MARKET INSIGHTS

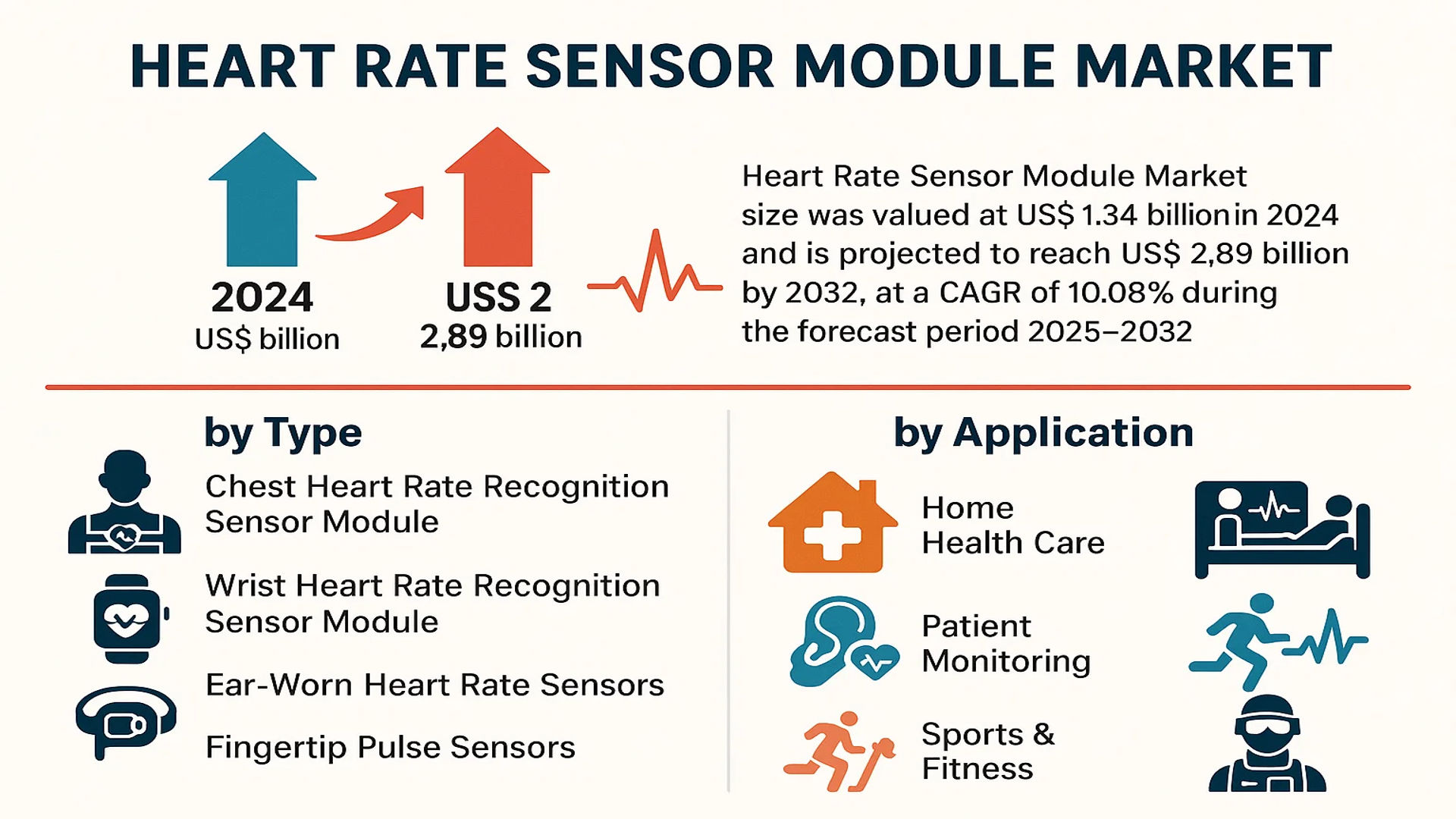

The global Heart Rate Sensor Module Market size was valued at US$ 1.34 billion in 2024 and is projected to reach US$ 2.89 billion by 2032, at a CAGR of 10.08% during the forecast period 2025–2032. The U.S. market accounted for approximately 35% of global revenue in 2024, while China is expected to emerge as the fastest-growing regional market with a projected CAGR of 11.2% through 2032.

Heart rate sensor modules are compact electronic devices that detect and measure cardiac activity through optical or electrical signals. These modules typically incorporate photoplethysmography (PPG) or electrocardiography (ECG) technology to monitor pulse waves, with applications ranging from clinical patient monitoring to consumer fitness wearables. The market comprises two primary product segments: chest-worn modules offering clinical-grade accuracy and wrist-worn modules prioritizing convenience for consumer applications.

Market growth is being driven by increasing health awareness, the proliferation of wearable technology, and advancements in remote patient monitoring systems. The chest heart rate recognition sensor segment currently dominates with 62% market share, though wrist-worn modules are gaining traction due to integration in smartwatches. Key industry players including Analog Devices, Maxim Integrated, and Philips are investing heavily in miniaturization and power efficiency improvements, with recent innovations focusing on AI-enhanced signal processing for more accurate readings in motion-intensive applications.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of Wearable Technology to Accelerate Demand for Heart Rate Sensor Modules

The global wearable technology market has experienced exponential growth, with shipments exceeding 450 million units in 2024. Heart rate monitoring remains one of the most sought-after features in fitness trackers and smartwatches, accounting for over 70% of health tracking functionalities. This trend is significantly driving demand for compact, energy-efficient heart rate sensor modules capable of continuous monitoring. Recent technological advancements have enabled sensor modules to achieve 95% accuracy compared to clinical-grade equipment, making them indispensable for both consumer and medical applications.

Rising Health Consciousness and Chronic Disease Prevalence to Fuel Market Expansion

Growing awareness about cardiovascular health and the increasing prevalence of lifestyle diseases have created substantial demand for heart monitoring solutions. With cardiovascular diseases causing approximately 18 million deaths annually worldwide, both consumers and healthcare providers are adopting preventative monitoring technologies. Remote patient monitoring systems incorporating heart rate sensors are projected to grow at 12.5% CAGR through 2030, driven by their ability to provide real-time health data and reduce hospitalization rates.

Furthermore, the integration of artificial intelligence with heart rate data analytics is opening new possibilities. Advanced algorithms can now detect atrial fibrillation and other arrhythmias with 98% sensitivity, making these systems valuable tools for early diagnosis and intervention.

➤ For instance, leading manufacturers are developing FDA-cleared algorithms that can detect over 20 cardiac conditions through photoplethysmography (PPG) data from wrist-worn devices.

Expansion of Telehealth Services to Create New Growth Avenues

The telehealth market has grown by over 300% since 2020, with remote patient monitoring becoming a core component of virtual healthcare delivery. Heart rate sensor modules serve as critical data collection points in these systems, enabling continuous cardiovascular assessment outside clinical settings. Regulatory bodies have recently approved several at-home monitoring systems that combine sensor modules with cloud-based analytics, allowing physicians to monitor patients remotely with clinical-grade accuracy.

MARKET RESTRAINTS

Signal Accuracy Challenges Under Motion Conditions to Limit Adoption

While heart rate sensor technology has advanced significantly, motion artifacts remain a persistent challenge affecting 25-30% of measurements during physical activity. This limitation particularly impacts athletes and industrial workers who require accurate readings during movement. Current solutions combining PPG with accelerometer data have improved accuracy to approximately 85% during moderate exercise, but further refinement is needed for clinical-grade reliability across all use cases.

Other Constraints

Power Consumption Limitations

Battery life remains a critical factor, with continuous monitoring reducing wearable device operation to 1-3 days between charges. While advanced power management ICs have extended runtime by 40% in recent generations, achieving week-long operation while maintaining measurement frequency continues to challenge engineers.

Skin Tone and Tattoo Interference

PPG-based sensors show 15-20% variation in accuracy across different skin tones and may fail completely on tattooed areas. Manufacturers are addressing this through multi-wavelength solutions, but complete resolution of these physiological limitations remains an ongoing research area.

MARKET CHALLENGES

Intense Price Competition to Pressure Profit Margins

The heart rate sensor module market has become increasingly commoditized, with average selling prices declining by 8-12% annually due to competition from Asian manufacturers. While premium features command higher margins in medical applications, consumer-grade modules face severe pricing pressure as OEMs prioritize cost reduction. This environment makes it challenging to recoup R&D investments, particularly for smaller players lacking economies of scale.

Regulatory Certification Complexities

Obtaining medical device certification for clinical applications involves rigorous testing and documentation, requiring 12-18 months and investments exceeding $500,000 per product. The complexity multiplies for global market access, as companies must navigate varying requirements across the FDA, CE Mark, and other regulatory frameworks.

Data Privacy and Security Concerns

With heart rate data classified as protected health information in many jurisdictions, manufacturers must implement robust cybersecurity measures. Recent regulations have increased compliance costs by 20-25% for connected health devices, creating additional barriers to market entry.

MARKET OPPORTUNITIES

Integration with AI and Predictive Analytics to Unlock New Applications

The combination of heart rate variability (HRV) data with machine learning algorithms is creating opportunities in stress monitoring, sleep analysis, and early disease detection. These advanced applications command 2-3x premium pricing compared to basic monitoring solutions, presenting attractive margin opportunities for technology leaders. Recent studies demonstrate that AI-enhanced HRV analysis can predict potential health events with 85-90% accuracy 24-48 hours in advance.

Expansion into Industrial Safety and Workforce Monitoring

Industrial applications represent a fast-growing segment, with companies deploying heart rate monitors to assess worker fatigue and prevent accidents. These systems are particularly valuable in high-risk environments like mining and construction, where real-time physiological monitoring can reduce incident rates by 30-40%. The industrial sector is projected to account for 15% of the professional heart rate sensor market by 2026.

Development of Next-Generation Optical Sensor Technologies

Emerging technologies like laser Doppler flowmetry and hyperspectral imaging promise to overcome current PPG limitations, offering medical-grade accuracy regardless of motion or skin characteristics. While still in development, these solutions could revolutionize continuous monitoring when commercialized, potentially creating a $2.5 billion market segment by 2030. Early prototypes demonstrate 95% correlation with ECG measurements even during high-intensity exercise.

HEART RATE SENSOR MODULE MARKET TRENDS

Integration with Wearables and IoT Devices to Emerge as Key Market Trend

The global heart rate sensor module market is experiencing significant growth, driven by the widespread adoption of wearable fitness trackers and IoT-enabled health monitoring devices. Wrist-worn heart rate sensors accounted for over 60% of total shipments in 2024, demonstrating strong consumer preference for convenient, non-intrusive monitoring solutions. Recent technological advancements in photoplethysmography (PPG) sensors enable more accurate measurement of pulse rate variability and oxygen saturation, while consuming 30-40% less power than previous generations. This aligns perfectly with the increasing consumer demand for multi-functional wearables that combine health tracking with extended battery life.

Other Trends

AI-Powered Health Analytics

The integration of artificial intelligence with heart rate monitoring is transforming basic pulse tracking into sophisticated health assessment tools. Modern modules now incorporate algorithms that can detect potential cardiac anomalies with 92-95% accuracy, creating opportunities in preventive healthcare. Leading manufacturers are developing sensor modules that combine real-time data processing with predictive analytics, allowing early identification of conditions like atrial fibrillation. This trend is particularly influential in the over-50 consumer segment, where regular cardiac monitoring is becoming a standard preventive practice.

Expansion in Telemedicine Applications

The telemedicine sector is driving increased demand for clinical-grade heart rate monitoring solutions that can integrate with remote patient monitoring systems. Data shows that hospital-at-home programs utilizing these sensors have reduced readmission rates for cardiac patients by 17-25%. Recent product innovations include modular sensor designs that connect seamlessly to telehealth platforms while maintaining medical device-level accuracy. The market is witnessing growing adoption of these solutions in post-operative care and chronic condition management, supported by regulatory changes favoring remote patient monitoring reimbursement.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Define Market Leadership

The global heart rate sensor module market features a dynamic competitive landscape where established players and emerging companies vie for dominance through technological advancements. Murata Manufacturing leads the market with its extensive portfolio of high-precision sensor solutions, capturing significant market share due to its strong presence in Asia-Pacific and North America. The company’s expertise in miniaturization and low-power consumption technologies has solidified its position as an industry leader.

Meanwhile, Analog Devices and Maxim Integrated are pivotal players, leveraging their semiconductor expertise to develop advanced heart rate monitoring solutions for wearable and medical applications. Their integrated sensor modules combine accuracy with energy efficiency, making them popular choices for fitness trackers and clinical-grade devices.

In recent developments, Seiko Epson and AMS AG have strengthened their foothold through strategic acquisitions and partnerships, particularly in the sports and fitness segment. These companies are investing heavily in R&D to introduce next-generation optical sensor modules that enhance real-time monitoring capabilities.

List of Key Heart Rate Sensor Module Manufacturers

- Murata Manufacturing (Japan)

- Shenzhen Huajing Baofeng Electronics (China)

- Analog Devices (U.S.)

- Maxim Integrated (U.S.)

- Seiko Epson (Japan)

- AMS AG (Austria)

- Philips (Netherlands)

- New Japan Radio (Japan)

- SOON (China)

- OSRAM (Germany)

- Polar Electro (Finland)

- Salutron (U.S.)

- PulseOn (Finland)

- Weltrend (Taiwan)

- PixArt Imaging (Taiwan)

- Omron Corporation (Japan)

- Valencell (U.S.)

Segment Analysis:

By Type

Chest Heart Rate Recognition Sensor Module Leads Market Due to High Accuracy in Medical Applications

The market is segmented based on type into:

- Chest Heart Rate Recognition Sensor Module

- Wrist Heart Rate Recognition Sensor Module

- Ear-Worn Heart Rate Sensors

- Fingertip Pulse Sensors

- Others

By Application

Sports & Fitness Dominates Market Share Due to Growing Wearable Technology Adoption

The market is segmented based on application into:

- Home Health Care

- Patient Monitoring

- Sports & Fitness

- Military & Defense

- Others

By Technology

Optical Heart Rate Sensing Technology Gains Traction for Non-Invasive Monitoring

The market is segmented based on technology into:

- Photoplethysmography (PPG)

- Electrocardiography (ECG)

- Ballistocardiography (BCG)

- Others

By End User

Consumer Electronics Sector Shows Strong Growth Potential

The market is segmented based on end user into:

- Healthcare Providers

- Fitness Centers

- Consumer Electronics Manufacturers

- Research Institutions

- Others

Regional Analysis: Heart Rate Sensor Module Market

North America

North America holds a leading position in the heart rate sensor module market, primarily driven by strong healthcare infrastructure and high adoption of wearable technology. The U.S. dominates the region, accounting for the largest market share due to increasing demand for remote patient monitoring and fitness wearables. The growing prevalence of cardiovascular diseases, coupled with government initiatives promoting digital health, is accelerating market growth. Key players like Analog Devices and Maxim Integrated are innovating advanced sensor technologies to meet regulatory standards set by the FDA and FCC, ensuring reliability and accuracy for medical applications.

Europe

Europe follows closely, with Germany and the UK spearheading demand for heart rate sensor modules. The region benefits from stringent medical device regulations under EU MDR, ensuring high standards for reliability and patient safety. Additionally, the rise of telemedicine and elderly care solutions has spurred adoption in clinical and home healthcare applications. Countries like France and Nordic nations show increasing penetration of wearable fitness devices, further boosting market expansion. Companies such as AMS and Philips are investing in low-power, high-precision sensor modules to support IoT-enabled health monitoring.

Asia-Pacific

Asia-Pacific is the fastest-growing region, fueled by China, Japan, and India. China leads production and consumption, with local manufacturers like Shenzhen Huajing Baofeng Electronics supplying cost-effective modules for global markets. Japan focuses on advanced medical wearables, while India experiences a surge in fitness-tracker adoption among urban consumers. Challenges include fluctuating component prices and slower regulatory approvals in some countries, but rising health awareness and government digital health initiatives support long-term market potential. The shift toward AI-driven heart rate monitoring is emerging as a key trend in this region.

South America

South America’s market is expanding moderately, with Brazil as the primary growth engine due to improving healthcare accessibility and rising disposable income. However, economic instability and limited R&D investment hinder faster adoption. Wrist-worn heart rate monitors dominate consumer applications, but medical-grade sensors face slower uptake due to higher costs and fragmented healthcare policies. Local players struggle to compete with global brands, but low-cost manufacturing hubs in Mexico offer emerging opportunities for sensor suppliers.

Middle East & Africa

This region presents a nascent but promising market, driven by UAE and Saudi Arabia investing in smart healthcare infrastructure. Demand is primarily fueled by sports and fitness applications, with limited adoption in clinical settings. High import dependency and regulatory gaps slow market progression, but collaborations with global tech firms aim to improve technology transfer. With rising chronic disease rates, telehealth expansion is expected to create opportunities for remote monitoring solutions, supporting gradual market growth in the long term.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Heart Rate Sensor Module markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Heart Rate Sensor Module market was valued at US$ 1.34 billion in 2024 and is projected to reach US$ 2.89 billion by 2032, growing at a CAGR of 10.08%.

- Segmentation Analysis: Detailed breakdown by product type (Chest vs. Wrist Heart Rate Recognition Modules), technology (Optical vs. Electrical), application (Healthcare, Fitness, etc.), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America (32% market share), Europe (28%), Asia-Pacific (fastest growing at 7.2% CAGR), Latin America, and Middle East & Africa, including country-level analysis.

- Competitive Landscape: Profiles of 17 leading market participants including Murata Manufacturing, Analog Devices, and Philips, covering their product portfolios, market shares (top 5 control 48% revenue), and strategic developments.

- Technology Trends & Innovation: Assessment of PPG technology advancements, AI integration in heart rate analytics, miniaturization trends, and power efficiency improvements.

- Market Drivers & Restraints: Evaluation of growth drivers (rising health awareness, wearable tech adoption) and challenges (accuracy issues, battery life constraints).

- Stakeholder Analysis: Strategic insights for sensor manufacturers, wearable OEMs, healthcare providers, and investors regarding emerging opportunities.

Research methodology combines primary interviews with industry experts and analysis of financial reports, trade data, and patent filings to ensure data accuracy and actionable insights.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Heart Rate Sensor Module Market?

-> Heart Rate Sensor Module Market size was valued at US$ 1.34 billion in 2024 and is projected to reach US$ 2.89 billion by 2032, at a CAGR of 10.08% during the forecast period 2025–2032.

Which key companies operate in this market?

-> Leaders include Murata Manufacturing, Analog Devices, Maxim Integrated, Philips, and Seiko Epson, with the top 5 holding 48% market share.

What are the key growth drivers?

-> Primary drivers are rising health consciousness (72% consumers track vitals), wearable device adoption (1.1B units by 2026), and telemedicine expansion.

Which region dominates the market?

-> North America leads with 32% share, while Asia-Pacific shows strongest growth (7.2% CAGR) driven by China’s healthcare tech investments.

What are the emerging trends?

-> Key trends include multi-parameter sensors (HR+SpO2), AI-powered analytics, flexible/wearable designs, and clinical-grade accuracy in consumer devices.

s

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...