MARKET INSIGHTS

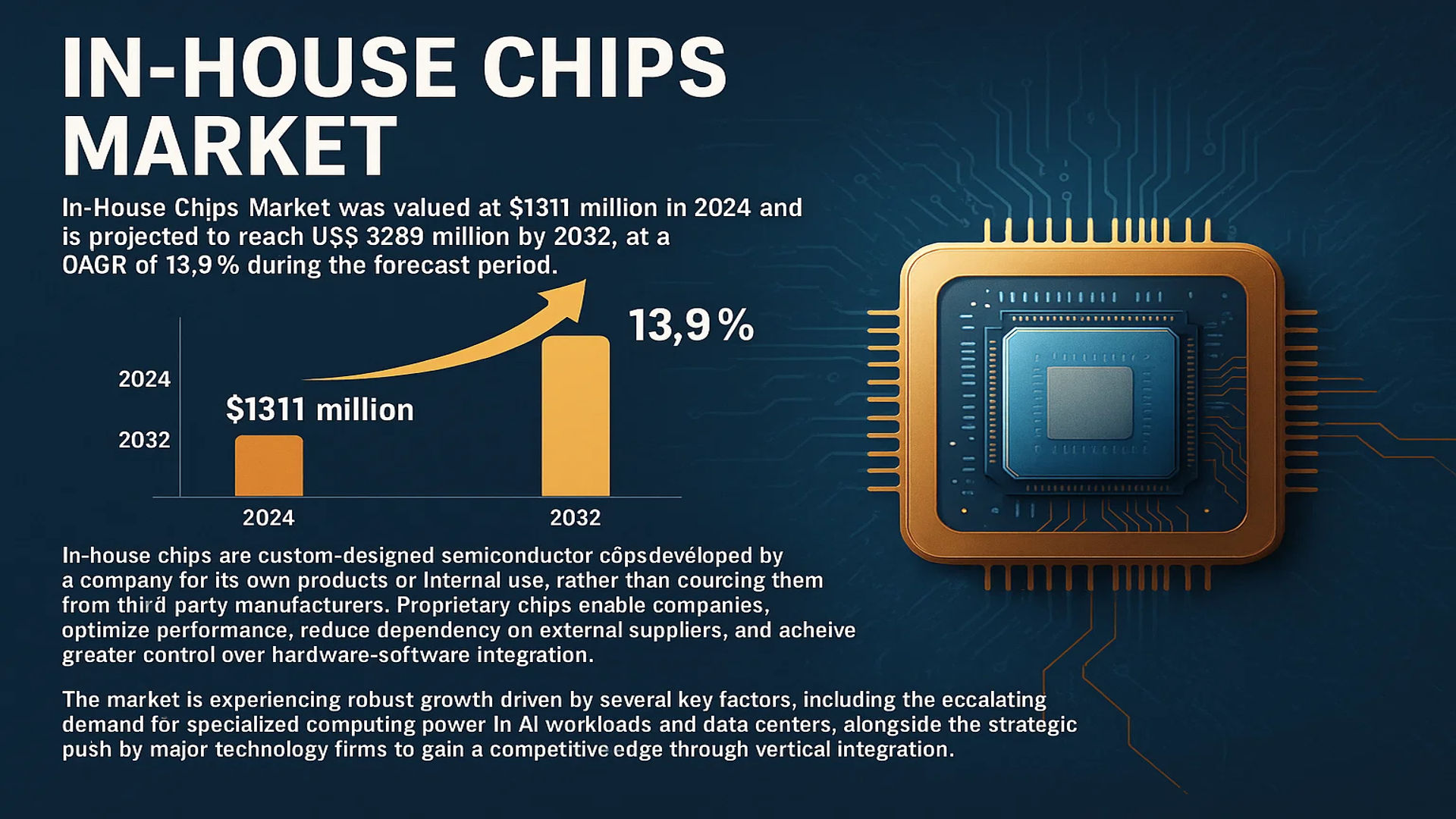

The global In-House Chips Market was valued at 1311 million in 2024 and is projected to reach US$ 3289 million by 2032, at a CAGR of 13.9% during the forecast period.

In-house chips are custom-designed semiconductor chips developed by a company for its own products or internal use, rather than sourcing them from third-party manufacturers. These proprietary chips enable companies to optimize performance, reduce dependency on external suppliers, and achieve greater control over hardware-software integration. They are often tailored for specific high-performance applications, such as artificial intelligence (AI), machine learning, cloud computing, and consumer electronics, allowing for enhanced efficiency and product differentiation.

The market is experiencing robust growth driven by several key factors, including the escalating demand for specialized computing power in AI workloads and data centers, alongside the strategic push by major technology firms to gain a competitive edge through vertical integration. For instance, Apple’s M-series chips for Macs and iPads, Google’s Tensor Processing Units (TPUs) for AI, and Tesla’s Full Self-Driving (FSD) chips for autonomous vehicles exemplify this trend. This movement is further accelerated by the need for improved power efficiency and performance in an increasingly connected world, solidifying in-house chip development as a critical strategic initiative across the technology sector.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for AI and Machine Learning Applications to Accelerate Market Growth

The exponential growth in artificial intelligence and machine learning applications represents a primary catalyst for the in-house chips market. Companies across sectors are developing custom silicon to optimize AI workloads, with the global AI chip market projected to exceed $80 billion by 2025. This surge is driven by the need for specialized processing capabilities that generic chips cannot provide. In-house chips offer superior performance per watt for specific AI algorithms, enabling companies to achieve competitive advantages in areas such as natural language processing, computer vision, and predictive analytics. The increasing complexity of AI models, with some containing over 1 trillion parameters, necessitates custom hardware solutions that can handle massive computational requirements efficiently.

Growing Need for Supply Chain Security and Technological Sovereignty to Boost Market Expansion

Geopolitical tensions and semiconductor supply chain vulnerabilities have accelerated the adoption of in-house chip development strategies. The global semiconductor shortage that began in 2020 exposed critical dependencies on external suppliers, prompting companies to invest in proprietary chip designs to ensure business continuity. This trend is particularly evident in regions seeking technological sovereignty, where governments are implementing policies and funding initiatives to support domestic semiconductor capabilities. Companies are recognizing that controlling their chip design and manufacturing processes provides greater resilience against supply disruptions and geopolitical risks. This strategic shift is driving significant investments in internal semiconductor expertise and infrastructure.

Increasing Focus on Energy Efficiency and Performance Optimization to Drive Market Adoption

The relentless pursuit of energy efficiency and performance optimization is compelling companies to develop custom chips tailored to their specific workloads. In-house chips can achieve up to 40% better power efficiency compared to off-the-shelf solutions, making them particularly valuable for energy-intensive applications such as data centers and mobile devices. This efficiency gain translates to substantial operational cost savings and environmental benefits. Additionally, custom chips enable tighter hardware-software integration, allowing companies to optimize their entire technology stack for maximum performance. The growing emphasis on sustainable computing and reduced carbon footprints further incentivizes organizations to invest in purpose-built semiconductor solutions that minimize energy consumption while delivering superior computational capabilities.

MARKET RESTRAINTS

High Development Costs and Complex Design Processes to Limit Market Penetration

The development of in-house chips involves substantial financial investment and technical complexity that can deter many organizations from pursuing this strategy. Designing a custom semiconductor requires expertise across multiple domains including architecture, verification, physical design, and manufacturing coordination. The initial development costs for a sophisticated chip can range from hundreds of millions to over a billion dollars, creating significant barriers to entry. This financial burden is particularly challenging for small and medium-sized enterprises that lack the resources of technology giants. Furthermore, the lengthy development cycles, often spanning 2-4 years, require sustained investment without immediate returns, making it difficult for companies to justify the expenditure compared to purchasing commercially available solutions.

Manufacturing Constraints and Foundry Capacity Limitations to Hinder Market Growth

Even after successful chip design, companies face significant challenges in manufacturing their custom semiconductors due to global foundry capacity constraints. The semiconductor manufacturing industry is dominated by a few major foundries, creating intense competition for production slots and advanced process nodes. This concentration of manufacturing capability means that companies developing in-house chips must compete with established semiconductor companies for access to production facilities. The current global chip shortage has exacerbated these capacity issues, with lead times for manufacturing extending beyond 12 months in some cases. Additionally, the transition to more advanced process nodes below 7nm requires specialized expertise and equipment that further limits available manufacturing options.

Rapid Technological Obsolescence and Continuous Innovation Requirements to Restrain Market Development

The semiconductor industry’s rapid pace of innovation creates significant challenges for companies developing in-house chips. Technological advancements occur so quickly that a chip designed today may become obsolete within 2-3 years, requiring continuous investment in new designs and manufacturing processes. This constant innovation cycle demands substantial ongoing research and development expenditure to maintain competitiveness. Furthermore, the complexity of modern chip designs continues to increase, with advanced nodes incorporating 3D packaging, heterogeneous integration, and novel materials that require specialized expertise. Companies must maintain large teams of highly skilled engineers across multiple disciplines to keep pace with industry advancements, creating organizational and financial burdens that can outweigh the benefits of vertical integration for many organizations.

MARKET CHALLENGES

Intellectual Property Protection and Patent Landscape Complexities to Challenge Market Participants

Navigating the complex intellectual property landscape presents significant challenges for companies developing in-house chips. The semiconductor industry is characterized by extensive patent portfolios and cross-licensing agreements that can create legal obstacles for new entrants. Companies must conduct thorough IP clearance analyses to avoid infringement claims, which can be time-consuming and costly. Additionally, protecting proprietary chip designs requires robust security measures throughout the design and manufacturing process. The global nature of semiconductor supply chains introduces additional IP protection challenges, as companies must ensure their designs remain secure across multiple jurisdictions with varying intellectual property laws and enforcement mechanisms.

Other Challenges

Talent Acquisition and Retention Difficulties

The global shortage of semiconductor design talent represents a critical challenge for the in-house chips market. The specialized skills required for chip design, including expertise in architecture, verification, physical design, and manufacturing interface, are in high demand but limited supply. Companies face intense competition for qualified engineers, with experienced semiconductor designers commanding premium compensation packages. This talent scarcity is exacerbated by the concentration of semiconductor expertise in specific geographic regions and the lengthy training period required to develop proficiency in chip design methodologies.

Testing and Validation Complexities

Ensuring the reliability and performance of custom chips presents substantial testing and validation challenges. In-house chips must undergo rigorous testing across various environmental conditions, voltage levels, and temperature ranges to guarantee proper functionality. The complexity of modern chips, containing billions of transistors, makes comprehensive testing increasingly difficult and time-consuming. Companies must invest in sophisticated testing infrastructure and develop extensive validation methodologies to identify and address potential design flaws before mass production. This testing phase often reveals issues that require design modifications, creating additional delays and costs in the development process.

MARKET OPPORTUNITIES

Emerging Applications in Edge Computing and IoT Devices to Create New Growth Avenues

The proliferation of edge computing and Internet of Things devices presents substantial opportunities for in-house chip development. These applications require highly specialized processors optimized for low power consumption, specific computational tasks, and cost-effective manufacturing. The edge computing market is projected to grow significantly as organizations seek to process data closer to its source, reducing latency and bandwidth requirements. Custom chips can provide the performance and efficiency needed for these applications while enabling differentiation in competitive markets. Companies developing IoT solutions can leverage in-house chips to create optimized hardware platforms that precisely match their application requirements, leading to improved product performance and reduced total system costs.

Advancements in Chiplet Technology and Heterogeneous Integration to Enable Market Expansion

Recent advancements in chiplet technology and heterogeneous integration methodologies are creating new opportunities for companies to develop in-house chips more efficiently. Chiplet-based designs allow organizations to combine proprietary silicon with commercially available components, reducing development costs and time-to-market. This approach enables companies to focus their design efforts on differentiating elements while leveraging standard components for common functions. The emergence of standardized interfaces and packaging technologies facilitates the integration of multiple chiplets into cohesive systems, making custom chip development more accessible to organizations without extensive semiconductor design expertise. These technological advancements are lowering barriers to entry and enabling more companies to benefit from custom silicon solutions.

Growing Ecosystem of Design Tools and Services to Support Market Development

The expanding ecosystem of semiconductor design tools, intellectual property blocks, and design services is creating new opportunities for companies to enter the in-house chip market. Advanced electronic design automation tools have become more accessible and user-friendly, enabling organizations with limited semiconductor expertise to participate in custom chip development. The availability of proven IP blocks for common functions reduces development risks and accelerates design cycles. Additionally, the growth of design service providers offers companies alternative approaches to developing custom chips without maintaining large internal design teams. This evolving ecosystem is making custom semiconductor solutions more attainable for a broader range of organizations across various industries.

IN-HOUSE CHIPS MARKET TRENDS

Artificial Intelligence and Machine Learning Integration Driving Market Momentum

The proliferation of artificial intelligence and machine learning workloads is fundamentally reshaping the in-house chip market landscape. Companies are increasingly developing custom silicon specifically optimized for AI inference and training tasks, moving away from generic GPU solutions to achieve superior performance and energy efficiency. This trend is particularly evident in data center operations, where custom AI accelerators can deliver performance improvements exceeding 50% compared to off-the-shelf alternatives. The demand for specialized neural processing units (NPUs) and tensor processing units (TPUs) has created a new paradigm in semiconductor design, with major cloud providers and technology firms investing billions annually in proprietary chip development. This strategic shift enables companies to tailor hardware architectures precisely to their software requirements, resulting in significant competitive advantages in processing speed and operational cost reduction.

Other Trends

Vertical Integration and Supply Chain Resilience

The global semiconductor supply chain disruptions have accelerated the adoption of in-house chip development strategies across multiple industries. Companies are pursuing vertical integration to mitigate risks associated with component shortages and geopolitical tensions, particularly in critical sectors such as automotive and consumer electronics. This trend has gained substantial momentum since 2022, with numerous manufacturers establishing dedicated semiconductor design teams and forging strategic partnerships with foundries. The automotive industry exemplifies this shift, where electric vehicle manufacturers are developing proprietary chips for battery management systems and autonomous driving capabilities to ensure supply chain stability and technological differentiation. This movement toward greater control over critical components represents a fundamental restructuring of traditional electronics manufacturing relationships.

Performance Optimization and Energy Efficiency Demands

Increasing computational demands coupled with growing environmental concerns are driving innovation in energy-efficient chip design. The development of in-house chips allows companies to optimize power consumption specifically for their applications, achieving energy savings of 30-40% compared to commercial alternatives. This optimization is particularly crucial for mobile devices and edge computing applications where battery life and thermal management are paramount. Recent advancements in chip architecture, including heterogeneous computing designs and advanced packaging technologies, enable companies to create highly specialized processors that balance performance requirements with power constraints. The trend toward more efficient computing is further amplified by regulatory pressures and corporate sustainability initiatives, making energy efficiency a primary design consideration rather than merely a technical specification.

Specialized Application-Specific Integrated Circuits (ASICs) Proliferation

The market is witnessing exponential growth in application-specific integrated circuits designed for particular use cases beyond traditional computing. Specialized chips for cryptocurrency mining, quantum computing control systems, and advanced sensor processing are emerging as significant market segments. This specialization enables unprecedented performance in niche applications, with custom ASICs often delivering 100x improvements in specific computational tasks compared to general-purpose processors. The healthcare sector particularly demonstrates this trend, with companies developing dedicated chips for medical imaging processing and genomic sequencing that significantly reduce processing times while maintaining accuracy. This movement toward extreme specialization reflects the industry’s recognition that one-size-fits-all solutions are increasingly inadequate for cutting-edge technological applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Technology Giants Drive Innovation Through Vertical Integration

The global competitive landscape for in-house chips is highly dynamic and innovation-driven, dominated by large technology corporations with significant R&D capabilities and vertical integration strategies. Apple Inc. stands as a pioneer and market leader, primarily due to its successful deployment of custom silicon like the A-series and M-series chips across its product ecosystem, achieving remarkable performance and power efficiency gains that differentiate its hardware.

Google and Amazon also command substantial market influence, driven by their development of Tensor Processing Units (TPUs) and Graviton processors, respectively, which are critical for optimizing their cloud infrastructure and AI services. The growth of these companies is heavily attributed to their vast data center requirements and strategic focus on reducing external supply chain dependencies.

Furthermore, these leading players are aggressively expanding their market presence through continuous architectural innovations, strategic talent acquisitions from the semiconductor industry, and multi-billion-dollar investments in fabrication partnerships and proprietary design tools.

Meanwhile, Microsoft and Tesla are rapidly strengthening their positions through significant R&D investments in AI accelerators and autonomous driving chips. Microsoft’s development of its Azure Maia AI chip and Tesla’s Full Self-Driving (FSD) computer exemplify the strategic move towards hardware-software co-design, ensuring tighter integration and performance optimization for their core services and products.

The market also features strong competition from established semiconductor designers like NVIDIA, Qualcomm, and AMD, who are responding to the in-house trend by offering more customizable and application-specific solutions. However, the overarching trend sees end-user companies bringing chip design in-house to capture greater value and control their technology roadmap.

List of Key Companies Profiled in the In-House Chips Market

- Apple Inc. (U.S.)

- Tesla, Inc. (U.S.)

- Google LLC (Alphabet Inc.) (U.S.)

- Amazon.com, Inc. (U.S.)

- Microsoft Corporation (U.S.)

- Intel Corporation (U.S.)

- Qualcomm Incorporated (U.S.)

- NVIDIA Corporation (U.S.)

- Advanced Micro Devices, Inc. (AMD) (U.S.)

- Broadcom Inc. (U.S.)

- Samsung Electronics Co., Ltd. (South Korea)

- Huawei Technologies Co., Ltd. (China)

- Sony Group Corporation (Japan)

Segment Analysis:

By Type

ASICs Segment Leads the Market Due to Superior Performance and Customization for Specific Workloads

The market is segmented based on type into:

- ASICs (Application-Specific Integrated Circuits)

- System on Chip (SoC)

- FPGAs (Field-Programmable Gate Arrays)

- Others

By Application

Consumer Electronics Segment Dominates Owing to High-Volume Integration in Smartphones and Wearables

The market is segmented based on application into:

- Consumer Electronics

- Autonomous Driving

- Cloud & Data Centers

- Internet of Things (IoT)

- Others

By End User

Technology Giants Drive Adoption to Achieve Vertical Integration and Product Differentiation

The market is segmented based on end user into:

- Technology Companies

- Automotive OEMs

- Cloud Service Providers

- Telecommunication Companies

- Others

Regional Analysis: In-House Chips Market

North America

North America, particularly the United States, is the undisputed leader in the global in-house chips market, driven by a concentration of the world’s most influential technology companies. The region’s dominance stems from massive R&D investments, estimated to exceed $100 billion annually in semiconductor design, and a mature ecosystem of fabless design houses and advanced foundries. Companies like Apple (with its M-series chips), Google (Tensor TPUs), Amazon (Graviton and Inferentia), Tesla (Dojo and FSD), and Microsoft are aggressively developing proprietary silicon to optimize performance, enhance security, and reduce supply chain dependencies. This trend is further accelerated by government initiatives like the CHIPS and Science Act, which allocates over $52 billion to bolster domestic semiconductor research, development, and manufacturing. The primary focus areas are high-performance computing, artificial intelligence, data centers, and next-generation consumer electronics, with a strong emphasis on achieving technological sovereignty.

Asia-Pacific

The Asia-Pacific region represents the fastest-growing and most volume-intensive market for in-house chips, fueled by its massive electronics manufacturing base and rapid technological adoption. China is a pivotal force, with companies like Huawei (HiSilicon Kirin and Ascend chips), Alibaba (Pingtouge), and Baidu (Kunlun) leading a national charge toward semiconductor self-sufficiency amidst ongoing geopolitical tensions and trade restrictions. This has spurred significant investment in domestic design capabilities. Meanwhile, South Korea’s Samsung and LG, along with Taiwan’s MediaTek, are powerhouse competitors, developing advanced in-house solutions for everything from smartphones and displays to automotive systems. While the region benefits from a vast talent pool and government support, it faces challenges related to access to the latest fabrication technologies and advanced EDA tools, prompting a strategic shift toward mature nodes and specialized chips for AIoT and mobile applications.

Europe

Europe is steadily emerging as a significant player in the in-house chips market, characterized by a strong focus on automotive, industrial, and research applications. The region’s strategy is heavily influenced by the European Chips Act, which aims to mobilize over €43 billion in public and private investments to double its global market share to 20% by 2030. Automotive giants, particularly in Germany, are at the forefront, developing custom chips for autonomous driving, electric vehicle powertrains, and advanced driver-assistance systems (ADAS) to secure their supply chains and differentiate their products. Companies like Arm Holdings, though a design IP provider, are central to this ecosystem. Furthermore, significant research initiatives, such as those supported by IMEC in Belgium, are fostering innovation in areas like neuromorphic computing and FD-SOI technology. The European approach is highly collaborative, often involving consortia of automotive OEMs, Tier-1 suppliers, and research institutions to pool resources and mitigate risk.

South America

The in-house chips market in South America is in a nascent stage of development, with limited local design activity. The region’s market is primarily driven by the import and integration of finished semiconductor products from global leaders for consumer electronics and industrial automation. Brazil and Argentina have nascent tech sectors, but economic volatility, limited access to capital for high-risk R&D projects, and a lack of a robust semiconductor infrastructure hinder the development of significant in-house chip design capabilities. However, the market shows potential for long-term growth as digital transformation accelerates across industries like agriculture technology (AgriTech) and fintech. Currently, growth is more likely to be seen in the adoption and application of chips designed elsewhere rather than in indigenous development, with multinational corporations serving the region’s needs from their global design centers.

Middle East & Africa

The in-house chips market in the Middle East and Africa is predominantly emerging, with activity concentrated in a few Gulf nations making strategic investments to diversify their economies away from oil. The UAE and Saudi Arabia, through initiatives like the UAE’s “Operation 300bn” industrial strategy, are investing in building a technology and semiconductor knowledge base. Israel stands as a notable exception, with a globally recognized semiconductor design industry; it is a world leader in cybersecurity chips, imaging sensors, and automotive semiconductor design, hosting design centers for many major multinational companies. For the broader region, the immediate focus is on building foundational digital infrastructure and fostering a tech-literate workforce. While large-scale in-house chip development by local companies is not yet widespread, the region is becoming an important consumer of specialized semiconductors for smart city projects, telecommunications, and energy management systems.

Report Scope

This market research report provides a comprehensive analysis of the global In-House Chips market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global In-House Chips Market?

-> In-House Chips Market was valued at 1311 million in 2024 and is projected to reach US$ 3289 million by 2032, at a CAGR of 13.9% during the forecast period.

Which key companies operate in Global In-House Chips Market?

-> Key players include Apple, Tesla, Google, Amazon, Microsoft, Intel, Qualcomm, NVIDIA, AMD, Broadcom, Micron, Cisco, Arm Holdings, Sony, Samsung, LG, MediaTek, Huawei, Baidu, and Alibaba, among others.

What are the key growth drivers?

-> Key growth drivers include demand for AI/ML acceleration, performance optimization, supply chain control, and hardware-software integration advantages.

Which region dominates the market?

-> North America is the dominant market, while Asia-Pacific is the fastest-growing region.

What are the emerging trends?

-> Emerging trends include AI-specific chip design, advanced packaging technologies, RISC-V architecture adoption, and sustainable semiconductor manufacturing.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...