High-Efficiency PV Market Insights

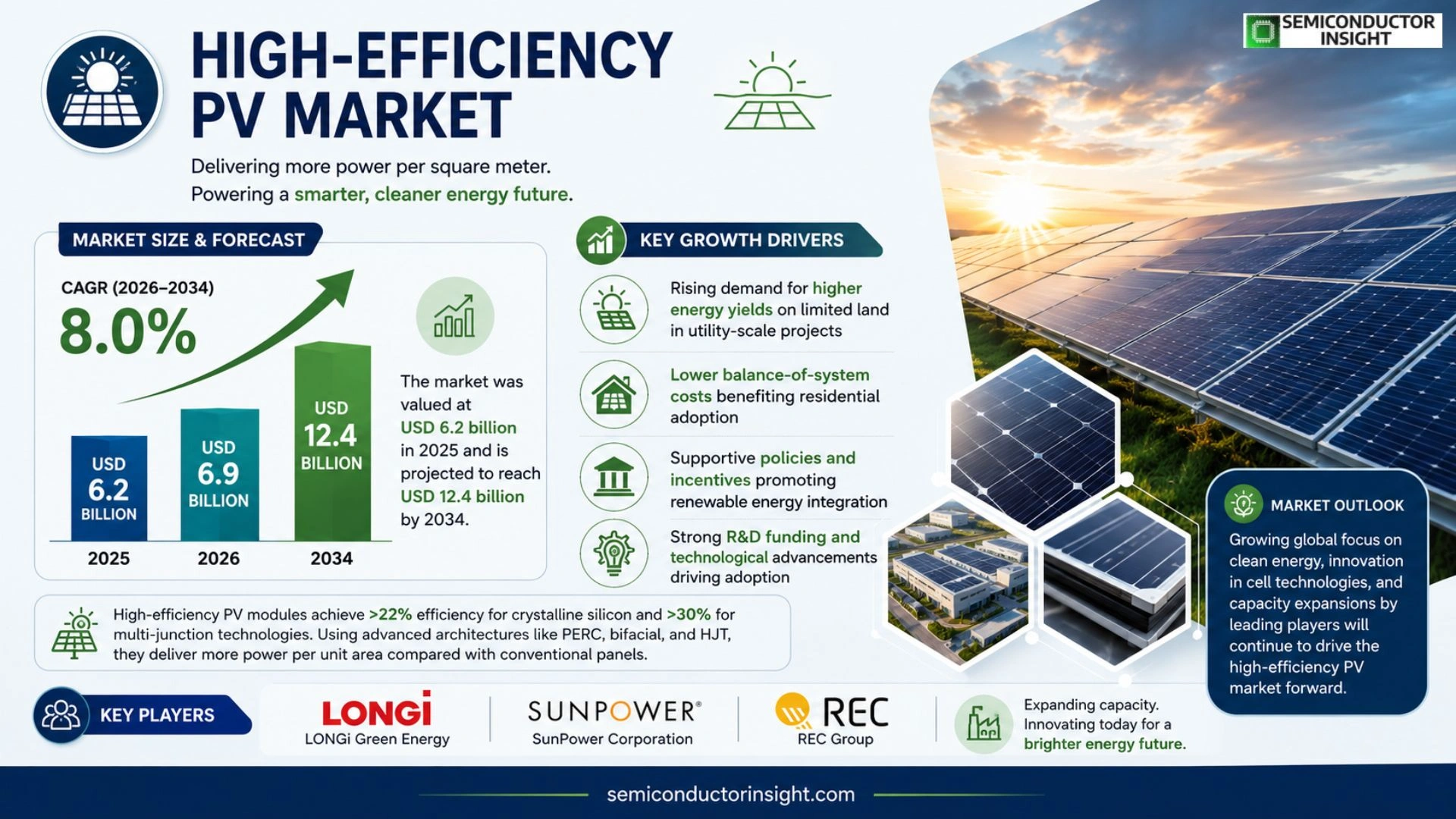

Global High‑Efficiency PV Market size was valued at USD 6.2 billion in 2025. The market is projected to grow from USD 6.9 billion in 2026 to USD 12.4 billion by 2034, exhibiting a CAGR of 8.0% during the forecast period.

High‑efficiency photovoltaic (PV) modules are solar cells that achieve conversion efficiencies above 22 % for crystalline silicon and above 30 % for multi‑junction technologies. These modules incorporate advanced cell architectures such as PERC, bifacial designs, and heterojunction back‑contact (HJT) structures, delivering more power per unit area compared with conventional panels.

The market is accelerating because utility‑scale developers seek higher energy yields on limited land, while residential adopters benefit from lower balance‑of‑system costs. Furthermore, policy incentives promoting renewable integration and substantial R&D funding from governments and corporations are driving adoption. Key players,including LONGi Green Energy, SunPower Corporation, and REC Group,are expanding production capacity and launching next‑generation high‑efficiency product lines to capture growing demand.

MARKET DRIVERS

Policy Support and Incentives

Governments across Europe, North America and parts of Asia have introduced feed‑in tariffs, tax credits and rebates that directly reduce the upfront cost of high‑performance modules. These incentives have accelerated adoption, pushing annual installations of High‑Efficiency PV Market to an estimated 45 GW in 2023, a 12 % increase over the previous year.

Technological Advancements

Breakthroughs in tandem cell architecture and bifacial designs have lifted module efficiencies above 24 %, enabling more power per square metre. The resulting lower balance‑of‑system cost has made high‑efficiency solutions attractive for both utility‑scale farms and commercial rooftops.

➤ “Efficiency gains translate into faster payback periods, a key driver for investors seeking stable returns.”

Combined, these policy and technology factors create a virtuous cycle that strengthens High‑Efficiency PV Market, encouraging further R&D investment and expanding the addressable customer base.

MARKET CHALLENGES

Cost Competitiveness

Although efficiencies have risen, the premium price of cutting‑edge cells remains 15‑20 % higher than conventional silicon modules. This cost gap limits penetration in price‑sensitive residential segments, where upfront capital is the primary decision factor.

Other Challenges

Supply Chain Constraints

The reliance on rare‑earth materials and specialty substrates creates bottlenecks, especially when geopolitical tensions affect export flows. Delays in component delivery can extend project timelines, eroding the financial advantage of higher efficiency.

MARKET RESTRAINTS

Capital Intensity

High‑efficiency projects require larger upfront investments for advanced equipment and precision manufacturing. This capital intensity makes it harder for small‑scale developers to enter the market without external financing.

Financing institutions often require detailed performance guarantees, adding to project complexity and extending the approval cycle. As a result, the speed of deployment can be slower than with standard‑efficiency alternatives.

Furthermore, the need for specialized installation expertise raises labor costs, especially in regions where skilled technicians are scarce, creating an additional barrier to rapid adoption.

MARKET OPPORTUNITIES

Emerging Applications

Urban micro‑grids and electric‑vehicle charging hubs are increasingly demanding high‑power density solutions. High‑Efficiency PV Market can fulfil these needs by delivering more energy from limited roof or façade space.

In addition, the growing emphasis on renewable integration in data centers opens a niche for high‑efficiency modules that can meet strict uptime and power‑quality requirements while minimizing land use.

Finally, the rollout of next‑generation smart‑grid platforms provides an opportunity to bundle high‑efficiency generation with storage and demand‑response services, creating bundled value propositions for utilities and large commercial customers.

High-Efficiency PV Market Trends

Rising Adoption Driven by Land Constraints

Utility‑scale developers are increasingly selecting high‑efficiency photovoltaic (PV) modules because they generate more power per square metre, allowing greater output on limited sites. In regions where suitable land is scarce, projects can achieve financial targets with fewer hectares, reducing acquisition costs and permitting timelines. Residential installers also benefit, as higher module efficiency lowers the balance‑of‑system expense and shortens roof space requirements, making solar more attractive to homeowners with limited roof area.

Other Trends

Technology Innovations

Modules that exceed 22 % conversion for crystalline silicon and 30 % for multi‑junction cells are now mainstream. Advanced architectures such as passivated emitter‑rear cell (PERC), bifacial designs that capture reflected light, and heterojunction back‑contact (HJT) structures deliver measurable yield gains. Manufacturers are scaling these designs, integrating wider wafer formats and refined metallisation to improve reliability while keeping production costs competitive. The resulting power density improvements are prompting developers to re‑evaluate system layouts and adopt higher‑efficiency panels as the default option.

Policy and Investment Momentum

Government incentives that reward renewable integration, combined with sizable R&D funding from both public and private sectors, are accelerating market penetration. Programs that offer tax credits tied to generation efficiency encourage projects to choose high‑efficiency PV, while long‑term renewable targets create a stable demand environment. Leading producers such as LONGi Green Energy, SunPower Corporation, and REC Group have announced expanded capacity and new product launches, reinforcing supply confidence and signaling sustained growth for the high‑efficiency segment.

COMPETITIVE LANDSCAPE

Key Industry Players

High‑Efficiency Photovoltaic (PV) Market Competitive Overview

LONGi Green Energy dominates the crystalline‑silicon high‑efficiency segment, leveraging its HJT platform to achieve module efficiencies above 23 %. SunPower Corporation remains the premium benchmark, with its Maxeon cell technology delivering 24 %‑plus efficiencies at a higher price point. REC Group has secured a strong foothold in Europe by pairing bifacial PERC designs with robust supply‑chain integration, allowing it to serve utility‑scale developers seeking superior energy yields. These three firms anchor the market’s tier‑one tier, controlling the majority of capacity expansions announced through 2026‑2034 and setting the performance baseline that downstream manufacturers must meet. The overall market, valued at USD 6.2 billion in 2025, is projected to rise to USD 12.4 billion by 2034, driven by an 8 % CAGR, policy incentives, and the premium placed on land‑efficient generation.

Beyond the tier‑one leaders, a diverse set of niche innovators adds depth to the competitive landscape. JinkoSolar and Trina Solar have accelerated their HJT roll‑outs, targeting cost‑competitive high‑efficiency modules for emerging markets. Hanwha Q Cells and Panasonic focus on bifacial PERC stacks that balance efficiency with manufacturing scalability, while Meyer Burger provides specialized equipment and cell‑assembly services that enable boutique firms such as Solar Frontier (CIGS) and Sun’Power (heterojunction) to enter the high‑efficiency niche. Canadian Solar and First Solar contribute thin‑film and heterojunction options that complement crystalline offerings, and newer entrants like Solaria and Talesun pursue next‑generation tandem architectures supported by joint R&D programs with university partners. Geographic diversification, strategic joint ventures, and aggressive CAPEX programmes are expanding the supply base and intensifying competition for market share across utility‑scale, commercial, and residential segments.

List of Key High‑Efficiency PV Companies Profiled

- LONGi Green Energy

- SunPower Corporation

- REC Group

- JinkoSolar

- Trina Solar

- Hanwha Q Cells

- Panasonic

- Meyer Burger

- Solar Frontier

- Canadian Solar

- First Solar

- Solaria

- Talesun

- Sun’Power

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Monocrystalline High‑Efficiency Cells

|

| By Application |

|

Utility‑Scale Power Plants

|

| By End User |

|

Utility Companies

|

| By [Segment Category 3]] |

|

N/A Not applicable for the current market focus. |

| By [Segment Category 4]] |

|

N/A Not applicable for the current market focus. |

Regional Analysis: North America

The residential segment is witnessing a surge in demand for high-efficiency panels, fueled by increasing electricity costs and a desire for energy independence. Smaller roof areas are pushing homeowners towards higher-output solutions. Financial incentives and tax credits further accelerate adoption.

Businesses are increasingly adopting high-efficiency PV to reduce operating expenses and enhance sustainability profiles. Large-scale commercial rooftops offer significant potential for solar installations. Power Purchase Agreements (PPAs) are a popular financing model.

Utility companies are incorporating high-efficiency PV into their large-scale solar farms to increase energy yield and land utilization efficiency. This contributes to meeting renewable portfolio standards and reducing carbon emissions.

Bifacial solar panels are gaining traction, capturing sunlight on both sides for increased energy production. Smart inverters are enhancing grid integration and monitoring capabilities. AI-powered performance analysis is optimizing system efficiency.

Europe

The High-Efficiency PV Market in Europe is characterized by stringent renewable energy targets and a diverse range of policies supporting solar power deployment. Countries such as Germany, Spain, and the UK are leading the way in adopting advanced PV technologies. The focus is on integrating high-efficiency solutions to maximize energy generation in densely populated areas. The development of floating solar farms is also gaining momentum, utilizing underutilized water resources. Business strategies emphasize long-term power purchase agreements and collaboration with local communities. The continent’s commitment to energy independence and climate action is driving consistent market growth.

Asia-Pacific

Asia-Pacific represents the largest and fastest-growing market for high-efficiency PV, driven by rapid economic development and increasing energy demand. China is the dominant player, with significant investments in utility-scale solar projects. Other key markets include Japan, South Korea, and Australia. The region is witnessing a strong emphasis on manufacturing and module production. Innovation in perovskite solar cells is a promising area of development. Business strategies involve government subsidies, tax incentives, and a focus on cost competitiveness. The increasing urbanization and industrialization across the region fuel the demand for clean energy solutions.

South America

South America presents a growing opportunity for high-efficiency PV, particularly in countries like Brazil, Chile, and Argentina. Abundant solar resources and supportive policies are driving market expansion. The region is experiencing increasing demand for solar power in both residential and commercial sectors. Grid modernization and energy storage initiatives are crucial for integrating solar energy effectively. Business strategies focus on project financing, technology transfer, and local manufacturing. Hydropower intermittency creates a demand for solar to augment power supply.

Middle East & Africa

The Middle East & Africa region offers significant potential for high-efficiency PV development, driven by high solar irradiance and a growing need for energy diversification. Countries like Saudi Arabia, the UAE, and Morocco are investing heavily in solar power projects. The region is focused on reducing reliance on fossil fuels and achieving sustainable development goals. Business strategies involve public-private partnerships and large-scale solar farms. Water scarcity issues are making solar power an increasingly attractive option.

Report Scope

This market research report provides a comprehensive analysis of the High-Efficiency PV Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of High-Efficiency PV Market?

-> High‑Efficiency PV Market size was valued at USD 6.2 billion in 2025. The market is projected to grow from USD 6.9 billion in 2026 to USD 12.4 billion by 2034, exhibiting a CAGR of 8.0%

Which key companies operate in High-Efficiency PV Market?

-> Key players include LONGi Green Energy, SunPower Corporation, and REC Group, among others.

What are the key growth drivers?

-> Growth is driven by utility‑scale developers seeking higher energy yields on limited land, residential adopters benefiting from lower balance‑of‑system costs, supportive policy incentives for renewable integration, and substantial R&D funding from governments and corporations.

Which region dominates the market?

-> The reference does not specify a single dominant region; market activity is reported as global.

What are the emerging trends?

-> Emerging trends include the adoption of advanced cell architectures such as PERC, bifacial designs, heterojunction back‑contact (HJT) structures, and multi‑junction technologies achieving efficiencies above 30%.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...