, development of ultra‑low‑power rugged processors, and increasing adoption of processors that support advanced industrial communication protocols such as Ethernet/IP, CAN bus and PROFINET.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...