IC Substrates for Memory Market Insights

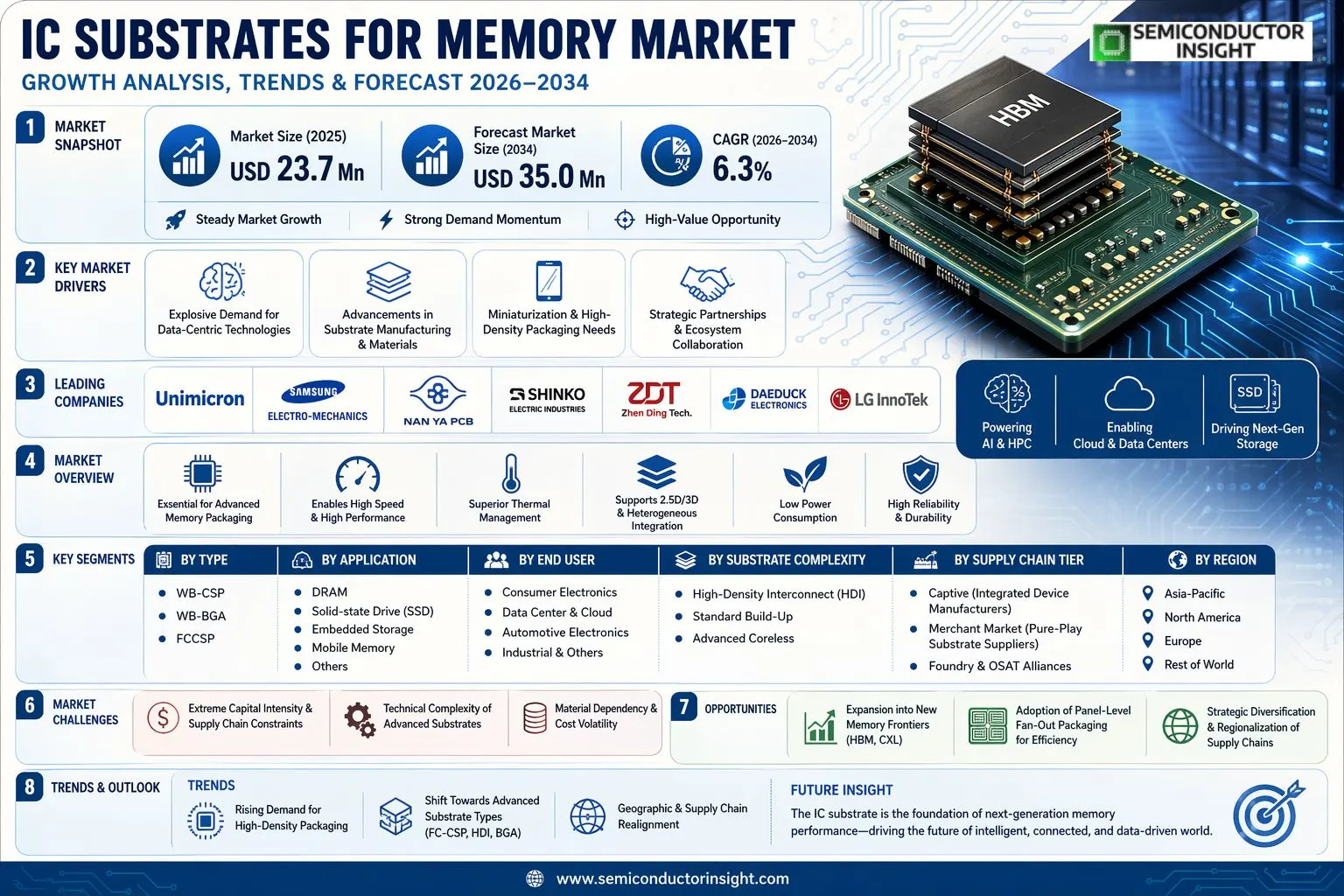

Global IC substrates for memory market size was valued at USD 23.7 million in 2025. The market is projected to grow from USD 25.2 million in 2026 to USD 35 million by 2034, exhibiting a CAGR of 6.3% during the forecast period.

IC substrates, or semiconductor package substrates, are critical components that protect integrated circuit (IC) chips from environmental factors and ensure reliable electrical connections for mounting onto printed wiring boards. This specific segment focuses on memory substrates, which are essential for various memory types including DRAM (volatile memory) and NAND Flash used in solid-state drives, embedded storage, and mobile memory. Key substrate technologies in this market encompass Wire Bond Chip Scale Packages (WB-CSP), Wire Bond Ball Grid Arrays (WB-BGA), and Flip Chip Chip Scale Packages (FCCSP).

The market is experiencing steady growth driven by the relentless demand for higher performance in electronics. This includes the need for high-speed, high-integration, and low-power consumption ICs fueled by advancements in artificial intelligence (AI), cloud computing, and automotive intelligence. Furthermore, the ongoing miniaturization of devices like smartphones and wearables necessitates semiconductor packages that are increasingly high-density, multilayer, and low-profile, directly increasing the complexity and value of advanced IC substrates. The competitive landscape features established players such as Unimicron, Samsung Electro-Mechanics, and Nan Ya PCB, who dominate the supply chain with their technological expertise and manufacturing scale.

MARKET DRIVERS

Explosive Demand for Data-Centric Technologies

The relentless growth of artificial intelligence, high-performance computing, and 5G infrastructure is fundamentally reshaping the memory landscape. These technologies require unprecedented levels of bandwidth and capacity, driving advanced memory solutions like High Bandwidth Memory (HBM) and DDR5. These next-generation memory modules depend on highly sophisticated IC substrates featuring ultra-high density interconnects and fine-line circuitry to manage signals and power efficiently. The performance of the entire memory package is critically dependent on the substrate’s quality, making it a pivotal component in the modern data ecosystem.

Advancements in Substrate Manufacturing and Materials

To keep pace with evolving memory architectures, substrate technology is undergoing rapid innovation. The shift towards panel-level processing and the adoption of advanced materials like Ajinomoto Build-up Film (ABF) are enabling higher yields and greater interconnect density essential for memory packaging. These manufacturing breakthroughs allow for more Input/Output connections in a smaller footprint, directly enabling the compact, high-speed designs required for memory market applications, from servers to edge devices.

➤ The transition to heterogeneous integration and 2.5D/3D packaging is not just an option but a necessity for future memory performance, placing the IC substrate at the heart of this architectural revolution.

Consequently, strategic partnerships between memory manufacturers and substrate suppliers are strengthening, creating a tightly integrated supply chain focused on co-design and innovation to meet the technical specifications of cutting-edge memory products.

MARKET CHALLENGES

Extreme Capital Intensity and Supply Chain Constraints

The fabrication of high-end IC substrates, especially for memory, requires multi-billion-dollar investments in specialized equipment like laser drilling and advanced lithography machines. This creates a high barrier to entry and concentrates production capacity among a few key players, leading to potential bottlenecks. Any disruption in this fragile supply chain can directly impact the availability of critical memory components for the broader electronics industry, creating significant production risks.

Other Challenges

Technical Complexity of Advanced Memory Substrates

Designing and manufacturing substrates for HBM stacks involves managing extreme thermal loads, signal integrity across multiple stacked dies, and minimizing parasitic effects. Achieving this with high yield and reliability is a persistent technical hurdle that requires continuous R&D investment and deep process expertise.

Material Dependency and Cost Volatility

IC substrates for memory market is heavily reliant on specific, high-performance materials like ABF. Fluctuations in the availability and price of these raw materials, coupled with geopolitical factors affecting supply, introduce cost instability and planning uncertainty for substrate manufacturers and their memory clients.

MARKET RESTRAINTS

High Production Costs and Price Sensitivity

The sophisticated technology required for memory-grade substrates results in significantly higher manufacturing costs compared to standard substrates. While premium memory applications can absorb some of this cost, there remains intense price pressure from OEMs, particularly in consumer segments. This cost factor restrains broader, more rapid adoption of the most advanced substrate solutions across all tiers of the memory market, creating a bifurcation between high-performance and cost-sensitive applications.

Cyclical Nature of the Semiconductor Memory Industry

The memory market is notoriously cyclical, experiencing periods of oversupply and price erosion followed by shortages. This volatility makes it challenging for substrate manufacturers to plan long-term capital expenditures and maintain stable profit margins. During downturns, investment in next-generation substrate capacity may be delayed, potentially creating a supply crunch when the next upturn in demand for advanced memory modules arrives.

MARKET OPPORTUNITIES

Expansion into New Memory Frontiers

The evolution of memory-centric computing and novel architectures like Compute Express Link (CXL) opens new avenues for specialized substrate solutions. These interfaces require substrates that can handle exceptionally high data rates and low latency between memory and processors. Companies that can develop and mass-produce substrates optimized for these emerging standards will capture significant value in the next phase of IC substrates for memory market growth.

Adoption of Panel-Level Fan-Out Packaging

Panel-level fan-out packaging represents a major opportunity to increase production efficiency and reduce the cost per unit for advanced memory packaging. This technology allows for the processing of multiple device packages on a large-format panel, improving substrate utilization dramatically. Its successful integration could lower the barrier for employing advanced packaging in a wider range of memory market applications, from enterprise storage to automotive memory systems.

Strategic Diversification and Regionalization

Geopolitical shifts and supply chain resilience concerns are prompting a reevaluation of global manufacturing footprints. This presents a strategic opportunity for substrate manufacturers to establish new production facilities in regions like North America and Europe, supported by government incentives. Diversifying the geographic supply base for these critical components reduces systemic risk and positions firms to serve localized demand for memory substrates more effectively.

IC Substrates for Memory Market Trends

Rising Demand for High-Density Packaging

The primary trend transforming IC substrates for Memory Market is the relentless drive towards higher density and multilayer configurations. This is directly fueled by the demands of next-generation electronics such as AI servers, advanced cloud computing infrastructure, and intelligent automotive systems. As these technologies require memory with higher speed, greater integration, and lower power consumption, semiconductor packages must evolve. Consequently, memory substrates are being engineered for increased I/O counts within shrinking form factors, pushing the evolution of advanced substrate types like FC-CSP and high-density BGA to meet the performance benchmarks for DRAM and NAND flash applications.

Other Trends

Shift Towards Advanced Substrate Types

Within IC substrates for Memory Market, there is a notable product mix evolution. Traditional wire-bond CSP substrates continue to serve cost-sensitive segments, but growth is increasingly concentrated in flip-chip CSP (FC-CSP) and sophisticated BGA solutions. These advanced substrates offer superior electrical performance and thermal management, which are critical for high-bandwidth memory (HBM) stacks and high-performance SSDs. This technological shift necessitates significant R&D investment and manufacturing capability upgrades from key suppliers, influencing the competitive dynamics of the market.

Geographic and Supply Chain Realignment

The manufacturing landscape for IC Substrates for Memory is undergoing strategic realignment, influenced by regional policies and supply chain resilience initiatives. While established manufacturers in Taiwan, South Korea, and Japan maintain a stronghold, capacity expansion is actively occurring in other regions to secure supply. This trend aims to mitigate geographic concentration risks and cater to growing local demand, particularly from memory module and SSD assembly operations. The market’s growth is intrinsically linked to the broader memory semiconductor cycle, with substrate suppliers aligning their capacity plans with the long-term roadmaps of major memory manufacturers.

COMPETITIVE LANDSCAPE

Key Industry Players

A High-Barrier Market Defined by Technological Prowess and Strategic Partnerships

Global IC substrates for memory market is characterized by a consolidated competitive structure dominated by a handful of technologically advanced and highly capitalized manufacturers. Unimicron Technology Corp. of Taiwan is widely regarded as the market leader, holding a significant revenue share, followed closely by Samsung Electro-Mechanics (SEMCO) and Nan Ya PCB Corporation. These top players maintain their positions through continuous R&D investment in high-density interconnect (HDI) and advanced build-up substrate technologies, which are critical for next-generation DRAM and high-bandwidth memory (HBM) modules. The competitive edge is largely determined by the ability to produce ultra-fine line/space substrates and achieve high yields in complex, multilayer FC-CSP and WB-BGA packages, creating substantial barriers to entry for new competitors.

Beyond the top tier, the landscape includes several other significant players specializing in specific niches or geographic markets. Japanese supplier Shinko Electric Industries is a key technology provider, especially for advanced flip-chip packages. Korean manufacturers like Daeduck Electronics and LG InnoTek have strong captive and merchant market positions driven by the country’s memory semiconductor dominance. In China, companies such as Zhen Ding Technology (ZDT), Shennan Circuit, and Shenzhen Fastprint Circuit Tech are rapidly expanding capacity and technological capabilities, supported by national semiconductor self-sufficiency goals, positioning them as formidable challengers in the mid-to-long term.

List of Key IC Substrates for Memory Companies Profiled

- Unimicron Technology Corp.

- Samsung Electro-Mechanics (SEMCO)

- Nan Ya PCB Corporation

- Shinko Electric Industries Co., Ltd.

- Zhen Ding Technology Holding Limited (ZDT)

- Daeduck Electronics Co., Ltd.

- LG InnoTek

- DAISHO DENSHI KOGYO CO., LTD.

- Korea Circuit Co., Ltd.

- Shennan Circuit Company (SCC)

- Shenzhen Fastprint Circuit Tech Co., Ltd.

- Shenzhen Hemei Jingyi Semiconductor Technology Co., Ltd.

- Hong Yuen Electronics

- Huizhou China Eagle Electronic Technology Inc.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

WB-CSP is a dominant packaging solution, driven by its critical balance of performance and miniaturization. Its suitability for high-density interconnections aligns perfectly with the relentless demand for thinner, more powerful memory devices in smartphones and wearables. The architecture supports the essential high-speed signaling required by modern DRAM and NAND Flash, while ongoing material and process innovations continue to enhance its thermal and electrical properties for next-generation memory modules. |

| By Application |

|

Mobile Memory represents a primary growth engine for IC substrate demand, fueled by the pervasive global adoption of smartphones and the expansion into wearable devices. This segment demands substrates that enable extreme miniaturization and low power consumption without compromising data transfer speeds. Concurrently, the Solid-state Drive application is experiencing robust demand due to the datacenter expansion for cloud computing and AI, requiring substrates that support higher storage densities, superior thermal management, and exceptional reliability for enterprise-grade storage solutions. |

| By End User |

|

Consumer Electronics remains the cornerstone end-user segment, with insatiable demand for high-performance memory in devices ranging from flagship smartphones to gaming consoles. The trend towards device intelligentization and feature proliferation directly translates to more complex substrate requirements. The Data Center & Cloud segment is rapidly emerging as a critical high-value market, driven by investments in AI infrastructure and hyperscale computing, which necessitate memory substrates capable of handling immense data workloads with maximum efficiency and reliability. |

| By Substrate Complexity |

|

High-Density Interconnect (HDI) substrates are leading the market’s technological evolution, essential for meeting the requirements of advanced memory packaging. The shift towards finer line widths and micro-vias is critical for enabling the higher I/O counts and miniaturized form factors demanded by cutting-edge memory chips. This complexity is a key differentiator for suppliers, as mastering HDI and Advanced Coreless technologies allows for improved electrical performance and signal integrity, which are paramount for high-speed DRAM and low-latency storage applications in premium market segments. |

| By Supply Chain Tier |

|

Merchant Market (Pure-Play Substrate Suppliers) plays a vital and expanding role, providing specialized manufacturing scale and technological expertise to a broad array of memory chip makers. These suppliers are crucial for absorbing market demand fluctuations and driving innovation in substrate materials and processes. The competitive landscape is characterized by deep technical collaboration, where leading substrate companies work closely with memory manufacturers in Foundry & OSAT Alliances to co-develop tailored solutions that meet specific performance, power, and form-factor challenges for next-generation memory products. |

Regional Analysis: Global IC Substrates for Memory Market

Asia-Pacific

These nations form the technological epicenter, housing the world’s most advanced foundries and memory fabs. Their substrate industries are pioneering next-generation solutions for 3D NAND and HBM stacks, focusing on thermal management and signal integrity to support extreme performance requirements, setting Global benchmark for IC substrates for Memory Market.

Japan’s strength lies upstream, providing critical high-performance substrate materials, specialty resins, and precision manufacturing equipment. Its suppliers are essential for enabling the miniaturization and reliability demanded by advanced memory packaging, making Japan a cornerstone of the regional supply chain for memory IC substrates.

China is rapidly expanding its domestic substrate capabilities, driven by self-sufficiency goals in semiconductors. Meanwhile, Southeast Asia is emerging as a key site for new manufacturing capacity, offering geographic diversification for Global IC Substrates for Memory Market supply chain to mitigate concentration risks.

Proximity between substrate manufacturers, memory chip producers, and OEM assembly plants creates unparalleled supply chain efficiency. This synergy, combined with voracious regional demand for data centers, smartphones, and AI hardware, fuels continuous investment and cements Asia-Pacific’s leadership in the memory IC substrates landscape.

North America

The North America IC Substrates for Memory Market is characterized by high-value design, R&D, and strong demand from end-user industries. The region’s strength is its concentration of leading fabless semiconductor companies, hyperscale data center operators, and AI accelerator firms, which drive specifications for cutting-edge memory solutions. Demand for substrates that support high-performance computing, AI workloads, and advanced server architectures is intense. While substrate manufacturing is limited, the region exerts significant influence through design intellectual property, strategic partnerships with Asia-Pacific manufacturers, and investments in advanced packaging R&D, positioning it as a critical innovation and consumption pillar for Global memory substrates ecosystem.

Europe

Europe holds a specialized position in IC substrates for Memory Market, focusing on automotive, industrial, and high-reliability applications. The region’s substrate requirements are heavily influenced by the rigorous quality and longevity standards of the automotive industry, particularly for memory used in advanced driver-assistance systems and in-vehicle infotainment. European strategies involve developing substrates with enhanced thermal and mechanical robustness for harsh environments. Collaboration between equipment suppliers, material science institutes, and semiconductor firms supports niche innovations, though the region relies on manufacturing imports, making it a key design-in and quality-driven market segment.

South America

South America’s role in IC substrates for Memory Market is evolving, primarily as a growing consumption region rather than a production base. The market is fueled by increasing digitization, expanding data center presence from global providers, and growth in consumer electronics. While local semiconductor manufacturing is nascent, the focus is on developing the electronics assembly and testing ecosystem. Regional dynamics involve navigating import dependencies and building technical expertise to support the regional supply chain for memory modules, with Brazil and Mexico showing the most significant activity in attracting related investments.

Middle East & Africa

The Middle East & Africa region presents a long-term strategic growth avenue for IC substrates for Memory Market, driven by massive investments in digital infrastructure and technology hubs. Gulf nations, in particular, are making concerted efforts to diversify into high-tech sectors, including semiconductor packaging and testing. The primary market driver is the construction of large-scale data centers to support regional cloud adoption and smart city initiatives, creating sustained demand for memory and its foundational substrates. The region’s strategy focuses on forming technology transfer partnerships and establishing special economic zones to cultivate a future-facing electronics ecosystem.

Report Scope

This market research report provides a comprehensive analysis of the IC Substrates for Memory Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of IC Substrates for Memory Market?

-> Global IC Substrates for Memory Market was valued at USD 23.7 million in 2025 and is projected to reach USD 35 million by 2034, at a CAGR of 6.3% during the forecast period.

Which key companies operate in IC Substrates for Memory Market?

-> Key players include Unimicron, Samsung Electro-Mechanics, Nan Ya PCB, Shinko Electric Industries, Zhen Ding Technology, Daeduck Electronics, LG InnoTek, DAISHO DENSHI, Korea Circuit, and Shennan Circuit, among others.

What are the key growth drivers?

-> Key growth drivers include demand for high-speed, high-integration, and low power consumption ICs driven by AI, cloud computing, intelligentization of automobiles, and the miniaturization of electronic devices which require semiconductor packages with higher density, multilayer, and low-profile features.

Which region dominates the market?

-> Asia, particularly China and South Korea, is a key region for the market, with the U.S. also representing a significant market size, while specific regional dominance in revenue share may vary among the leading manufacturing hubs.

What are the emerging trends?

-> Emerging trends include advancements in memory substrates like WB-CSP, WB-BGA, and FCCSP to support next-generation DRAM and NAND Flash applications in solid-state drives, embedded storage, and mobile memory, driven by continuous technological innovation.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...