MARKET INSIGHTS

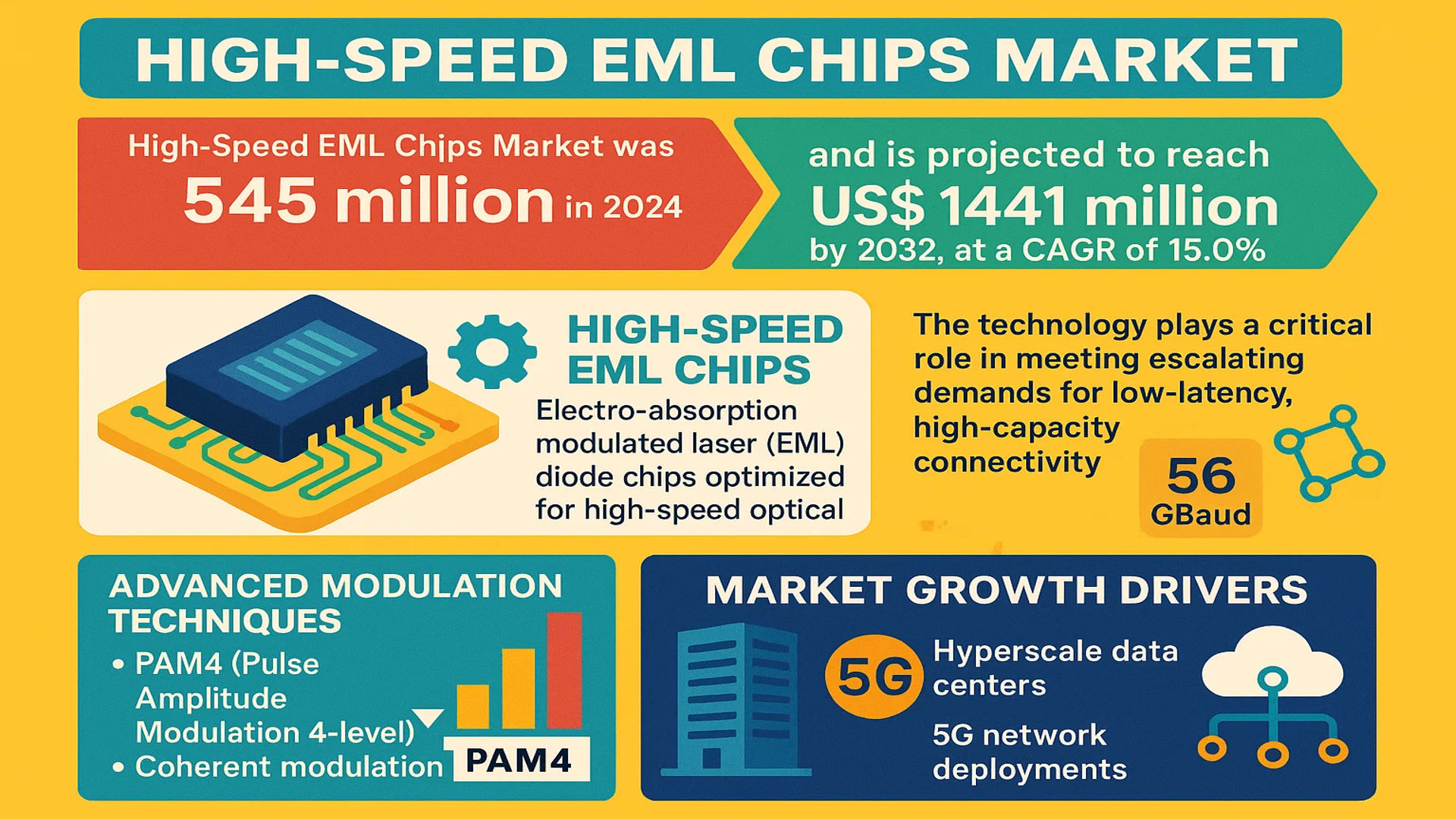

The global High-Speed EML Chips Market was valued at 545 million in 2024 and is projected to reach US$ 1441 million by 2032, at a CAGR of 15.0% during the forecast period.

High-Speed EML Chips are electro-absorption modulated laser (EML) diode chips optimized for high-speed optical signal transmission in telecommunications and data centers. These chips leverage advanced modulation techniques such as PAM4 (Pulse Amplitude Modulation 4-level) and coherent modulation to achieve data rates exceeding 56 GBaud, enabling efficient bandwidth utilization in next-generation networks. The technology plays a critical role in meeting escalating demands for low-latency, high-capacity connectivity.

The market growth is driven by surging bandwidth requirements from hyperscale data centers, 5G network deployments, and cloud computing expansion. While North America currently leads adoption due to early 5G rollouts, Asia-Pacific shows the fastest growth trajectory, with China’s market projected to reach USD 420 million by 2032. Key players like Lumentum and Coherent (II-VI) dominate the competitive landscape, collectively holding over 60% market share through continuous innovation in chip miniaturization and power efficiency.

MARKET DYNAMICS

MARKET DRIVERS

Exponential Growth in Data Traffic Driving Demand for High-Speed EML Chips

The global surge in data consumption is creating unprecedented demand for high-speed optical communication solutions. With internet traffic projected to grow at a compound annual rate exceeding 30% through 2030, network operators are aggressively upgrading infrastructure to handle these bandwidth requirements. High-Speed EML Chips, capable of supporting data rates above 100G per channel, have become critical enablers for next-generation networks. Their ability to maintain signal integrity at higher baud rates makes them indispensable for 400G and 800G optical transceivers that form the backbone of modern data centers and telecom networks.

Cloud Computing Expansion Accelerating EML Chip Adoption

The rapid growth of cloud services is significantly impacting the High-Speed EML Chips market. Leading cloud service providers are deploying hyperscale data centers that require thousands of optical interconnect links, each demanding reliable high-speed transmission capabilities. The shift toward disaggregated data center architectures has further increased the need for high-performance optical components. These chips are now essential for meeting the low-latency, high-bandwidth requirements of cloud-native applications, artificial intelligence workloads, and 5G backhaul networks. Recent technology advancements have enabled EML chips to achieve higher modulation efficiency while reducing power consumption, making them particularly attractive for large-scale deployments.

5G Network Deployments Creating New Market Opportunities

The global rollout of 5G networks represents a significant growth opportunity for High-Speed EML Chip manufacturers. 5G fronthaul and backhaul networks require optical transmission systems capable of handling substantially higher data rates than previous generations. EML-based optical modules are becoming the preferred solution for these applications due to their superior performance characteristics compared to traditional laser technologies. With projections indicating over 4 billion 5G connections by 2030, the demand for high-speed optical components in telecommunications infrastructure is expected to remain strong throughout the decade. The development of advanced EML chip designs optimized for 5G-specific requirements is further accelerating market adoption.

MARKET RESTRAINTS

High Production Costs and Complex Manufacturing Processes Limiting Market Expansion

Despite strong demand, the High-Speed EML Chips market faces significant cost-related challenges. The manufacturing process for these components involves sophisticated epitaxial growth techniques and precise wafer processing steps that require specialized equipment and cleanroom facilities. These factors contribute to high production costs that can limit adoption in price-sensitive market segments. Additionally, the yield rates for high-performance EML chips remain challenging, with many manufacturers reporting yield percentages below optimal levels. This cost structure creates barriers to entry for new market participants and can slow the pace of technology adoption in developing regions.

Thermal Management Challenges Impacting Performance and Reliability

As data rates continue to increase, thermal management has emerged as a critical restraint for High-Speed EML Chip performance. The operation of these chips at higher speeds generates significant heat, which can affect wavelength stability and component reliability. Managing thermal effects becomes particularly challenging in dense optical module configurations where multiple high-speed channels operate in close proximity. While advanced packaging techniques and improved heat dissipation materials are being developed, thermal constraints continue to influence product designs and may limit performance scaling in certain applications.

Supply Chain Vulnerabilities Creating Market Uncertainty

The global semiconductor supply chain disruptions have significantly impacted the High-Speed EML Chips market. These specialized components rely on rare earth materials and compound semiconductor substrates that face supply constraints. Lead times for critical manufacturing equipment have extended, while geopolitical factors have introduced additional complexity to raw material sourcing. Such supply chain challenges have created production bottlenecks and price volatility that may persist in the near term, potentially slowing market growth in the short to medium term.

MARKET OPPORTUNITIES

Emerging Datacom and Telecom Standards Opening New Application Areas

The development of new optical networking standards presents significant growth opportunities for High-Speed EML Chip suppliers. Emerging specifications for 800G and 1.6T Ethernet create demand for next-generation optical components with enhanced performance characteristics. The transition to higher-order modulation schemes and the development of co-packaged optics architectures are driving innovation in EML chip design. These technology trends enable manufacturers to deliver solutions that address the evolving requirements of hyperscale data centers and telecommunications networks, positioning themselves for future market expansion.

Artificial Intelligence Workloads Driving Demand for Specialized Optical Solutions

The exponential growth of artificial intelligence and machine learning applications is creating new opportunities for High-Speed EML Chip developers. AI clusters require ultra-high-bandwidth interconnect solutions to support distributed training and inference workloads. Optical interconnect technologies based on advanced EML chips are well-positioned to address these requirements, particularly in applications requiring low-latency communication between computing nodes. The development of optimized solutions for AI-specific connectivity needs represents a promising area for technology differentiation and market growth.

Geographic Expansion into Emerging Markets

Growing investments in digital infrastructure across developing regions present substantial market expansion opportunities. Governments in Asia, Latin America, and Africa are prioritizing broadband network upgrades and data center construction projects. These initiatives create demand for high-performance optical components, with High-Speed EML Chips playing a crucial role in next-generation network architectures. Strategic partnerships with regional telecom operators and data center providers can help manufacturers establish strong market positions in these high-growth territories.

MARKET CHALLENGES

Intense Competition from Alternative Technologies

The High-Speed EML Chips market faces growing competition from emerging optical technologies that threaten to disrupt traditional product segments. Silicon photonics solutions are achieving increasingly competitive performance levels at potentially lower cost points, creating pricing pressure across the market. Additionally, developments in tunable laser technologies and vertical-cavity surface-emitting lasers (VCSELs) are expanding the range of available options for optical system designers. These competitive dynamics require EML chip manufacturers to continuously innovate and demonstrate clear performance advantages to maintain market share.

Rapid Technology Evolution Increasing R&D Investment Requirements

The accelerated pace of technological advancement in optical communications presents significant challenges for High-Speed EML Chip developers. Product lifecycles continue to shorten as new performance benchmarks are established, requiring substantial ongoing investments in research and development. Developing next-generation EML chips capable of supporting 200G per lane operation and beyond involves complex engineering challenges and significant capital expenditures. These requirements create financial pressures for market participants and may drive further industry consolidation as companies seek to combine technical expertise and financial resources.

Regulatory and Compliance Complexities in Global Markets

Navigating diverse regulatory environments represents an ongoing challenge for High-Speed EML Chip suppliers operating in global markets. Export control regulations, particularly those concerning advanced semiconductor technologies, have introduced additional complexity to international business operations. Furthermore, evolving standards for energy efficiency and product safety require continuous monitoring and product adaptation. These regulatory factors can impact time-to-market for new products and increase compliance costs, particularly for companies targeting multiple geographic regions with differing requirements.

HIGH-SPEED EML CHIPS MARKET TRENDS

Rising Demand for High-Speed Data Transmission Drives Market Growth

The global high-speed EML (Electro-Absorption Modulated Laser) chips market is experiencing robust growth, fueled by soaring demand for faster data transmission in telecommunications and data centers. With internet traffic doubling every three years, network operators are investing heavily in ultra-high-speed optical modules to meet bandwidth requirements. In 2024, the market was valued at $545 million, with projections indicating a surge to $1.44 billion by 2032, growing at a 15.0% CAGR. Leading manufacturers are focusing on chips exceeding 56 GBaud speeds to support next-gen networks such as 800G and 1.6T Ethernet.

Other Trends

Adoption in Data Center Interconnect (DCI) Networks

High-speed EML chips are increasingly critical for hyperscale data centers, where low-latency, high-capacity connectivity is essential. The rising deployment of cloud computing and AI-driven workloads has amplified the need for EML-based transceivers capable of 400G and beyond. Industry leaders like Broadcom and Lumentum are innovating in coherent optics, enhancing transmission efficiency. Approximately 70% of new data center installations now incorporate EML-based solutions for long-haul DCI applications, reflecting this shift.

Regional Market Expansion and Competitive Landscape

North America and Asia-Pacific dominate the high-speed EML chips market, collectively holding over 60% of global revenue. The U.S. remains the largest contributor, driven by 5G rollouts and investments in fiber-optic infrastructure. Meanwhile, China is rapidly closing the gap with aggressive R&D in indigenous semiconductor technologies. Key players like Coherent (II-VI) and Mitsubishi Electric are expanding production capacities to address regional demands, with the top five manufacturers accounting for a significant market share as of 2024.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Leaders Drive Innovation in High-Speed EML Chips to Meet Growing Bandwidth Demands

The competitive landscape of the global High-Speed EML (Electroabsorption Modulated Laser) Chips market is characterized by a mix of established players and emerging innovators working to meet the surging demand for high-speed optical communication solutions. Lumentum Holdings Inc. leads the market with its cutting-edge product portfolio and strong foothold across North America, Europe, and Asia-Pacific. The company specializes in high-performance EML chips, particularly for data center and telecommunications applications, leveraging its expertise in photonics.

Coherent Corp. (formerly II-VI) and Mitsubishi Electric also hold significant market shares, driven by their technological advancements in semiconductor lasers and long-term investments in R&D. These companies have demonstrated resilience in scaling production to meet the rapid growth in 400G and 800G optical modules, which rely heavily on high-speed EML chips.

Market leaders are actively engaging in strategic expansions to strengthen their positions. For instance, Broadcom Inc. recently enhanced its optical portfolio through targeted acquisitions, while Source Photonics continues to expand its manufacturing capabilities in Asia to cater to growing regional demand. Such moves are expected to intensify competition while accelerating innovation cycles.

List of Leading Global High-Speed EML Chip Manufacturers

- Lumentum Holdings Inc. (U.S.)

- Coherent Corp. (II-VI) (U.S.)

- Mitsubishi Electric Corporation (Japan)

- Source Photonics (U.S.)

- Broadcom Inc. (U.S.)

- Sumitomo Electric Industries, Ltd. (Japan)

- Applied Optoelectronics, Inc. (U.S.)

- NTT Electronics Corporation (Japan)

While established players dominate the landscape, the market also sees promising innovations from smaller specialized firms developing niche solutions for emerging applications like AI infrastructure and next-gen DCI networks. This dynamic ensures healthy competition that benefits end-users through improved performance and cost efficiencies.

Segment Analysis:

By Type

Above 56 GBaud Segment Leads Due to Rising Demand for Ultra-High-Speed Data Transmission

The market is segmented based on type into:

- Below 56 GBaud

- Above 56 GBaud

By Application

Telecommunications Segment Dominates Owing to Increasing Fiber Optic Network Deployments

The market is segmented based on application into:

- Telecommunications

- Data Center Interconnection (DCI Network)

By End User

Network Service Providers Hold Major Share Due to 5G Infrastructure Requirements

The market is segmented based on end user into:

- Network Service Providers

- Cloud Service Providers

- Enterprise Networks

- Others

By Region

Asia Pacific Shows Strongest Growth Potential with Rapid Digitalization Initiatives

The market is segmented based on region into:

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

Regional Analysis: High-Speed EML Chips Market

Asia-Pacific

The Asia-Pacific region dominates the High-Speed EML Chips market, driven by rapid digital transformation and massive investments in 5G infrastructure. China leads the regional demand due to its extensive fiber optic network deployments and government initiatives like the “Digital China” strategy. Japan and South Korea follow closely, with their advanced semiconductor industries and early adoption of high-speed optical communication technologies. The region benefits from strong manufacturing capabilities, with key players like Mitsubishi Electric and Sumitomo expanding production to meet growing data center and telecom needs. However, geopolitical tensions and supply chain vulnerabilities pose challenges for uninterrupted component sourcing.

North America

North America’s market growth is fueled by hyperscale data center expansion and telecommunications upgrades to support cloud computing and AI applications. The U.S. accounts for over 60% of regional demand, with major tech hubs in Silicon Valley and Virginia driving innovation. Lumentum and Broadcom lead the supplier landscape, collaborating with cloud service providers for customized EML solutions. While the Chips Act provides funding for domestic semiconductor production, dependence on Asian foundries remains a concern. Regulatory pressures for energy-efficient data transmission further accelerate adoption of high-performance chips in this mature market.

Europe

European demand centers around Germany and the UK, where stringent data privacy laws necessitate localized data processing infrastructure. The region shows strong uptake of above-56 GBaud chips for high-capacity metro networks, with Nokia and Ericsson integrating EML solutions into their telecom equipment. EU funding programs for photonics innovation support R&D, but market growth is tempered by slower 5G rollout compared to Asia. Environmental regulations on electronic components also influence product designs, pushing manufacturers toward more sustainable packaging and materials in their chip production.

Middle East & Africa

This emerging market is witnessing gradual infrastructure modernization, with UAE and Saudi Arabia making strategic investments in smart cities and digital hubs. Limited local manufacturing capabilities currently create reliance on imports, though economic diversification initiatives are fostering technology partnerships. Submarine cable projects along African coasts present long-term opportunities, but uneven internet penetration and power stability issues delay widespread EML chip adoption. The region shows potential as a testing ground for cost-effective solutions tailored for developing economies.

South America

Brazil represents the primary market in this region, where growing internet usage drives upgrades to backbone networks. However, economic constraints limit large-scale deployments, with many operators prioritizing below-56 GBaud solutions for cost efficiency. Political instability in some countries creates supply chain uncertainties, though free trade agreements facilitate equipment imports. As digital transformation accelerates in banking and e-commerce sectors, selective opportunities emerge for EML chip suppliers willing to navigate the region’s complex business environment.

Report Scope

This market research report provides a comprehensive analysis of the global and regional High-Speed EML Chips markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global High-Speed EML Chips market was valued at USD 545 million in 2024 and is projected to reach USD 1441 million by 2032.

- Segmentation Analysis: Detailed breakdown by product type (Below 56 GBaud, Above 56 GBaud), application (Telecommunications, Data Center Interconnection), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with China and the U.S. as key growth markets.

- Competitive Landscape: Profiles of leading market participants including Lumentum, Coherent (II-VI), Mitsubishi Electric, Source Photonics, and Broadcom, covering their product offerings and strategic developments.

- Technology Trends & Innovation: Assessment of emerging optical communication technologies, advanced modulation techniques, and semiconductor fabrication improvements.

- Market Drivers & Restraints: Evaluation of factors like 5G deployment and data center expansion driving growth, along with supply chain challenges and high manufacturing costs.

- Stakeholder Analysis: Insights for chip manufacturers, network equipment providers, telecom operators, and investors regarding market opportunities.

The report employs both primary and secondary research methods, including interviews with industry experts and analysis of verified market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global High-Speed EML Chips Market?

-> High-Speed EML Chips Market was valued at 545 million in 2024 and is projected to reach US$ 1441 million by 2032, at a CAGR of 15.0% during the forecast period.

Which key companies operate in Global High-Speed EML Chips Market?

-> Key players include Lumentum, Coherent (II-VI), Mitsubishi Electric, Source Photonics, Broadcom, Sumitomo, Applied Optoelectronics, and NTT Electronics.

What are the key growth drivers?

-> Key growth drivers include 5G network deployment, hyperscale data center expansion, increasing bandwidth demand, and cloud computing adoption.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by China’s telecom infrastructure development, while North America leads in technological adoption.

What are the emerging trends?

-> Emerging trends include higher modulation speeds (100G+), co-packaged optics, silicon photonics integration, and energy-efficient designs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...