MARKET INSIGHTS

The term humanoid robot-specific chip market refers to the entire ecosystem of manufacturers, integrators, and end users that rely on the specialised processors, motor-driver chips, sensor fusion ICs, and safety controllers made especially for human-shaped robots. These devices, in contrast to generic industrial processors, are designed for human-like motion (legs, arms, and grippers), real-time perception, and safe human collaboration in crowded, dangerous environments like chemical reactors, blending lines, and pilot plants.

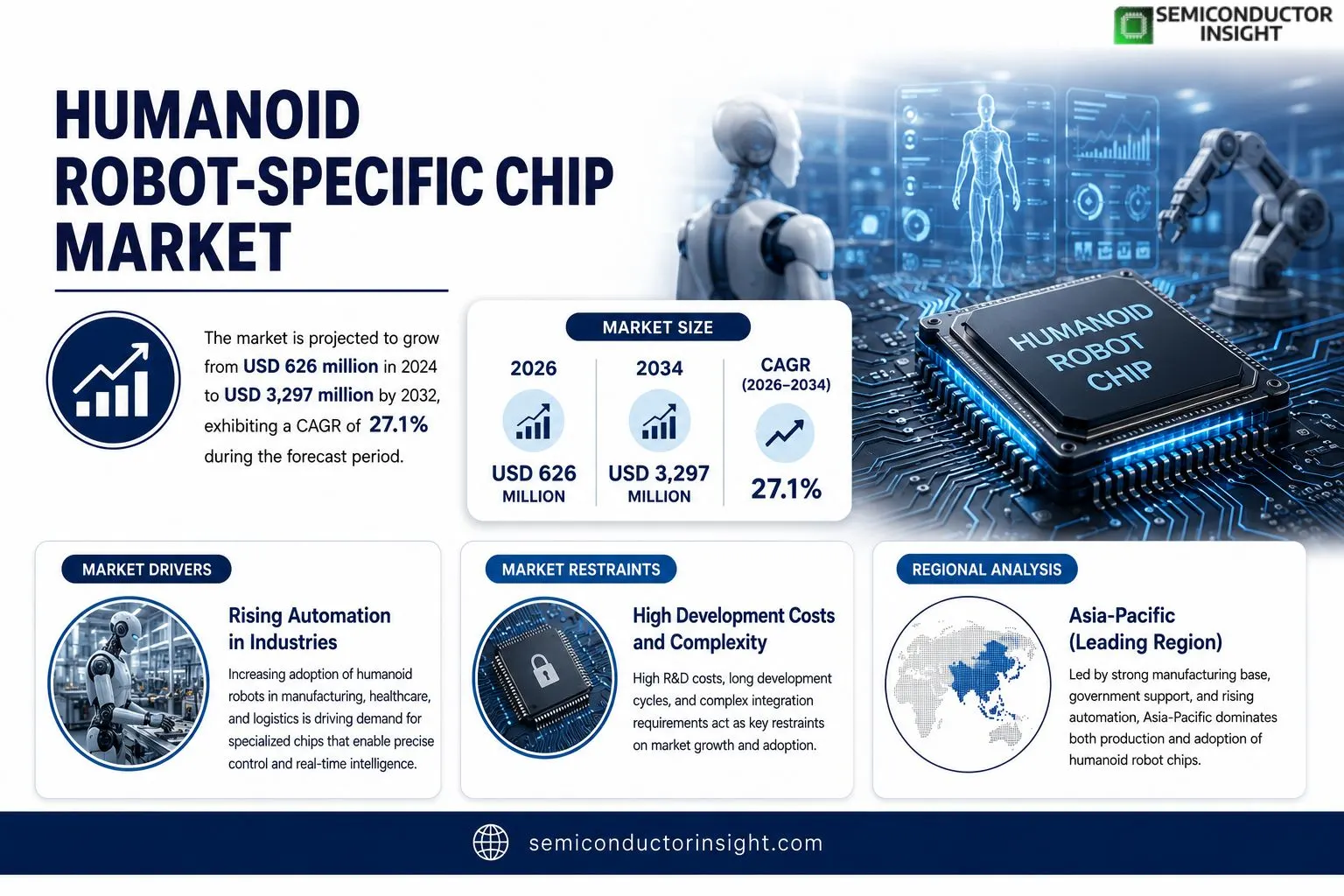

- Global market valuation reached USD 626 million in 2024

- Anticipated to attain USD 3297 million by 2032

- Expanding at an annual growth rate (CAGR) of 27.1%

As each humanoid deployed in a chemical industry might carry 30–80 dedicated chips across joints, vision modules, safety circuits, and communication boards, even a small fleet of 100 robots really generates demand for 3,000-8,000 robot-specific chips within a single organization.

Scaled to a national chemical cluster with 500 mid- to large-scale plants, it can easily surpass 50,000 humanoids and more than 2-4 million specialised chips once acceptance matures.

Key Takeaways:

- Industrial chemical manufacturing leads humanoid chip demand, as plants rely on precise motion and sensing to run reactors, transfer corrosive materials, and automate high‑risk tasks at scale.

- AI and decision‑processing chips are the chemical brain of humanoids, coordinating dosing, sampling, and route planning so robots can work autonomously across complex multi‑step processes and batch records.

- North America and Europe set the pace for high‑end AI and safety‑certified designs, but Asia‑Pacific dominates volume, supplying a growing share of chips embedded in humanoids that work on corrosive, high‑temperature, and explosive chemical processes.

MARKET DYNAMICS

MARKET DRIVERS

Rising Adoption of AI and Machine Learning in Robotics to Accelerate Market Growth

The integration of artificial intelligence and machine learning capabilities into humanoid robots is fundamentally driving demand for specialized chips designed to handle complex computational tasks. These chips enable real-time processing of sensor data, environmental mapping, and autonomous decision-making, which are critical for advanced human-robot interactions. The global AI chip market, which supports these functionalities, is experiencing exponential growth, with projections indicating it could surpass $80 billion by 2027. This expansion directly benefits the humanoid robot-specific chip segment, as manufacturers develop processors capable of delivering the necessary computational power while maintaining energy efficiency. The increasing deployment of humanoid robots in healthcare, retail, and manufacturing applications further amplifies this demand, creating a robust growth trajectory for specialized semiconductor solutions.

Growing Investments in Industrial Automation to Fuel Market Expansion

Industrial automation represents a significant growth driver for the humanoid robot-specific chip market, particularly as manufacturers seek to enhance productivity and address labor shortages. The global industrial automation market is projected to reach approximately $300 billion by 2027, with humanoid robots playing an increasingly important role in complex assembly, quality inspection, and logistics operations. These applications require chips that can process vast amounts of visual and sensory data while coordinating precise motor movements. Recent advancements in chip architecture have enabled processing capabilities that can handle up to 275 trillion operations per second while consuming less than 50 watts of power, making them ideal for continuous industrial operation. This technological progression is creating substantial opportunities for chip manufacturers catering to the industrial robotics segment.

Expansion of Service Robotics in Healthcare and Hospitality to Drive Demand

The service robotics sector is experiencing remarkable growth, particularly in healthcare and hospitality applications, which is generating increased demand for specialized processing chips. The global service robotics market is expected to grow at a compound annual growth rate of over 25% through 2030, with humanoid robots becoming increasingly prevalent in patient care, customer service, and assistance roles. These applications require chips that can support natural language processing, emotional recognition, and sophisticated interaction capabilities while maintaining safety and reliability standards. Recent developments in neural processing units have enabled humanoid robots to process and respond to human emotions with over 90% accuracy, creating new possibilities for empathetic human-robot interactions. This technological advancement is driving substantial investment in specialized chip development for service applications.

MARKET CHALLENGES

High Development Costs and Complex Design Requirements to Challenge Market Penetration

The development of humanoid robot-specific chips faces significant challenges related to extremely high research and development costs and increasingly complex design requirements. Creating chips that can simultaneously handle motion control, environmental perception, and decision processing requires substantial investment in specialized engineering expertise and advanced manufacturing capabilities. The development cycle for such specialized processors typically ranges from 18 to 36 months, with development costs often exceeding $50 million for a single chip design. This financial barrier makes it difficult for new entrants to compete with established semiconductor companies that have existing research infrastructure and manufacturing partnerships. Additionally, the need to maintain compatibility with evolving robotics platforms and software frameworks adds another layer of complexity to chip design and development.

Other Challenges

Thermal Management and Power Consumption Constraints

Managing thermal output and power consumption represents a critical challenge for humanoid robot-specific chips. These processors must deliver high computational performance while operating within strict thermal and power budgets to ensure robot safety and mobility. Achieving computational densities exceeding 10 teraoperations per second per watt requires advanced cooling solutions and power management architectures that add complexity and cost to chip designs. The limitation becomes particularly pronounced in autonomous humanoid robots that rely on battery power, where every watt of power consumption directly impacts operational duration and mobility.

Integration Complexity with Existing Robotics Platforms

The integration of specialized chips with existing robotics platforms presents significant technical challenges. Many humanoid robot manufacturers have established hardware and software ecosystems that may not be compatible with new processor architectures. This creates interoperability issues that can delay adoption and increase implementation costs. The need to maintain backward compatibility while introducing new processing capabilities requires careful balancing of innovation and practicality, often resulting in extended development cycles and increased testing requirements.

MARKET RESTRAINTS

Supply Chain Constraints and Semiconductor Shortages to Limit Market Growth

The humanoid robot-specific chip market faces significant restraints due to ongoing global semiconductor supply chain challenges and manufacturing capacity limitations. The specialized nature of these chips requires access to advanced fabrication facilities that are already operating at near-maximum capacity serving other high-demand sectors such as automotive, consumer electronics, and data centers. The global semiconductor shortage that began in 2020 continues to affect production timelines, with lead times for certain advanced processors extending beyond 52 weeks. This supply constraint is particularly challenging for smaller robotics companies that lack the purchasing volume to secure preferential allocation from foundries. The situation is further complicated by geopolitical factors and trade restrictions that affect the global distribution of semiconductor manufacturing equipment and materials.

Technical Complexity in Achieving Real-Time Processing Capabilities

Developing chips that can deliver true real-time processing capabilities for humanoid robot applications presents substantial technical restraints. The requirement for deterministic response times within microsecond tolerances while processing multiple data streams from various sensors creates significant design challenges. Achieving this level of performance requires sophisticated architecture that can prioritize critical tasks while maintaining overall system responsiveness. The complexity increases when considering the need for fault tolerance and safety certification, as humanoid robots often operate in proximity to humans. These technical requirements necessitate extensive validation and testing procedures that can extend development timelines and increase costs, ultimately restraining market growth during the development and adoption phases.

Regulatory Compliance and Safety Certification Requirements

Stringent regulatory requirements and safety certification processes act as significant restraints on the humanoid robot-specific chip market. Chips designed for humanoid robots must comply with multiple international standards covering functional safety, electromagnetic compatibility, and operational reliability. The certification process for safety-critical applications can take between 12 and 24 months and requires extensive documentation and testing. This regulatory burden is particularly challenging for applications in medical and healthcare robotics, where chips must meet additional requirements for patient safety and data security. The complexity of navigating different regulatory frameworks across various countries and regions adds another layer of difficulty for manufacturers seeking global market access.

MARKET OPPORTUNITIES

Emergence of Advanced Manufacturing Technologies to Create New Opportunities

The development of advanced semiconductor manufacturing technologies presents significant opportunities for the humanoid robot-specific chip market. Recent advancements in 3D chip stacking, advanced packaging techniques, and heterogeneous integration enable the creation of more powerful and efficient processors specifically tailored for robotics applications. These technologies allow manufacturers to combine different types of processing unitssuch as CPUs, GPUs, and NPUson a single chip, optimizing performance for specific robotics tasks. The ability to integrate memory and processing elements in close proximity reduces latency and power consumption while increasing computational density. This technological progression enables the development of chips that can deliver the performance required for advanced humanoid applications while meeting the strict size and power constraints of mobile robotics platforms.

Growing Adoption in Emerging Applications to Drive Future Growth

The expansion of humanoid robots into new application areas creates substantial opportunities for specialized chip manufacturers. Beyond traditional industrial and service applications, humanoid robots are increasingly being deployed in education, research, and space exploration contexts. The educational robotics market alone is projected to grow significantly, with institutions worldwide incorporating humanoid platforms into STEM curricula. Space agencies are developing humanoid robots for extraterrestrial exploration and habitat maintenance, requiring radiation-hardened chips capable of operating in extreme environments. These emerging applications often have unique requirements that drive innovation in chip architecture and functionality, creating specialized market segments with less price sensitivity and greater willingness to adopt cutting-edge technology.

Increasing Collaboration Between Chip Manufacturers and Robotics Companies

Strategic partnerships and collaborations between semiconductor companies and robotics manufacturers present significant growth opportunities for the market. These collaborations enable chip designers to work directly with robotics companies to develop processors specifically optimized for particular platforms and applications. Recent partnerships have resulted in chips that deliver up to 40% better performance per watt for specific robotics tasks compared to general-purpose processors. The trend toward custom silicon solutions allows robotics companies to differentiate their products through optimized performance and unique capabilities. This collaborative approach also facilitates earlier adoption of new chip technologies, as robotics manufacturers gain confidence in the reliability and performance of purpose-built processors through close involvement in the development process.

HUMANOID ROBOT-SPECIFIC CHIP MARKET TRENDS

Advancements in AI and Machine Learning Integration to Emerge as a Dominant Trend

The integration of sophisticated artificial intelligence and machine learning capabilities is fundamentally reshaping the development of humanoid robot-specific chips. These specialized processors are increasingly required to handle complex tasks such as real-time environmental perception, natural language processing, and autonomous decision-making, necessitating architectures that go beyond traditional computing. The demand for chips capable of processing vast sensor data streams with minimal latency has led to the adoption of neuromorphic computing designs and dedicated AI accelerators. This trend is accelerating as humanoids transition from controlled environments to dynamic, real-world applications, where the ability to learn and adapt is paramount. Consequently, chip manufacturers are prioritizing the development of system-on-chip (SoC) solutions that combine high-performance CPU cores with powerful neural processing units (NPUs) and specialized vision processing units (VPUs), all while maintaining stringent power efficiency targets.

Other Trends

Rise of Application-Specific Full-Customized Chips

While general-purpose and semi-customized chips currently hold significant market share, there is a marked and growing shift towards full-customized application-specific integrated circuits (ASICs). This trend is driven by the unique and demanding requirements of different humanoid robot applications. For instance, chips designed for precision tasks in industrial manufacturing require unparalleled real-time control and deterministic response times, whereas those destined for medical or caregiving roles prioritize safety, reliability, and ultra-low power operation. The development of these bespoke silicon solutions allows for optimized performance, reduced physical footprint, and enhanced power efficiency, which are critical for extending operational battery life in autonomous humanoids. This move towards specialization is expected to capture a larger portion of the market’s value as the industry matures and application segments become more defined.

Geopolitical and Supply Chain Factors Influencing Regional Production Hubs

The global landscape for semiconductor production is exerting a profound influence on the humanoid robot-specific chip market, prompting a strategic re-evaluation of supply chain resilience and regional capabilities. While the market remains global in nature, recent geopolitical tensions and trade policies have accelerated investments in establishing and strengthening regional semiconductor ecosystems. This is not about isolation but rather about ensuring a diversified and secure supply of these critical components. Consequently, we are witnessing increased R&D collaboration between leading humanoid robot developers and chip fabricators within specific economic blocs to co-design next-generation processors. This trend supports the overall market growth by mitigating risks and fostering innovation tailored to regional industrial and technological priorities, ensuring that the rapid expansion of the humanoid robotics sector is built on a stable and sustainable foundation.

Recent Devlopments:

- In December 2025, GMO AI & Robotics Trading Co., Ltd., part of the GMO Internet Group and a company driving AI and robotics into society, has acquired all shares of Various Robotics Inc., a developer of advanced robot solutions. This action improves GMO AIR’s position in physical AI and brings together some of Japan’s leading robotics engineers. The acquisition would enable the business to provide more sophisticated robot solutions targeted at addressing societal issues like population decline and labor shortages while producing experiences that make people smile and feel moved.

- In October 2025, Unitree Technology officially released its next-generation bionic humanoid robot, the Unitree H2. Standing 180 cm tall and weighing 70 kg, the Unitree H2’s overall design more closely resembles a real human form, giving it a more lifelike appearance. In the official video, the Unitree H2 is shown wearing clothing, further enhancing its anthropomorphic appearance.

- In August 2025, Living or working with robots that have human-like qualities could not be limited to science fiction. While robotaxis tout the independence made possible by the most recent advancements in vehicle autonomy, collaborative robots may find clever tasks like doing the weekly shop or assembling automobile parts. IDTechEx’s Robotics & Autonomy research reveals some of the emerging industrial applications and uses in the field, such as automobiles and logistics, as well as for both commercial and personal use.

- In August 2025, Nvidia has launched Jetson Thor, a powerful new robotics computer that promises to act as the brain of the next generation of AI-powered robots. The chip, which is currently widely accessible, offers a significant improvement in performance over Jetson Orin, its predecessor, and is intended to run real-time robotic applications that call for quick data processing from several sensors. Nvidia claims that Jetson Thor offers twice the memory of Jetson Orin, 3.1 times better CPU speed, and 7.5 times more AI compute. This could change how robots operate in dynamic surroundings by enabling developers to interpret high-speed sensor input and conduct sophisticated visual reasoning tasks right on the device.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Accelerate Innovation to Capture Market Share in High-Growth Robotics Sector

The competitive landscape of Humanoid Robot-Specific Chip Market is characterized by intense rivalry among established semiconductor giants and agile specialized firms. The market structure is semi-consolidated, with a mix of multinational corporations and emerging technology companies vying for dominance. This dynamic competition is driven by the critical need for chips that deliver unprecedented computational power while maintaining extreme energy efficiency for bipedal locomotion and real-time environmental interaction.

NVIDIA Corporation has established itself as a dominant force in this market segment, primarily due to its advanced GPU architecture that excels at parallel processing required for complex AI algorithms and sensor fusion. The company’s Jetson platform, specifically designed for robotics applications, has become a preferred solution for many humanoid robot developers. NVIDIA’s significant R&D investment, exceeding $8.68 billion in fiscal year 2024, underscores its commitment to maintaining technological leadership in AI and robotics computing.

Intel Corporation and Qualcomm Incorporated also command substantial market presence, leveraging their extensive experience in mobile computing and connectivity solutions. Intel’s focus on neuromorphic computing through its Loihi chips represents a groundbreaking approach to energy-efficient AI processing, while Qualcomm’s robotics platform integrates 5G connectivity with advanced AI capabilities, enabling seamless human-robot interaction and cloud connectivity.

Meanwhile, Chinese technology leaders Baidu, Inc. and Horizon Robotics are rapidly expanding their influence through aggressive investment in AI chip development tailored for the Asian market. Baidu’s Kunlun chips, specifically optimized for its AI ecosystem, and Horizon Robotics’ Journey series, designed for autonomous machines, demonstrate how regional players are developing specialized solutions that address local manufacturing and application requirements.

These companies are pursuing growth through multiple strategic initiatives, including technological partnerships with robotics manufacturers, academic research collaborations, and targeted acquisitions. The recent surge in venture capital funding for humanoid robotics, which reached $2.25 billion in global investments in 2023, has further accelerated innovation and competition in the specialized chip segment.

List of Key Humanoid Robot-Specific Chip Companies Profiled

- NVIDIA Corporation (U.S.)

- Intel Corporation (U.S.)

- Qualcomm Incorporated (U.S.)

- Horizon Robotics (China)

- Baidu, Inc. (China)

- Rockchip Electronics Co., Ltd. (China)

- AMD (Advanced Micro Devices, Inc.) (U.S.)

- Texas Instruments Incorporated (U.S.)

- STMicroelectronics N.V. (Switzerland)

Segment Analysis:

By Type

Full-Customized Chip Segment Leads Due to Unmatched Performance Optimization for Complex Humanoid Tasks

The market is segmented based on type into:

- General-Purpose Chip

- Subtypes: High-performance CPUs, GPUs, and others

- Semi-Customized Chip

- Subtypes: ASICs and FPGAs

- Full-Customized Chip

- Subtypes: SoCs (System on a Chip) and AI-specific processors

By Application

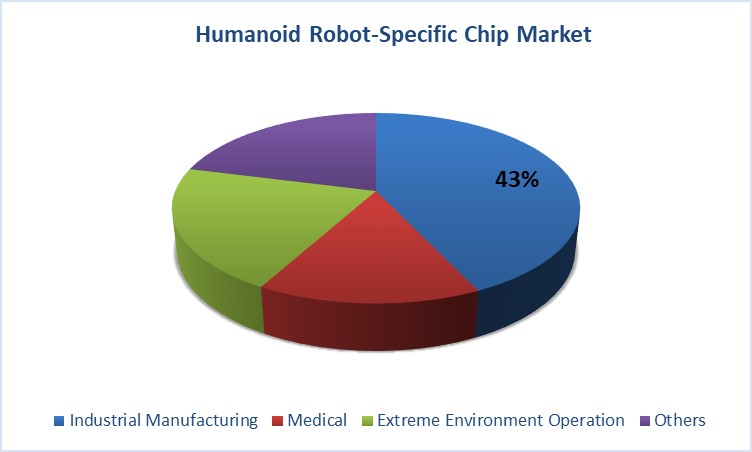

Industrial Manufacturing Segment Dominates Owing to High Demand for Automation and Precision

The market is segmented based on application into:

- Industrial Manufacturing

- Medical

- Extreme Environment Operation

- Others

By Function

AI and Decision Processing Chips Hold Significant Share for Enabling Autonomous Operation

The market is segmented based on primary function into:

- Motion Control Processors

- Environment Perception Chips

- Subtypes: Vision processors and sensor fusion units

- AI and Decision Processing Units

- Power Management ICs

By End User

Automotive and Electronics Industries are Key Adopters Driving Market Growth

The market is segmented based on end user into:

- Automotive

- Electronics

- Healthcare

- Research and Academia

- Others

By End User:

Regional Analysis: Humanoid Robot-Specific Chip Market

Asia-Pacific

The Asia-Pacific region is the undisputed leader in the humanoid robot-specific chip market, driven by immense manufacturing capabilities, aggressive government initiatives, and a robust consumer electronics ecosystem. China, in particular, is a powerhouse, with its “Made in China 2025” policy heavily promoting advanced robotics and domestic semiconductor production. This has fostered the growth of local champions like Horizon Robotics and Baidu, which are developing sophisticated chips tailored for AI and robotic applications. Japan and South Korea contribute significantly through their established expertise in precision engineering and automation, with corporations investing heavily in R&D for next-generation robotics. The region’s dominance is further cemented by its role as the world’s primary manufacturing hub, creating massive, immediate demand for industrial automation solutions powered by these specialized processors. While cost-competitiveness remains a key driver, there is a strong and growing emphasis on developing indigenous, high-performance computing solutions to reduce reliance on foreign technology.

North America

North America is a major hub for innovation and high-end development in the humanoid robot-specific chip sector, largely propelled by its world-leading technology corporations and substantial venture capital investment. The presence of industry titans such as NVIDIA, Intel, and Qualcomm provides a formidable foundation, with these companies leveraging their expertise in GPUs, AI accelerators, and mobile computing to create powerful chipsets for complex humanoid applications. Significant research funding from agencies like DARPA for advanced robotics, particularly for defense and healthcare applications, fuels cutting-edge development. The market’s focus is predominantly on high-performance, full-customized chips that enable advanced cognitive functions, environmental perception, and real-time decision-making. However, the high cost of development and a complex regulatory landscape for AI and robotics can sometimes slow the pace of commercial deployment compared to Asia.

Europe

Europe’s market is characterized by a strong focus on precision, safety, and compliance with stringent regulatory frameworks. The region excels in niche applications, particularly in industrial manufacturing, medical robotics, and collaborative robots (cobots) designed to work alongside humans. European chip designers and robotics firms often prioritize energy efficiency, reliability, and adherence to EU regulations concerning AI ethics and machine safety. Countries like Germany, with its strong industrial base (Industry 4.0), and the UK, with its thriving AI research sector, are key contributors. There is a concerted effort to develop chips that not only deliver high computational power but also guarantee functional safety and data security, making them suitable for sensitive environments like hospitals and highly automated factories. Collaboration between academic institutions and industry players is a notable strength driving innovation in the region.

South America

The humanoid robot-specific chip market in South America is in a nascent stage of development. Growth is primarily driven by the gradual adoption of automation in key sectors such as mining, agriculture, and manufacturing in countries like Brazil and Argentina. The market currently relies heavily on imported technology and general-purpose or semi-customized chips due to budget constraints and a less developed domestic semiconductor industry. Economic volatility often limits large-scale investments in cutting-edge, full-customized chip development. However, the long-term potential is recognized, with increasing awareness of the productivity benefits of robotics. The market’s evolution is expected to be gradual, initially focusing on integrating existing chip solutions into industrial applications before moving towards more specialized, localized development.

Middle East & Africa

This region represents an emerging market with growth potential largely tied to long-term economic diversification plans. Nations like the UAE and Saudi Arabia, through visions such as Saudi Vision 2030, are investing in advanced technologies, including robotics, to move beyond oil-dependent economies. This creates a budding demand for the chips that power these technologies, particularly for service robots in hospitality, healthcare, and public services. Currently, the market is almost entirely dependent on imports from established global players. The lack of a local semiconductor fabrication base and a focus on deploying complete robotic systems rather than developing core components like chips means progress will be incremental. Nonetheless, these strategic investments lay the groundwork for future market development as local technological capabilities mature.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Humanoid Robot-Specific Chip markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Humanoid Robot-Specific Chip Market?

-> Humanoid Robot-Specific Chip Market was valued at 626 million in 2024 and is projected to reach USD 3297 million by 2032, at a CAGR of 27.1% during the forecast period.

Which key companies operate in Global Humanoid Robot-Specific Chip Market?

-> Key players include NVIDIA, Intel, Qualcomm, Horizon Robotics, Baidu, and Rockchip, among others.

What are the key growth drivers?

-> Key growth drivers include advancements in AI and robotics, increasing automation in manufacturing and healthcare, and rising investments in humanoid robot development.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while North America remains a dominant market.

What are the emerging trends?

-> Emerging trends include integration of neuromorphic computing, development of energy-efficient chips, and increased adoption of full-customized chips for specialized applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...