MARKET INSIGHTS

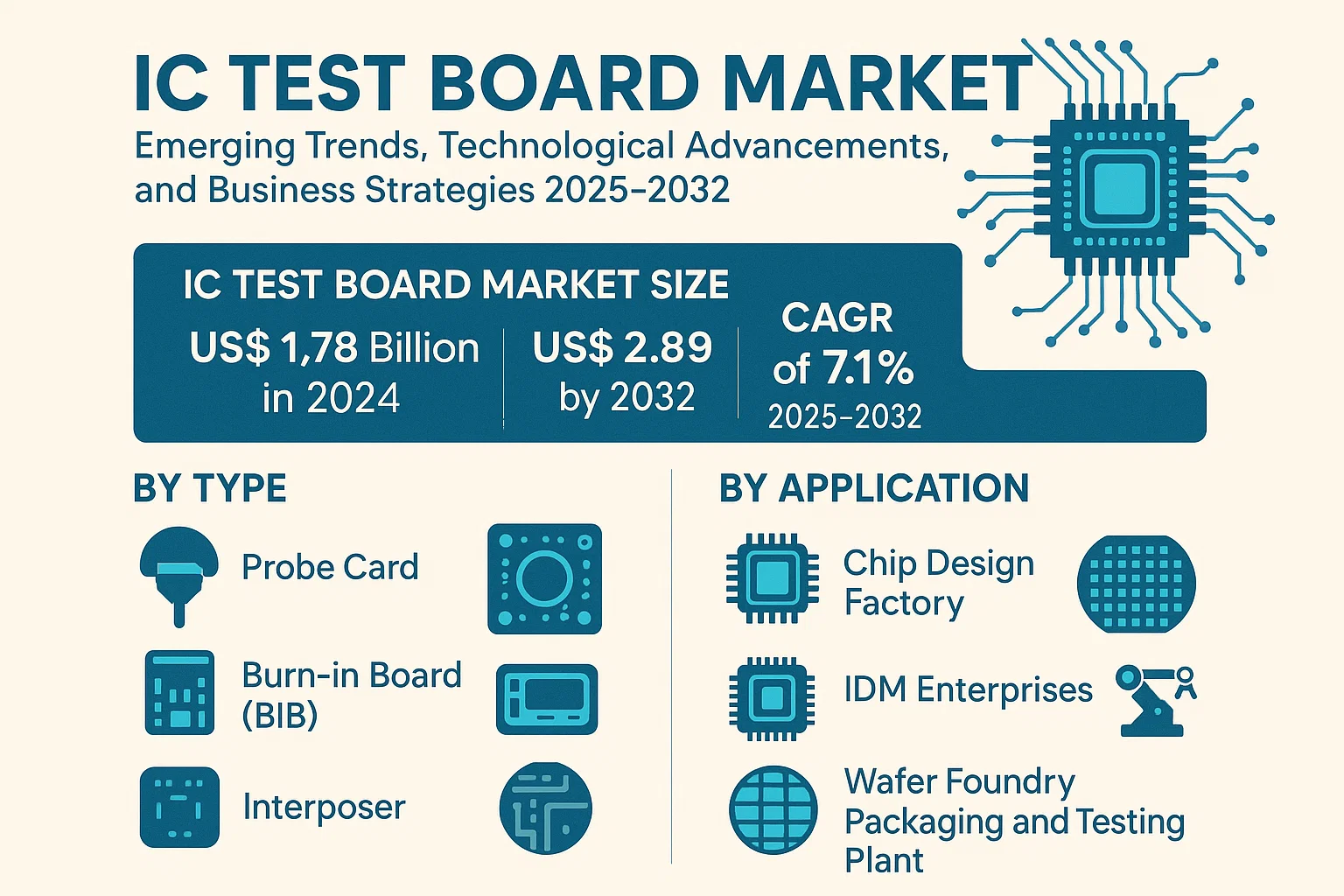

The global IC Test Board Market size was valued at US$ 1.78 billion in 2024 and is projected to reach US$ 2.89 billion by 2032, at a CAGR of 7.1% during the forecast period 2025-2032.

IC Test Boards (also known as probe cards or load boards) are specialized printed circuit boards used for testing integrated circuits during semiconductor manufacturing. These critical components facilitate electrical connections between test equipment and semiconductor devices, enabling quality verification at wafer-level testing, final test, and burn-in stages. Key product types include probe cards (holding 42% market share in 2024), load boards, burn-in boards (BIB), and interposers.

Market growth is driven by increasing semiconductor complexity and miniaturization, with 5G, AI, and IoT applications demanding advanced testing solutions. The U.S. accounted for 32% of global revenue in 2024, while China’s market is growing at 9.1% CAGR through 2032. Major players like Advantest and Cohu are expanding their test board portfolios through strategic acquisitions and R&D investments to address emerging testing challenges in 3D IC packaging and heterogeneous integration.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of Advanced Semiconductor Testing Requirements to Drive IC Test Board Demand

The global semiconductor industry’s shift toward smaller node technologies below 7nm is creating unprecedented demand for sophisticated IC test solutions. As chip complexities increase with advanced packaging technologies like 3D IC and chiplets, the need for corresponding test boards with higher pin counts and finer pitch capabilities grows exponentially. Recent technological leaps now require test boards capable of handling signals above 10GHz, driving innovation across the supply chain. Market intelligence suggests that test board revenue for AI accelerator chips alone grew by over 35% year-over-year in 2023, reflecting this critical market need.

Automotive Semiconductor Boom Fuels Specialized Test Board Development

Automotive electrification and autonomous driving technologies are creating qualitatively different testing requirements that benefit IC test board manufacturers. The automotive semiconductor market, projected to maintain 12% CAGR through 2030, demands test boards capable of extreme temperature cycling (-40°C to 175°C) and extended operational lifetimes. This has led to innovations in materials like polyimide-based substrates and advanced contact technologies. Major IDMs and test houses are investing heavily in automotive-grade test solutions, with dedicated automotive test board capacity expanding by approximately 25% annually across leading manufacturers.

MARKET RESTRAINTS

Extreme Technical Demands and Supply Chain Complexities Constrain Market Expansion

While the IC test board market shows strong growth potential, technical barriers in high-frequency signal integrity and thermal management create significant development bottlenecks. Advanced test boards for 5G and high-performance computing applications now require impedance control within ±5% across the entire board, necessitating specialized materials and ultra-precise manufacturing processes. This technological hurdle has led to yield challenges, with industry averages for complex multilayer boards sometimes falling below 70% in initial production runs. Such technical constraints directly impact time-to-market for cutting-edge semiconductor devices.

Talent Shortage and IP Protection Issues Hinder Innovation Pace

The specialized nature of test board design has created a critical skills gap in the industry. With RF engineering, materials science, and thermal simulation expertise all required, qualified designers command premium compensation, driving up development costs. Concurrently, the industry faces growing intellectual property protection challenges, as reverse engineering of proprietary test interface designs has become increasingly sophisticated. These factors combine to create significant barriers to entry for new market participants while constraining expansion for established players.

MARKET OPPORTUNITIES

Emerging Advanced Packaging Architectures Create New Testing Paradigms

The rapid adoption of heterogeneous integration technologies presents transformative opportunities for IC test board providers. Emerging 2.5D and 3D packaging solutions require completely new test methodologies, driving demand for specialized probe cards and interposers capable of wafer-level testing. Market analysis indicates that advanced packaging test solutions could represent over 30% of total test board revenue by 2026, up from just 15% in 2022. This shift is prompting strategic partnerships between packaging houses and test board manufacturers to co-develop next-generation solutions.

AI-Driven Test Optimization Opens New Value Creation Paths

The integration of machine learning algorithms into test processes is creating adjacent opportunities for intelligent test boards. These next-generation solutions incorporate embedded sensors and adaptive testing capabilities that can reduce test time by up to 40% for complex devices. Forward-thinking manufacturers are now developing active test boards with onboard processing to perform real-time data analysis, opening new revenue streams in test optimization services. This technological evolution is particularly impactful in memory and processor testing, where test time reduction directly correlates to significant cost savings.

MARKET CHALLENGES

Cost Pressures and Margin Erosion Threaten Industry Sustainability

The IC test board sector faces intensifying pricing pressures as semiconductor companies push for lower test costs per device. While test complexity increases exponentially with each new device generation, average selling prices have remained relatively flat, compressing margins throughout the value chain. This dynamic has led to consolidation in the market, with several mid-sized test board specialists being acquired by larger players seeking economies of scale. The challenge is particularly acute for probe card manufacturers, where advanced MEMS solutions require capital investments exceeding $50 million for new production lines.

Geopolitical Tensions Disrupt Supply Chain Stability

Ongoing trade restrictions and regional manufacturing policies are creating significant supply chain uncertainties for test board components. Critical materials like high-frequency laminates and specialized connectors face allocation challenges as geopolitical tensions reshape global trade patterns. Multiple industry reports confirm lead times for certain test board materials have extended from 8 weeks to over 6 months since 2021. This volatility complicates production planning and inventory management, requiring test board manufacturers to maintain higher safety stocks and diversify their supplier networks, both of which negatively impact working capital efficiency.

IC TEST BOARD MARKET TRENDS

Growing Semiconductor Industry to Drive Demand for IC Test Boards

The semiconductor industry’s rapid expansion is a primary driver for the IC test board market, which is projected to grow at a CAGR of over 5% through 2032. With the increasing complexity of integrated circuits across applications like 5G, AI, and IoT, manufacturers require highly precise test boards to ensure device reliability. The market size is expected to reach US$1.8 billion by 2032, propelled by the need for advanced testing solutions in wafer fabrication and packaging. Technological advancements in probe cards, which account for nearly 40% of the market, are enabling higher throughput testing for next-generation chips.

Other Trends

Miniaturization and High-Frequency Testing Requirements

The trend toward smaller node sizes (<7nm) and high-frequency applications is necessitating sophisticated IC test boards capable of handling complex signal integrity challenges. Leading manufacturers are developing boards with superior impedance control, reaching frequencies beyond 50GHz to accommodate 5G mmWave and automotive radar testing. This technological evolution is particularly crucial for IDM enterprises and foundries that require zero-defect assurance in high-volume production environments.

Automation and Smart Manufacturing Integration

The integration of Industry 4.0 practices is transforming IC test board applications through AI-driven predictive maintenance and automated test workflows. Major players are incorporating intelligent monitoring systems that reduce test time by approximately 15-20% while improving yield rates. This automation trend aligns with the semiconductor industry’s shift toward smart factories, where real-time data analytics from test boards contribute to overall equipment effectiveness improvements. The growing demand from packaging and testing plants, representing over 25% of the market, further underscores this transition toward intelligent testing solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Invest in R&D and Strategic Collaborations to Expand Market Presence

The global IC Test Board market is characterized by a mix of established players and emerging competitors, driving innovation and price competitiveness. Shenzhen Fastprint Circuit Technology Co Ltd and Advantest dominate the market, holding a significant combined share of approximately 30% in 2024. Their leadership stems from extensive product portfolios spanning probe cards, load boards, and burn-in boards, coupled with strong manufacturing capabilities in Asia and North America.

Japanese players like OKI Printed Circuits and Nidec SV TCL maintain a strong foothold, particularly in high-density interconnect (HDI) test boards, which are critical for advanced semiconductor testing. Meanwhile, U.S.-based firms such as Cohu and Intel Corporation leverage their proximity to major chip manufacturers to secure long-term contracts, especially in the automotive and AI semiconductor segments.

Strategic partnerships are reshaping the competitive dynamics. For instance, FormFactor recently acquired a smaller European test board manufacturer to enhance its MEMS probe card offerings, while Chroma ATE expanded its production facilities in Taiwan to meet growing demand from foundries. Such moves reflect the industry’s focus on vertical integration and regional market penetration.

List of Key IC Test Board Manufacturers

- Shenzhen Fastprint Circuit Technology Co Ltd (China)

- Advantest Corporation (Japan)

- Db-design (U.S.)

- OKI Printed Circuits (Japan)

- Cohu, Inc. (U.S.)

- M Specialties (U.S.)

- Nippon Avionics (Japan)

- Intel Corporation (U.S.)

- Chroma ATE (Taiwan)

- R&D Altanova (U.S.)

- FormFactor (U.S.)

- Japan Electronic Materials (JEM) (Japan)

- Nidec SV TCL (Japan)

- FEINMETALL (Germany)

Segment Analysis:

By Type

Probe Card Segment Dominates Due to Increasing Demand for Semiconductor Testing

The IC Test Board market is segmented based on type into:

- Probe Card

- Load Board

- Burn-in Board (BIB)

- Interposer

By Application

Wafer Foundry Application Leads the Market with Rising Semiconductor Production

The market is segmented based on application into:

- Chip Design Factory

- IDM Enterprises

- Wafer Foundry

- Packaging and Testing Plant

- Others

By End User

Semiconductor Manufacturers Hold Largest Share Amid Technological Advancements

The market is segmented by end user into:

- Semiconductor Manufacturers

- Test Solution Providers

- Research Institutions

- Electronic Device Manufacturers

Regional Analysis: IC Test Board Market

North America

The North American IC Test Board market is driven by strong semiconductor demand, particularly in the U.S., where domestic chip production initiatives like the CHIPS Act ($52.7 billion allocated) are accelerating investments in testing infrastructure. Major IDM enterprises and fabless companies require advanced test boards (especially probe cards and load boards) to support cutting-edge nodes below 7nm. However, supply chain disruptions and stringent export controls on semiconductor technologies pose challenges for regional suppliers. The presence of key players like Intel and FormFactor strengthens technological competitiveness, though growing labor costs impact margins.

Europe

Europe’s IC Test Board market benefits from specialized automotive and industrial semiconductor applications, with Germany and France leading demand for high-reliability burn-in boards (BIBs). The EU Chips Act’s €43 billion investment plan is expected to bolster local test infrastructure, particularly for power electronics and MEMS sensors. Nevertheless, the region faces limitations due to its relatively smaller share in global semiconductor manufacturing (below 10%). Collaborations between research institutes and companies like FEINMETALL aim to develop advanced interposers for heterogeneous integration testing.

Asia-Pacific

Dominating over 60% of global IC Test Board consumption, Asia-Pacific thrives on concentrated semiconductor hubs in China, Taiwan, South Korea, and Japan. China’s aggressive fab expansion (29 new projects announced in 2023) drives demand for cost-effective probe cards, while Taiwan’s OSAT leaders require high-volume test solutions. Japan maintains technological leadership in advanced materials for fine-pitch testing. However, geopolitical tensions and export restrictions create supply chain vulnerabilities. Local manufacturers like Fastprint and JEM continue gaining market share by offering rapid turnaround times.

South America

The nascent IC Test Board market in South America primarily serves analog and legacy chip testing needs, with Brazil being the largest importer. Limited local semiconductor production restricts market growth, though increasing electronics manufacturing in Argentina and Chile presents opportunities for entry-level test boards. Economic instability and import dependencies hinder the adoption of advanced testing solutions, forcing most manufacturers to rely on refurbished or lower-spec equipment. Strategic partnerships with Asian suppliers provide cost advantages for regional distributors.

Middle East & Africa

This region represents an emerging opportunity as countries like Saudi Arabia and UAE invest in semiconductor testing facilities as part of economic diversification plans. The demand focuses on maintenance-grade test boards for industrial and telecommunications applications. Israel’s thriving fabless sector creates niche demand for advanced probe technologies. Infrastructure limitations and skills gaps slow adoption, but sovereign wealth fund investments in technology (e.g., Saudi’s $500 million semiconductor initiative) indicate long-term potential. Most test boards are currently sourced through European and Asian distributors.

Report Scope

This market research report provides a comprehensive analysis of the global and regional IC Test Board markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global IC Test Board market was valued at USD 1.2 billion in 2024 and is projected to reach USD 1.8 billion by 2032, growing at a CAGR of 5.3%.

- Segmentation Analysis: Detailed breakdown by product type (Probe Card, Load Board, Burn-in Board, Interposer), technology, application (Chip Design Factory, IDM Enterprises, Wafer Foundry, Packaging and Testing Plant), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America (USD 380 million in 2024), Europe, Asia-Pacific (projected 6.1% CAGR), Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants including Shenzhen Fastprint Circuit Technology Co Ltd, Advantest, Cohu, and Intel Corporation, covering their product offerings, R&D focus (15% average revenue allocation), manufacturing capacity, pricing strategies, and recent M&A activity.

- Technology Trends & Innovation: Assessment of emerging technologies in semiconductor testing, integration of AI for predictive maintenance, advanced probe card designs, and evolving industry standards for 5nm and below process nodes.

- Market Drivers & Restraints: Evaluation of factors driving market growth (40% increase in semiconductor R&D spending since 2020) along with challenges including supply chain constraints for specialty materials and rising test complexity for advanced packaging.

- Stakeholder Analysis: Insights for semiconductor equipment suppliers, foundries, OSAT providers, investors, and policymakers regarding the evolving testing ecosystem and strategic opportunities in heterogeneous integration.

Primary and secondary research methods are employed, including interviews with industry experts from top 10 manufacturers, data from semiconductor industry associations, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global IC Test Board Market?

-> IC Test Board Market size was valued at US$ 1.78 billion in 2024 and is projected to reach US$ 2.89 billion by 2032, at a CAGR of 7.1% during the forecast period 2025-2032.

Which key companies operate in Global IC Test Board Market?

-> Key players include Shenzhen Fastprint Circuit Technology Co Ltd, Advantest, Cohu, Intel Corporation, Chroma ATE, FormFactor, and Japan Electronic Materials (JEM), among others.

What are the key growth drivers?

-> Key growth drivers include increasing semiconductor complexity (45% of ICs now require advanced testing solutions), growth in 5G and AI chips, and rising demand for wafer-level testing.

Which region dominates the market?

-> Asia-Pacific holds 58% market share in 2024, driven by semiconductor manufacturing growth in China, Taiwan, and South Korea.

What are the emerging trends?

-> Emerging trends include AI-driven test optimization, high-density interposers for 3D IC testing, and modular test board designs for multi-site testing.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...