MARKET INSIGHTS

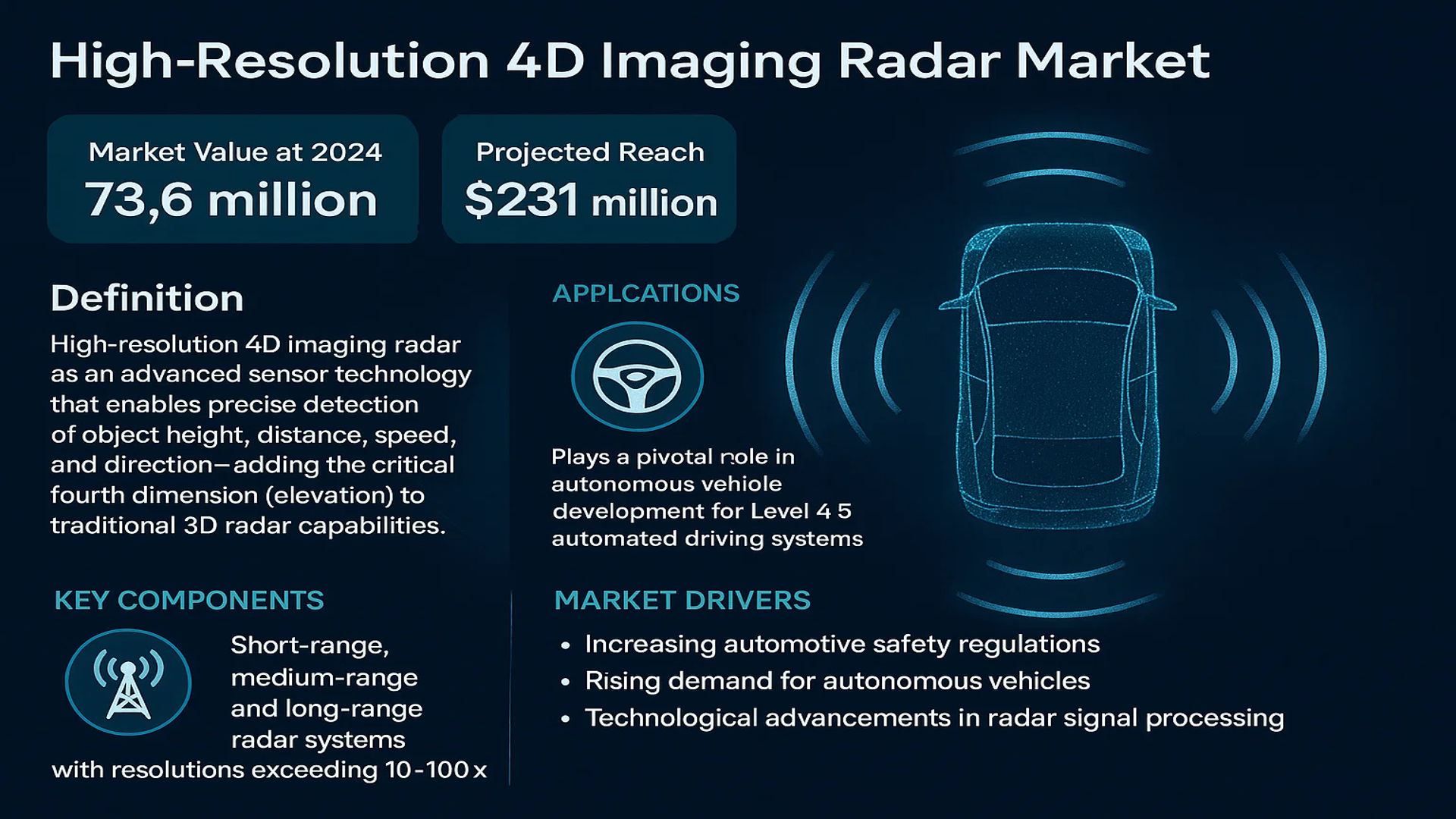

The global High-Resolution 4D Imaging Radar Market was valued at 73.6 million in 2024 and is projected to reach US$ 231 million by 2032, at a CAGR of 18.2% during the forecast period.

High-resolution 4D imaging radar is an advanced sensor technology that enables precise detection of object height, distance, speed, and direction—adding the critical fourth dimension (elevation) to traditional 3D radar capabilities. This technology plays a pivotal role in autonomous vehicle development, particularly for Level 4 and 5 automated driving systems, while also enhancing advanced driver-assistance systems (ADAS) in passenger and commercial vehicles. Key components include short-range, medium-range, and long-range radar systems with resolutions exceeding traditional automotive radars by 10-100x.

The market growth is primarily driven by increasing automotive safety regulations, rising demand for autonomous vehicles, and technological advancements in radar signal processing. Major automakers are accelerating adoption, with over 15 automotive OEMs currently testing or implementing 4D imaging radar solutions. Strategic collaborations, such as Continental AG’s 2023 partnership with a leading semiconductor manufacturer to develop next-gen radar chips, are further propelling innovation. Other key players shaping the competitive landscape include ZF Friedrichshafen AG, Arbe Robotics, and Aptiv PLC, who collectively hold approximately 45% of the 2024 market share.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Autonomous Vehicles to Accelerate Market Growth

The automotive industry’s rapid shift toward autonomous driving systems is a key driver for the high-resolution 4D imaging radar market. As vehicle manufacturers target Level 4 and 5 autonomy, they require sensors with superior object detection capabilities. 4D imaging radar provides centimeter-level accuracy in detecting an object’s position, velocity, and elevation – capabilities that traditional radar systems cannot match. By 2030, nearly 30% of new vehicles sold globally are projected to feature some level of autonomous functionality, creating massive demand for advanced sensing technologies. Major automakers have already begun integrating these radars into their flagship models, with deployment expected to grow at 45% annually through 2028.

Government Regulations Mandating Advanced Safety Features

Stringent vehicle safety regulations worldwide are compelling automakers to adopt next-generation radar systems. Regulatory bodies in North America and Europe now require advanced driver assistance systems (ADAS) as standard equipment, with many Asian markets following suit. For instance, the European Union’s General Safety Regulation mandates intelligent speed assistance and autonomous emergency braking for all new vehicles. These policies directly increase demand for high-resolution 4D imaging radar, as it provides more reliable object detection compared to traditional radar or camera systems alone. The technology’s all-weather performance makes it particularly valuable for meeting these regulatory requirements while maintaining high safety standards.

➤ Currently, over 60% of premium vehicle models include some form of ADAS functionality, with mid-range models expected to reach similar adoption rates by 2027.

Furthermore, the increasing integration of artificial intelligence with radar systems enhances detection algorithms, allowing for better interpretation of complex driving scenarios. This technological synergy further strengthens the case for 4D imaging radar adoption across automotive applications.

MARKET RESTRAINTS

High Development Costs Limiting Mass Market Adoption

While the technology offers clear advantages, the current cost structure remains prohibitive for widespread implementation. Developing high-resolution 4D imaging radar systems requires significant investment in specialized hardware and signal processing software. The average unit cost currently ranges between $150-$300 for automotive-grade systems, which is nearly triple the price of conventional radar modules. This pricing gap creates affordability challenges, particularly for economy vehicle segments that account for over 60% of global automotive sales. Until manufacturing processes achieve economies of scale, cost barriers will continue restricting market penetration to premium vehicle categories.

Other Restraints

Computational Complexity

The massive data processing requirements of 4D imaging radar systems pose significant technical challenges. Each sensor generates over 1 terabyte of raw data per hour of operation, demanding powerful onboard computing resources. This computational burden increases system costs and energy consumption, creating trade-offs in vehicle design.

Sensor Fusion Integration

Effectively combining 4D radar data with inputs from cameras and LiDAR requires sophisticated fusion algorithms. The automotive industry currently lacks standardized approaches for this integration, leading to implementation challenges that slow product development cycles.

MARKET CHALLENGES

Technical Limitations in Extreme Weather Conditions

While 4D imaging radar performs better than optical sensors in adverse weather, significant challenges remain in extreme precipitation scenarios. Heavy rain and snow can attenuate radar signals by up to 40%, reducing detection range and accuracy. These limitations create reliability concerns for fully autonomous systems that must operate without human intervention. Current research focuses on algorithmic compensation techniques, but real-world performance under all weather conditions remains an area requiring substantial improvement. This technical hurdle is particularly critical as automakers aim to deliver fully autonomous vehicles capable of operating safely in all environments.

Other Challenges

Spectrum Allocation Issues

The automotive radar industry faces increasing congestion in the 76-81 GHz frequency band traditionally used for these applications. With multiple adjacent technologies competing for spectrum space, interference risks could degrade system performance unless robust mitigation strategies are developed.

Standardization Gaps

The absence of universal performance metrics and testing protocols for 4D imaging radar creates uncertainty for manufacturers and regulators alike. The industry needs standardized evaluation criteria to ensure consistent performance across different implementations.

MARKET OPPORTUNITIES

Emerging Applications in Smart Infrastructure Creating New Revenue Streams

Beyond automotive applications, 4D imaging radar presents significant opportunities in smart city infrastructure and industrial automation. Municipalities are increasingly deploying these systems for traffic management, pedestrian detection, and intersection safety monitoring. The technology’s ability to operate reliably in diverse environments makes it ideal for outdoor installations where cameras face limitations. Current projections indicate the smart infrastructure radar market could exceed $500 million annually by 2028. This non-automotive segment offers manufacturers valuable diversification opportunities while accelerating technology maturation through volume production.

Advancements in Semiconductor Technology Enabling Cost Reductions

Recent breakthroughs in radar chipset design are paving the way for more affordable 4D imaging solutions. The development of highly integrated radar-on-chip designs reduces component count and assembly complexity, potentially cutting production costs by 30-40% within the next three years. These innovations, coupled with the transition to more cost-effective manufacturing processes, will help bridge the price gap with conventional radar systems. As these technological advancements reach mass production, they will enable broader market adoption across mid-range vehicle segments and industrial applications.

Additionally, the growing interest from technology companies entering the automotive sector is accelerating innovation. These new entrants often bring fresh perspectives on system architectures and unique approaches to solving traditional radar challenges, further expanding the technology’s potential applications.

HIGH-RESOLUTION 4D IMAGING RADAR MARKET TRENDS

Autonomous Vehicle Integration Accelerates Adoption

The rapid development of autonomous vehicles (AVs) is driving significant demand for high-resolution 4D imaging radar systems. Unlike traditional radar, which provides limited elevation data, 4D radar offers high-resolution detection capabilities that enable vehicles to distinguish between objects at different heights, such as overpasses and bridges. Major automakers are increasingly incorporating this technology into Level 4 and Level 5 autonomous driving systems, as it provides superior environmental perception in adverse weather conditions where cameras and LiDAR may struggle. Recent innovations, such as beamforming and multi-input multi-output (MIMO) antenna configurations, have further enhanced the resolution and reliability of these systems.

Other Trends

Expansion of ADAS Applications

The growing need for advanced driver-assistance systems (ADAS) in passenger and commercial vehicles is a key factor fueling market growth. 4D imaging radar is increasingly being adopted for adaptive cruise control, automatic emergency braking, and blind-spot detection due to its ability to detect stationary objects more accurately than conventional radar. Leading automotive suppliers are developing compact, low-power 4D radar modules that integrate seamlessly into newer vehicle models, expanding their applicability beyond high-end autonomous platforms.

Technological Advancements in Sensor Fusion

The integration of 4D imaging radar with other sensor modalities, such as LiDAR and cameras, is emerging as a critical trend in the automotive and smart infrastructure sectors. Sensor fusion enhances decision-making accuracy by cross-referencing data from multiple sources, reducing false positives in object detection. Recent breakthroughs in AI-based signal processing enable 4D radar systems to classify pedestrians, cyclists, and other vulnerable road users with higher precision, addressing one of the key safety concerns in autonomous driving. Investments in silicon-based radar chips are also lowering production costs, making the technology more accessible to mid-range vehicle manufacturers.

COMPETITIVE LANDSCAPE

Key Industry Players

Automotive and Tech Giants Accelerate Innovation in 4D Radar for Autonomous Driving

The High-Resolution 4D Imaging Radar market is witnessing intensified competition as established automotive suppliers and emerging tech firms race to develop next-generation sensor solutions. Continental AG and ZF Friedrichshafen AG currently lead the market, collectively accounting for over 35% of global revenue in 2024 due to their long-standing relationships with automakers and vertically integrated manufacturing capabilities.

While traditional players dominate OEM partnerships, innovative startups like Arbe Robotics and Oculii are gaining traction through disruptive chipset designs. Arbe’s Phoenix radar system, capable of detecting objects at 300 meters with 1° angular resolution, has secured design wins with multiple Asian automakers. Similarly, Vayyar Imaging’s software-defined radar technology has demonstrated strong potential for interior monitoring applications.

The competitive environment is further intensified by strategic moves from technology conglomerates. HUAWEI entered the market in 2023 with its 4D imaging radar solution, leveraging its expertise in signal processing. This reflects the broader trend of tech firms expanding into automotive sensing technologies as the industry transitions toward autonomous mobility.

Meanwhile, established players are responding through acquisitions and partnerships. Aptiv PLC strengthened its position through the 2022 acquisition of Wind River Systems to enhance its radar-software integration capabilities. Such consolidation activities are expected to continue as companies seek to offer comprehensive autonomous driving solutions rather than standalone radar components.

List of Key High-Resolution 4D Imaging Radar Companies Profiled

- Continental AG (Germany)

- ZF Friedrichshafen AG (Germany)

- Arbe Robotics (Israel)

- Aptiv PLC (Ireland)

- Steradian Semiconductors (India – Acquired by Renesas)

- Zadar Labs, Inc. (U.S.)

- Vayyar Imaging (Israel)

- Smartmicro (Germany)

- HUAWEI Technologies (China)

- Oculii (U.S.)

- Robert Bosch GmbH (Germany)

Segment Analysis:

By Type

Long-Range 4D Imaging Radar Leads Market Due to High Demand in Advanced Autonomous Driving Applications

The market is segmented based on type into:

- Short Range

- Subtypes: Below 100 meters operational range

- Medium Range

- Subtypes: 100-250 meters operational range

- Long Range

- Subtypes: Above 250 meters operational range

By Application

Passenger Vehicle Segment Dominates Owing to Increasing Integration of ADAS Features

The market is segmented based on application into:

- Passenger Vehicle

- Commercial Vehicle

By Technology

MMIC-based Radars Gain Traction for Their Compact Size and High Performance

The market is segmented based on technology into:

- MMIC (Monolithic Microwave Integrated Circuit)

- SiGe (Silicon-Germanium)

- CMOS (Complementary Metal-Oxide-Semiconductor)

- Others

Regional Analysis: High-Resolution 4D Imaging Radar Market

North America

North America leads the global 4D imaging radar market, driven by robust automotive R&D and substantial investments in autonomous vehicle technology. The U.S., in particular, accounts for over 65% of regional revenue, with key players like Aptiv and Continental AG accelerating deployments in ADAS applications. Government mandates for vehicle safety systems and partnerships between automakers and radar manufacturers further propel adoption. Long-range radar dominates due to highway-focused testing, while short-range variants gain traction for urban mobility applications. However, high production costs and complex integration with existing vehicle architectures remain challenges.

Europe

Europe demonstrates strong growth potential, with Germany at the forefront contributing nearly 40% of regional demand. The EU’s strict NCAP safety ratings and emphasis on pedestrian protection create a favorable regulatory environment. Companies like ZF Friedrichshafen and Bosch are pioneering compact radar solutions that comply with stringent electromagnetic interference standards. Medium-range radar dominates for European road conditions, though supply chain disruptions from geopolitical tensions occasionally hinder production. Collaborative projects like the EU’s Vision Zero initiative continue to stimulate market expansion through 2030.

Asia-Pacific

The fastest-growing region, Asia-Pacific is projected to surpass North America in unit shipments by 2027. China’s aggressive autonomous vehicle roadmap drives 53% of regional demand, with Huawei and domestic manufacturers prioritizing cost-effective radar solutions. Japan and South Korea follow closely, focusing on precision radar for dense urban environments. While passenger vehicles currently lead adoption, commercial vehicle applications show promising growth, particularly in last-mile delivery automation. Price sensitivity and intense local competition present challenges for international suppliers entering this dynamic market.

South America

South America represents an emerging market where adoption is primarily led by Brazil’s automotive manufacturing sector. Limited local production capacity means over 85% of 4D radar systems are imported, creating opportunities for global suppliers. The focus remains on entry-level ADAS features in premium vehicle segments due to economic constraints. Infrastructure limitations and fluctuating import tariffs impact market consistency, though regional trade agreements show potential for stabilized growth. Recent testing of radar-based toll collection systems indicates diversification beyond automotive applications.

Middle East & Africa

This developing market demonstrates uneven growth, with the UAE and Saudi Arabia driving most demand through smart city initiatives. The absence of local automotive manufacturing means adoption is concentrated in aftermarket upgrades and infrastructure projects. High ambient temperatures pose unique technical challenges for radar performance, prompting tailored solutions from suppliers. While current penetration remains below 5% of the global market, strategic investments in transport automation and border security applications suggest long-term potential, particularly for ruggedized long-range radar systems.

Report Scope

This market research report provides a comprehensive analysis of the global and regional High-Resolution 4D Imaging Radar markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global High-Resolution 4D Imaging Radar market was valued at USD 73.6 million in 2024 and is projected to reach USD 231 million by 2032, growing at a CAGR of 18.2%.

- Segmentation Analysis: Detailed breakdown by product type (Short Range, Medium Range, Long Range), application (Passenger Vehicle, Commercial Vehicle), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific is expected to dominate the market due to rapid automotive industry growth.

- Competitive Landscape: Profiles of leading market participants including ZF Friedrichshafen AG, Arbe, Aptiv, Continental AG, and Bosch, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies in 4D radar, integration with ADAS and autonomous vehicles, semiconductor advancements, and evolving industry standards for Level 4/5 automation.

- Market Drivers & Restraints: Evaluation of factors driving market growth (increasing demand for autonomous vehicles, safety regulations) along with challenges (high development costs, supply chain constraints).

- Stakeholder Analysis: Insights for component suppliers, automotive OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities in radar technology.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global High-Resolution 4D Imaging Radar Market?

-> High-Resolution 4D Imaging Radar Market was valued at 73.6 million in 2024 and is projected to reach US$ 231 million by 2032, at a CAGR of 18.2% during the forecast period.

Which key companies operate in Global High-Resolution 4D Imaging Radar Market?

-> Key players include ZF Friedrichshafen AG, Arbe, Aptiv, Continental AG, Bosch, Vayyar Imaging, and Huawei, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for autonomous vehicles, stringent safety regulations, and advancements in ADAS technology.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by automotive manufacturing growth in China, Japan, and South Korea, while North America leads in technological innovation.

What are the emerging trends?

-> Emerging trends include integration with AI for object classification, development of compact radar systems, and increasing adoption in commercial vehicles.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...