MARKET INSIGHTS

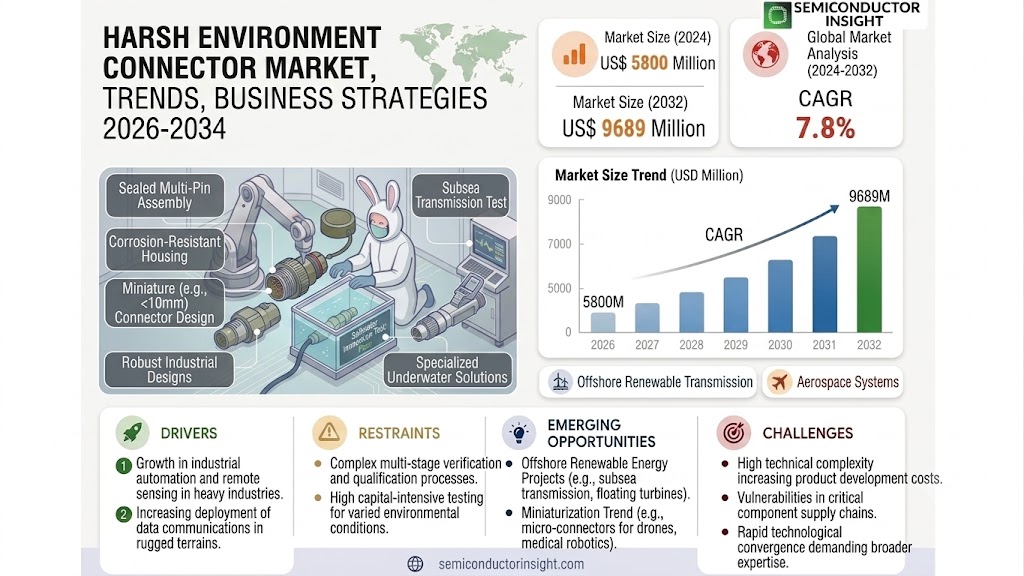

The global Harsh Environment Connector Market was valued at 5800 million in 2024 and is projected to reach US$ 9689 million by 2032, at a CAGR of 7.8% during the forecast period.

Harsh environment connectors are specialized electromechanical components designed to maintain reliable performance under extreme conditions. These ruggedized solutions feature durable housings that protect against moisture ingress, dust contamination, chemical exposure, mechanical stress, and temperature fluctuations. Common variants include circular connectors, rectangular connectors, and fiber optic connectors – each engineered for specific industrial requirements.

The market growth is driven by increasing automation in manufacturing, expanding renewable energy infrastructure, and stringent reliability requirements in defense applications. Recent technological advancements in material science have enabled connectors to withstand temperatures ranging from -65°C to +200°C while maintaining IP68/IP69K ratings for water resistance. Leading manufacturers like TE Connectivity and Amphenol are developing compact, high-density solutions to meet space constraints in modern equipment designs. The telecommunications sector shows particular promise, with 5G network expansion creating demand for weatherproof fiber optic connections in outdoor small cell deployments.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Industrial Automation and Energy Sector Investments Accelerate Demand

The rapid adoption of industrial automation across manufacturing plants, oil & gas facilities, and renewable energy projects is significantly boosting the harsh environment connector market. With global industrial automation investments projected to grow at over 8% annually, the need for reliable connectivity solutions in extreme conditions has intensified. These connectors ensure uninterrupted data transmission and power supply in environments with high vibration, moisture, and temperature fluctuations – critical for maintaining operational efficiency in automated systems. The energy sector, particularly offshore wind farms and solar power installations, represents another major growth driver, with deployment of harsh environment connectors increasing by 12-15% year-over-year in renewable energy applications.

Military Modernization Programs Fuel Aerospace & Defense Segment Growth

Defense budgets worldwide are increasingly allocating funds to modernization initiatives, creating substantial demand for ruggedized connectivity solutions. Military applications account for approximately 28-30% of the harsh environment connector market, driven by the need for fail-safe performance in extreme battlefield conditions. Recent contracts for next-generation fighter jets, unmanned systems, and naval vessels often specify military-grade connectors that meet stringent MIL-DTL-38999 or MIL-DTL-5015 standards. The aerospace sector similarly requires connectors that can withstand altitude variations, electromagnetic interference, and mechanical stress – factors contributing to the segment’s projected 6.5% CAGR through 2032.

5G Infrastructure Rollout Drives Telecommunications Adoption

The global transition to 5G networks is creating unprecedented demand for outdoor-rated connectivity solutions capable of withstanding environmental challenges. Telecom operators are deploying harsh environment fiber optic connectors at a rapid pace to support small cell installations and tower equipment in varied climates. These connectors must maintain signal integrity despite temperature extremes ranging from -40°C to +85°C while resisting moisture ingress – specifications that standard commercial connectors cannot meet. With over 3 million 5G base stations expected to be operational worldwide by 2025, the telecommunications segment is emerging as one of the fastest-growing application areas for specialized connectivity solutions.

MARKET RESTRAINTS

High Product Costs and Extended Qualification Processes Limit Market Penetration

While demand grows across industries, the premium pricing of harsh environment connectors remains a significant barrier for cost-sensitive applications. These specialized components typically carry 3-5 times the price premium of standard industrial connectors due to advanced materials like nickel-plated bronze or stainless steel housings and sophisticated sealing technologies. Moreover, the qualification process for harsh environment certification (including IP68/69K, NEMA 6P, or MIL-SPEC standards) can extend to 12-18 months, delaying time-to-market for equipment manufacturers. These factors collectively restrain adoption in price-sensitive market segments, particularly in developing economies where cost considerations often outweigh environmental durability requirements.

Supply Chain Disruptions Impact Component Availability

The market continues facing challenges from persistent supply chain bottlenecks affecting specialty metals and electronic components. Nickel, a critical material for corrosion-resistant connector housings, has experienced supply volatility with prices fluctuating by 35-40% in recent years. This instability creates pricing uncertainty and extended lead times for finished products, particularly impacting smaller manufacturers with limited inventory buffers. The aerospace and defense sectors have been especially vulnerable, where single-source components and stringent qualification requirements make supplier diversification challenging. These disruptions have prompted some end-users to delay equipment upgrades or seek alternative connectivity solutions, temporarily slowing market growth.

MARKET OPPORTUNITIES

Offshore Renewable Energy Projects Create New Application Frontiers

The accelerating development of offshore wind farms presents significant growth opportunities, with installations requiring connectors that withstand saltwater immersion, high pressures, and extreme weather conditions. Floating wind turbines, in particular, demand connectors with enhanced resistance to dynamic mechanical stresses and deep-water pressures. As global offshore wind capacity is projected to increase sevenfold by 2030, connector solutions tailored for subsea transmission systems and turbine-to-grid interfaces are becoming increasingly vital. Manufacturers investing in specialized underwater connector technologies capable of 20+ year service life in marine environments stand to capture substantial market share in this emerging segment.

Miniaturization Trend Opens New Design Possibilities

Advancements in connector miniaturization are enabling previously impossible applications in medical robotics, drone systems, and wearable industrial devices. The development of micro- and nano-style harsh environment connectors with current ratings up to 8A in packages smaller than 10mm diameter addresses space-constrained applications. This technological evolution allows equipment designers to maintain environmental protection while reducing weight and footprint – critical factors in aerospace and portable medical devices. Companies developing innovative sealing techniques for miniature connectors at competitive price points are well-positioned to capitalize on the growing demand for compact yet durable interconnection solutions.

MARKET CHALLENGES

Technical Complexity Increases Product Development Costs

The escalating performance requirements for harsh environment connectors are driving up R&D expenditures across the industry. New applications in electric vehicle charging (requiring 1000V+ ratings), aerospace (demanding aluminum alloy housings), and industrial IoT (needing embedded sensors) are pushing connector technology beyond traditional boundaries. Developing solutions that combine high-voltage capability with environmental sealing and data transmission often requires multi-disciplinary engineering teams and extensive prototype testing. These technical hurdles translate to development cycles extending 24-36 months for next-generation products, straining R&D budgets and delaying market entry for innovative solutions.

Counterfeit Components Pose Reliability Risks

The market faces growing challenges from counterfeit connectors that mimic military and industrial specifications but fail under actual operating conditions. These imitation products, often originating from unauthorized suppliers, compromise system reliability in critical applications ranging from aircraft avionics to nuclear power plants. Industry studies indicate counterfeit electrical components account for approximately 5-7% of aftermarket replacements in harsh environment applications, representing a serious safety concern. Combating this issue requires enhanced supply chain visibility and authentication technologies, adding operational complexity for legitimate manufacturers striving to maintain product integrity while competing on price.

HARSH ENVIRONMENT CONNECTOR MARKET TRENDS

Increasing Demand for Ruggedized Connectivity Solutions in Industrial and Aerospace Sectors

The harsh environment connector market is experiencing robust growth, driven by the rising need for durable connectivity solutions in extreme operating conditions. These connectors are engineered to withstand extreme temperatures, moisture, vibrations, and corrosive elements, making them indispensable in industries like industrial automation, aerospace, and defense. In 2024, the global market was valued at $5800 million, with projections indicating it will reach $9689 million by 2032, growing at a CAGR of 7.8%. The aerospace and military segment alone accounts for over 35% of market revenues due to stringent durability requirements in defense applications. The industrial sector follows closely, driven by automation and machinery operating in challenging environments.

Other Trends

Expansion in Renewable Energy Applications

The transition toward renewable energy sources has amplified the adoption of harsh environment connectors in wind turbines, solar farms, and offshore energy installations. These connectors must endure salt mist, humidity, and dynamic loads—common challenges in coastal and marine settings. Wind turbine installations, which exceeded 59 GW globally in 2023, heavily rely on high-performance fiber-optic and circular connectors for reliable data and power transmission. Additionally, increasing investments in smart grid infrastructure further propel demand for ruggedized connectors capable of functioning in extreme climates.

Technological Innovations Enhancing Durability and Performance

Connector manufacturers are focusing on materials science to improve resilience against harsh conditions. Advancements in sealing technologies, such as IP69K-rated connectors for high-pressure washdown environments, are becoming industry standards. Leading players like TE Connectivity and Amphenol are developing hybrid solutions that combine electrical, optical, and fluid transfer capabilities within a single ruggedized housing. Furthermore, the integration of lightweight alloys and composite materials ensures connectors meet aerospace requirements without compromising mechanical strength. These innovations are critical as industries demand smaller, yet more robust, connectors for next-generation applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Ruggedization and Reliability Drive Strategic Positioning in Harsh Environment Connector Market

The harsh environment connector market features a moderately consolidated competitive landscape, with established global players competing alongside specialized regional manufacturers. TE Connectivity and Amphenol Corporation dominate the market through their extensive product portfolios and robust distribution networks across aerospace, industrial, and energy sectors. These market leaders collectively held over 30% revenue share in 2024, leveraging their technological expertise in sealing technologies and material science.

Huber+Suhner has emerged as a key innovator in fiber optic connectors for extreme conditions, particularly in telecommunications infrastructure and renewable energy applications. Their recent RADOX® series connectors, capable of withstanding temperatures from -55°C to 125°C, have gained significant traction in offshore wind farm projects across Northern Europe.

Mid-tier players like ITT Cannon and Staubli are focusing on niche applications—ITT’s D-Sub connectors for military avionics and Staubli’s CombiTac modular system for factory automation demonstrate how specialized solutions create competitive advantages. Both companies are investing heavily in miniaturization technologies to address space-constrained applications in medical devices and unmanned systems.

The market also sees strong competition from component specialists. Glenair differentiates through its Mighty Mouse micro-miniature connectors, while Lemo dominates in broadcast and medical applications with its push-pull connector systems. Eaton’s recent acquisition of TriMark Corporation signals increasing consolidation as companies seek to broaden their harsh environment solutions portfolios.

Regional dynamics influence competition significantly—Molex and Smiths Interconnect maintain strong positions in North America’s oil & gas sector, whereas Diamond SA leads in European railway applications. Meanwhile, Optical Cable Corporation is expanding aggressively in Middle Eastern markets, particularly for infrastructure projects in desert environments.

List of Key Harsh Environment Connector Manufacturers

- TE Connectivity (Switzerland)

- Amphenol Corporation (U.S.)

- Huber+Suhner (Switzerland)

- ITT Cannon (U.S.)

- Staubli (Switzerland)

- Glenair (U.S.)

- Lemo (Switzerland)

- Eaton (Ireland)

- Molex (U.S.)

- Smiths Interconnect (U.K.)

- Diamond SA (Switzerland)

- Optical Cable Corporation (U.S.)

Segment Analysis:

By Type

Circular Connector Segment Dominates the Market Due to High Durability and Reliability in Extreme Conditions

The market is segmented based on type into:

- Circular Connector

- Subtypes: IP68-rated, waterproof, and high-temperature resistant variants

- Rectangular Connector

- Fiber Optic Connector

By Application

Aerospace & Military Segment Leads Due to Stringent Requirements for Rugged Connectivity

The market is segmented based on application into:

- Aerospace & Military

- Industrial

- Telecommunications

- Medical

- Energy

By Environment

Underwater Applications Drive Demand for Sealed and Corrosion-Resistant Connectors

The market is segmented based on environmental conditions into:

- Extreme Temperature Zones

- High-Vibration Environments

- Underwater/Subsea Applications

- Corrosive Chemical Environments

By Material

High-Performance Polymer Composites Gain Preference for Lightweight and Durable Solutions

The market is segmented based on material composition into:

- Stainless Steel

- Titanium Alloys

- High-Performance Polymers

- Nickel Plated Brass

Regional Analysis: Harsh Environment Connector Market

North America

The North American market for harsh environment connectors is driven by stringent industrial standards and robust demand from aerospace, defense, and energy sectors. The region—particularly the U.S.—hosts key players like TE Connectivity, Amphenol, and Molex, which dominate innovation in ruggedized connectors. The U.S. Department of Defense’s focus on military modernization, with contracts exceeding $50 billion annually for avionics and naval systems, fuels demand for high-reliability connectors. Additionally, expanding 5G infrastructure and renewable energy projects in wind and solar farms further propel market growth, supported by regulatory frameworks ensuring product durability and environmental resistance.

Europe

Europe’s market thrives on its advanced industrial base and strict EU directives on product safety and performance, such as the ATEX certification for explosive environments. Countries like Germany and France lead in industrial automation and automotive applications, where connectors must withstand extreme temperatures and vibrations. The offshore wind sector, especially in the North Sea, is a significant driver, with projects like Dogger Bank Wind Farm requiring connectors resistant to saltwater corrosion. However, high manufacturing costs and competition from亚洲供应商pose challenges to local manufacturers, pushing them to prioritize premium, high-value solutions.

Asia-Pacific

As the fastest-growing region, Asia-Pacific benefits from massive infrastructure development and manufacturing hubs in China, Japan, and India. China’s “Made in China 2025” initiative emphasizes self-sufficiency in high-tech components, boosting domestic connector production for railways, telecom, and energy. India’s expanding urban infrastructure and Japan’s precision electronics industry further contribute to demand. While cost-efficient solutions dominate, rising investments in aerospace (e.g., India’s defense procurement) are shifting focus toward higher-grade connectors. Nonetheless, price sensitivity and fragmented supply chains create hurdles for standardized quality adoption.

South America

The market here is emerging, with Brazil and Argentina driving demand through oil & gas and mining sectors, where connectors face harsh conditions like dust and humidity. However, economic instability and reliance on imports limit local manufacturing. Recent offshore oil discoveries, such as Brazil’s pre-salt basins, offer growth potential, but bureaucratic delays and underdeveloped infrastructure slow market expansion. Partnerships with global firms like Eaton and ITT Cannon are critical to bridging technology gaps.

Middle East & Africa

Growth is concentrated in Gulf Cooperation Council (GCC) countries, where oil refineries and desalination plants demand corrosion-resistant connectors. The UAE’s focus on smart cities and Saudi Arabia’s Vision 2030 projects present opportunities, but the market remains constrained by geopolitical risks and a lack of local expertise. Africa’s mining sector shows promise, though inconsistent regulations and limited investment in harsh-environment applications hinder progress.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Harsh Environment Connector markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Harsh Environment Connector market was valued at USD 5,800 million in 2024 and is projected to reach USD 9,689 million by 2032, growing at a CAGR of 7.8%.

- Segmentation Analysis: Detailed breakdown by product type (Circular, Rectangular, Fiber Optic Connectors), application (Aerospace & Military, Industrial, Telecommunications, Medical, Energy), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. and China are key markets, with Asia-Pacific showing the fastest growth.

- Competitive Landscape: Profiles of leading market participants including Huber+Suhner, Amphenol, TE Connectivity, ITT Cannon, and Smiths Interconnect, covering their product portfolios, market share, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging connector technologies, materials innovation, and evolving industry standards for harsh environment applications.

- Market Drivers & Restraints: Evaluation of factors such as increasing industrial automation, growing defense expenditures, and infrastructure development versus supply chain challenges and material costs.

- Stakeholder Analysis: Strategic insights for connector manufacturers, OEMs, system integrators, and investors regarding market opportunities and competitive positioning.

The report combines primary research (industry expert interviews) with comprehensive secondary research and data validation to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Harsh Environment Connector Market?

-> Harsh Environment Connector Market was valued at 5800 million in 2024 and is projected to reach US$ 9689 million by 2032, at a CAGR of 7.8% during the forecast period.

Which key companies operate in Global Harsh Environment Connector Market?

-> Key players include Huber+Suhner, Amphenol Communications Solutions, TE Connectivity, ITT Cannon, Smiths Interconnect, and Glenair, among others.

What are the key growth drivers?

-> Key growth drivers include increasing industrial automation, growing defense and aerospace investments, expansion of renewable energy projects, and rising demand for ruggedized connectivity solutions.

Which region dominates the market?

-> North America currently holds the largest market share, while Asia-Pacific is expected to witness the highest growth rate during the forecast period.

What are the emerging trends?

-> Emerging trends include miniaturization of connectors, development of hybrid connector solutions, increased use of composite materials, and integration of smart monitoring capabilities.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...