MARKET INSIGHTS

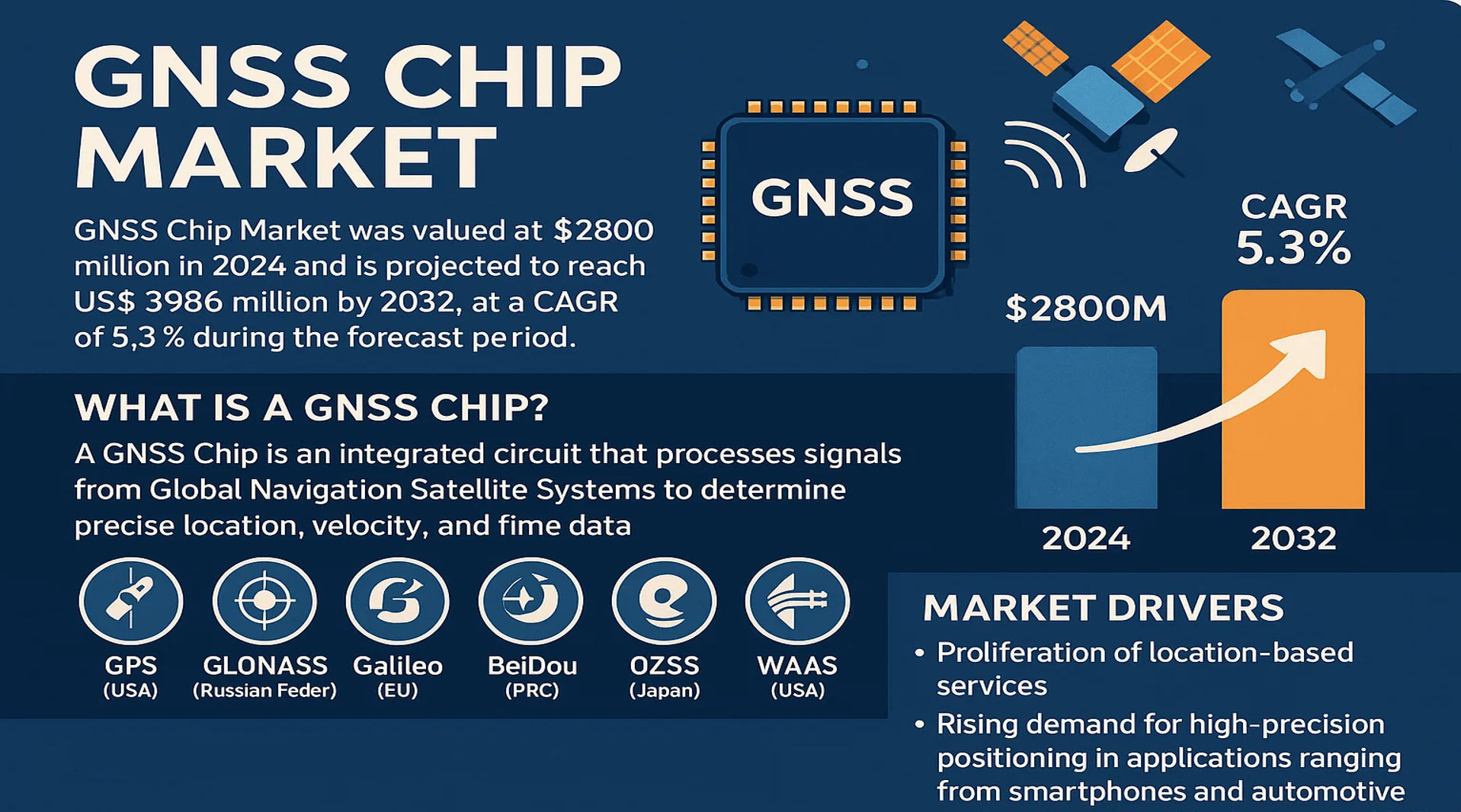

The global GNSS Chip Market was valued at 2800 million in 2024 and is projected to reach US$ 3986 million by 2032, at a CAGR of 5.3% during the forecast period.

A GNSS Chip is an integrated circuit that processes signals from Global Navigation Satellite Systems to determine precise location, velocity, and time data. These chips are fundamental components in a vast array of devices, enabling them to interface with constellations such as GPS (USA), GLONASS (Russian Federation), Galileo (EU), and BeiDou (PRC). The technology also leverages regional systems like QZSS (Japan) and augmentation systems including WAAS (USA) and EGNOS (EU) to enhance accuracy and reliability.

Market expansion is primarily driven by the proliferation of location-based services and the rising demand for high-precision positioning in applications ranging from smartphones and automotive systems to wearable devices and the Internet of Things (IoT). China dominates the market, holding approximately 45% of the global share, largely because of its massive consumer electronics manufacturing base and the widespread adoption of the BeiDou system. Furthermore, the Standard Precision GNSS Chips segment leads the product category, accounting for nearly 70% of the market, due to their cost-effectiveness and suitability for high-volume consumer applications like smartphones, which represent the largest application segment.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of Smartphones and IoT Devices to Accelerate Market Expansion

The global smartphone market, exceeding 1.4 billion units shipped annually, remains the primary driver for GNSS chip demand, accounting for approximately 60% of total consumption. The integration of high-precision location services for navigation, ride-hailing, and augmented reality applications necessitates advanced GNSS chipsets in every device. Furthermore, the explosive growth of the Internet of Things (IoT), projected to connect over 29 billion devices by 2030, is creating unprecedented demand for low-power, high-accuracy positioning solutions. Asset tracking, smart agriculture, and logistics rely heavily on GNSS technology for real-time location data, fueling consistent market growth. The convergence of 5G connectivity with GNSS enhances positioning accuracy and reliability, particularly in urban environments, further embedding these chips as critical components in modern connected devices.

Advancements in Automotive and Autonomous Driving Technologies to Propel Demand

The automotive sector represents a high-growth segment for GNSS chips, driven by the rapid adoption of Advanced Driver-Assistance Systems (ADAS) and the development of autonomous vehicles. Modern vehicles increasingly incorporate multiple GNSS receivers for navigation, emergency call systems (eCall), and telematics. The shift towards autonomous driving levels 2 and 3 requires centimeter-level accuracy, which is achieved through dual-frequency, multi-constellation GNSS chips combined with inertial navigation systems and real-time kinematic corrections. Global sales of vehicles equipped with ADAS features are growing at a compound annual growth rate of over 11%, directly correlating with increased GNSS chip integration. This technological evolution in the automotive industry is a significant catalyst for market expansion, demanding more sophisticated and reliable positioning solutions.

Government Initiatives and Modernization of Global Navigation Satellite Systems to Stimulate Growth

Continuous investment and modernization of global satellite constellations by governments worldwide enhance the accuracy, availability, and reliability of GNSS signals. The full operational capability of systems like Europe’s Galileo and China’s BeiDou-3 has created a more robust and precise global navigation infrastructure. These improvements allow GNSS chip manufacturers to develop products that leverage multiple constellations simultaneously, significantly improving performance in challenging environments like urban canyons. National initiatives promoting smart cities and intelligent transportation systems further mandate the deployment of GNSS technology in public infrastructure. This sustained governmental support and infrastructure development create a stable, long-term foundation for market growth, encouraging innovation and adoption across various sectors.

MARKET CHALLENGES

Signal Vulnerability and Interference Issues to Impede Reliable Performance

GNSS signals are inherently weak when reaching Earth’s surface, making them susceptible to various forms of interference, including jamming, spoofing, and natural obstacles. Urban canyon environments, where signals are reflected or blocked by tall buildings, can cause significant positioning errors exceeding 30 meters. Multipath interference remains a persistent technical challenge that affects location accuracy in densely built areas. Additionally, intentional jamming and spoofing activities pose security risks for critical applications in aviation, maritime, and defense sectors. These vulnerabilities necessitate the development of sophisticated anti-jamming technologies and alternative positioning systems, increasing system complexity and cost.

Other Challenges

Power Consumption Constraints

The increasing demand for always-on location services in battery-powered devices creates significant power management challenges. High-precision GNSS operation can substantially reduce battery life in smartphones, wearables, and IoT devices. Designing chips that balance accuracy with power efficiency remains a critical engineering hurdle, particularly for applications requiring continuous tracking.

Technical Complexity of Multi-Constellation Support

Supporting multiple satellite constellations (GPS, GLONASS, Galileo, BeiDou) increases design complexity and manufacturing costs. The need for broader frequency coverage and more sophisticated signal processing algorithms challenges manufacturers to maintain cost-effectiveness while delivering enhanced performance.

MARKET RESTRAINTS

High Development Costs and Intense Price Competition to Limit Profit Margins

The GNSS chip market faces significant pressure from relentless price competition, particularly in consumer electronics segments where cost sensitivity is extreme. Research and development expenses for advanced chips supporting multiple frequencies and constellations can exceed several million dollars per design cycle. Meanwhile, average selling prices for standard precision chips have declined consistently, dropping approximately 7-10% annually due to fierce competition among major manufacturers. This price erosion makes it challenging to achieve satisfactory returns on investment, especially for smaller players lacking economies of scale. The market dominance of a few large semiconductor companies further intensifies pricing pressures, creating barriers for new entrants and limiting innovation funding for specialized applications.

Regulatory Compliance and Certification Requirements to Slow Market Entry

GNSS chips used in safety-critical applications such as aviation, automotive, and maritime navigation must undergo rigorous certification processes that can take several years and cost millions of dollars. Compliance with various international standards and regional regulations adds complexity to product development and time-to-market. The certification requirements differ across geographical markets and application segments, forcing manufacturers to maintain multiple product variations and navigate complex regulatory landscapes. These compliance burdens particularly affect high-precision chips destined for automotive and aerospace applications, where failure rates during certification can reach 20-30%, significantly impacting development timelines and costs.

Dependence on Consumer Electronics Market to Create Volatility Risks

Approximately 70% of GNSS chip demand originates from the consumer electronics sector, primarily smartphones and tablets. This heavy dependence makes the market vulnerable to fluctuations in consumer spending patterns and device replacement cycles. Economic downturns can rapidly decrease demand, as evidenced during recent global economic challenges when smartphone sales declined by over 10% in certain quarters. The cyclical nature of consumer electronics manufacturing, with its inventory adjustments and production cuts, directly impacts GNSS chip orders and manufacturing volumes. This volatility makes long-term planning and capacity investment challenging for chip manufacturers, restraining steady market growth.

MARKET OPPORTUNITIES

Emergence of Precision Applications in Agriculture and Construction to Open New Revenue Streams

The agriculture and construction sectors present substantial growth opportunities for high-precision GNSS chips, driven by increasing automation and efficiency demands. Precision agriculture applications, including automated steering and yield monitoring, require centimeter-level accuracy provided by dual-frequency GNSS receivers with correction services. The global precision farming market is expanding at approximately 12% annually, creating consistent demand for specialized positioning solutions. Similarly, the construction industry increasingly adopts machine control and site mapping technologies that depend on high-accuracy GNSS. These industrial applications typically command higher profit margins than consumer markets and show less sensitivity to economic cycles, offering manufacturers more stable and profitable business opportunities.

Integration with Complementary Technologies to Enhance System Value

The convergence of GNSS with other positioning technologies creates significant opportunities for enhanced system solutions. Integration with inertial measurement units (IMUs), cellular network positioning, and low Earth orbit satellite signals provides seamless positioning in challenging environments where GNSS alone proves inadequate. The development of hybrid positioning systems that maintain accuracy during GN signal outages addresses a critical market need across various applications. Additionally, the combination of GNSS with sensor fusion algorithms and artificial intelligence enables context-aware positioning that adapts to environmental conditions. These integrated solutions command premium pricing and create differentiation opportunities in increasingly competitive markets.

Expansion of Location-Based Services and Augmented Reality to Drive Innovation

The rapid growth of location-based services and augmented reality applications creates new requirements for precise, low-latency positioning. Applications ranging from immersive gaming to enterprise navigation solutions demand better location accuracy than standard GNSS can provide. This market segment drives innovation in crowd-sourced positioning, 3D mapping, and real-time kinematic solutions. The augmented reality market, projected to exceed $50 billion by 2026, particularly depends on precise spatial awareness that integrates GNSS with other sensors. These emerging applications encourage development of next-generation chips with improved accuracy, lower power consumption, and faster time-to-first-fix capabilities, opening new market segments beyond traditional navigation.

GNSS CHIP MARKET TRENDS

Integration of Multi-Constellation Support to Emerge as a Dominant Trend

The GNSS chip market is undergoing a significant transformation driven by the widespread adoption of multi-constellation support. Modern chipsets are increasingly designed to process signals from multiple global navigation satellite systems simultaneously, including GPS (USA), GLONASS (Russia), Galileo (EU), and BeiDou (China). This technological evolution enhances positioning accuracy, reliability, and availability, particularly in challenging urban canyons or dense foliage environments where signals from a single constellation may be obstructed. The ability to leverage over 120 satellites from these combined systems drastically reduces time-to-first-fix and improves overall performance. This trend is critical for advanced applications like autonomous vehicles and precision agriculture, where centimeter-level accuracy is not just a luxury but a necessity. The demand for such high-performance chips is reflected in their growing penetration, with multi-constellation chips now constituting a substantial portion of new device integrations, especially in the automotive and industrial sectors.

Other Trends

Proliferation of IoT and Connected Devices

The explosive growth of the Internet of Things (IoT) ecosystem is a primary catalyst for the GNSS chip market. Billions of new connected devices, from asset trackers and smart sensors to wearable health monitors, require efficient and low-power location capabilities. This has spurred demand for highly integrated, power-optimized GNSS chips that can operate for extended periods on small batteries. The market has responded with innovations in chip design that significantly reduce power consumption, with some modern chipsets consuming less than 10 milliwatts during active tracking. This efficiency is paramount for applications like logistics and supply chain management, where real-time asset visibility is crucial for operational optimization. The convergence of GNSS with other wireless technologies like LTE-M and NB-IoT in single-chip solutions is further accelerating this adoption, creating a robust pipeline for future market expansion.

Advancements in High-Accuracy Positioning Technologies

A pivotal trend shaping the market is the rapid advancement and commercialization of high-accuracy positioning technologies. While standard precision chips dominate consumer applications like smartphones, there is a surging demand for high-precision GNSS chips capable of delivering centimeter-level accuracy. This demand is fueled by the automation of machinery in agriculture, construction, and maritime applications. Technologies such as Real-Time Kinematic (RTK) and Precise Point Positioning (PPP), once reserved for specialized survey equipment, are now being miniaturized and integrated into mass-market chipsets. The development of dedicated satellite-based augmentation systems (SBAS) and correction services has made this high accuracy more accessible and affordable. Furthermore, the integration of inertial measurement units (IMUs) with GNSS chips provides resilient positioning solutions that continue to function accurately even during temporary GNSS signal outages, which is a critical requirement for the safety systems of autonomous vehicles and drones.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Focus on Innovation and Strategic Alliances to Maintain Dominance

The global GNSS chip market exhibits a semi-consolidated structure, dominated by a handful of major semiconductor and technology firms, while numerous smaller players compete in niche segments. Qualcomm Incorporated stands as the unequivocal market leader, primarily due to its integration of GNSS technology into its widely adopted Snapdragon platforms for smartphones and IoT devices. Its expansive global footprint and deep relationships with mobile OEMs afford it a significant competitive edge.

Broadcom Inc. and MediaTek Inc. also command substantial market shares, collectively holding a notable portion of the global revenue. Their growth is largely driven by robust demand from the consumer electronics sector, particularly smartphones, which remains the largest application segment. These companies continuously invest in developing more power-efficient and highly accurate multi-constellation chipsets to cater to evolving consumer and industrial requirements.

Furthermore, these leading players are aggressively pursuing growth through strategic initiatives, including geographical expansion into high-growth markets like Asia-Pacific and the launch of next-generation products supporting emerging signals like Galileo and BeiDou. Such moves are anticipated to further solidify their market positions throughout the forecast period.

Meanwhile, specialized players like u-blox Holding AG and STMicroelectronics N.V. are strengthening their presence by focusing on high-precision applications for automotive, industrial, and automotive markets. Their strategy involves significant R&D investments in dual-frequency technology and strategic partnerships with automotive Tier-1 suppliers and industrial automation companies, ensuring their relevance and growth in an increasingly competitive and technologically advanced landscape.

List of Key GNSS Chip Companies Profiled

- Qualcomm Incorporated (U.S.)

- Broadcom Inc. (U.S.)

- MediaTek Inc. (Taiwan)

- u-blox Holding AG (Switzerland)

- STMicroelectronics N.V. (Switzerland)

- Intel Corporation (U.S.)

- Furuno Electric Co., Ltd. (Japan)

- Unicore Communications, Inc. (China)

- Hexagon AB (Sweden)

Segment Analysis:

By Type

Standard Precision GNSS Chips Segment Dominates the Market Due to High Volume Adoption in Consumer Electronics

The market is segmented based on type into:

- High Precision GNSS Chips

- Standard Precision GNSS Chips

By Application

Smartphones Segment Leads Due to Pervasive Integration for Location-Based Services and Navigation

The market is segmented based on application into:

- Smartphones

- Tablets

- Personal Navigation Devices

- In-Vehicle Systems

- Wearable Devices

- Digital Cameras

- Others

By End User

Consumer Electronics Represents the Largest End-User Segment Driven by Mass-Market Device Proliferation

The market is segmented based on end user into:

- Consumer Electronics

- Automotive

- Aviation & Marine

- Agriculture

- Surveying & Mapping

- Defense & Government

- Others

By Constellation Support

Multi-Constellation Chips Gain Traction for Enhanced Accuracy and Reliability Across Diverse Geographic Regions

The market is segmented based on constellation support into:

- GPS-only Chips

- Multi-Constellation Chips

- Subtypes: GPS + GLONASS, GPS + Galileo, GPS + BeiDou, and others

Regional Analysis: GNSS Chip Market

Asia-Pacific

The Asia-Pacific region is the dominant force in the global GNSS chip market, accounting for approximately 45% of the total market share, with China being the single largest consumer. This leadership is fueled by the region’s massive consumer electronics manufacturing base, particularly in smartphones, tablets, and wearable devices. The proliferation of affordable smartphones from manufacturers like Xiaomi, Oppo, and Samsung, which integrate standard precision GNSS chips for location services and navigation, is a primary driver. Furthermore, significant government investment in national satellite systems, most notably China’s BeiDou, has created a robust and self-reliant infrastructure, fostering domestic chip development and adoption. While cost sensitivity keeps standard precision chips as the mainstream choice, there is a growing, albeit nascent, demand for high-precision chips driven by advancements in automotive ADAS, precision agriculture, and drone applications. The region’s rapid urbanization and expanding logistics networks continue to present substantial growth opportunities for GNSS technology integration.

North America

North America represents a mature and technologically advanced market for GNSS chips, characterized by high adoption rates of cutting-edge applications. The region is a hub for innovation, largely driven by key players like Qualcomm and Broadcom who are headquartered there. Demand is heavily influenced by the automotive sector’s integration of advanced driver-assistance systems (ADAS) and the development of autonomous vehicles, which require high-precision, multi-constellation chips for reliable positioning. Furthermore, the strong presence of major tech companies fuels demand in smartphones and wearable devices. The region benefits from the well-established GPS constellation and augmentation systems like WAAS, ensuring high service reliability. While consumer electronics drive volume, the higher-value, high-precision segments for automotive, aerospace, and surveying applications contribute significantly to revenue, making North America a critical market for technological advancement and premium product development.

Europe

Europe maintains a strong position in the GNSS chip market, underpinned by a robust automotive industry and strict regulatory frameworks promoting technological standards. The region’s focus is on high-integrity applications, with the automotive sector being a major consumer of chips for telematics, emergency call systems (eCall), and evolving autonomous driving functionalities. The full operational capability of the EU’s Galileo system provides a strategic advantage, offering improved accuracy and authentication services compared to other constellations, which European chip designers and manufacturers are keen to leverage. This focus on sovereignty and precision drives innovation in chip design towards dual-frequency and multi-constellation support. Environmental and safety regulations also act as key market drivers, mandating the use of GNSS in various transport and logistics applications. The market is characterized by a balanced demand between consumer electronics and high-value industrial uses.

South America

The South American market for GNSS chips is in a growth phase, presenting significant potential amidst economic challenges. The primary demand stems from the consumer electronics segment, particularly smartphones, as mobile penetration continues to increase across the region. Countries like Brazil and Argentina are seeing gradual adoption in automotive applications for basic navigation and fleet management services. However, economic volatility often constrains investment in more advanced, high-precision applications found in agriculture or construction. The lack of a regional satellite constellation means the market is entirely dependent on global systems like GPS and Galileo. While the long-term outlook is positive due to infrastructure development needs and digitalization trends, the current market is price-sensitive, with growth being steady rather than explosive.

Middle East & Africa

The Middle East and Africa region is an emerging market for GNSS chips, with growth prospects tied to infrastructure development and economic diversification efforts. In the Middle East, nations like the UAE, Israel, and Saudi Arabia are investing heavily in smart city initiatives, autonomous transportation projects, and construction, which are beginning to generate demand for high-precision positioning solutions. The African continent shows potential largely within the consumer mobile device segment and basic fleet management for logistics and transportation services. However, the widespread adoption of advanced applications is hindered by infrastructural limitations and less mature regulatory environments. The market is nascent but holds long-term promise as digital transformation and urban planning projects gain momentum across the region.

Report Scope

This market research report provides a comprehensive analysis of the global GNSS Chip market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global GNSS Chip Market?

-> GSS Chip Market wNas valued at 2800 million in 2024 and is projected to reach US$ 3986 million by 2032, at a CAGR of 5.3% during the forecast period.

Which key companies operate in Global GNSS Chip Market?

-> Key players include Qualcomm, Broadcom, Mediatek, U-blox, STMicroelectronics, Intel, and Furuno Electric, among others. The top five manufacturers collectively hold approximately 60% of the global market share.

What are the key growth drivers?

-> Key growth drivers include increasing demand for location-based services, proliferation of IoT devices, advancements in autonomous vehicle technology, and government investments in global navigation satellite infrastructure.

Which region dominates the market?

-> Asia-Pacific dominates the market with approximately 45% share, primarily driven by China’s significant market presence, followed by Europe and North America which together account for about 30% of the global market.

What are the emerging trends?

-> Emerging trends include integration of multi-constellation support (GPS, Galileo, BeiDou, GLONASS), development of low-power chips for wearable devices, advancement in high-precision positioning for autonomous systems, and miniaturization of chip designs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...