MARKET INSIGHTS

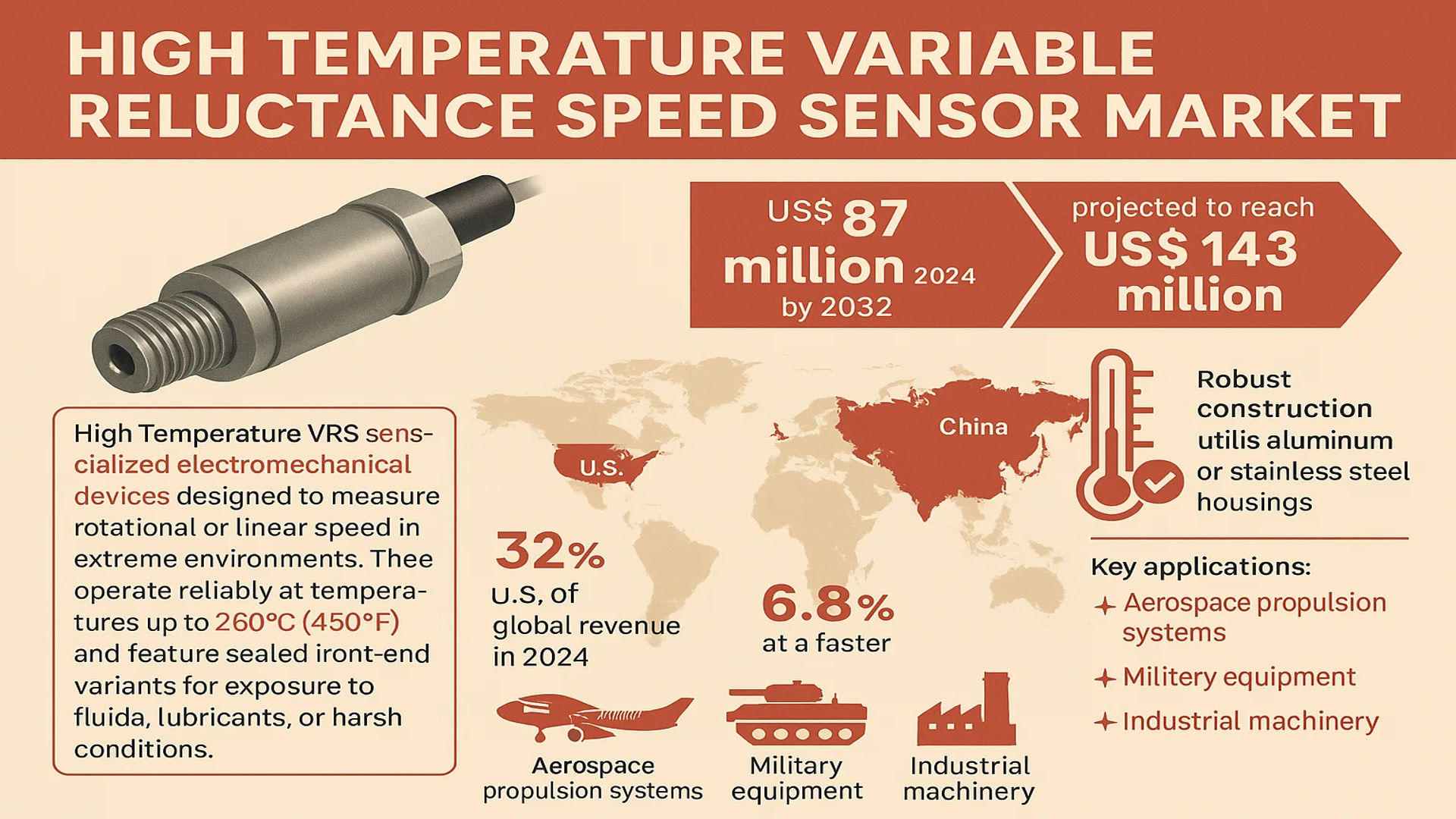

The global High Temperature Variable Reluctance Speed Sensor Market size was valued at US$ 87 million in 2024 and is projected to reach US$ 143 million by 2032, at a CAGR of 7.4% during the forecast period 2025-2032. The U.S. market accounted for 32% of global revenue in 2024, while China is expected to grow at a faster 6.8% CAGR through 2032.

High Temperature VRS sensors are specialized electromechanical devices designed to measure rotational or linear speed in extreme environments. These rugged sensors operate reliably at temperatures up to 260°C (450°F) and feature sealed front-end variants for exposure to fluids, lubricants, or harsh conditions. Their robust construction typically utilizes aluminum or stainless steel housings, with key applications in aerospace propulsion systems, military equipment, and industrial machinery.

The market growth is driven by increasing demand for precision speed monitoring in extreme environments, particularly in aerospace turbine monitoring and defense applications. Recent technological advancements in sensor materials and signal processing algorithms are enhancing measurement accuracy at elevated temperatures. Key industry players like Honeywell and TE Connectivity are expanding their high-temperature sensor portfolios through strategic R&D investments, with the aluminum housing segment projected to reach USD 210 million by 2032.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand from Aerospace and Military Applications to Fuel Market Expansion

The aerospace and defense sectors are witnessing increased adoption of high-temperature variable reluctance speed sensors due to their ability to operate reliably in extreme environments. These sensors play a critical role in monitoring turbine engine speeds, landing gear systems, and other high-temperature applications where conventional sensors might fail. With global military expenditures reaching record levels and commercial aerospace sectors expanding rapidly, the demand for robust sensor solutions is accelerating. The commercial aviation sector alone is projected to require over 40,000 new aircraft in the next two decades, creating sustained demand for reliable speed sensing technologies.

Stringent Safety Regulations Driving Adoption Across Industries

Regulatory mandates across multiple industries are compelling manufacturers to implement more reliable speed monitoring systems. In oil and gas operations, where process safety is paramount, government regulations now require continuous monitoring of rotating equipment in hazardous areas. Similarly, automotive emission control systems operating at high temperatures increasingly incorporate these sensors to comply with tightening environmental standards. These regulatory pressures, coupled with the growing emphasis on predictive maintenance strategies, are creating sustained market growth opportunities across industrial sectors.

➤ Recent standards updates in industrial automation now explicitly recommend variable reluctance sensors for high-temperature applications above 200°C, recognizing their superior reliability compared to Hall-effect alternatives.

Furthermore, the development of advanced materials and manufacturing techniques has significantly improved sensor durability, making them more viable for harsh environment applications. This technological evolution is removing previous barriers to adoption while opening new application possibilities.

MARKET CHALLENGES

High Development and Certification Costs Create Market Entry Barriers

While the market potential is significant, developing high-temperature capable variable reluctance sensors involves substantial engineering challenges and associated costs. The specialized materials required to withstand extreme thermal cycling can increase production costs by 30-50% compared to standard sensors. Moreover, certification processes for aerospace and military applications often require extensive testing protocols spanning several months, significantly delaying time-to-market. These factors combine to create significant barriers for new market entrants and can limit innovation from smaller manufacturers.

Other Challenges

Material Compatibility Issues

Extended operation at high temperatures can lead to material degradation and performance drift in conventional sensor designs. The thermal expansion mismatch between sensor components and mounting surfaces presents ongoing engineering challenges that require continuous R&D investment to overcome.

Supply Chain Vulnerabilities

The reliance on specialty alloys and high-performance materials makes the supply chain particularly susceptible to geopolitical disruptions and commodity price fluctuations. Recent supply chain analyses indicate lead times for critical sensor components have extended by 40-60% compared to pre-pandemic levels.

MARKET RESTRAINTS

Competition from Alternative Technologies Limits Market Penetration

Despite their advantages, high-temperature variable reluctance sensors face strong competition from emerging sensing technologies. Optical encoders and fiber-optic sensors are gaining traction in applications where electromagnetic interference is a concern, while advanced Hall-effect sensors continue to improve their high-temperature performance. In the industrial automation sector, the growing adoption of wireless sensor networks and vibration monitoring systems is displacing traditional speed sensing solutions in some applications. These competing technologies are benefitting from significant R&D investments, resulting in progressive performance improvements that threaten to erode the value proposition of traditional variable reluctance designs.

Additionally, the relatively low accuracy of variable reluctance sensors compared to these alternatives limits their applicability in precision applications, further constraining market growth potential in some segments.

MARKET OPPORTUNITIES

Expansion in Energy Sector Presents Significant Growth Potential

The global shift toward renewable energy systems is creating new opportunities for high-temperature sensor applications. In concentrated solar power plants, where mirror arrays focus sunlight to generate extreme temperatures, reliable speed monitoring of tracking mechanisms is critical. Similarly, advanced geothermal energy projects require robust sensing solutions capable of withstanding harsh underground conditions. As governments worldwide continue to increase investment in alternative energy infrastructure, these applications are expected to drive substantial demand for specialized sensor solutions.

Moreover, the oil and gas industry’s transition toward digital transformation is generating demand for more sophisticated monitoring solutions. The integration of high-temperature sensors with Industrial Internet of Things (IIoT) platforms enables real-time equipment health monitoring, creating opportunities for sensor manufacturers to develop more intelligent, networked solutions. Industry projections suggest the market for smart sensors in harsh environments will grow substantially as asset owners increasingly prioritize predictive maintenance capabilities.

HIGH TEMPERATURE VARIABLE RELUCTANCE SPEED SENSOR MARKET TRENDS

Demand for High-Tolerance Industrial Applications Drives Growth

The High Temperature Variable Reluctance Speed (VRS) Sensor market is experiencing significant expansion due to increasing demand from industries requiring robust sensing solutions in extreme conditions. These sensors, capable of operating in temperatures up to 260°C (450°F), are indispensable in aerospace, military, and heavy industrial applications where traditional sensors fail. In 2024, the market was valued at millions, with projections indicating a strong compound annual growth rate (CAGR) through 2032. The aluminum housing segment is particularly poised for accelerated growth, anticipated to reach multi-million-dollar benchmarks within six years.

Other Trends

Technological Advancements in Material Science

Innovations in sensor materials, including corrosion-resistant alloys and advanced polymers, are enhancing the durability and accuracy of high-temperature VRS sensors. Manufacturers are focusing on improving sensor housings—such as stainless steel variants—to extend operational lifespans in harsh environments like jet engines and industrial turbines. Sealed front-end designs are also gaining traction for applications exposed to fluids and extreme weather conditions, further solidifying their adoption in critical sectors.

Expansion in Aerospace and Defense Sectors

The aerospace and defense industries are key drivers of market growth, accounting for a substantial share of revenue. High-temperature VRS sensors are critical for monitoring turbine speeds, propeller rotations, and other high-stress mechanical systems in aircraft and military vehicles. With global defense budgets increasing—particularly in regions like North America and Asia-Pacific—the demand for reliable, high-performance sensors is expected to rise proportionally. The U.S. currently leads in market size, while China is projected to close the gap by 2032 due to aggressive investments in indigenous aerospace technologies.

Supply Chain Optimization and Regional Manufacturing

To mitigate disruptions, major players like Honeywell and TE Connectivity are localizing production facilities in emerging markets, reducing lead times and costs. This strategy not only addresses logistical challenges but also aligns with regional regulatory requirements, particularly in Europe and Asia. Meanwhile, collaborative R&D initiatives between sensor manufacturers and end-users are accelerating the development of application-specific solutions, such as lightweight sensors for next-generation aircraft.

COMPETITIVE LANDSCAPE

Key Industry Players

Sensor Manufacturers Expand High-Temperature Capabilities to Meet Industrial Demands

The global high temperature variable reluctance speed (VRS) sensor market features a mix of established aerospace/defense suppliers and specialized sensor manufacturers. Honeywell maintains a dominant position due to its extensive application expertise in extreme environment sensing and trusted reputation in aerospace markets where precision reliability is non-negotiable. Their 2024 product refresh of the HTVR series with improved thermal stabilization demonstrates continued category leadership.

TE Connectivity captured nearly 18% market share in 2024 through strategic acquisitions in industrial sensing and proprietary alloy developments that extended operating ceilings to 300°C. Meanwhile, Bosch Sensortec leverages automotive sector synergies, adapting magnetic sensing architectures originally developed for engine management systems to serve adjacent high-temperature industrial applications.

Specialist players like Spectec Thunderbird differentiate through customized sealing solutions for fluid immersion scenarios, holding 62% of the military marine propulsion sub-segment. Their patented dual-housing designs effectively address both thermal and corrosion challenges in naval applications.

Emerging competition comes from motion control specialists such as Motion Sensors Inc., who recently partnered with three tier-1 aerospace suppliers to co-develop next-generation sensors with embedded condition monitoring capabilities. This reflects broader industry convergence between sensing and predictive maintenance functionalities.

List of Key High Temperature VRS Sensor Manufacturers

- Honeywell International Inc. (U.S.)

- Motion Sensors Inc. (U.S.)

- Spectec Thunderbird International Corp (U.S.)

- TE Connectivity Ltd. (Switzerland)

- HarcoSemco (U.S.)

- Bosch Sensortec GmbH (Germany)

- Curtiss-Wright Corporation (U.S.)

- PCB Piezotronics (U.S.)

- Sensata Technologies (Netherlands)

Consolidation accelerated in 2024 with three mid-sized players acquired by conglomerates seeking sensor technology portfolios. This reflects the growing strategic value of high-temperature sensing IP as industries push operational envelopes. However, nimble specialists continue thriving in niche applications through material science innovations and application-specific calibration services.

Segment Analysis:

By Type

Aluminum Housing Segment Leads Due to Lightweight and Cost-Effective Properties

The market is segmented based on type into:

- Aluminum Housing

- Stainless Steel Housing

By Application

Aerospace Segment Dominates Owing to High Demand for Engine Monitoring Systems

The market is segmented based on application into:

- Aerospace

- Military

- Others

By Temperature Range

Standard Range (Up to 260°C) Segment Holds Majority Share Due to Wide Industrial Applications

The market is segmented based on temperature range into:

- Standard Range (Up to 260°C)

- Extended Range (Above 260°C)

By End-User

Commercial Aviation Segment Leads Due to High Fleet Expansion Activities

The market is segmented based on end-user into:

- Commercial Aviation

- Defense

- Industrial

- Energy

Regional Analysis: High Temperature Variable Reluctance Speed Sensor Market

North America

North America leads the global High Temperature Variable Reluctance Speed Sensor (HT-VRS) market, driven by robust aerospace and military spending, particularly in the U.S. The region’s dominance stems from technological advancements, stringent regulatory standards for high-performance sensors, and strong R&D investments by key players like Honeywell and TE Connectivity. The U.S. Department of Defense’s continued modernization programs, with a $842 billion budget allocation in 2024, further accelerate demand for reliable speed sensors in extreme-condition applications. However, supply chain disruptions and stringent export controls pose challenges for manufacturers operating in this region.

Europe

Europe holds significant market share in HT-VRS sensors, supported by advanced automotive and aerospace industries across Germany, France, and the UK. The region’s focus on Industry 4.0 automation and precision engineering creates steady demand for high-temperature capable sensors. EU regulations mandating fail-safe components in transportation systems and energy infrastructure reinforce market growth. While labor costs remain high, European manufacturers differentiate through superior material science, particularly in stainless steel housing sensors that dominate high-end applications. Competition from Asian suppliers and Brexit-related trade complexities present ongoing challenges for the regional market.

Asia-Pacific

The Asia-Pacific region exhibits the fastest growth potential for HT-VRS sensors, propelled by China’s expanding aerospace sector and accelerating industrialization. Local manufacturing capabilities have improved significantly, with Chinese firms now producing cost-competitive aluminum housing sensors suitable for mid-range applications. Japan and South Korea contribute strong demand from their automotive and robotics industries, while India emerges as a promising market with its defense modernization initiatives. However, intellectual property protection concerns and inconsistent quality standards in some countries restrain faster adoption of advanced sensor technologies across the region.

South America

South America represents a developing market for HT-VRS sensors, with Brazil and Argentina showing gradual uptake in mining and oil & gas applications. The region benefits from its abundant natural resources that require rugged sensing solutions for extraction equipment. Economic volatility and reliance on imports for high-end sensor components limit market expansion, though local assembly partnerships with global suppliers are beginning to establish footholds. Infrastructure constraints and political uncertainties in some countries continue to deter larger investments in sensor technology upgrades.

Middle East & Africa

The Middle East & Africa region demonstrates niche demand for HT-VRS sensors, primarily driven by oilfield operations and selected defense applications in GCC countries. Saudi Arabia’s Vision 2030 diversification strategy includes growing investments in aerospace and industrial automation that may boost sensor adoption. In Africa, South Africa leads in mining-related sensor deployments while other nations show minimal uptake due to limited industrialization. The region overall faces challenges including harsh operating environments, lack of technical expertise, and budget constraints for advanced sensor systems.

Report Scope

This market research report provides a comprehensive analysis of the Global High Temperature Variable Reluctance Speed Sensor Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at US$ 87 million in 2024 and is projected to reach US$ 143 million by 2032, growing at a CAGR of 7.4%.

- Segmentation Analysis: Detailed breakdown by product type (Aluminum Housing, Stainless Steel Housing), application (Aerospace, Military, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. market is estimated at USD million in 2024, while China is projected to reach USD million by 2032.

- Competitive Landscape: Profiles of leading market participants, including Honeywell, TE Connectivity, BoschSensortec, and Spectec Thunderbird International Corp, covering their product portfolios, market share, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging sensor technologies, high-temperature material advancements, and integration with IoT platforms.

- Market Drivers & Restraints: Evaluation of factors such as increasing demand from aerospace sector, harsh environment applications, alongside challenges like supply chain disruptions.

- Stakeholder Analysis: Strategic insights for sensor manufacturers, system integrators, and investors regarding market opportunities and competitive positioning.

The research methodology combines primary interviews with industry experts and analysis of verified secondary data sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global High Temperature Variable Reluctance Speed Sensor Market?

-> High Temperature Variable Reluctance Speed Sensor Market size was valued at c and is projected to reach US$ 143 million by 2032, at a CAGR of 7.4% during the forecast period 2025-2032.

Which key companies operate in this market?

-> Key players include Honeywell, Motion Sensors, TE Connectivity, BoschSensortec, and Spectec Thunderbird International Corp.

What are the key growth drivers?

-> Growth is driven by increasing aerospace applications, demand for harsh environment sensors, and industrial automation trends.

Which region dominates the market?

-> North America currently leads, while Asia-Pacific shows the fastest growth potential.

What are the emerging trends?

-> Emerging trends include development of ultra-high temperature sensors, miniaturization, and smart sensor integration.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...