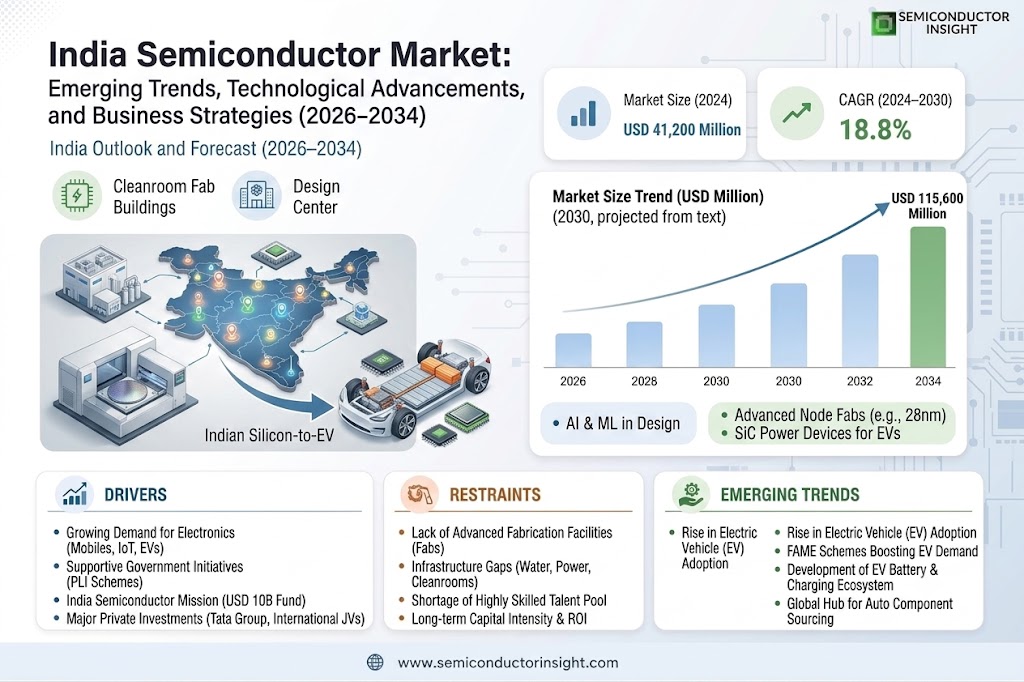

The India Semiconductor Market was valued at US$41,200 million in 2024 and is projected to reach US$115,600 million by 2030, at a CAGR of 18.8% during the forecast period.

Due to government measures to increase domestic manufacturing, technological improvements, and the growing demand for electronic products, the Indian semiconductor market is expected to grow significantly. The need for semiconductors has increased due to India’s growing consumer electronics, automotive, and industrial sectors, making the nation a vital link in the worldwide supply chain. To encourage domestic manufacturing and lessen reliance on imports, especially from East Asia, the government has implemented a number of initiatives, including the Semiconductor Mission and the National Policy on Electronics. Consequently, a number of international semiconductor firms are establishing research and production facilities in India, which is driving the market’s expansion.

In 2017, India’s semiconductor imports totalled US$ 4.65 billion, while its exports totalled US$ 0.21 billion. While imports decreased to US$ 3.15 billion by 2019, exports increased to US$ 0.33 billion. However, due to global economic disturbances like the COVID-19 pandemic, 2020 saw a decline in both imports and exports. Due to pent-up demand following the slump, 2021 saw an extraordinary comeback, with imports totalling US$5.36 billion. India made significant attempts to become a semiconductor hub in 2022, as seen by its exports, which hit a record high of US$0.52 billion.

The market is further bolstered by the growing demand for specialized chips and integrated circuits needed for technologies like 5G, artificial intelligence (AI), the Internet of Things (IoT), and electric vehicles (EVs). Notwithstanding these potential opportunities, obstacles still exist, including inadequate infrastructure, high upfront costs for manufacturing facilities, and reliance on international supply networks for raw materials. However, it is anticipated that the Indian semiconductor business will continue to develop, with local production, innovation, and greater investment all being crucial to its growth.

The Semicon India Programme was initiated by the government in December 2021 with an initial allocation of Rs. 76,000 crore (US$ 9.2 billion) aimed at fuelling the growth of semiconductor and display manufacturing ecosystems in the country.

India increased the funding for the Semicon India Program to Rs. 6,903 crore (US$ 833.7 million) in the interim Union Budget for 2024. A revised expenditure estimate of US $181.5 million (Rs. 1,503 crore) is suggested by the most recent financial information available for the Modified Programme for Development of Semiconductors and Display Manufacturing Ecosystem in India during FY24.

Segmental Analysis

Integrated circuits (ICs) holds the highest market share: By Type

Among product kinds, integrated circuits (ICs) have the largest market share in the Indian semiconductor industry due to their vital significance in a variety of electronic applications. ICs are essential to the operation of computing devices, industrial automation, consumer electronics, automotive electronics, and telecommunications—all of which are rapidly expanding in India. Since ICs offer the processing power, memory, and functionality needed for these applications, demand for them is only expected to grow as India moves closer to implementing technologies like 5G, IoT, and artificial intelligence. Additionally, integrated circuits are very adaptable, encompassing a variety of types such as memory chips, microprocessors, and microcontrollers, each of which is designed to satisfy certain requirements in a variety of industries.

ICs are the most popular type in the Indian semiconductor industry due to their adaptability and crucial function in electronics; they routinely surpass other areas such as optoelectronics, discrete semiconductors, and sensors. Even though these other market categories are expanding as well, particularly in light of developments in fields like automation and automotive electronics, ICs are anticipated to hold onto their dominant market position because of their wide range of applications and the growing digitization of various industries.

Process Technology to hold the highest market share: By Technology

Out of all the technological segments, process technology has the largest market share in the Indian semiconductor industry. Process technology describes the particular tools and techniques needed to build the complex circuitry layers on semiconductor wafers, which affect the final chip’s performance, power efficiency, and transistor density. Process technology is essential to satisfying the needs of applications in the consumer electronics, automotive, telecommunications, and industrial sectors—all of which are expanding quickly in India—because it directly affects chip performance and efficiency.

The demand for increasingly sophisticated devices—such as those that integrate AI, 5G, and IoT—has increased the significance of process technology even more, as producers aim for increased efficiency and miniaturization to improve device capabilities. Therefore, improvements in process nodes—such as going from 14 nm to 7 nm or smaller—remain crucial in this market and attract a lot of attention and investment. Process technology continues to be the mainstay of semiconductor production, holding the largest market share because of its crucial role in determining chip performance and application suitability, even though packaging and fabrication technologies are also crucial because they allow for efficient thermal management and structural integrity for chips.

Competitive Analysis

- HCL Technologies

- Vedanta Ltd

- Tata Electronics

- Wipro

- Micron Technology

- Bharat Electronics Limited (BEL)

- ASM Technologies

- Saankhya Labs

- Continental Device India Pvt. Ltd. (CDIL)

- Dixon Technologies (India) Ltd.

- ISMC Digital

- SPEL Semiconductor

- Other Key Players

Recent development

July 2024: The Japanese analytical and measurement solutions company Horiba, valued at $2.5 billion and a major force in the worldwide semiconductor market, intends to open a facility in India. This facility will serve the nation’s future fabrication (fab) factories, as well as the expanding global market and OSAT (outsourced semiconductor assembly and test) and ATMP (modified assembly, testing, marking, and packaging) businesses.

July, 2024, AMD announced a collaboration with IIT Bombay’s Society for Innovation and Entrepreneurship (SINE). AMD will award funds to IIT Bombay-incubated startups that are working on creating energy-efficient Spiking Neural Network (SNN) chips as a result of this partnership. These startups will be developing novel approaches to reduce the energy usage of conventional neural networks. The first funding to build SNN devices employing ultralow power quantum tunneling on silicon-on-insulator (SOI) technology was given to Numelo Technologies as part of this collaboration.

Industry Dynamics

Industry Driver

Government Initiatives and Policies

In an effort to strengthen its domestic supply chain and lessen reliance on imports, the Indian government has taken proactive measures to promote a self-sufficient semiconductor ecosystem. One of the most important of these programs is the Production Linked Incentive (PLI) Scheme, which offers financial rewards to increase electronics manufacture. In order to assist create a thorough local industry framework, this program is especially important for luring international semiconductor companies to set up manufacturing and research centers in India. Another important program that provides funds and incentives especially for the semiconductor industry is the Semiconductor Mission. In order to improve India’s infrastructure in this area, this mission is intended to assist businesses in establishing semiconductor fabrication factories and design facilities.

Large investments have been made in the Indian semiconductor industry to reflect the country’s increasing significance in the global context. In addition to domestic entities, foreign organizations have established production bases and research centres in various parts of India. For instance, Tata Group unveils ₹27,000 crore semiconductor facility in Assam, promising 15 billion chips annually, in addition to partnerships with the world’s leading companies, PSMC and Renesas Electronics Corporation.

The Indian government has allocated US$ 10 billion towards its Semiconductor Mission to drive investments and propel India towards becoming a leading player in chip manufacturing. Looking ahead, import projections suggest they will surge past US$ 100 billion by 2025, with the aim to reach US$ 80 billion in exports by 2030, hoping that India will secure around 10% of semiconductor production by then.

Industry Trend

Rise in Electric Vehicles (EVs)

The automotive and semiconductor sectors are undergoing significant change as a result of the surge in electric cars (EVs) in India. The Indian EV industry is expected to grow quickly in the upcoming years due to rising customer acceptance, government assistance, and environmental awareness. Important government programs that offer subsidies and incentives to both EV manufacturers and consumers include the Faster Adoption and Manufacturing of Hybrid and Electric Vehicles (FAME) scheme. State governments are also enacting advantageous laws, such as tax exemptions, to encourage the construction of EV infrastructure, such as charging stations and factories that produce batteries. EV adoption is further accelerated by these measures, which are in line with India’s objective of lowering carbon emissions and reducing reliance on fossil fuels.

According to IBEF, The Indian EV market is forecasted to expand from US$ 3.21 billion in 2022 to US$ 113.99 billion by 2029, with a 66.52% CAGR. The Indian EV battery market is projected to surge from US$ 16.77 billion in 2023 to a remarkable US$ 27.70 billion by 2028.

India is emerging as a global hub for auto component sourcing and the industry exports over 25% of its production annually.

Hyundai Motor intends to invest US$ 2.45 billion in Tamil Nadu over the next decade to enhance its electric vehicle initiatives in India. Also, the company is planning to assemble EV battery packs and install 100 charging stations for EVs.

Industry Restraint

Infrastructure and Supply Chain Limitations

The semiconductor industry in India is still in its early stages, and the nation faces significant infrastructure obstacles in its efforts to establish a strong manufacturing base. The main cause of this restriction is the dearth of advanced semiconductor fabrication facilities, or fabs, which are necessary for the manufacturing of chips and integrated circuits. These factories need highly sophisticated infrastructure that are currently unavailable in India, including as cleanrooms, specialized machinery, and incredibly accurate manufacturing techniques. Building semiconductor factories is a very capital-intensive endeavor with lengthy payback periods that requires large investments, frequently billions of dollars, as well as highly qualified workers and state-of-the-art equipment.

Report Scope

The report includes Global & Regional market status and outlook for 2017-2028. Further, the report provides break down details about each region & countries covered in the report. Identifying its sales, sales volume & revenue forecast. With detailed analysis by types, applications, technology, end-users. The report also covers the key players of the industry including Company Profile, Product Specifications, Production Capacity/Sales, Revenue, Price, and Gross Margin 2017-2028 & Sales with a thorough analysis of the market’s competitive landscape and detailed information on vendors and comprehensive details of factors that will challenge the growth of major market vendors.

|

Attributes |

Details |

|

Segments |

By Type

· Integrated Circuits (ICs) · Optoelectronics · Discrete Semiconductors

By Application · Consumer Electronics · Automotive · Industrial · Telecommunications · Computing · Healthcare By Technology · Process Technology · Packaging Technology · Fabrication Technology By End User · Automotive & Transportation · Telecommunications · Consumer Electronics · Industrial Automation & Manufacturing · Healthcare & Medical Devices |

|

Region Covered |

· North America

· Europe · Asia Pacific · Middle East and Africa · South Africa |

|

Key Market Players |

· HCL Technologies

· Vedanta Ltd · Tata Electronics · Wipro · Micron Technology · Bharat Electronics Limited (BEL) · ASM Technologies · Saankhya Labs · Continental Device India Pvt. Ltd. (CDIL) · Dixon Technologies (India) Ltd. · ISMC Digital · SPEL Semiconductor · Other Key Players |

|

Report Coverage |

· Industry Trends

o SWOT Analysis o PESTEL Analysis o Porter’s Five Forces Analysis · Market Competition by Manufacturers · Production by Region · Consumption by Region · Key Companies Profiled · Marketing Channel, Distributors and Customers · Market Dynamics · Production and Supply Forecast · Consumption and Demand Forecast · Research Findings and Conclusion |

Industry Dynamics:

1. Government Support and Strategic Investments

- Major Investments: The India Semiconductor Mission (ISM), initiated in 2021 with a budget of $10 billion, seeks to build a robust domestic semiconductor ecosystem. A standout example is Micron Technology’s $2.75 billion investment in an Assembly, Testing, Marking, and Packaging (ATMP) facility in Gujarat, expected to produce its first chip by late 2024.

- Incentive Programs: Government-backed programs, such as the Production-Linked Incentive (PLI) and Design-Linked Incentive (DLI) schemes, aim to accelerate domestic manufacturing, enhance R&D, and generate jobs within the semiconductor sector. The PLI program particularly supports domestic manufacturing, while the DLI program fosters innovation and design capabilities in India.

2. Market Growth and Demand Drivers

- Projected Growth: Industry forecasts suggest the Indian semiconductor market could achieve a CAGR of 20%, reaching an estimated $55 billion by 2026. This growth is driven by the rising demand for semiconductors in high-tech fields such as artificial intelligence (AI), 5G, and the Internet of Things (IoT), which require sophisticated chip designs and large-scale production capacity.

- End-User Demand: High demand is anticipated across sectors, including automotive, telecommunications, and consumer electronics. This trend is fueled by India’s expanding middle class and rapid digital transformation, requiring a continuous supply of advanced semiconductor technologies.

3. Challenges in Establishing Self-Reliance

- Capital and Resource-Intensive Infrastructure: Establishing semiconductor fabrication plants (fabs) is highly resource-intensive, requiring substantial investments in capital, water, and power. Additionally, environmental considerations present regulatory hurdles, adding complexity to establishing these facilities.

- Skilled Workforce Shortage: The industry faces a shortage of skilled semiconductor engineers. To address this, the government and private companies have launched initiatives to train 250,000 engineers by 2030. Ensuring an adequate talent pool is crucial to supporting future semiconductor R&D and production goals.

4. Supply Chain Resilience and Import Reduction

- Geopolitical and Pandemic-Related Pressures: India’s reliance on imports has exposed vulnerabilities in the supply chain, particularly during the COVID-19 pandemic and amidst geopolitical tensions. Reducing dependence on imports and enhancing supply chain resilience are now strategic priorities for India to secure its semiconductor needs.

5. Future Outlook

- Partnerships and Ecosystem Development: With continued investments and a focus on public-private partnerships, India’s semiconductor industry is on a path to growth and global competitiveness. The focus remains on building a domestic ecosystem to reduce import reliance and create a sustainable, long-term growth trajectory for the country’s semiconductor sector.

Key Indicators Analysed

• Market Players & Competitor Analysis: The report covers the key players of the industry including Company Profile, Product Specifications, Production Capacity/Sales, Revenue, Price and Gross Margin 2019-2030 & Sales with a thorough analysis of the market’s competitive landscape and detailed information on vendors and comprehensive details of factors that will challenge the growth of major market vendors.

• Indian Market Analysis: The report includes Indian market status and outlook 2019-2030. Further the report provides break down details about each region & countries covered in the report. Identifying its sales, sales volume & revenue forecast. With detailed analysis by types and applications.

• Market Trends: Market key trends which include Increased Competition and Continuous Innovations.

• Opportunities and Drivers: Identifying the Growing Demands and New Technology

• Porters Five Force Analysis: The report provides with the state of competition in industry depending on five basic forces: threat of new entrants, bargaining power of suppliers, bargaining power of buyers, threat of substitute products or services, and existing industry rivalry.

Key Benefits of This Market Research:

• Industry drivers, restraints, and opportunities covered in the study

• Neutral perspective on the market performance

• Recent industry trends and developments

• Competitive landscape & strategies of key players

• Potential & niche segments and regions exhibiting promising growth covered

• Historical, current, and projected market size, in terms of value

• In-depth analysis of the Semiconductor Market Market

• Overview of the regional outlook of the Semiconductor Market Market

Key Reasons to Buy this Report:

• Access to date statistics compiled by our researchers. These provide you with historical and forecast data, which is analyzed to tell you why your market is set to change

• This enables you to anticipate market changes to remain ahead of your competitors

• You will be able to copy data from the Excel spreadsheet straight into your marketing plans, business presentations or other strategic documents

• The concise analysis, clear graph, and table format will enable you to pinpoint the information you require quickly

• Provision of market value (USD Billion) data for each segment and sub-segment

• Indicates the region and segment that is expected to witness the fastest growth as well as to dominate the market

• Analysis by geography highlighting the consumption of the product/service in the region as well as indicating the factors that are affecting the market within each region

• Competitive landscape which incorporates the market ranking of the major players, along with new service/product launches, partnerships, business expansions, and acquisitions in the past five years of companies profiled

• Extensive company profiles comprising of company overview, company insights, product benchmarking, and SWOT analysis for the major market players

• The current as well as the future market outlook of the industry concerning recent developments which involve growth opportunities and drivers as well as challenges and restraints of both emerging as well as developed regions

• Includes in-depth analysis of the market from various perspectives through Porter’s five forces analysis

• Provides insight into the market through Value Chain

• Market dynamics scenario, along with growth opportunities of the market in the years to come

• 6-month post-sales analyst support

We offer additional regional and global reports that are similar:

• Global Semiconductor Market Market

• United States Semiconductor Market Market

• Japan Semiconductor Market Market

• Germany Semiconductor Market Market

• South Korea Semiconductor Market Market

• Indonesia Semiconductor Market Market

• Brazil Semiconductor Market Market

Customization of the Report: In case of any queries or customization requirements, please connect with our sales team, who will ensure that your requirements are meet.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...