MARKET INSIGHTS

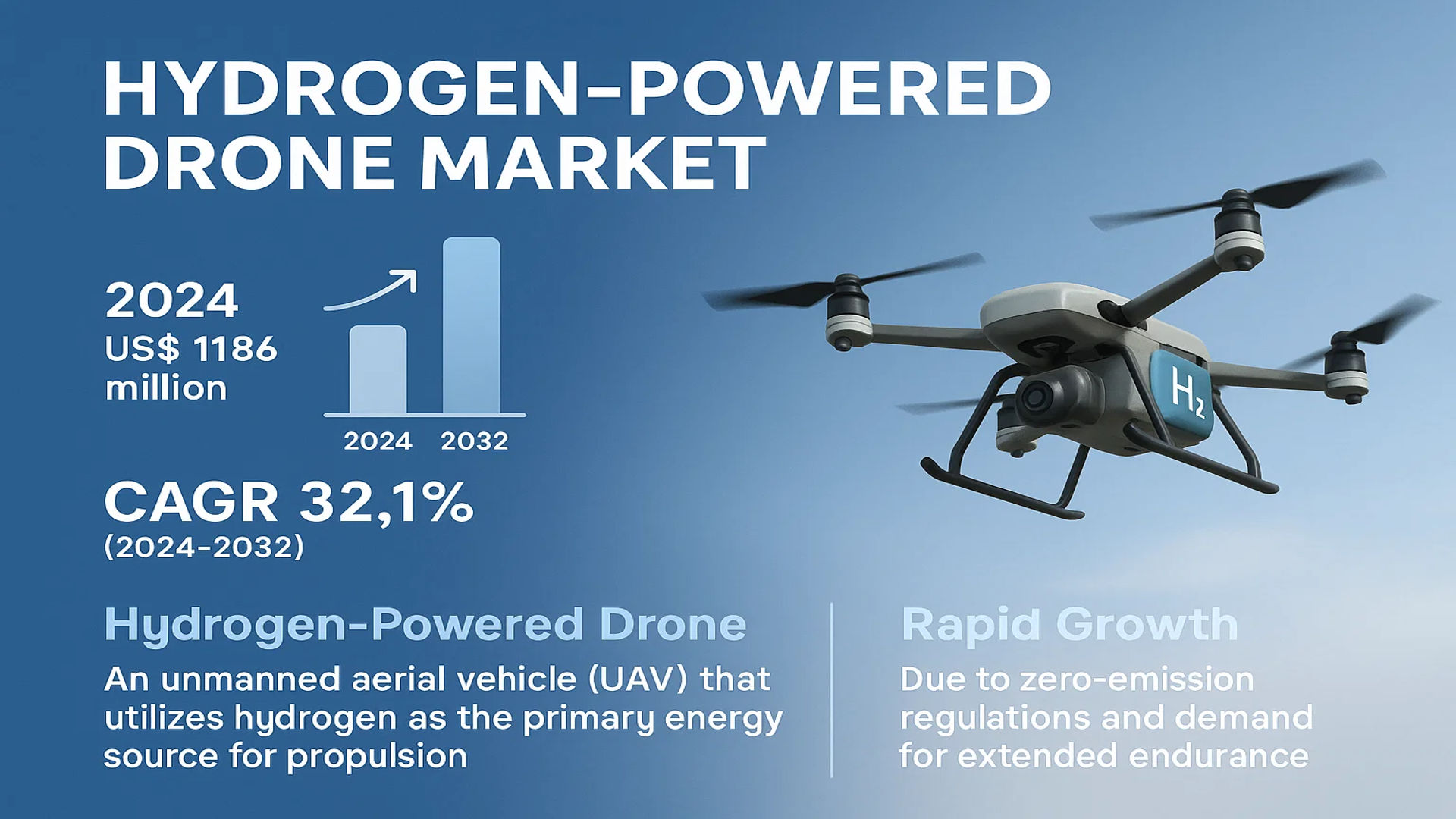

The global Hydrogen-Powered Drone Market was valued at 200 million in 2024 and is projected to reach US$ 1186 million by 2032, at a CAGR of 32.1% during the forecast period.

A hydrogen-powered drone is an unmanned aerial vehicle (UAV) that utilizes hydrogen as its primary energy source for propulsion. Unlike traditional drones that rely on batteries or fossil fuels, these advanced systems employ hydrogen fuel cells or hydrogen combustion engines to generate electricity, which powers the drone’s motors. This technology offers a significant leap in performance, providing substantially longer flight times and greater payload capacities compared to battery-electric counterparts.

The market is experiencing rapid growth due to several factors, including stringent environmental regulations pushing for zero-emission technologies and increasing demand for extended endurance in commercial drone applications. Furthermore, substantial investments in hydrogen infrastructure and fuel cell R&D are accelerating technological maturity and cost reduction. For instance, in 2023, Doosan Mobility Innovation secured significant funding to expand its hydrogen drone production capabilities, highlighting the strong investor confidence in this sector. Key players such as MicroMultiCopter (MMC), Hylium Industries, and Alaka’i Technologies are actively developing and commercializing innovative hydrogen-powered UAV solutions for sectors like infrastructure inspection, emergency logistics, and aerial surveying.

MARKET DYNAMICS

MARKET DRIVERS

Superior Endurance and Payload Capabilities Driving Market Adoption

Hydrogen fuel cells deliver significantly higher energy density compared to lithium-ion batteries, enabling extended flight durations and heavier payload capacities. Hydrogen-powered drones achieve flight times exceeding 3 hours and carry payloads up to 5 kilograms, outperforming battery-powered alternatives which typically offer less than 45 minutes of operation. This technological advantage is critical for applications requiring prolonged aerial presence, such as infrastructure inspection, emergency response, and agricultural monitoring. The energy efficiency of hydrogen systems, converting chemical energy directly to electricity with minimal loss, provides operational cost savings over time despite higher initial investment. Recent advancements in fuel cell durability and cold-weather performance have further enhanced their reliability in diverse environmental conditions.

Global Environmental Regulations Accelerating Clean Technology Adoption

Stringent environmental policies worldwide are accelerating the transition to zero-emission technologies across multiple industries. Hydrogen-powered drones produce only water vapor as exhaust, aligning perfectly with carbon reduction mandates and sustainability initiatives. The European Union’s Green Deal and similar initiatives in North America and Asia are creating regulatory pressure for industries to adopt environmentally friendly alternatives. In the drone sector, this translates to growing preference for hydrogen solutions over conventional combustion engines, particularly in sensitive applications like environmental monitoring and urban logistics. The aviation industry’s commitment to achieving net-zero emissions by 2050 further reinforces the strategic importance of hydrogen technologies.

Expanding Application Scope Across Multiple Industries

The versatility of hydrogen-powered drones is unlocking new applications across numerous sectors. In energy infrastructure, they enable comprehensive inspection of power lines and wind turbines without frequent battery changes. Emergency services utilize their extended flight times for search and rescue operations over large areas. Agricultural applications benefit from prolonged crop monitoring and precision spraying capabilities. Medical logistics represent another growing segment, with hydrogen drones demonstrating potential for long-distance transport of medical supplies and organs. The telecommunications industry is exploring their use for maintaining network coverage during emergencies. This diversification of applications creates multiple revenue streams and reduces market dependency on any single industry.

MARKET CHALLENGES

High Initial Investment and Total Cost of Ownership

The substantial capital expenditure required for hydrogen-powered drone systems presents a significant barrier to widespread adoption. A complete hydrogen drone system, including the aircraft, fuel cells, and hydrogen infrastructure, can cost between 50,000 and 150,000 dollars, compared to 5,000 to 20,000 dollars for equivalent battery-powered systems. This cost differential affects not only initial purchase decisions but also operational budgeting, particularly for small and medium enterprises. The specialized maintenance requirements and need for trained technicians further increase the total cost of ownership. While operational costs may be lower over time, the high upfront investment delays return on investment calculations and limits market penetration to well-funded organizations.

Other Challenges

Hydrogen Infrastructure Limitations

The limited availability of hydrogen refueling infrastructure restricts operational flexibility and geographic coverage. Unlike battery charging stations, hydrogen refueling requires specialized equipment and safety protocols. The current global hydrogen infrastructure primarily serves industrial applications rather than distributed drone operations. This infrastructure gap forces operators to transport hydrogen cylinders or establish their own refueling stations, adding logistical complexity and cost. The situation is particularly challenging in remote areas where drone applications are often most valuable but infrastructure is least developed.

Safety Perceptions and Regulatory Compliance

Safety concerns surrounding hydrogen storage and handling influence market acceptance and regulatory approval. Hydrogen’s high flammability and invisible flame characteristics require stringent safety measures during storage, transportation, and refueling. Regulatory agencies are developing specific guidelines for hydrogen drone operations, but the evolving nature of these regulations creates uncertainty for operators. Insurance premiums for hydrogen drone operations remain higher than for conventional systems due to perceived risks. These factors collectively slow market growth despite the technology’s performance advantages.

MARKET RESTRAINTS

Technical Complexity and Supply Chain Constraints

The sophisticated nature of hydrogen fuel cell technology introduces multiple technical challenges that restrain market growth. Fuel cells require precise control of temperature, humidity, and gas purity to maintain optimal performance and longevity. The sensitivity of these systems to environmental conditions complicates operation in extreme temperatures or high-altitude environments. Additionally, the global supply chain for fuel cell components faces constraints in membrane electrode assemblies, catalysts, and bipolar plates. These supply chain issues affect production scalability and lead times for manufacturers. The technical complexity also extends to system integration, where balancing the fuel cell, hydrogen storage, and power management systems requires specialized engineering expertise.

Limited Hydrogen Production and Green Hydrogen Availability

The environmental benefits of hydrogen-powered drones are contingent upon the production method of hydrogen itself. Currently, approximately 95% of global hydrogen production relies on fossil fuels through steam methane reforming, which generates significant carbon emissions. Green hydrogen production through electrolysis using renewable energy accounts for less than 5% of total production and faces scalability challenges. The limited availability of truly clean hydrogen undermines the environmental value proposition of hydrogen drones. The energy-intensive nature of electrolysis and renewable energy requirements further complicate the economics of green hydrogen production. This situation creates a paradox where the adoption of hydrogen drones might increase carbon emissions unless the hydrogen supply becomes cleaner.

Competition from Advancing Battery Technologies

Rapid advancements in battery technology are narrowing the performance gap between hydrogen and battery-powered drones. Lithium-sulfur and solid-state battery technologies promise energy densities approaching 500 Wh/kg, significantly higher than current lithium-ion batteries. These developments could provide flight durations competitive with hydrogen systems while maintaining simpler operational requirements. Battery technology benefits from massive research investments driven by the automotive and consumer electronics industries, accelerating innovation cycles. The improving recharge speeds and declining costs of advanced batteries make them increasingly attractive alternatives. This competitive pressure forces hydrogen drone manufacturers to continuously improve their cost-performance ratio to maintain market relevance.

MARKET OPPORTUNITIES

Emerging Applications in Long-Range Logistics and Emergency Services

The unique capabilities of hydrogen-powered drones create substantial opportunities in long-distance logistics and emergency response applications. Medical supply delivery to remote areas, disaster response operations, and inter-facility transport of critical items represent growing market segments. The ability to cover distances exceeding 100 kilometers without refueling enables services previously impossible with battery-powered systems. Emergency services increasingly recognize the value of persistent aerial surveillance during natural disasters and search operations. The integration of hydrogen drones into existing logistics networks requires minimal infrastructure adaptation compared to other alternative propulsion systems. These applications demonstrate the technology’s potential to transform service delivery in critical sectors.

Government and Defense Sector Investments Creating New Markets

Increased government funding and defense sector interest are opening new market opportunities for hydrogen-powered drones. National security applications require extended endurance for border surveillance, maritime patrol, and critical infrastructure protection. Defense organizations worldwide are allocating significant budgets to develop and deploy hydrogen drone capabilities. Civil government agencies are exploring their use for environmental monitoring, disaster management, and public safety applications. These institutional customers often have larger budgets and longer investment horizons than commercial entities, providing stable demand for manufacturers. The strategic importance of energy independence and technological leadership further motivates government support for hydrogen aviation technologies.

Technological Convergence with Hydrogen Economy Initiatives

The parallel development of hydrogen infrastructure for transportation and energy storage creates synergistic opportunities for drone applications. Investments in hydrogen refueling stations for fuel cell vehicles can be leveraged to support drone operations with minimal additional investment. The standardization of hydrogen storage and dispensing systems across applications improves economies of scale and reduces costs. Energy companies developing hydrogen hubs and distribution networks represent potential partners for drone service providers. This convergence enables integrated solutions where drones can utilize existing hydrogen supply chains while providing additional revenue streams for infrastructure operators. The holistic development of the hydrogen economy thus multiplies the addressable market for hydrogen drone technologies.

HYDROGEN-POWERED DRONE MARKET TRENDS

Advancements in Fuel Cell Technology to Emerge as a Primary Market Trend

Advancements in hydrogen fuel cell technology are fundamentally reshaping the capabilities and commercial viability of unmanned aerial vehicles. While traditional lithium batteries severely limit flight times, hydrogen fuel cells offer a paradigm shift with their superior energy density. Recent innovations have led to fuel cells that are not only more powerful but also lighter and more durable, directly addressing the core demands of extended flight operations. For instance, the gravimetric energy density of hydrogen fuel cells can exceed 800 Wh/kg, a figure that dwarfs the 200-300 Wh/kg typical of the best lithium polymer batteries available today. This technological leap is enabling flight durations that were previously unimaginable; certain fixed-wing hydrogen-powered drones are now achieving flight times exceeding 6 hours, a more than 300% increase compared to their battery-powered counterparts. Furthermore, the integration of advanced materials for hydrogen storage, such as lightweight composite tanks capable of holding gas at pressures up to 700 bar, is enhancing safety and operational range. These collective improvements in power system efficiency, weight reduction, and storage safety are creating a powerful trend that is accelerating the adoption of hydrogen-powered drones across demanding commercial and industrial applications.

Other Trends

Expansion into Critical Infrastructure and Emergency Services

The market is witnessing a significant expansion into critical infrastructure monitoring and emergency response services, driven by the unique endurance and reliability of hydrogen-powered drones. Sectors such as energy, where inspecting hundreds of kilometers of power lines or pipelines is required, are increasingly adopting this technology because it eliminates the need for frequent landings and battery swaps. In emergency services, the ability to remain airborne for extended periods is invaluable for tasks like search and rescue operations, wildfire monitoring, and disaster assessment. For example, a single hydrogen-powered drone can provide continuous aerial surveillance over a wildfire for hours, delivering real-time data to ground crews, a task that would require multiple rotations of battery-powered units. This trend is further supported by regulatory bodies in various regions beginning to draft specific guidelines for beyond visual line of sight (BVLOS) operations, for which long-endurance drones are a prerequisite. The convergence of proven operational need and evolving regulatory frameworks is creating a robust and growing demand segment.

Strategic Partnerships and Increased Investment in R&D

A notable trend accelerating market maturation is the surge in strategic partnerships between drone manufacturers, fuel cell developers, and end-user industries. Established aerospace corporations are forming alliances with specialized hydrogen technology startups to co-develop integrated solutions, combining expertise in aviation with cutting-edge energy systems. This collaborative approach is crucial for overcoming remaining technical hurdles, such as further reducing system costs and improving cold-weather performance. Concurrently, investment in research and development has reached new heights, with total global funding for hydrogen drone-related technologies estimated to have grown significantly year-over-year. This influx of capital is fueling innovation across the value chain, from more efficient electrolyzers for producing green hydrogen to drones specifically designed around fuel cell architecture rather than adapted from battery models. These concerted efforts in collaboration and investment are not only solving existing challenges but are also paving the way for next-generation applications, ensuring the market’s momentum continues its upward trajectory.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Strive to Strengthen their Product Portfolio to Sustain Competition

The competitive landscape of the global hydrogen-powered drone market is fragmented, characterized by a mix of established aerospace firms, specialized drone manufacturers, and innovative startups pioneering fuel cell integration. While the market is still in its growth phase, Doosan Mobility Innovation has emerged as a prominent player, largely due to its advanced hydrogen fuel cell technology derived from its parent company’s extensive work in the energy sector and its strategic global partnerships, particularly across Asia and North America.

MicroMultiCopter (MMC) and Hylium Industries, INC. also command significant market presence as of 2024. The growth of these companies is attributed to their robust R&D capabilities and successful deployment of drones in critical applications like infrastructure inspection and emergency logistics, which demand the long endurance that hydrogen power provides.

Furthermore, these companies’ aggressive growth initiatives, including geographical expansions into Europe and strategic new product launches featuring enhanced payload capacities, are expected to significantly increase their market share over the forecast period. For instance, several players have recently launched drones capable of flight times exceeding 4 hours, a key competitive advantage.

Meanwhile, companies like Alaka’i Technologies and HevenDrones are strengthening their market positions through substantial investments in R&D, focusing on making hydrogen fuel systems more compact and cost-effective. Their strategic partnerships with hydrogen infrastructure providers and government bodies for pilot projects are crucial for market penetration and ensuring continued growth within the competitive landscape.

List of Key Hydrogen-Powered Drone Companies Profiled

- Doosan Mobility Innovation (South Korea)

- MicroMultiCopter (MMC) (China)

- Hylium Industries, INC. (South Korea)

- Hypower (China)

- Hydrogen Craft Corporation (South Korea)

- Shenzhen Keweitai Enterprise Development CO.,LTD (China)

- H2go Power Ltd (UK)

- Pearl Hydrogen Co.,Ltd. (China)

- Alaka’i Technologies (U.S.)

- HevenDrones (Israel)

- X-Drone (China)

- HyFly (U.S.)

Segment Analysis:

By Type

Fixed-Wing Hydrogen-Powered Drones Segment Dominates the Market Due to Superior Range and Payload Capacity

The market is segmented based on type into:

- Fixed-Wing Hydrogen-Powered Drones

- Multirotor Hydrogen-Powered Drones

By Application

Infrastructure Inspection Segment Leads Due to Critical Need for Long-Endurance Monitoring and Data Collection

The market is segmented based on application into:

- Agriculture

- Infrastructure Inspection

- Aerial Mapping and Surveying

- Medical Logistics and Emergency Transportation

- Others

By End User

Commercial & Industrial Segment Leads Owing to Widespread Adoption Across Multiple High-Value Sectors

The market is segmented based on end user into:

- Commercial & Industrial

- Government & Defense

- Research & Academia

By Power Source

Hydrogen Fuel Cell Segment Dominates as the Primary Technology for Clean and Efficient Energy Conversion

The market is segmented based on power source into:

- Hydrogen Fuel Cell

- Hydrogen Combustion Engine

- Hybrid Systems

Regional Analysis: Hydrogen-Powered Drone Market

Asia-Pacific

Led by China, Japan, and South Korea, the Asia-Pacific region is the dominant market for hydrogen-powered drones, accounting for over 45% of global revenue in 2024. China’s aggressive national hydrogen strategy, including its “Medium- and Long-Term Plan for the Development of the Hydrogen Energy Industry (2021-2035),” has positioned it as the world’s largest market and manufacturing hub. The region benefits from massive government funding, strong industrial policy, and a growing focus on decarbonizing logistics and infrastructure. Japan’s focus on building a “hydrogen society” and South Korea’s investments in fuel cell technology further drive adoption. The region’s vast agricultural lands, extensive power grids, and dense urban environments create strong demand for long-endurance drones in applications like crop monitoring, power line inspection, and emergency logistics.

North America

North America is a key innovation hub, driven by strong R&D investment and growing demand for zero-emission logistics solutions. The United States leads the region, with federal support through the Inflation Reduction Act and Department of Energy funding for hydrogen infrastructure. Companies like Alaka’i Technologies have made notable progress, and the region sees significant adoption in pipeline monitoring, emergency response, and border security applications. However, the market faces challenges related to hydrogen refueling infrastructure and higher initial costs compared to battery drones. Regulatory bodies like the FAA are actively developing frameworks to safely integrate these drones into national airspace, supporting future growth.

Europe

Europe is a major market driven by its strong commitment to decarbonization and green technology. The EU’s Hydrogen Strategy and funding through programs like Horizon Europe support the development and deployment of hydrogen-powered drones. Countries like Germany, France, and the UK are leading in research and pilot projects, particularly in applications such as offshore wind farm inspection, medical logistics, and environmental monitoring. Stringent environmental regulations and carbon reduction targets across the continent create a favorable environment for adoption. However, the market is still emerging commercially, with challenges related to certification standards and hydrogen supply chain maturity.

South America

South America is an emerging market with potential driven by applications in agriculture, mining, and environmental monitoring. Countries like Brazil and Argentina are exploring hydrogen-powered drones for large-scale crop monitoring and pipeline inspection in remote areas. However, the market is still nascent due to limited hydrogen infrastructure, economic volatility, and lower regulatory pressure for zero-emission technologies. While there is growing interest from the agriculture and energy sectors, widespread adoption requires significant investment in hydrogen production and distribution facilities.

Middle East & Africa

The Middle East & Africa region is in the early stages of development, with potential driven by the region’s focus on diversifying its economy and adopting green technology. Countries like Saudi Arabia and the UAE are investing in hydrogen production as part of their economic vision plans, which could support drone adoption in applications like security, oil and gas inspection, and logistics. However, the market faces challenges related to high temperatures affecting fuel cell performance, limited local manufacturing, and underdeveloped hydrogen infrastructure. While there is long-term growth potential, the market is currently limited to pilot projects and specialized applications.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Hydrogen-Powered Drone markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, hydrogen fuel cell advancements, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Hydrogen-Powered Drone Market?

-> Hydrogen-Powered Drone Market was valued at 200 million in 2024 and is projected to reach US$ 1186 million by 2032, at a CAGR of 32.1% during the forecast period.

Which key companies operate in Global Hydrogen-Powered Drone Market?

-> Key players include MicroMultiCopter (MMC), Doosan Mobility Innovation, Hypower, Hydrogen Craft Corporation, Shenzhen Keweitai Enterprise Development CO.,LTD, H2go Power Ltd, Pearl Hydrogen Co.,Ltd., Hylium Industries, INC., Alaka’i Technologies, HevenDrones, X-Drone, and HyFly, among others.

What are the key growth drivers?

-> Key growth drivers include technological innovation in hydrogen fuel cells, policy and regulatory support for clean energy, growing demand for long-endurance drones in various applications, environmental sustainability requirements, and increasing capital market investments.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while North America remains a dominant market due to strong technological infrastructure and regulatory support.

What are the emerging trends?

-> Emerging trends include integration of AI for autonomous operations, development of lightweight hydrogen storage solutions, expansion into medical logistics and emergency transportation applications, and increasing public-private partnerships for hydrogen infrastructure development.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...