MARKET INSIGHTS

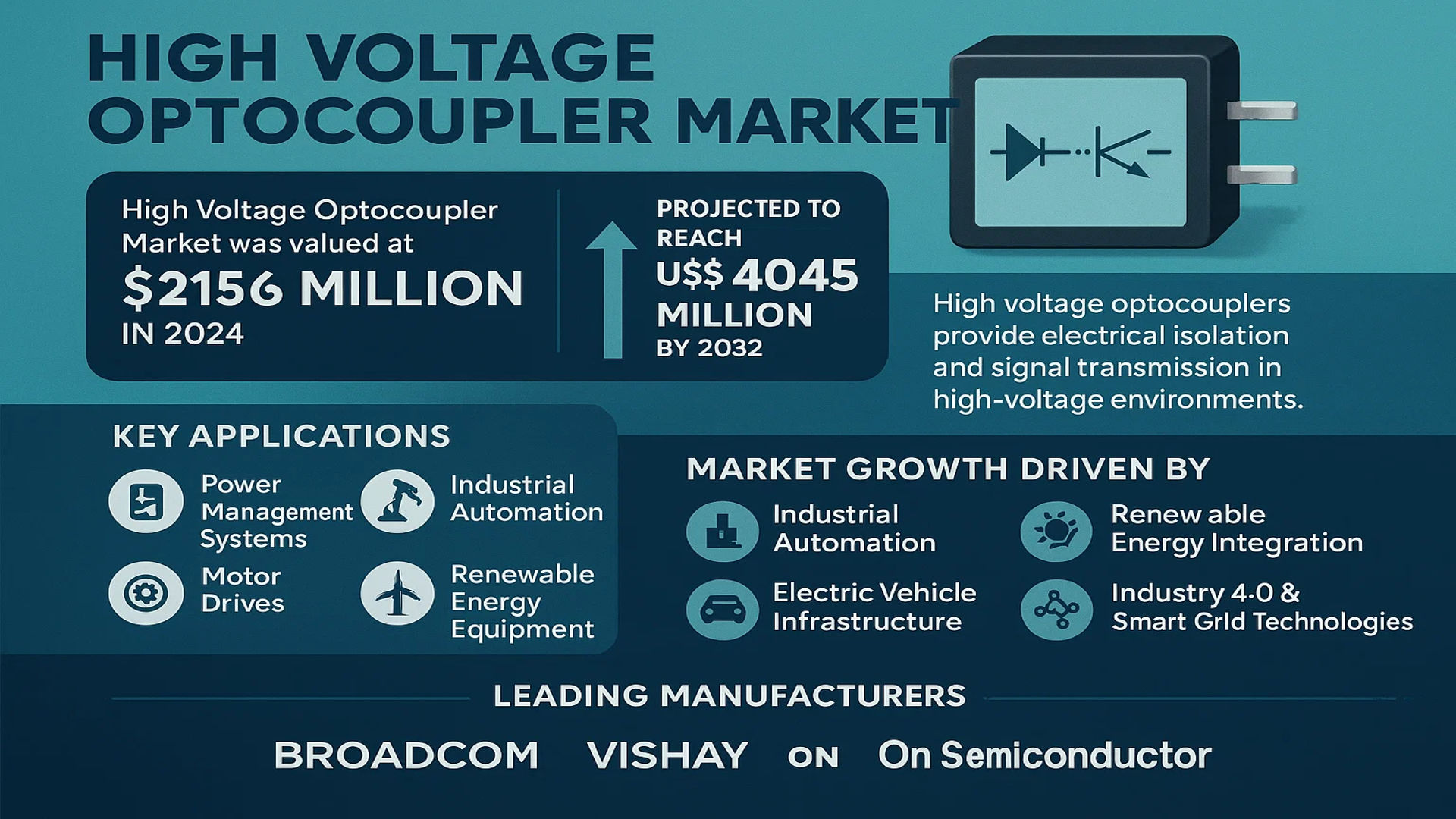

The global High Voltage Optocoupler Market was valued at 2156 million in 2024 and is projected to reach US$ 4045 million by 2032, at a CAGR of 9.6% during the forecast period.

High voltage optocouplers are specialized electronic components designed to provide electrical isolation and signal transmission in high-voltage environments. These devices use photoelectric conversion technology to transmit signals through light between input and output circuits, ensuring robust electrical isolation while maintaining signal integrity. Key applications include power management systems, industrial automation, motor drives, and renewable energy equipment, where they protect sensitive circuits from high-voltage interference.

Market growth is driven by increasing demand for reliable isolation solutions in industrial automation, renewable energy integration, and electric vehicle infrastructure. The shift toward Industry 4.0 and smart grid technologies further accelerates adoption, as these systems require precise signal transmission under high-voltage conditions. Leading manufacturers like Broadcom, Vishay, and On Semiconductor continue to innovate, developing compact, high-efficiency optocouplers to meet evolving industry requirements.

MARKET DYNAMICS

MARKET DRIVERS

Rising Adoption of Industrial Automation Accelerates High Voltage Optocoupler Demand

The global industrial automation market is experiencing rapid expansion, projected to grow at a compound annual rate of nearly 9% through 2030. This surge directly fuels demand for high voltage optocouplers as they are critical components in automation systems, providing essential electrical isolation in motor drives, power supplies, and control circuits. Manufacturers increasingly prioritize reliable isolation solutions to protect sensitive electronics from voltage spikes in harsh industrial environments. For instance, modern automated manufacturing plants now incorporate hundreds of optocouplers across their control systems, with each robotic assembly line typically requiring 40-60 isolation points for safe operation.

Electric Vehicle Revolution Creates New Isolation Requirements

The automotive industry’s accelerated transition to electric vehicles presents significant opportunities for high voltage optocoupler manufacturers. With EV battery systems operating at 400-800V and charger infrastructure reaching 1000V, reliable isolation components become imperative for safety and performance. Current estimates suggest each electric vehicle incorporates 15-30 high voltage optocouplers in battery management systems, onboard chargers, and power distribution units. As global EV production is forecast to exceed 40 million units annually by 2030, this represents a substantial growth vector for isolation component suppliers.

Renewable Energy Expansion Drives Power Electronics Demand

Global investments in renewable energy infrastructure continue breaking records, with solar and wind capacity installations growing over 12% annually. High voltage optocouplers play vital roles in these systems, particularly in solar inverters and wind turbine converters where they provide galvanic isolation between power stages and control circuits. Modern 1500V photovoltaic systems now demand optocouplers capable of withstanding 10-15kV isolation voltages, pushing manufacturers to develop more robust solutions. The renewable sector’s rapid expansion, particularly in Asia-Pacific markets, is creating sustained demand for specialized isolation components.

MARKET RESTRAINTS

Material Shortages and Supply Chain Disruptions Impact Production

The high voltage optocoupler market faces ongoing challenges from semiconductor material shortages and supply chain volatility. Specialized components like gallium arsenide photodiodes and high-grade isolation materials remain in constrained supply, with lead times stretching beyond 40 weeks in some cases. These bottlenecks have forced manufacturers to extend delivery timelines for certain product families by 6-8 months. While capacity expansions are underway, the capital-intensive nature of semiconductor fabrication means supply-demand balance may not stabilize until 2025.

Other Restraints

Technical Limitations in Extreme Environments

Certain industrial and aerospace applications now demand optocouplers capable of operating reliably at temperatures exceeding 150°C or in high-radiation environments. Current generation components often require derating or additional protection in these conditions, limiting their suitability for critical infrastructure projects such as nuclear power plants or deep-space applications.

Price Pressure from Alternative Technologies

Emerging isolation technologies including capacitive and magnetic couplers are gaining traction in medium voltage applications below 5kV. These alternatives offer smaller form factors and lower costs in certain use cases, compelling optocoupler manufacturers to accelerate innovation cycles while maintaining competitive pricing.

MARKET CHALLENGES

Design Complexity Increases with Higher Voltage Requirements

As industrial and energy applications push isolation voltage requirements beyond 15kV, optocoupler manufacturers face escalating design complexities. Achieving reliable performance at these extreme voltages requires innovative packaging solutions and material science breakthroughs, with development cycles for new product families now extending to 24-36 months. The technical challenges are further compounded by the need to maintain competitive pricing while incorporating these advanced technologies.

Regulatory Compliance Adds Development Costs

Increasingly stringent international safety standards for electrical isolation components require substantial certification investments. New optocoupler designs must now comply with multiple regional standards including IEC 60747-5-5, UL 1577, and VDE 0884-11, with compliance testing alone costing $150,000-$300,000 per product family. These regulatory hurdles particularly challenge smaller manufacturers lacking established certification infrastructure.

MARKET OPPORTUNITIES

Medical Equipment Innovations Create New Applications

The global medical equipment market’s shift toward higher voltage imaging systems and portable diagnostic devices presents significant growth opportunities. New generations of CT scanners, proton therapy systems, and surgical robotics require reliable high voltage isolation with ultra-low leakage current. Medical applications now represent the fastest growing segment for high performance optocouplers, with compound annual growth exceeding 14% as healthcare providers worldwide upgrade aging equipment.

Smart Grid Modernization Drives Infrastructure Investments

Utilities globally are investing over $300 billion annually in smart grid upgrades, creating substantial demand for high reliability isolation components. Modern solid-state transformers, fault current limiters, and grid-edge devices all incorporate multiple high voltage optocouplers for control and monitoring functions. As power grids transition to bidirectional power flows and higher distribution voltages, utilities require components with 20+ year lifespans under continuous operation – a key strength of optocoupler technology.

HIGH VOLTAGE OPTOCOUPLER MARKET TRENDS

Rising Demand for Industrial Automation Drives Market Expansion

The global High Voltage Optocoupler market, valued at $2.156 billion in 2024, is witnessing substantial growth driven by the rapid adoption of industrial automation technologies. These components play a critical role in ensuring electrical isolation and signal integrity in high-voltage environments, making them indispensable in modern manufacturing systems. Factories transitioning to Industry 4.0 standards increasingly rely on optocouplers for robust circuit protection against voltage spikes, with the industrial segment accounting for over 40% of total market demand. Their ability to prevent ground loops and suppress electromagnetic interference has become particularly valuable as automation systems grow more complex and interconnected.

Other Trends

Electric Vehicle Revolution Accelerates Adoption

The automotive industry’s shift toward electrification is creating unprecedented opportunities for high voltage optocoupler manufacturers. Modern electric vehicles require multiple isolation solutions for battery management systems, onboard chargers, and traction inverters. With projections indicating over 30 million EVs will be sold annually by 2030, this sector represents one of the fastest-growing application areas. Optocouplers with reinforced insulation ratings above 5kV are becoming standard in power electronics designs, ensuring safe operation while meeting stringent automotive safety standards.

Renewable Energy Infrastructure Fuels Innovation

Expansion of solar and wind power installations globally is pushing the boundaries of high voltage isolation technology. Grid-tied inverters for photovoltaic systems frequently utilize optocouplers with isolation voltages exceeding 10kV to handle the demanding requirements of medium-voltage distributed generation. The renewable energy sector’s compound annual growth rate of 8-10% creates sustained demand for reliable isolation components that can withstand harsh environmental conditions while maintaining signal accuracy. Concurrently, smart grid modernization projects are incorporating digital communication-enabled optocouplers for protective relaying and monitoring applications across transmission networks.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Players Compete Through Innovation and Strategic Expansion in High Voltage Optocouplers Market

The global High Voltage Optocoupler Market exhibits a semi-consolidated competitive landscape, dominated by established semiconductor companies alongside specialized component manufacturers. Broadcom leads the market with an estimated 22% revenue share in 2024, owing to its comprehensive product portfolio spanning single, dual and quad channel optocouplers with voltage ratings up to 10kV. The company’s extensive R&D investments in GaN (Gallium Nitride) based optocoupler technology have strengthened its position in industrial automation applications.

Following closely, Littelfuse and Vishay collectively account for nearly 30% of the market, distinguished by their focus on ruggedized optocouplers for harsh industrial environments. Both companies have recently launched new product lines featuring reinforced isolation barriers exceeding 8kV, responding to growing demand from renewable energy applications. Meanwhile, On Semiconductor is gaining traction through strategic partnerships with Chinese EV manufacturers, supplying optocouplers for battery management systems.

The market has witnessed four major acquisitions since 2022 as companies aim to expand their technological capabilities. Most notably, Skyworks Solutions’ acquisition of ISOCOM in 2023 enhanced its position in aerospace-grade optocouplers. Smaller players like HVM Technology and Resource Group are differentiating through niche applications, particularly in medical high-voltage equipment where precision and reliability are paramount.

Product innovation remains the key battleground, with companies racing to develop optocouplers featuring lower power consumption, higher switching speeds, and improved noise immunity. EVERLIGHT recently introduced an automotive-qualified optocoupler series with AEC-Q100 Grade 1 certification, tapping into the growing electric vehicle market. Similarly, Amptek has focused on miniaturized optocoupler packages for space-constrained industrial control applications.

List of Key High Voltage Optocoupler Companies Profiled

- Broadcom (U.S.)

- PPM Power (UK)

- ISOCOM (UK)

- Voltage Multipliers Inc. (U.S.)

- Skyworks Solutions (U.S.)

- Littelfuse (U.S.)

- On Semiconductor (U.S.)

- Amptek (Germany)

- Vishay (U.S.)

- EVERLIGHT (Taiwan)

- Resource Group (UK)

- HVM Technology (U.S.)

Segment Analysis:

By Type

Quad Channel Optocoupler Segment Leads Due to Higher Isolation Capabilities in Industrial Applications

The market is segmented based on type into:

- Single Channel Optocoupler

- Dual Channel Optocoupler

- Quad Channel Optocoupler

- Others

By Application

Industrial Segment Dominates Market Share Due to Widespread Use in Automation and Power Management

The market is segmented based on application into:

- Industrial

- Aerospace

- Automotive

- Others

By Isolation Voltage

Above 10kV Segment Gains Traction for High Voltage Power Transmission Systems

The market is segmented based on isolation voltage into:

- Below 5kV

- 5-10kV

- Above 10kV

- Others

By End-User Industry

Energy & Power Sector Shows Strong Demand for HV Optocouplers in Smart Grid Applications

The market is segmented based on end-user industry into:

- Energy & Power

- Manufacturing

- Telecommunications

- Healthcare

- Others

Regional Analysis: High Voltage Optocoupler Market

Asia-Pacific

The Asia-Pacific region dominates the global high voltage optocoupler market, accounting for over 40% of total revenue in 2024. This leadership position stems from massive industrialization in China, Japan, and South Korea, coupled with rapid growth in semiconductor manufacturing and renewable energy projects. China’s push toward domestic semiconductor self-sufficiency and India’s escalating automotive electronics production are key drivers. The region also benefits from concentrated manufacturing hubs for consumer electronics and industrial automation systems, where optocouplers provide critical isolation functions. While price competition remains intense among local suppliers, multinational players are establishing regional R&D centers to develop specialized optocoupler solutions for high-growth applications like solar inverters and EV charging systems.

North America

North America represents the second-largest market, with the U.S. contributing approximately 60% of regional demand. Strict safety regulations in power electronics and medical equipment manufacturing necessitate high-reliability isolation solutions. The region’s advanced semiconductor industry and substantial investments in smart grid infrastructure – including the $65 billion grid modernization allocation in the Bipartisan Infrastructure Law – are accelerating optocoupler adoption. Major aerospace and defense contractors increasingly specify MIL-SPEC qualified optocouplers for avionics and radar systems. However, supply chain challenges for specialty optoelectronic components and pressure to reduce system BOM costs pose hurdles for market expansion.

Europe

Europe maintains strong demand for high voltage optocouplers, particularly in industrial automation and renewable energy applications. Germany’s robust manufacturing sector and Italy’s extensive motor drive industry utilize optocouplers extensively for equipment protection. The region’s stringent EN/ IEC safety standards for electrical equipment create sustained demand for certified isolation components. EU initiatives like the Green Deal Industrial Plan are driving investments in power conversion systems that integrate advanced optocouplers. However, the market faces pricing pressures from Asian suppliers and increasing competition from digital isolators in certain applications, requiring continuous innovation from established European component manufacturers.

South America

The South American market is emerging, with Brazil accounting for nearly half of regional demand. Growth stems from expanding industrial automation in mining operations and gradual modernization of power infrastructure. While economic instability sometimes disrupts electronics supply chains, the automotive sector’s recovery post-pandemic has boosted optocoupler usage in vehicle electronics. Local manufacturers primarily source components from global suppliers, though some regional assembly operations are developing. The market potential remains constrained by limited technical expertise in high-reliability applications and reliance on imported electronic components for critical systems.

Middle East & Africa

This region presents growing opportunities, particularly in renewable energy projects and industrial modernization programs in the GCC countries. Saudi Arabia and UAE’s investments in smart city infrastructure and oil & gas automation are creating demand for high voltage isolation solutions. However, the market remains price-sensitive, with preference for cost-competitive Asian imports over premium-grade components. Infrastructure limitations and intermittent power quality issues complicate the adoption of sophisticated electronic systems containing optocouplers. Nevertheless, long-term growth prospects exist as regional industrial diversification policies accelerate.

Report Scope

This market research report provides a comprehensive analysis of the global and regional High Voltage Optocoupler markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global High Voltage Optocoupler market was valued at USD 2156 million in 2024 and is projected to reach USD 4045 million by 2032, at a CAGR of 9.6%.

- Segmentation Analysis: Detailed breakdown by product type (Single Channel, Dual Channel, Quad Channel), application (Aerospace, Industrial, Automotive, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with country-level analysis where relevant. Asia-Pacific dominates the market due to rapid industrialization and expanding electronics manufacturing.

- Competitive Landscape: Profiles of leading market participants including Broadcom, Vishay, ON Semiconductor, and Skyworks Solutions, covering product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent M&A activities.

- Technology Trends & Innovation: Assessment of emerging technologies in optoelectronic components, integration with IoT systems, and advancements in high-voltage isolation techniques.

- Market Drivers & Restraints: Evaluation of factors such as rising demand for industrial automation, growth in renewable energy systems, and increasing safety regulations, along with challenges like supply chain constraints and material costs.

- Stakeholder Analysis: Strategic insights for component manufacturers, OEMs, system integrators, and investors regarding market opportunities and the evolving supply chain ecosystem.

The research methodology combines primary interviews with industry experts and secondary data from verified sources, ensuring accuracy and reliability of all market insights and projections.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global High Voltage Optocoupler Market?

->High Voltage Optocoupler Market was valued at 2156 million in 2024 and is projected to reach US$ 4045 million by 2032, at a CAGR of 9.6% during the forecast period.

Which key companies operate in Global High Voltage Optocoupler Market?

-> Key players include Broadcom, Vishay, ON Semiconductor, Skyworks Solutions, Littelfuse, and EVERLIGHT, among others.

What are the key growth drivers?

-> Key growth drivers include industrial automation adoption, renewable energy expansion, electric vehicle production growth, and stringent safety regulations for electrical isolation.

Which region dominates the market?

-> Asia-Pacific leads the market with over 45% share, driven by electronics manufacturing in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include higher voltage ratings (up to 10kV), miniaturization of components, integration with smart grid systems, and development of high-speed optocouplers for 5G infrastructure.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...